- Home

- »

- Renewable Chemicals

- »

-

Furfural Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Furfural Market (2026 - 2033)Report]()

Furfural Market (2026 - 2033)

Size, Share & Trends Analysis Report By Process (Quaker Batch Process, Chinese Batch Process), By Raw Material (Rice Husk, Corn Cob, Sunflower Hull, Sugar Cane Bagasse), By Application, By End-use, By Region, And Segment Forecasts

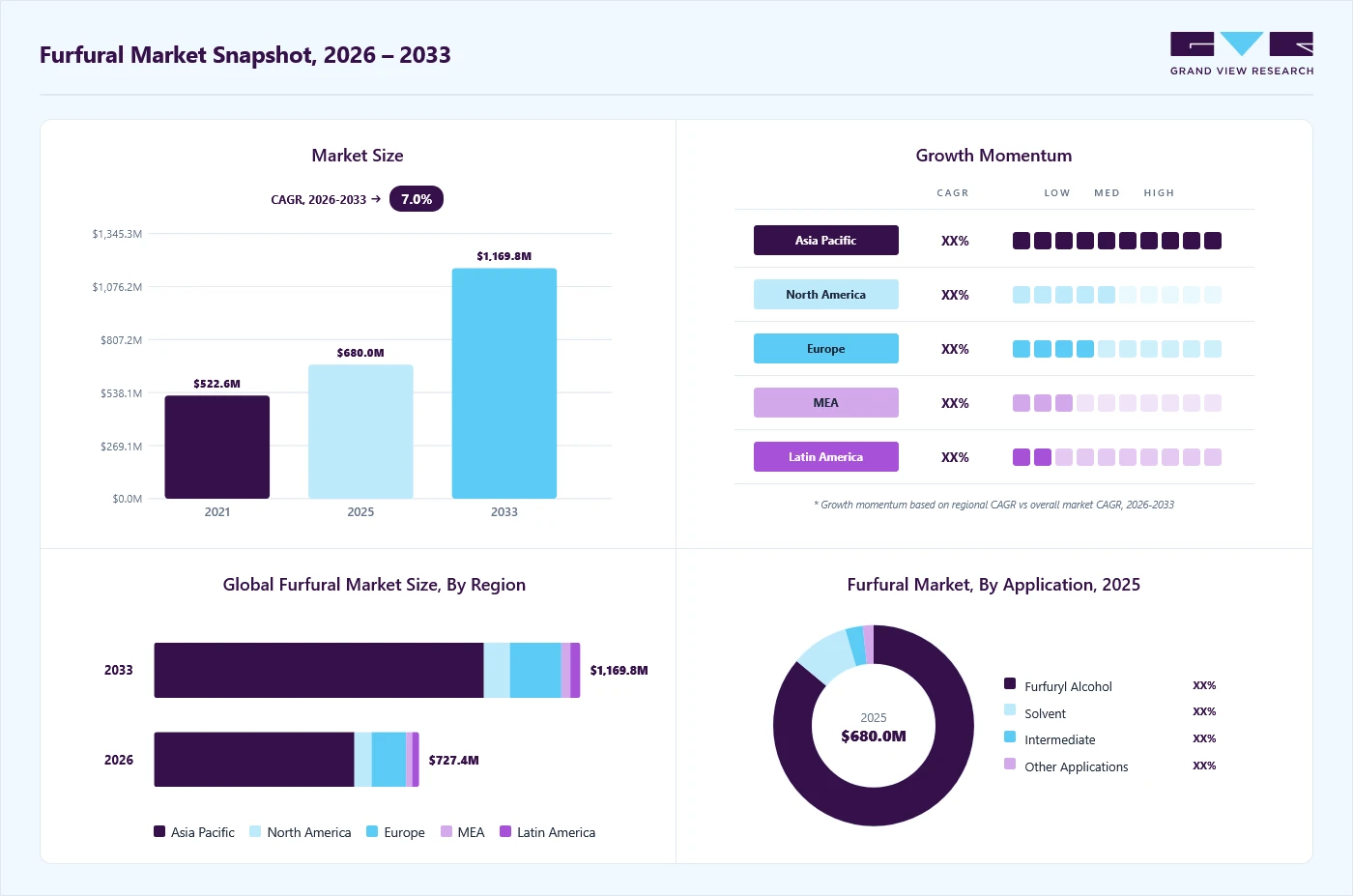

Market Size, 2025

$680.0MMarket Estimate, 2026

$727.4MMarket Forecast, 2033

$1,169.8MCAGR, 2026–2033

7.0%Furfural Market Summary

The global furfural market size was valued at USD 680.0 million in 2025 and is projected to grow from USD 727.4 million in 2026 to USD 1,169.8 million by 2033, at a CAGR of 7.0% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 75.3% in 2025. The demand also benefits from growing applications across solvents, chemical intermediates, and specialty formulations in industrial sectors.

Key Market Trends & Insights

- By process: Chinese batch process segment held the largest market share of 82.2% in 2025.

- By raw material: Corn cob segment held the largest market share of 70.6% in 2025.

- By application: Furfuryl alcohol segment held the largest market share of 86.0% in 2025.

- By end-use: Refineries segment held the largest market share of 51.2% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (75.3% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 680.0 Million

- Estimated market size in 2026: USD 727.4 Million

- Projected market size by 2033: USD 1,169.8 Million

- CAGR (2026-2033): 7.0%

A key application driving market growth is its use as a renewable chemical intermediate in industrial manufacturing. Furfural is primarily converted into furfuryl alcohol, which is widely utilized in foundry resins, corrosion-resistant materials, and industrial binders, supporting demand from metal casting, construction, and heavy manufacturing sectors. As industries increasingly focus on sustainable and bio-based alternatives to petroleum-derived chemicals, furfural continues to gain importance as a value-added product derived from agricultural residues such as corn cobs and sugar cane bagasse.")

