- Home

- »

- Advanced Interior Materials

- »

-

Fire Clay Market Size, Share And Trends Report, 2026-2033GVR Report cover

![Fire Clay Market (2026 - 2033)Report]()

Fire Clay Market (2026 - 2033)

Size, Share & Trends Analysis Report By Application (Refractories, Metallurgy), By Product (Bricks, Mortars & Cements, Castables), By End Use, By Region, And Segment Forecasts

Market Size, 2025

$8.0BMarket Estimate, 2026

$8.4BMarket Forecast, 2033

$14.4BCAGR, 2026–2033

8.0%Fire Clay Market Summary

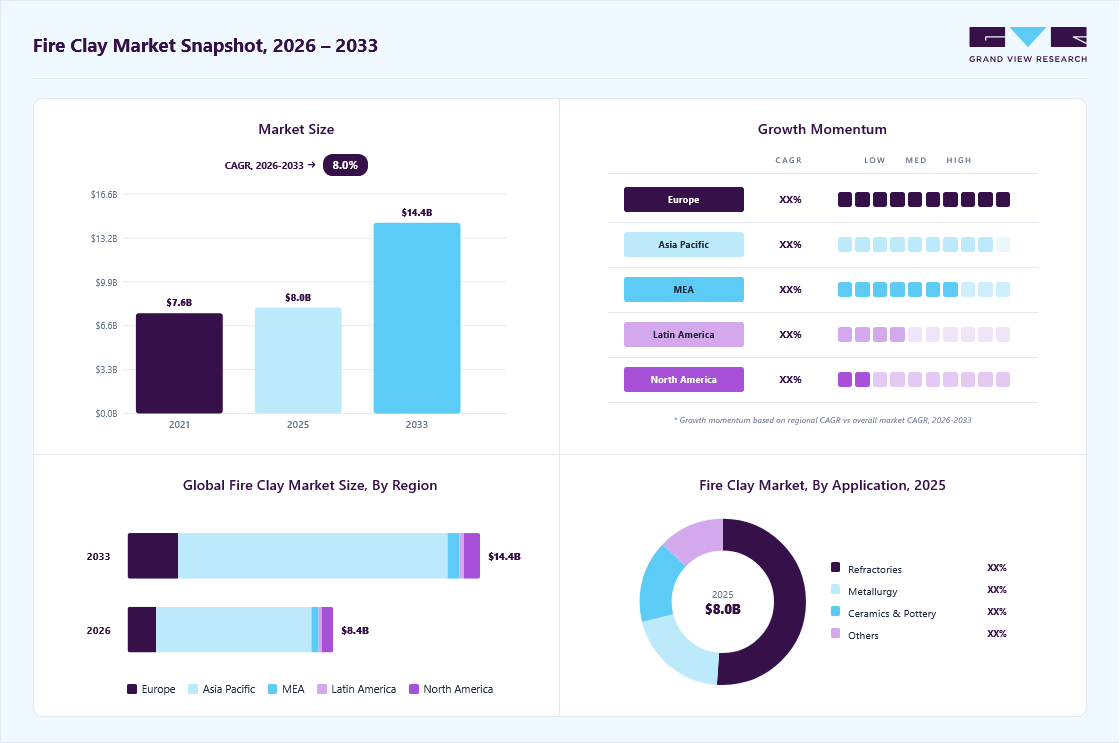

The global fire clay market size was valued at USD 8.0 billion in 2025 and is projected to grow from USD 8.4 billion in 2026 to USD 14.4 billion by 2033, at a CAGR of 8.0% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 75.2% in 2025. The market growth is primarily driven by the expanding demand from the iron & steel and cement industries, where fire clay is widely used in refractory linings for high-temperature operations.

Key Market Trends & Insights

- By application: Ceramics & pottery segment held the largest market share in 2025.

- By product: Castables segment held the largest market share in 2025.

