- Home

- »

- Next Generation Technologies

- »

-

Collaborative Robot Market Size & Share Report, 2026-2033GVR Report cover

![Collaborative Robot Market (2026 - 2033)Report]()

Collaborative Robot Market (2026 - 2033)

Size, Share & Trends Analysis Report By Payload Capacity (Up to 5kg, Up to 10kg, Above 10kg), By Application (Assembly, Pick & Place, Handling), By Industry Vertical, By Region, And Segment Forecasts

Market Size, 2025

$2.9BMarket Estimate, 2026

$4.0BMarket Forecast, 2033

$17.2BCAGR, 2026–2033

23.1%Collaborative Robot Market Summary

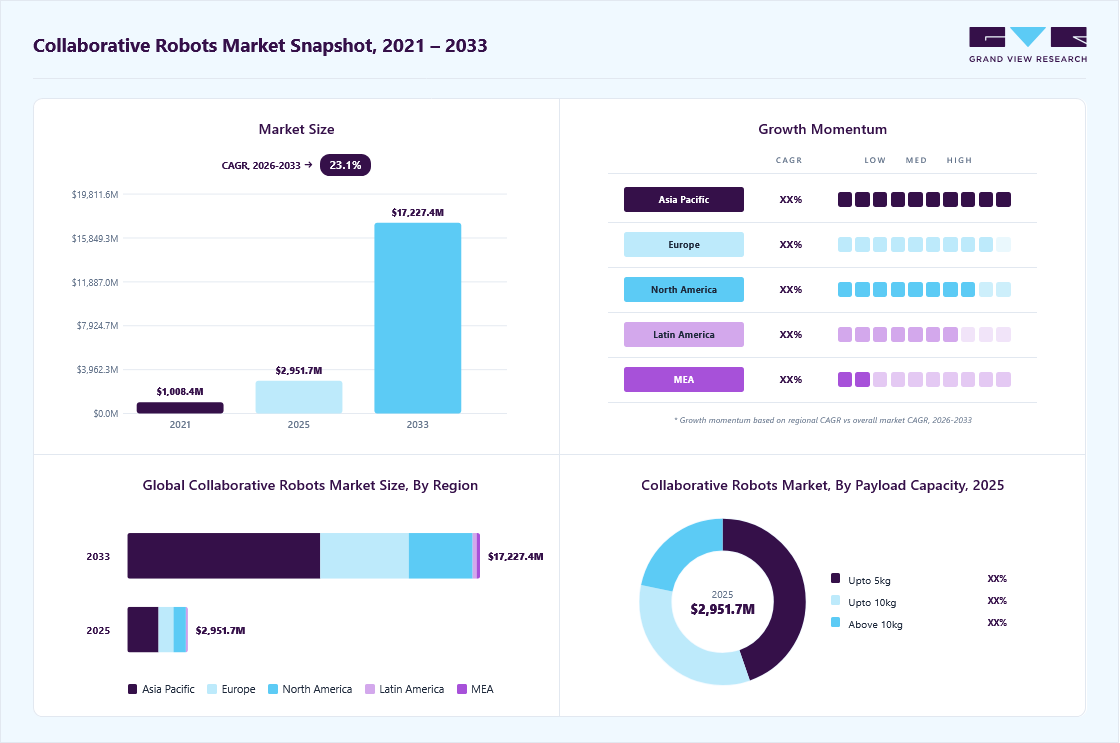

The global collaborative robot market size was valued at USD 2.9 billion in 2025 and is projected to grow from USD 4.0 billion in 2026 to USD 17.2 billion by 2033, at a CAGR of 23.1% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 51.0% in 2025. The market is primarily driven by the accelerating deployment of Industry 4.0 technologies, the growing need to address labor shortages and rising operational costs in industrial operations, and the expanding use of collaborative robot for precision assembly.

Key Market Trends & Insights

- By payload capacity: Up to 5kg segment held the largest market share of 44.0% in 2025.

- By application: Assembly segment held the largest market share of 23.0% in 2025.

