- Home

- »

- Next Generation Technologies

- »

-

5G Services Market Size, Share & Trends Report, 2026-2033GVR Report cover

![5G Services Market (2026 - 2033)Report]()

5G Services Market (2026 - 2033)

Size, Share & Trends Analysis Report By Communication Type (FWA, eMBB, uRLLC, mMTC), By Vertical (Consumer, Enterprises), By Region (North America, Europe, Asia Pacific, Latin America, Middle East And Africa), And Segment Forecasts

Market Size, 2025

$196.4BMarket Estimate, 2026

$315.8BMarket Forecast, 2033

$1,874.1BCAGR, 2026–2033

29.0%5G Services Market Summary

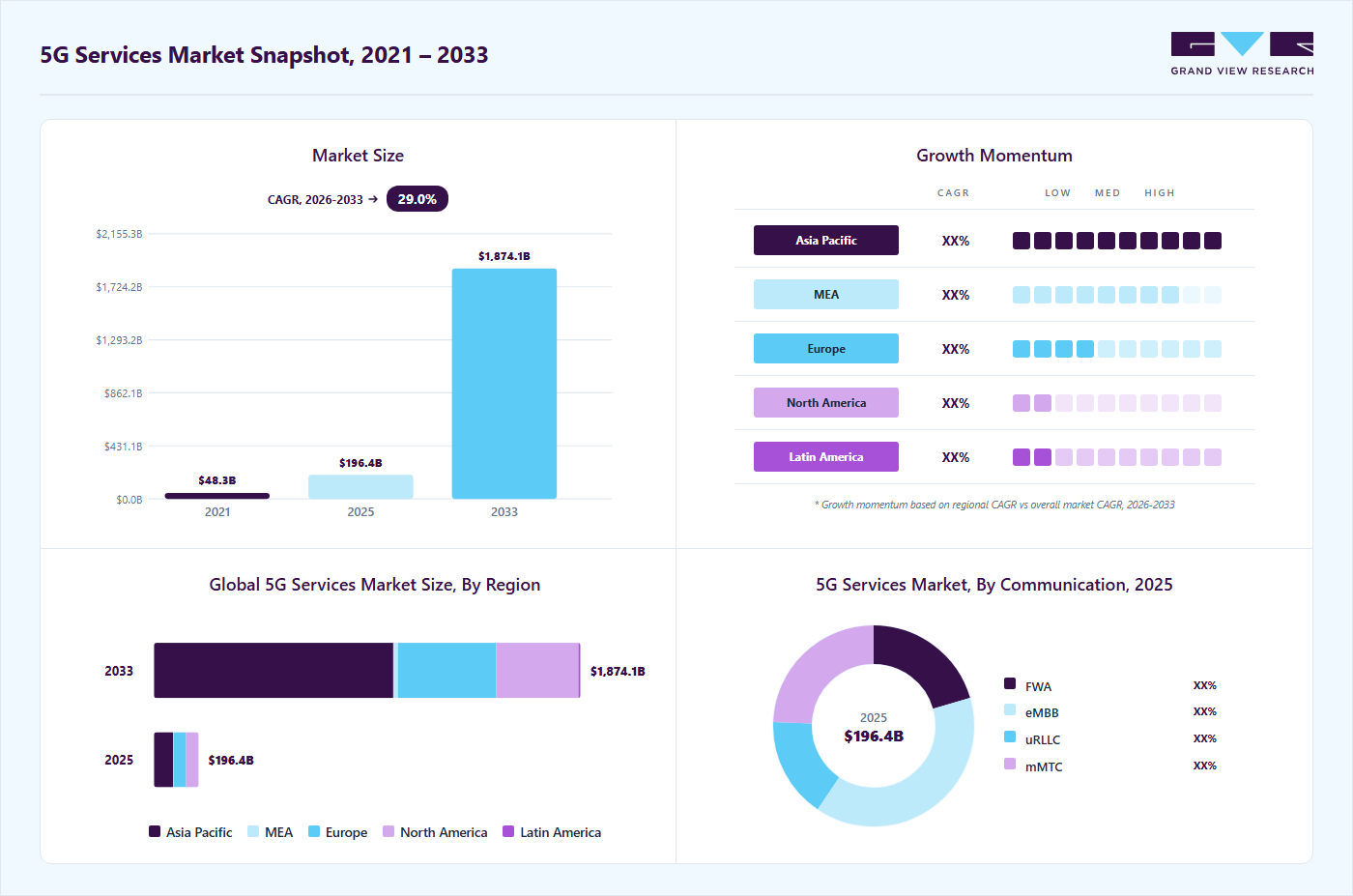

The global 5G services market size was valued at USD 196.4 billion in 2025 and is projected to grow from USD 315.8 billion in 2026 to USD 1,874.1 billion by 2033, at a CAGR of 29.0% from 2026 to 2033. Asia Pacific held the largest revenue share of 42.7% of the global market in 2025.The market growth is attributed to rising demand for high-speed, low-latency, and reliable connectivity, which is critical for data-intensive applications such as cloud computing, ultra-HD streaming, real-time communication, and emerging technologies that require uninterrupted network performance.

Key Market Trends & Insights

- By communication type: Enhanced mobile broadband (eMBB) segment held the largest market share of 38.8% in 2025.

- By vertical: Enterprises segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (42.7% market share, 2025)

- By Country: China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 196.4 Billion

- Estimated market size in 2026: USD 315.8 Billion

- Projected market size by 2033: USD 1,874.1 Billion

- CAGR (2026–2033): 29.0%

Additionally, increased investments in 5G infrastructure by telecom operators and governments are accelerating network deployment and expansion. These investments support the large-scale rollout of advanced network architectures and enable next-generation applications in sectors such as healthcare, manufacturing, transportation, and smart cities.

The growth of the 5G services industry is further attributed to the rapid expansion of the Internet of Things (IoT) ecosystem. As more connected devices are deployed across industries such as smart homes, industrial automation, agriculture, and logistics, there is an increasing need for large-scale connectivity and efficient data exchange, which 5G networks effectively enable. Moreover, the growing use of advanced digital applications such as augmented reality, virtual reality, and immersive gaming is increasing demand for 5G services. These applications require ultra-low latency and high bandwidth, making 5G essential for next-generation digital services in both consumer and enterprise markets.

")