- By end use: Iron & steel segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (75.2% revenue share, 2025)

- Fastest-growing regional market: Europe (highest CAGR, 2026-2033)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 8.0 Billion

- Estimated market size in 2026: USD 8.4 Billion

- Projected market size by 2033: USD 14.4 Billion

- CAGR (2026-2033): 8.0%

Rising infrastructure development and industrialization across emerging economies are further supporting the consumption of fire clay-based materials in construction and ceramics applications. Sustainability is becoming a central theme in the fire clay market, driven by increasing environmental regulations and industry commitments to reduce carbon footprints. Manufacturers are focusing on refractory recycling, energy-efficient kiln technologies, and the use of secondary raw materials to minimize waste and emissions. The shift toward circular economy practices, particularly in the steel and cement industries, is encouraging the reuse of spent refractories, including fire clay-based products. In addition, companies are investing in cleaner mining and processing methods to reduce environmental impact while ensuring long-term raw material availability.")

Technological advancements are reshaping the fire clay market through the development of high-performance refractory formulations and advanced manufacturing processes. Innovations such as improved alumina-silica compositions, enhanced thermal shock resistance, and longer service life materials are increasing operational efficiency in high-temperature industries. Furthermore, the adoption of automation, digital monitoring, and smart furnace technologies is enabling better performance tracking and predictive maintenance, thereby optimizing the use of fire clay refractories. These advancements are particularly critical in industries such as steel and glass, where efficiency, durability, and cost control are key competitive factors.

Drivers, Opportunities & Restraints

The market is primarily driven by growing demand from high-temperature industries such as iron & steel, cement, and glass, where refractory materials are essential for continuous operations. A recent instance can be observed in February 2024, when industry updates highlighted increased investments in global steel production capacity and infrastructure development, leading to higher consumption of refractory materials. This trend is particularly strong in the Asia Pacific, where expanding industrial output and capacity additions are driving frequent replacement and maintenance of furnace linings, thereby supporting steady demand for fire clay.

A key opportunity for the market is increasing focus on sustainability and circular economy practices, especially through refractory recycling and energy-efficient production methods. In 2023 and 2024, industry publications and sustainability disclosures emphasized that a significant portion of refractory materials can be recovered, reused, and reprocessed, reducing both raw material dependency and environmental impact. This shift encourages manufacturers to invest in recycling infrastructure and develop eco-friendly product lines, creating new growth avenues while aligning with global decarbonization goals.

The market faces constraints due to fluctuating raw material availability, rising energy costs, and tightening environmental regulations, which collectively increase operational complexity. In 2024, several industry analysts pointed out that refractory producers are experiencing cost pressures linked to volatile prices of key inputs and stricter emission norms, particularly in Europe and North America. These factors can lead to supply disruptions and margin pressures, especially for producers dependent on high-purity fire clay, thereby posing a challenge to consistent market growth.

Application Insights

The ceramics & pottery segment is expected to register the highest CAGR in the fire clay market, driven by rising demand for industrial ceramics, sanitaryware, and decorative pottery products. Increasing urbanization and infrastructure development, especially in emerging economies, are further supporting the adoption of fire clay-based materials in ceramic kilns and processing applications.

Refractories held the largest share in 2025, as fire clay is extensively used in furnace linings, kilns, boilers, and other high-temperature industrial equipment. Continuous demand from the steel, cement, and glass industries for heat-resistant and durable lining materials has reinforced the dominance of this segment.

Product Insights

Castables are expected to witness the highest growth in the fire clay market, supported by their ease of installation, flexibility in application, and superior performance in complex industrial furnace structures. Growing preference for monolithic refractories over traditionally shaped products is further accelerating the adoption of castables across heavy industries.

Bricks accounted for the largest market share in 2025, owing to their widespread use in refractory linings and high-temperature industrial structures. Their durability, cost-effectiveness, and established usage in steel, cement, and glass manufacturing facilities continue to support strong demand.

End Use Insights

The iron & steel industry is expected to record the highest CAGR, driven by increasing steel production, modernization of furnaces, and rising adoption of electric-arc furnace technologies. Fire clay refractories play a critical role in withstanding extreme operating temperatures, making them essential in steelmaking processes.

Ceramics remained the largest end-use segment in 2025, supported by extensive demand for fire clay in ceramic tiles, sanitaryware, and pottery production. Strong growth in construction activities and rising consumer demand for aesthetic and durable ceramic products continue to reinforce this segment’s dominance.