- By industry vertical: Automotive segment held the largest market share of 25.0% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (51.0% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 2.9 Billion

- Estimated market size in 2026: USD 4.0 Billion

- Projected market size by 2033: USD 17.2 Billion

- CAGR (2026-2033): 23.1%

The growth of the collaborative robots market is driven by the rapid advancement of lightweight robotic arm designs, energy-efficient servo motors, and high-precision force and torque sensing technologies that enable safer human-robot interaction and improved operational flexibility. The adoption of ergonomically designed collaborative robots is accelerating as manufacturers, logistics operators, and healthcare providers seek flexible automation solutions to streamline repetitive tasks, reduce workplace injuries, and enhance productivity in dynamic production and service environments. The increasing integration of artificial intelligence, machine vision, and real-time data analytics technologies enhances task adaptability, autonomous decision-making, and operational efficiency across collaborative robot deployments.The rapid advancement of compact robotic joint architectures, high-efficiency brushless servo motors, and integrated force and torque sensing technologies is significantly transforming automation capabilities by enabling safer, more responsive, energy-efficient collaborative robot designs. These innovations improve motion accuracy, payload flexibility, and operational reliability to support precise assembly, packaging, and inspection tasks in dynamic production environments. The integration of advanced actuator engineering and modular hardware platforms further supports scalable deployment in the collaborative robots market.

")

In addition, the market is witnessing growing momentum toward the adoption of collaborative robots as part of enterprise workforce augmentation and flexible manufacturing strategies designed to enhance operational continuity and productivity. Manufacturers are increasingly incorporating cobot-assisted workflows into assembly, machine tending, and material handling operations to address labor shortages and maintain consistent production output. This shift toward human-robot collaboration and adaptive automation environments is enabling companies to reduce downtime and strengthen workforce safety in the collaborative robot industry.

Moreover, the expansion of e-commerce fulfillment centers, warehouse automation systems, and high-mix low-volume production models is driving demand for versatile robotic automation solutions capable of rapid deployment. Industrial operators are increasingly investing in collaborative robots to support pick-and-place operations, palletizing, and inventory handling tasks, enabling faster order processing and improved supply chain responsiveness. This growing emphasis on logistics optimization, throughput efficiency, and real-time inventory management is strengthening the role of collaborative robot technologies in the market.

Furthermore, the rising deployment of collaborative robots in healthcare, electronics manufacturing, and food processing environments is reshaping application opportunities across the collaborative robot market. Healthcare providers, electronics producers, and food manufacturers are increasingly adopting hygienic, precision-controlled robotic systems for laboratory automation, micro-assembly, and safe handling of sensitive materials. This transition toward automated quality control and contamination-safe production processes positions collaborative robot manufacturers to meet the evolving demands for regulatory compliance, product consistency, and operational safety across highly regulated industries.

Payload Capacity Insights

The up to 5kg segment accounted for the largest market share of over 44% in 2025, owing to the increasing demand for compact, lightweight, and cost-efficient collaborative robots designed for precision handling and repetitive light-duty tasks. Manufacturers and small to medium-sized enterprises are prioritizing investments in low-payload collaborative robot systems to support assembly, pick-and-place, packaging, and quality inspection operations in electronics, healthcare, and consumer goods production environments. The expansion of flexible manufacturing models and growing emphasis on improving workplace safety are encouraging organizations to deploy collaborative robots with payload capacities up to 5 kg, driving the segmental growth in the collaborative robot market.

The above 10kg segment is expected to witness the fastest CAGR of over 24% from 2026 to 2033. This growth is driven by the increasing demand for heavy-duty material handling, palletizing, and machine tending operations. The growing emphasis on automating physically demanding tasks and improving load-handling efficiency is encouraging manufacturers to adopt high-payload collaborative robots. The continuous expansion of large-scale manufacturing and warehouse automation facilities and sensor-based collision detection systems is accelerating the deployment of collaborative robot with payload capacities above 10 kg, which is further expected to propel the segment’s growth in the coming years.

Application Insights

The assembly segment accounted for the largest market share of 23% in 2025, owing to the increasing demand for high-precision component alignment, consistent production quality, and flexible automation solutions in modern manufacturing environments. Industrial operators are prioritizing investments in collaborative robots to support repetitive assembly operations, reduce human error, and improve cycle time efficiency. The expansion of modular manufacturing systems, rising adoption of lean production practices, and growing emphasis on workforce safety are encouraging organizations to integrate collaborative robots into assembly workflows, thereby driving the segmental growth in the collaborative robot industry.