Technological advancements play a crucial role in shaping the growth of the 5G services market by enabling faster, more reliable, and highly efficient network performance. The evolution from non-standalone (NSA) to standalone (SA) 5G architecture is significantly improving latency and network slicing capabilities. Additionally, innovations such as edge computing, massive MIMO, beamforming, and network virtualization are increasing data processing speed and spectrum efficiency. Moreover, the development of 5G-Advanced technologies is expanding support for ultra-reliable low-latency communications (URLLC) and massive machine-type communications (mMTC), thereby unlocking new opportunities across industries such as autonomous vehicles, smart cities, industrial automation, and immersive digital applications.

Governments worldwide are advancing 5G development and adoption through policy support, innovation programs, and ecosystem initiatives. For instance, in February 2026, the Government of India announced several measures to promote 5G application development, including the establishment of 100 5G Use Case Labs in educational institutions. These labs aim to foster 5G-enabled applications that integrate emerging technologies such as Artificial Intelligence (AI) and blockchain. Additionally, the 5G Innovation Hackathon 2025 was also launched to support the creation of solutions using 5G and advanced digital technologies. These initiatives aim to strengthen collaboration between academia and industry, encourage startup participation, and accelerate the development of socio-economic use cases in healthcare, education, agriculture, and digital services. These efforts support the long-term growth of the 5G ecosystem.

The market is shaped by evolving government policies and data governance requirements. Strict data privacy and cybersecurity guidelines are enforced to ensure safe and reliable operations. For instance, in 2025, the UK telecom regulators and government agencies strengthened 5G security compliance requirements under their updated Telecommunications (Security) framework, mandating stricter controls on high-risk vendors, enhanced network monitoring, and improved resilience standards for 5G infrastructure to reduce cybersecurity vulnerabilities across national networks. Furthermore, governments also encourage fair competition and open access to prevent monopolies and foster innovation. Global standards set by organizations such as the International Telecommunication Union (ITU) and 3rd Generation Partnership Project (3GPP) promote interoperability and consistent 5G deployment worldwide.

The 5G services market faces several challenges, notably infrastructure complexity and security risks. Deploying 5G networks is costly and complex, requiring dense small-cell networks, extensive fiber backhaul, and ongoing upgrades. These factors increase capital expenditure for telecom operators and delay deployment in less profitable or rural areas. Cybersecurity and data privacy risks are also significant concerns. The virtualized, software-driven architecture of 5G networks expands the attack surface, increasing vulnerability to cyber threats and network manipulation. These restraints may obstruct the expansion and adoption of 5G services across regions.