Beyond its primary industrial uses, furfural also serves as a solvent and chemical intermediate across refining, pharmaceuticals, and specialty chemical manufacturing, where it contributes to process efficiency and performance improvements. Growing environmental regulations and the shift toward greener production practices are encouraging manufacturers to adopt biomass-derived chemicals, supporting steady adoption of furfural in niche applications. However, challenges such as feedstock availability fluctuations, process efficiency constraints, and regulatory compliance requirements continue to influence market growth. At the same time, advancements in continuous processing technologies, diversification of raw material sources, and expanding downstream industrial demand are expected to create new opportunities and drive long-term development within the global market.

Market Concentration & Characteristics

The global furfural industry is moderately fragmented, with market leadership concentrated among several established producers such as Hongye Holding Group Corporation Ltd., Illovo Sugar Africa (Pty.) Ltd, Linzi Organic Chemical Inc., along with other regional biomass-based chemical manufacturers and specialty industrial chemical producers. These key players benefit from strong in-house production capabilities, established processing infrastructure, access to agricultural feedstock, and extensive regional and global distribution networks to maintain a competitive advantage. Their integration across the furfural value chain, from raw material sourcing and biomass processing to purification, quality assurance, and commercialization, enables improved operational efficiency, consistent product quality, and reliable supply across downstream industries.

At the same time, emerging players in the Asia Pacific, Latin America, and the Middle East & Africa are steadily expanding their presence in the global furfural industry by leveraging cost-efficient manufacturing capabilities, improving access to agricultural feedstock, and rising domestic demand for bio-based industrial chemicals and sustainable intermediates. These regional manufacturers are supported by targeted investments in biomass processing technologies, furfural production facilities, and localized distribution networks strategically positioned near key agricultural and industrial manufacturing hubs. Their focus is on delivering scalable and performance-driven solutions across high-growth application areas such as furfuryl alcohol production, solvents, intermediates, and specialty industrial formulations.