Regional Insights

North America's Fire Clay Market Trends

The North American market is characterized by stable demand from mature end-use industries, particularly iron & steel, cement, and glass manufacturing. The region benefits from well-established refractory consumption patterns, driven by maintenance and replacement cycles rather than new capacity additions. Increasing emphasis on energy-efficient furnaces and emission reduction technologies is supporting the adoption of high-performance fire clay refractories. In addition, the presence of key refractory manufacturers and recycling initiatives is contributing to supply chain stability.

U.S. Fire Clay Market Trends

The U.S. represents the largest contributor within North America, driven by its advanced industrial base and consistent demand from steel production and petrochemical processing. Fire clay consumption is largely tied to infrastructure renovation, shale gas-based industrial expansion, and manufacturing resilience initiatives. The market is also witnessing gradual growth in refractory recycling and sustainable material usage, aligning with environmental regulations and cost optimization strategies adopted by domestic producers.

Europe Fire Clay Market Trends

Europe’s market is mature and regulation-driven, with demand primarily stemming from the steel, cement, and specialty ceramics industries. The region is witnessing a shift toward low-carbon manufacturing and circular economy practices, encouraging the use of recycled refractory materials alongside primary fire clay. While industrial growth remains moderate, technological advancements in furnace design and efficiency improvements are sustaining demand for high-quality fire clay-based refractories.

Asia Pacific Fire Clay Market Trends

Asia Pacific dominates the global fire clay market, driven by rapid industrialization, infrastructure development, and high steel production, particularly in countries such as China and India. The region accounts for the largest consumption of refractories, supported by expanding cement, power, and ceramics industries. Strong government investments in infrastructure and manufacturing are further accelerating demand. In addition, the availability of abundant raw material reserves and low-cost production capabilities strengthens the region’s position as both a major consumer and supplier.

China dominates the Asia Pacific fire clay market, driven by its massive steel, cement, and ceramics manufacturing base, which generates sustained demand for refractory materials. The country remains the largest global producer and consumer of steel, and continuous investments in infrastructure, urban development, and industrial capacity expansion further reinforce fire clay consumption. In addition, China’s well-established refractory manufacturing ecosystem and access to abundant raw material reserves strengthen its leadership position in the regional market.

Latin America Fire Clay Market Trends

The Latin American market is emerging with moderate growth potential, supported by developments in the steel, mining, and construction sectors. Countries such as Brazil and Mexico are key contributors, where demand is driven by industrial expansion and infrastructure investments. However, market growth is somewhat constrained by economic volatility and fluctuating industrial output, although long-term prospects remain positive with increasing focus on local manufacturing capabilities.

Middle East & Africa Fire Clay Market Trends

The Middle East & Africa market is witnessing steady growth driven by infrastructure projects, energy sector investments, and cement production expansion. The region’s demand is supported by large-scale construction activities and industrial diversification efforts, particularly in Gulf countries. While local production of fire clay is limited in some areas, reliance on imports and development of regional refractory manufacturing capacities are shaping the market landscape.

Key Fire Clay Company Insights

Some of the key players operating in the market include RHI Magnesita, Vesuvius plc, and others.

-

RHI Magnesita, established in 2017, is the world’s leading global supplier of refractory products, systems, and solutions, with a strong presence across Europe, Asia Pacific, North America, and Latin America. The company offers a comprehensive portfolio of refractory materials, including fire clay-based bricks, magnesia-based products, and monolithics, serving industries such as iron & steel, cement, non-ferrous metals, and glass. RHI Magnesita is recognized for its vertically integrated business model, including raw material mining and recycling capabilities, and its focus on innovation, sustainability, and high-temperature industrial process optimization.

-

Vesuvius plc, established in 1916, is a leading global provider of molten metal flow engineering and refractory solutions, with operations spanning Europe, Asia Pacific, North America, and emerging markets. The company delivers a wide range of products, including fire clay-based refractories, flow control systems, and advanced ceramics for the steel and foundry industries. Vesuvius plc is known for its strong technical expertise, R&D-driven product development, and customized solutions that enhance efficiency, safety, and performance in high-temperature industrial processes.