Market Dynamics

The growing use of edge computing and low-latency applications is accelerating the 5G services market, as industries demand real-time data processing and rapid response. By processing data closer to its source rather than relying solely on centralized cloud infrastructure, 5G networks significantly reduce latency and enhance performance. This is critical for advanced applications such as autonomous vehicles, industrial automation, remote healthcare, and smart manufacturing, where even brief delays can affect results.

In the manufacturing sector, companies such as Siemens AG, Nokia, and Ericsson are implementing edge-enabled 5G networks to support predictive maintenance and real-time production monitoring. Machinery sensors send continuous data for edge processing, allowing immediate fault detection and reduced downtime. Similarly, in autonomous driving, 5G-powered edge computing enables vehicles to process road data, traffic signals, and environmental inputs in real time, enhancing safety and decision-making speed.

High operational and energy costs significantly restrain 5G network deployment, mainly due to the substantial capital required for infrastructure. Telecom operators must invest in dense small-cell networks, fiber backhaul, spectrum acquisition, and ongoing technology upgrades to meet 5G standards. These factors raise deployment costs above those of previous mobile network generations, thus increasing financial pressure on service providers, particularly in competitive, price-sensitive markets.

Beyond initial investments, ongoing operational and energy expenses further limit profitability in the 5G services market. Maintaining numerous network nodes, including energy-intensive base stations and edge infrastructure, increases electricity and maintenance costs. These challenges are more pronounced in rural and low-traffic areas, where slower returns often delay or restrict network expansion. Telecom operators must therefore balance service quality improvements with effective cost management.

The expansion of private 5G networks offers significant opportunities in the 5G services market, as enterprises seek secure and high-performance connectivity. Private 5G enables organizations to tailor network architecture to their operational requirements, providing reliable, low-latency communication and stronger data security. This is particularly valuable in settings where consistent connectivity supports automation, robotics, and real-time decision-making.

Companies are increasingly collaborating and deploying private 5G networks to enhance industrial efficiency and accelerate digital transformation. For instance, in February 2026, NTT DATA and Ericsson announced a partnership to scale private 5G and physical AI solutions for enterprises, delivering private 5G as a fully managed global service with consistent security and operational standards across regions. The collaboration also integrates edge AI and physical AI capabilities directly into enterprise connectivity infrastructure, enabling real-time autonomous decision-making.

Market Concentration & Characteristics

The 5G services market is fragmented, involving global, regional, and local telecom operators, private network providers, infrastructure vendors, and digital service enablers. Both multinational companies and smaller regional players compete, often serving specific geographic or enterprise needs. This fragmentation results from varying spectrum allocation policies, regulatory frameworks, auction processes, and national telecom strategies. Differences in infrastructure maturity and investment capacity across regions also contribute to the market’s complex structure.

The market is dynamic, capital-intensive, and ecosystem-driven, demanding ongoing investment in infrastructure, spectrum, and advanced technologies such as network slicing and edge computing. Strong interdependencies among telecom operators, equipment vendors, cloud providers, and enterprises create a collaborative environment. The growing adoption of private 5G networks and enterprise-specific solutions is further increasing fragmentation and diversifying competition across industries.

Communication Type Insights

The enhanced mobile broadband (eMBB) segment accounted for the largest share of 38.8% in 2025. The high share is attributed to the continued prioritization of high-speed data services by telecom operators, driven by rising consumer demand for data-intensive applications such as ultra-high-definition (UHD) video streaming, cloud gaming, augmented and virtual reality (AR/VR), and seamless video conferencing. The rapid expansion of 5G standalone networks has further enhanced eMBB capabilities, delivering higher bandwidth, lower latency, and more reliable connectivity in urban and semi-urban areas. Furthermore, rising smartphone adoption and growth in remote work and digital content consumption are further strengthening the segment. Moreover, ongoing network densification and spectrum improvements continue to enhance service quality and support the strong growth of the eMBB segment.

The massive machine-type communications (mMTC) segment is expected to grow at the fastest CAGR in the forecast period. The segment's growth is driven by the rapid expansion of the Internet of Things (IoT) ecosystem and the increasing deployment of connected devices across industries. mMTC supports high-density device connectivity with low power consumption, making it well-suited for smart cities, smart buildings, industrial automation, agriculture monitoring, and utility management. Advancements in 5G standalone (SA) networks are improving efficiency and scalability, enabling seamless connectivity for millions of devices within a single network. Moreover, growing investments in digital infrastructure and the adoption of sensor-based technologies and real-time data monitoring are further accelerating segment growth.