The gluing & welding segment is expected to register the fastest CAGR from 2026 to 2033. This growth can be attributed to the increasing demand for precise material bonding, uniform weld quality, and automated process control in high-volume manufacturing operations. The growing emphasis on improving structural integrity and reducing material waste is encouraging manufacturers to adopt collaborative robots equipped with advanced motion control and adaptive path planning technologies. The continuous advancement of robotic dispensing systems and sensor-enabled quality verification solutions is accelerating the deployment of collaborative robots for gluing and welding applications, supporting growth in the segment of the collaborative robot market.

Industry Vertical Insights

The automotive segment accounted for the largest market share of over 25% in 2025, owing to the increasing demand for high-precision assembly automation, consistent production quality, and flexible manufacturing solutions. Automotive manufacturers are prioritizing investments in collaborative robots to support welding assistance, component assembly, machine tending, and quality inspection operations. The expansion of electric vehicle manufacturing programs, production line modernization initiatives, and advanced robotics integration strategies is encouraging automakers to deploy collaborative robot systems to improve throughput efficiency, reduce production downtime, and enhance operational safety, thereby driving the segmental growth in the collaborative robots market.

The electronics segment is expected to register the fastest CAGR from 2026 to 2033. This growth is driven by the rapid miniaturization of electronic components, increasing demand for precision handling, and rising adoption of automation in semiconductor and consumer electronics manufacturing facilities. The growing emphasis on high-speed production cycles and defect reduction is encouraging manufacturers to adopt collaborative robots equipped with advanced vision systems and fine-motion control technologies. The continuous expansion of global electronics production capacity and the integration of intelligent automation solutions into printed circuit board (PCB) assembly are accelerating the deployment of collaborative robots, supporting growth in the segment of the market.

Regional Insights

The Asia Pacific collaborative robot market accounted for the largest revenue share of over 51% in 2025, driven by rapid industrialization, expansion of manufacturing hubs, and increasing adoption of cost-efficient automation technologies. The region is experiencing strong demand for collaborative robots across electronics, automotive, and e-commerce logistics sectors. The growing penetration of smart factories, rising labor shortages in key manufacturing economies, and increasing investments in robotics infrastructure are significantly enhancing market growth across the region.

Collaborative robots market in Japan is gaining traction owing to the country’s leadership in robotics innovation and increasing adoption of automation in aging workforce environments. The market is witnessing rising use of collaborative robots for precision assembly, inspection, and human-assist operations in high-tech manufacturing industries. The strong focus on integrating robotics with AI, machine vision, and advanced control systems is encouraging the development of highly efficient and compact collaborative robot solutions.

The China collaborative robots market is rapidly expanding, driven by large-scale industrial automation initiatives, strong government support for intelligent manufacturing, and the rapid growth of domestic robotics manufacturers. The country is witnessing increasing adoption of collaborative robots in electronics assembly, logistics, warehousing, and consumer goods production. The expansion of local manufacturing capabilities, cost advantages, and rising demand for flexible automation solutions are accelerating high-volume deployment of the collaborative robot industry across the country.

North America Collaborative Robot Market Trends

The North America collaborative robot market accounted for a revenue share of over 20% in 2025. The growth can be attributed to the strong presence of advanced automation solution providers, early adoption of human-machine collaboration technologies, and increasing labor cost pressures. The region is witnessing the rapid deployment of collaborative robots for assembly, material handling, and quality inspection tasks across automotive, electronics, and food processing industries. The expansion of smart manufacturing initiatives, integration of AI-powered robotics systems, and rising focus on workplace safety and productivity optimization are further strengthening market growth across North America.

U.S. Collaborative Robot Market Trends

The U.S. collaborative robot market held a dominant position with a share of over 87% in 2025, fueled by rising investments in industrial automation, workforce augmentation technologies, and flexible manufacturing systems. The growing demand for improving operational efficiency is encouraging the adoption of collaborative robots for repetitive and precision-based tasks. The presence of strong venture capital funding, rapid advancements in robotic software and vision systems, and the expanding ecosystem of robotics startups and system integrators are contributing to sustained growth of the collaborative robot industry in the country.