Process Insights

The Chinese batch process accounted for a significant revenue share of 82.2% in 2025, driven by its cost-effective setup, established operational base, and widespread adoption across large-scale biomass processing facilities. This process is extensively utilized in commercial furfural production as it offers operational flexibility, compatibility with agricultural residues such as corn cob and bagasse, and the ability to support high-volume manufacturing requirements. Its strong presence across major production hubs, particularly in China, has enabled manufacturers to maintain competitive pricing and stable supply levels in global trade.

The Quaker batch process is expected to grow significantly with a CAGR of 6.8% during the forecast period, reflecting increasing adoption due to its operational efficiency and suitability for diverse feedstocks. Other production methods, including the Rosenlew continuous process and emerging modified technologies, are also gaining gradual attention as manufacturers aim to improve operational efficiency and reduce environmental impact. Continuous processing technologies offer advantages such as improved yield optimization, reduced energy consumption, and enhanced automation capabilities, supporting long-term sustainability goals. However, higher capital investment requirements and infrastructure limitations continue to restrict rapid large-scale adoption.

Raw Material Insights

Corn cob represents the dominant raw material segment, accounting for the largest revenue share of 70.6% in 2025, due to its high pentosane content, wide agricultural availability, and cost-efficient processing characteristics. It is extensively used in commercial furfural production as it offers consistent yield performance and supports large-scale batch processing operations, particularly in regions with strong agricultural residue generation. The use of corn cob feedstock enables manufacturers to produce furfural efficiently while aligning with circular economy practices and biomass utilization strategies.

Sugar cane bagasse is expected to grow fastest with a CAGR of 7.2% during the forecast period, driven by its abundance in sugar-producing regions and suitability for biomass conversion processes. Growing industrial demand for renewable chemical intermediates is also supporting the use of alternative feedstocks such as rice husk, sunflower hull, and other agricultural residues in furfural production. These raw material options allow manufacturers to diversify sourcing strategies, improve supply resilience, and optimize production efficiency based on regional agricultural outputs.

End-use Insights

Refineries emerged as the largest end-use segment in the global market, capturing 51.2% of revenue in 2025. This dominance is largely driven by the use of furfural as a selective solvent in lubricant refining and petroleum processing, where it effectively removes aromatic compounds and enhances base oil quality. Strong demand from the automotive, industrial, and energy sectors continues to reinforce its position. Beyond refineries, furfural finds applications in foundries, chemical manufacturing, and industrial processing, including resins, intermediates, and specialty formulations. The growing shift toward bio-based chemicals and sustainable industrial inputs further supports its adoption across diverse sectors.

Agriculture is expected to grow significantly with a CAGR of 6.8% during the forecast period. Rising utilization in crop protection formulations, bio-stimulants, and soil conditioning products is driving this growth, as manufacturers increasingly seek renewable, high-performance inputs that improve efficiency and environmental sustainability in agricultural operations.

Application Insights

Furfuryl alcohol continues to be the leading application segment, representing 86.0% of the market in 2025. Its widespread usage in foundry resins, corrosion-resistant coatings, and industrial binder systems underpins robust demand from sectors such as metal casting, construction, and heavy manufacturing.

Solvent applications are emerging as the fastest-growing segment, projected to grow at a CAGR of 7.2% over the forecast period. Increased adoption in coatings, cleaning solutions, and specialty chemical formulations is driving this growth, as furfural enhances performance, process efficiency, and product quality. Additionally, its use in chemical intermediates and specialty industrial applications supports further market expansion.

Regional Insights

Asia Pacific dominated the global furfural market, accounting for a 75.3% value share in 2025, driven primarily by strong production capacity, abundant agricultural feedstock availability, and well-established biomass processing infrastructure across major manufacturing hubs. Rapid industrialization, expanding chemical manufacturing activities, and growing demand for bio-based intermediates across refining, foundry, and specialty chemical sectors have significantly contributed to rising furfural production and consumption in the region.