Vertical Insights

The enterprise segment dominated the 5G services market in 2025, attributed to rising demand for ultra-fast connectivity, low latency, and high network reliability in enterprise operations. Advancements in 5G standalone networks enable enterprises to leverage capabilities such as network slicing, edge computing, and private 5G networks, providing secure, tailored connectivity. These features are especially valuable in manufacturing, logistics, healthcare, and financial services, where real-time data processing and automation are essential. Additionally, the rising adoption of Industry 4.0 technologies, including IoT, artificial intelligence, and cloud computing, is accelerating demand for 5G in enterprises. Applications such as remote monitoring, predictive maintenance, autonomous operations, and real-time analytics are becoming more efficient and reliable, thereby improving productivity and operational efficiency.

The consumer segment is expected to grow at a significant CAGR from 2026 to 2033. The growth is propelled by rapid commercial 5G rollouts and more affordable 5G-enabled devices in key markets, including the U.S., China, Japan, Germany, and South Korea. The increasing demand for high-speed connectivity, seamless video streaming, cloud gaming, and immersive digital experiences is accelerating adoption. Further, ongoing improvements in network coverage and the shift to 5G standalone infrastructure are enhancing the user experience, with lower latency and greater reliability than 4G LTE. Moreover, promotional data plans and bundled service offerings from telecom operators are also supporting strong expansion in the consumer segment.

Regional Insights

The Asia Pacific 5G services market held the largest market share of 42.7% in 2025. The region’s dominance is driven by large-scale 5G deployment initiatives, strong government support for digital infrastructure, and the rapid commercialization of advanced connectivity services across key economies such as China, Japan, South Korea, and India. Major telecom operators, including China Mobile Ltd., China Telecom Corporation Ltd., SK Telecom Co., Ltd., and KT Corp., are investing to expand 5G network coverage and upgrade to 5G-Advanced capabilities. For instance, in May 2025, China Mobile Ltd. announced a USD 1.4 billion upgrade plan as part of a broader USD 3 billion 5G-Advanced (5G-A) rollout in China, aimed at improving network performance and accelerating the deployment of next-generation mobile services across multiple provinces. The growing adoption of industrial IoT, cloud computing, and AI-driven services is further strengthening the demand for high-speed and low-latency connectivity.

China 5G Services Market Trends

The China 5G services market held a dominant position in the market in 2025. The market continues to mature, driving broader economic value and increased connectivity. Further, rapid 5G adoption in the country is propelled by the swift deployment of networks and the development of a mature device ecosystem.

The 5G services market in India is expected to grow rapidly over the forecast period. Expanding digital infrastructure, along with growing adoption of cloud computing and AI-enabled applications, is supporting market expansion. Additionally, strong government initiatives promoting digital transformation and widespread availability of affordable 5G data plans are expected to significantly boost subscriber growth and enhance overall market penetration in the coming years.

North America 5G Services Market Trends

The North America 5G services industry is anticipated to grow at a significant CAGR of 23.3% during the forecast period. The region’s growth is driven by rapid enterprise digital transformation and increasing adoption of advanced technologies such as IoT, artificial intelligence, robotics, and cloud computing. These technologies require ultra-reliable and low-latency connectivity, which is enabled more effectively by 5G networks than by legacy 4G infrastructure. Enterprises across the region are increasingly expanding 5G to support real-time data processing, industrial automation, remote monitoring, and mission-critical operations, particularly in sectors such as manufacturing, logistics, healthcare, and retail. For instance, in March 2026, AT&T, Inc. expanded its 5G standalone (SA) capabilities in the U.S. to strengthen enterprise-focused solutions, including private 5G networks and edge computing services, enabling businesses to deploy more efficient and automated operations. As a result, growing enterprise reliance on advanced connectivity solutions is significantly accelerating the adoption of 5G services across North America.

The U.S. 5G services industry is expected to grow rapidly over the forecast period. The growth is attributed to the rising demand for high-speed, low-latency communication services, which is supported by the widespread adoption of data-intensive applications such as cloud computing, video streaming, IoT-based solutions, and immersive digital technologies. Additionally, strong enterprise adoption of 5G-enabled services for automation, real-time analytics, and remote operations across various industries is further accelerating market growth. Moreover, continuous technological advancements and the ongoing transition toward 5G standalone networks are also strengthening market expansion in the country.