-

Imerys, established in 1880, is a global leader in specialty minerals, including kaolin and fire clay, with a strong operational footprint across Europe, the Americas, and Asia Pacific. Imerys provides a diverse portfolio of mineral-based solutions used in refractories, ceramics, construction, and industrial applications, including high-quality fire clay for refractory bricks and kiln linings. The company is recognized for its extensive mineral reserves, advanced processing technologies, and focus on sustainable mining practices, enabling it to support high-performance material requirements across multiple end-use industries.

Key Fire Clay Companies:

The following key companies have been profiled for this study on the fire clay market.

- Calderys

- HarbisonWalker International

- Imerys

- Krosaki Harima Corporation

- Morgan Advanced Materials

- Refratechnik Holding GmbH

- RHI Magnesita

- Saint-Gobain

- Shinagawa Refractories Co., Ltd.

- Vesuvius plc

Recent Development

-

In March 2024, Imerys announced capacity optimization and operational improvements across its Performance Minerals segment, as disclosed in investor communications. The move is intended to strengthen supply reliability for key materials such as kaolin and fire clay used in refractory and ceramics applications.

-

In February 2024, RHI Magnesita announced the expansion of its recycling and raw material processing capabilities in Europe, as part of its sustainability strategy disclosed in company reports. The initiative is aimed at increasing the use of secondary raw materials, including fire clay-based inputs, to reduce carbon emissions and improve cost efficiency in refractory production.

-

In October 2023, Vesuvius plc announced continued investments in its Flow Control and Advanced Refractories divisions, as highlighted in its annual financial disclosures. The company is focusing on enhancing product performance and supporting steel industry customers with more efficient and durable refractory solutions, including alumina-silica (fire clay) products.

Fire Clay Market Report Scope

Report Attribute

Details

Market definition

The market size represents the total annual global sales revenue generated from fire clay, reflecting the value of raw and processed fire clay materials supplied for use in refractories, ceramics, and high-temperature industrial applications across industries for a given year.

Market size in 2025

USD 8.0 billion

Estimated market size in 2026

USD 8.4 billion

Projected market size by 2033

USD 14.4 billion

Growth rate

CAGR of 8.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Volume in kilotons, Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Volume forecast, revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Application, product, end use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; China; India; Japan; South Korea; Brazil; Argentina; Saudi Arabia; UAE; Egypt

Key companies profiled

Calderys; HarbisonWalker International; Imerys; Krosaki Harima Corporation; Morgan Advanced Materials; Refratechnik Holding GmbH; RHI Magnesita; Saint-Gobain; Shinagawa Refractories Co., Ltd.; Vesuvius plc

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Fire Clay Market Segmentation

This report forecasts revenue growth at the country & regional levels and provides an analysis of the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global fire clay market report on the basis of application, product, end use, and region.

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Refractories

-

Metallurgy

-

Ceramics & Pottery

-

Others

-

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Bricks

-

Castables

-

Mortars & Cements

-

Others

-

-

End Use Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Iron & Steel

-

Cement

-

Glass

-

Power Generation

-

Ceramics

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

Egypt

-

-

Frequently Asked Questions About This Report

The global fire clay market is driven by growing demand from high-temperature industries such as iron & steel, cement, and glass manufacturing. Rising infrastructure development and industrial expansion across emerging economies are further strengthening market growth.

The ceramics & pottery segment held the largest revenue share in 2025, while the refractories segment is the fastest-growing.

The castables segment held the largest revenue share in 2025, while the bricks segment is the fastest-growing.

The iron & steel segment held the largest revenue share in 2025, while the ceramics segment is the fastest-growing.

The global fire clay market size was valued at USD 8.0 billion in 2025 and is estimated at USD 8.4 billion for 2026.

The global fire clay market is expected to grow at a CAGR of 8.0% from 2026 to 2033, reaching USD 14.4 billion by 2033.

Asia Pacific dominated with a 75.2% revenue share in 2025.

Europe is the fastest-growing region over the forecast period.

Key players include Calderys; HarbisonWalker International; Imerys; Krosaki Harima Corporation; Morgan Advanced Materials; Refratechnik Holding GmbH; RHI Magnesita; Saint-Gobain; Shinagawa Refractories Co., Ltd.; Vesuvius plc

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.