China Furfural Market Trends

The furfural market in China represents the largest country-level market globally, accounting for 88.8% share in 2025, supported by extensive batch processing infrastructure, strong availability of agricultural residues such as corn cob, and cost-competitive large-scale production capabilities. The country’s well-established export network, long-standing expertise in biomass-based chemical manufacturing, and dominant presence in global furfural supply chains continue to reinforce its leadership position. Ongoing investments in process optimization and industrial capacity expansion further strengthen China’s role as a key production and export hub within the market.

Europe Furfural Market Trends

The furfural market in Europe accounted for the second-largest region by revenue, with a share of over 13.2% in 2025, driven by its increasing specialty chemical manufacturing, refining operations, and advanced industrial processing industries. The region maintains moderate consumption levels supported by well-established downstream sectors, including resins, coatings, and performance materials. Increasing regulatory focus on sustainability and bio-based chemicals is encouraging interest in biomass-derived intermediates. However, limited domestic production capacity results in continued reliance on imports to support regional demand.

Germany furfural market serves as a major industrial hub within Europe, supported by strong specialty chemical manufacturing and advanced materials production sectors. Demand for furfural is driven by applications in refining, resins, and high-performance industrial formulations used across the automotive and engineering industries. The country’s emphasis on high-quality chemical processing and sustainable production practices supports steady niche adoption of bio-based intermediates. However, domestic production remains limited, with most supply sourced through imports from major producing regions.

North America Furfural Market Trends

The furfural market in North America is expected to grow significantly with a CAGR of 6.1% during 2026-2033. Growth in the region is supported by increasing investments in renewable chemical production, expansion of furfural-based applications in agriculture and specialty chemicals, and the rising adoption of sustainable feedstock processing technologies. These factors are driving a steady increase in regional demand while supporting long-term market development.

The U.S. furfural marketrepresents a key market within North America, supported by demand from petroleum refining, specialty chemicals, and industrial manufacturing sectors. The country largely depends on imported furfural to meet domestic needs due to limited large-scale production capacity. Strong downstream consumption in lubricant refining, resins, and performance materials continues to sustain steady market demand. In addition, growing interest in renewable chemical intermediates and sustainable sourcing practices is gradually supporting niche adoption across industrial applications.

Latin America Furfural Market Trends

The furfural market in Latin America is experiencing significant growth due to its growing industrial activities and access to agricultural residues suitable for biomass-based chemical production. Countries with strong sugar and agricultural output present opportunities for localized furfural manufacturing using feedstocks such as sugar cane bagasse. Refining, resins, and specialty chemical applications mainly drive industrial demand. Although relatively small, ongoing industrial development and interest in renewable chemicals are expected to support gradual regional expansion.

Middle East & Africa Furfural Market Trends

The furfural market in the Middle East & Africa is expected to experience moderate growth, with demand largely tied to refining operations, industrial processing, and specialty chemical manufacturing. Established petroleum refining infrastructure continues to generate steady solvent application requirements. Local production remains limited, resulting in continued dependence on imported supply. Industrial diversification initiatives and sustainability-focused investments are expected to create emerging opportunities across niche applications over the long term.

Key Furfural Company Insights

The presence of several leading players, including Merck KGaA, Biospringer S.A., Kerry Group, Central Drug House, and Thermo Fisher Scientific Inc., among others, characterizes the global market. These companies actively focus on research and development, capacity expansion, and strategic collaborations while prioritizing sustainability. They continuously adapt to shifting industry requirements, especially in sectors such as batteries, cosmetics, and pharmaceuticals, while ensuring compliance with regulations and optimizing supply chains to meet growing global demand efficiently and cost-effectively.

Hongye Holding Group Corporation Ltd. is a significant market player in the global furfural and furfuryl alcohol industry, with substantial manufacturing operations based in China. The company specializes in large-scale biomass processing using agricultural residues such as corn cobs to produce bio-based chemical intermediates. Its integrated production capabilities, export-oriented supply network, and cost-efficient batch processing infrastructure support a strong presence in international industrial and refining markets.