Europe 5G Services Market Trends

The Europe 5G services industry was identified as a lucrative region in 2025. Telecom operators across the region are actively expanding 5G network coverage to deliver high-speed, reliable connectivity and enable the adoption of next-generation digital services. Prominent players in the region, such as Vodafone Group Plc, Deutsche Telekom AG, and Telefónica, S.A., are at the forefront of large-scale 5G deployment initiatives across Europe. The increasing availability of 5G networks is supporting the growth of advanced applications such as IoT, smart manufacturing, autonomous mobility, and cloud-based enterprise solutions. Additionally, ongoing network modernization efforts and the transition toward 5G standalone architectures are further enhancing service capabilities, thereby significantly emphasizing market growth across the region.

The UK 5G services market is expected to grow rapidly in the coming years. Market growth is driven by the continuous expansion of 5G network infrastructure and the increasing availability of high-speed mobile connectivity across the country. According to Ofcom, in 2025, 5G coverage outside premises has reached between 94% and 97% of the UK population from at least one mobile network operator, reflecting strong progress in nationwide rollout and improved service accessibility. This expansion is further supported by the increasing deployment of 5G Standalone (SA) networks and rising mobile data consumption, both of which are strengthening overall network performance and capacity. Moreover, the growing availability of advanced connectivity is enabling the wider adoption of digital applications and supporting sustainable nationwide market growth.

The 5G services market in Germany held a substantial revenue share in 2025. The country’s focus on Industry 4.0 initiatives is driving the adoption of private 5G networks to support automation and real-time production monitoring in smart factories. Additionally, integration of 5G with edge computing and industrial IoT applications is further enabling efficient data processing and operational optimization, thereby supporting sustained market growth in Germany.

Key 5G Services Company Insights

Some of the key companies in the 5G services market include AT&T, Inc., China Mobile Limited, Verizon Communications Inc., Deutsche Telekom AG, and Vodafone Group Plc. Organizations are focusing on increasing customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

Deutsche Telekom AG is a telecommunications service provider in Germany. The company offers fixed-network/broadband, internet, mobile, and internet-based TV services and products for consumers, as well as information and communication technology solutions for corporate and business customers.

-

British Telecommunications plc is a connectivity service provider. It provides global businesses with connectivity, networking, and security solutions. The company’s customers span a wide range of segments, including consumer, business, and communication providers.

Key 5G Services Companies:

The following key companies have been profiled for this study on the 5G services market.

- AT&T, Inc.

- China Mobile Ltd.

- China Telecom Corporation Ltd.

- Bharti Airtel Limited

- Vodafone Group Plc

- Deutsche Telekom AG

- SK Telecom Co., Ltd.

- Verizon Communications, Inc.

- NTT DOCOMO

- T-Mobile USA, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: China Mobile Ltd.; Verizon Communications, Inc.; AT&T, Inc.; Vodafone Group Plc; Deutsche Telekom AG; NTT DOCOMO

- Large-scale 5G rollout and infrastructure expansion.

- Upgrading legacy networks to 5G SA/NSA.

- Strong focus on strategic partnerships and ecosystem building.

- Strong financial capacity and large subscriber base.

- Extensive network coverage and service reliability.

- Strong brand presence and bundled service offerings.

- High CAPEX and operational costs.

- Legacy infrastructure integration challenges.

Emerging Players: Bharti Airtel Limited; SK Telecom Co., Ltd.; T-Mobile USA, Inc.; China Telecom Corporation Ltd.

- Fast 5G deployment in urban markets.

- Focus on digital transformation and cloud-based networks.

- Strategic collaborations for technology access.

- Agile and fast adoption of new technologies.

- Competitive pricing and data-focused plans.

- Strong focus on innovation and enterprise use cases.

- Limited global scale compared to mature players

- Dependence on partnerships for advanced capabilities.

Recent Developments

-

In March 2026, Vodafone Idea Limited announced a major expansion of its 5G services to target coverage across around 90 cities, as part of its accelerated nationwide rollout strategy. The expansion is supported by strategic partnerships with global telecom equipment providers, including Telefonaktiebolaget LM Ericsson, Nokia Corporation, and Samsung, enabling the deployment of advanced network infrastructure and improved service quality. The initiative reflects the company’s focus on strengthening its 5G footprint, enhancing network capacity, and delivering high-speed connectivity to a wider user base across India.