Europe Collaborative Robot Market Trends

The Europe collaborative robot market is expected to grow at a significant CAGR of over 23% from 2026 to 2033, driven by increasing adoption of Industry 4.0 initiatives and workforce modernization programs. The region is experiencing rising demand for collaborative automation solutions that enhance flexibility, precision, and efficiency in complex production environments. The integration of advanced sensors, AI-driven control systems, and strict regulatory emphasis on workplace safety and ergonomics is supporting improved operational efficiency and widespread adoption of collaborative robots.

Collaborative robot industry in the UK is expected to grow significantly in the coming years, driven by the increasing adoption of automation across small and medium-sized enterprises (SMEs) and the expansion of smart manufacturing ecosystems. Rising investments in robotics research, innovation hubs, and industrial digitalization initiatives are fostering the development of cost-effective and easy-to-deploy collaborative robots. The growing focus on addressing labor shortages and enhancing productivity in sectors such as food processing, logistics, and healthcare is further boosting demand in the country.

The Germany collaborative robots market is fueled by the country’s strong focus on advanced manufacturing, precision engineering, and industrial automation leadership. The market is witnessing increased adoption of collaborative robots for assembly line optimization, machine tending, and real-time quality control in automotive and industrial equipment manufacturing. The emphasis on high production efficiency, integration of cyber-physical systems, and continuous innovation in industrial robotics is accelerating the deployment of high-performance collaborative robot solutions.

Key Collaborative Robot Company Insights

Some of the key players operating in the market include ABB Group and Fanuc Corporation.

-

ABB Group is a provider of advanced industrial automation and robotics solutions, delivering a comprehensive portfolio of collaborative robots designed for assembly, material handling, machine tending, and quality inspection applications across automotive, electronics, and logistics sectors. The company’s strong presence in industrial automation systems, digital manufacturing platforms, and AI-enabled robotics technologies has reinforced its leadership in the global collaborative robots market, enabling large-scale deployment of flexible and safety-compliant human-robot collaboration solutions in smart factory environments.

-

Fanuc Corporation is a leading manufacturer of industrial robotics and factory automation systems, offering high-performance collaborative robots equipped with advanced motion control, vision integration, and safety monitoring capabilities for precision manufacturing operations. The company’s extensive global manufacturing network, strong expertise in CNC systems and industrial robotics engineering, and continuous investment in intelligent automation technologies have strengthened its position in the collaborative robots market, supporting reliable and high-efficiency robotic deployment across diverse industrial production facilities.

AUBO (Beijing) Robotics Technology Co., Ltd. and Techman Robot Inc. are some of the emerging participants in the collaborative robot market.

-

AUBO (Beijing) Robotics Technology Co., Ltd. is an emerging provider of cost-effective collaborative robot industry, delivering lightweight and user-friendly robotic arms designed for small and medium-sized enterprises seeking flexible automation for assembly, packaging, and inspection operations. The company’s focus on modular robot design, simplified programming interfaces, and expanding global distribution partnerships has enhanced its competitiveness in the collaborative robots market, enabling broader adoption of collaborative automation technologies in developing manufacturing regions.

-

Techman Robot Inc. is an emerging developer of smart collaborative robots integrated with built-in machine vision systems and AI-enabled inspection capabilities designed for electronics manufacturing, logistics automation, and precision handling applications. The company’s specialization in vision-guided robotics, user-friendly automation platforms, and continuous innovation in intelligent sensing technologies has strengthened its presence in the collaborative robots industry, supporting the deployment of adaptive and data-driven robotic solutions.

Key Collaborative Robot Companies:

The following key companies have been profiled for this study on the collaborative robot market.

- ABB Group

- DENSO Corporation

- Epson America Inc.

- AUBO (BEIJING) ROBOTICS TECHNOLOGY CO., LTD

- Comau S.p.A.

- Energid Technologies Corporation

- Fanuc Corporation

- KUKA AG

- Rethink Robotics GmbH

- Robert Bosch GmbH

- Techman Robot Inc.

- Universal Robots

- Yaskawa Electric Corporation

- Precise Automation, Inc.