Key Furfural Companies:

The following key companies have been profiled for this study on the furfural market.

- Hongye Holding Group Corporation Ltd.

- Illovo Sugar Africa (Pty.) Ltd

- Linzi Organic Chemical Inc. Ltd.

- Trans Furans Chemicals bvba

- Central Romana Corporation

- DalinYebo

- Hebeichem

- KRBL Ltd.

- Silva team S.p.a.

- LENZING AG.

Recent Developments

-

In September 2025, Engineers India Limited completed the mechanical setup of a biorefinery project for Assam Bio Ethanol Private Limited in Numaligarh. The facility is designed to produce 19,000 TPA of furfural from bamboo feedstocks, utilizing technology from Chempolis Oy. This development reflects the increasing focus on lignocellulosic biomass and the use of alternative feedstock sources beyond conventional agricultural residues. Similar initiatives are expected to drive broader adoption of bio-based chemicals and contribute to sustained market growth.

Furfural Market Report Scope

Report Attribute

Details

Market size in 2025

USD 680.0 million

Estimated market size in 2026

USD 727.4 million

Projected market size by 2033

USD 1,169.8 million

Growth rate

CAGR of 7.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2018 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Process, raw material, application, end-use, region

Regional scope

North America; Europe; Asia Pacific; MEA; Latin America

Country scope

U.S.; Canada; Mexico; Germany; France; Spain; Italy; UK; China; India; Japan; South Korea; Brazil; South Africa; Saudi Arabia; Turkey

Key companies profiled

Hongye Holding Group Corporation Ltd.; Illovo Sugar Africa (Pty.) Ltd.; Linzi Organic Chemical Inc. Ltd.; Trans Furans Chemicals bvba; Central Romana Corporation; DalinYebo; Hebeichem; KRBL Ltd.; Silva Team S.p.A.; Lenzing AG

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Furfural Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2033. For this study, Grand View Research has segmented the global furfural market report based on process, raw material, application, end-use, and region:

-

Process Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Quaker Batch Process

-

Chinese Batch Process

-

Rosenlew Continuous Process

-

Other Processes

-

-

Raw Material Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Corn Cob

-

Sugar Cane Bagasse

-

Sunflower Hull

-

Rice Husk

-

Other Raw Materials

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Furfuryl Alcohol

-

Solvent

-

Intermediate

-

Other Applications

-

-

End-use Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

Agriculture

-

Paints & Coatings

-

Pharmaceutical

-

Food & Beverage

-

Refineries

-

Other End Use

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2018 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

Spain

-

Italy

-

UK

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

Turkey

-

-

Frequently Asked Questions About This Report

Some key players operating in the furfural market include Teiling, Central Romana Corp., International Furan Chemicals, TransFurans Chemicals, Penn A Kem LLC, and Sugar Illovo Ltd.

Key factors that are driving the furfural market growth include the industry shift toward minimizing dependence on conventional petrochemicals on account of growing environmental concerns.

The global furfural market is expected to grow at a compound annual growth rate of 7.0% from 2023 to 2030 to reach USD 1,169.8 million by 2033.

The Asia Pacific dominated the furfural market with a share of 75.3% in 2025.

The global furfural market size was estimated at USD 680.0 million in 2025 and is expected to reach USD 727.4 million in 2026.

The chinese batch process segment led with a 82.2% revenue share in 2025.

Corn cob held the largest revenue share 70.6% in 2025, while sugar cane bagasse is the fastest-growing area.

Furfuryl alcohol held the largest share (over 86.0%) in 2025 and solvent applications is the fastest-growing market.

The refineries batch process segment led with a 51.2% revenue share in 2025.

About the Author(s)

Renewable Chemicals Research Team

Specialty & Chemicals · Renewable ChemicalsThis report was authored by the renewable chemicals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the renewable chemicals segment of the specialty & chemicals industry. All findings are based on proprietary specialty & chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.