-

In February 2025, Bharti Airtel Limited partnered with Telefonaktiebolaget LM Ericsson to deploy advanced 5G Core technology, marking a significant step in its transition to a full-scale 5G Standalone (SA) network in India. This collaboration builds on their 25-year relationship and aims to enhance Airtel's network capacity, enabling the delivery of innovative, differentiated services to millions of customers and enterprises. Ericsson's dual-mode 5G Core solutions will support Airtel in monetizing its network through features such as network slicing and API exposure, unlocking new use cases for consumers and businesses.

5G Services Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 196.4 billion

Estimated Market size in 2026

USD 315.8 bllion

Projected Market size by 2033

USD 1,874.1 billion

Growth rate

CAGR of 29.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Communication type, vertical, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Russia; Italy; Spain; China; Japan; India; South Korea; Brazil; Saudi Arabia; UAE; South Africa

Key companies profiled

AT&T, Inc.; China Mobile Ltd.; China Telecom Corporation Ltd.; Bharti Airtel Limited; Vodafone Group Plc; Deutsche Telekom AG; Verizon Communications, Inc.; T-Mobile USA, Inc.; NTT DOCOMO; SK Telecom Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global 5G Services Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global 5G services market report based on communication type, vertical, and region:

-

Communication Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Fixed Wireless Access (FWA)

-

Enhanced Mobile Broadband (eMBB)

-

Ultra-Reliable and Low-Latency Communications (uRLLC)

-

Massive Machine-Type Communications (mMTC)

-

-

Vertical Outlook (Revenue, USD Million, 2021 - 2033)

-

Consumer

-

Enterprises

-

Manufacturing

-

Public Safety

-

Healthcare & Social Work

-

Media & Entertainment

-

Energy & Utility

-

IT & Telecom

-

Transportation & Logistics

-

Aerospace & Defense

-

BFSI

-

Government

-

Retail

-

Mining

-

Oil & Gas

-

Agriculture

-

Construction

-

Real Estate

-

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Russia

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

5G Services Market Analysis

- Global and regional 5G adoption assessment.

- Spectrum allocation and regulatory landscape analysis.

- Network deployment and infrastructure evaluation.

- Identified high-growth regions and deployment hotspots.

- Supported strategic market entry decisions.

5G Use Case & Application Study

- Analysis of key 5G use cases such as IoT, AR/VR, autonomous systems, and smart cities.

- Enterprise vs consumer application segmentation.

- Private 5G network adoption trends.

- Enabled identification of high-value enterprise segments.

- Supported product and service innovation strategy.

Competitive Landscape Assessment

- Benchmarking of leading telecom operators and 5G infrastructure providers.

- Analysis of partnerships across telecom, cloud, and chipset ecosystems.

- Supported competitive intelligence development.

- Identified partnership and differentiation opportunities.

Frequently Asked Questions About This Report

Asia Pacific dominated with 42.7% market share in 2025.

Enterprise segment dominated the market in 2025, while consumer segment is expected to grow fastest.

The global 5G services market size was estimated at USD 196.4 billion in 2025 and is expected to reach USD 315.8 billion in 2026.

The global 5G service market is expected to grow at a compound annual growth rate of 29.0% from 2026 to 2033 to reach USD 1,874.1 billion by 2033.

The enhanced mobile broadband (eMBB) segment accounted for the largest share of 38.8% in 2025. The high share is attributed to the continued prioritization of high-speed data services by telecom operators, driven by rising consumer demand for data-intensive applications such as ultra-high-definition (UHD) video streaming, cloud gaming, augmented and virtual reality (AR/VR), and seamless video conferencing.

Some key players operating in the 5G services market include AT&T, Inc., China Mobile Ltd., China Telecom Corporation Ltd., Bharti Airtel Limited, Vodafone Group Plc, Deutsche Telekom AG, Verizon Communications, Inc., T-Mobile USA, Inc., NTT DOCOMO, SK Telecom Co., Ltd.

Key factors that are driving the 5G services market growth include rising demand for high-speed, low-latency, and reliable connectivity, which is critical for data-intensive applications such as cloud computing, ultra-HD streaming, real-time communication, and emerging technologies that require uninterrupted network performance.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.