- MRK-Systems GmbH

Recent Developments

-

In March 2026, ABB Group announced a strategic collaboration with NVIDIA Corporation to develop AI-enabled autonomous robotic systems powered by simulation-based training platforms. The initiative focused on enabling robots to learn tasks virtually before deployment, reducing implementation costs and accelerating the adoption of intelligent collaborative robots across manufacturing and logistics environments.

-

In March 2026, MRK-Systems GmbH expanded its Assistance and Safety Assessment solutions portfolio by introducing enhanced risk assessment and CE certification support services specifically designed for collaborative robot (cobot) deployments. The expansion focused on providing detailed safety validation, collision risk analysis, and compliance documentation aligned with updated EU Machinery Regulation (EU) 2023/1230 requirements, enabling manufacturers to accelerate approval timelines and ensure safe human-robot collaboration on assembly and material handling production lines.

-

In January 2026, KUKA AG announced a strategic collaboration with AI company Algorized at CES 2026 to integrate advanced perception software into collaborative robot arms capable of sensing human movement and intent in real time. The partnership focused on improving safety and responsiveness in human-robot collaboration environments, supporting the deployment of next-generation collaborative robots across smart factories and industrial automation settings.

Collaborative Robot Market Report Scope

Report Attribute

Details

Market size in 2025

USD 2.9 billion

Market size value in 2026

USD 4.0 billion

Revenue forecast in 2033

USD 17.2 billion

Growth rate

CAGR of 23.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD Million/Billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Payload capacity, application, industry vertical, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; Japan; India; South Korea; Australia; Brazil; South Africa; Saudi Arabia; UAE

Key companies profiled

ABB Group; DENSO Corporation; Epson America Inc.; AUBO (BEIJING) ROBOTICS TECHNOLOGY CO., LTD; Comau S.p.A.; Energid Technologies Corporation; Fanuc Corporation; KUKA AG; Rethink Robotics GmbH; Robert Bosch GmbH; Techman Robot Inc.; Universal Robots; Yaskawa Electric Corporation; Precise Automation, Inc.; MRK-Systems GmbH

Customization scope

Free report customization (equivalent to up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Collaborative Robot Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global collaborative robot market report based on payload capacity, application, industry vertical, and region:

-

Payload Capacity Outlook (Revenue, USD Million, 2021 - 2033)

-

Up to 5Kg

-

Up to 10Kg

-

Above 10Kg

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Assembly

-

Pick & Place

-

Handling

-

Packaging

-

Quality Testing

-

Machine Tending

-

Gluing & Welding

-

Others

-

-

Industry Vertical Outlook (Revenue, USD Million, 2021 - 2033)

-

Automotive

-

Food & Beverage

-

Furniture & Equipment

-

Plastic & Polymers

-

Metal & Machinery

-

Electronics

-

Pharma

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Australia

-

Japan

-

India

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

The global collaborative robot market size was valued at USD 2.9 billion in 2025 and is estimated at USD 4.0 billion for 2026.

The global collaborative robot market is expected to grow at a CAGR of 23.1% from 2026 to 2033, reaching USD 17.2 billion by 2033.

The Asia Pacific dominated the collaborative robots market with a share of over 51% in 2025. This is attributable to the enormous application of co-bots in different verticals, such as electronics, logistics, and inspection in the region.

Key factors that are driving the market growth include increasing investments for automation in the manufacturing processes, higher return on investment (RoI) and lower price of collaborative robots, growing opportunities for robot installations in various industry verticals, and increasing demand in the logistics.

The assembly segment led with a 23.0% revenue share in 2025, while gluing & welding is the fastest-growing application.

The automotive segment led with a 25.0% revenue share in 2025, while electronics is the fastest-growing industry vertical.

Up to 5kg segment held the largest share (over 44.0%) in 2025, while above 10kg is the fastest-growing payload capacity.

Key players include ABB Group; DENSO Corporation; Epson America Inc.; AUBO (BEIJING) ROBOTICS TECHNOLOGY CO., LTD; Comau S.p.A.; Energid Technologies Corporation; Fanuc Corporation; KUKA AG; Rethink Robotics GmbH; Robert Bosch GmbH; Techman Robot Inc.; Universal Robots; Yaskawa Electric Corporation; Precise Automation, Inc.; MRK-Systems GmbH.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.