- Home

- »

- Electronic Devices

- »

-

Laser Processing Market Size, Share, Industry Report, 2030GVR Report cover

![Laser Processing Market Size, Share & Trends Report]()

Laser Processing Market (2025 - 2030) Size, Share & Trends Analysis Report By Product (Gas, Solid-state, Fiber), By Process (Material Processing, Micro-Processing), By End-use (Automotive, Aerospace, Machine Tools), By Region, And Segment Forecasts

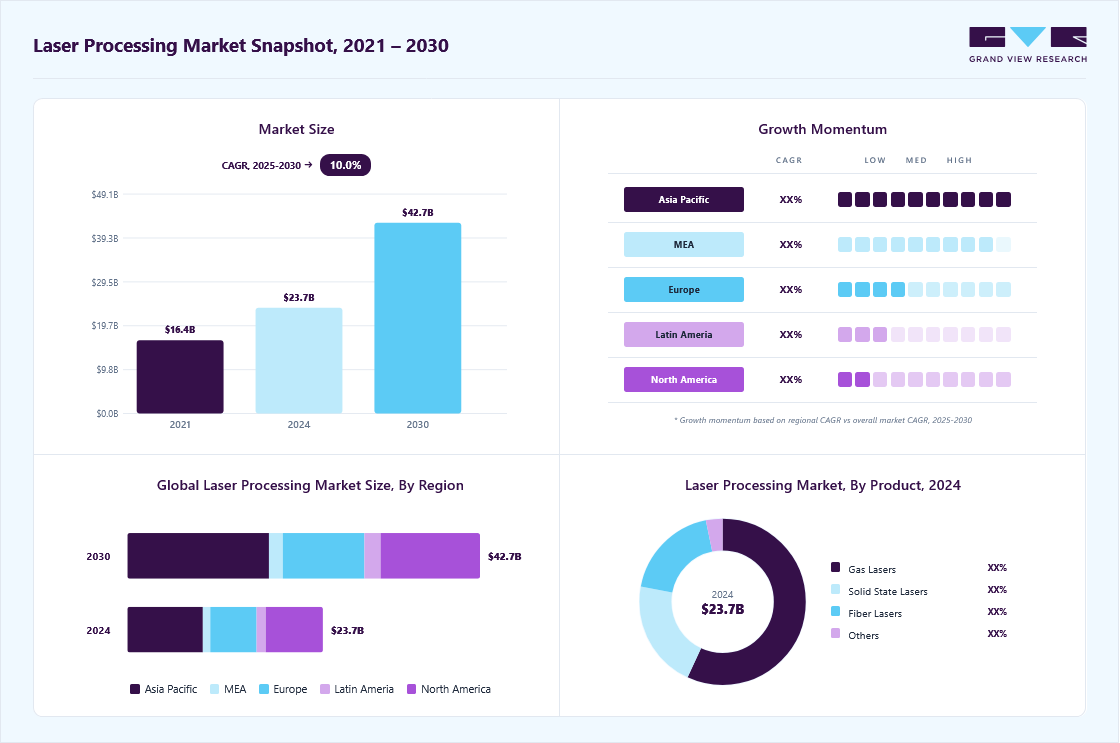

Market Size, 2024

$23.7BMarket Estimate, 2026

$26.6BMarket Forecast, 2030

$42.7BCAGR, 2025–2030

10.0%Laser Processing Market Summary

The global laser processing market size was estimated at USD 23.7 billion in 2024 and is projected to reach USD 42.73 billion by 2030, growing at a CAGR of 10.0% from 2025 to 2030. Laser processing is vital in additive manufacturing, particularly in selective laser melting (SLM) and laser sintering for metals and high-performance polymers.

Key Market Trends & Insights

- North America laser processing market has a significant revenue share of over 29% in 2024.

- The U.S. laser processing market is expected to grow at a CAGR from 2025 to 2030.

- By product, the gas lasers segment led the market in 2024, accounting for over 65% of the global revenue.

- By process, the material processing segment accounted for the largest market revenue share in 2024.

- By end-use, the machine tools segment accounted for the largest market revenue share in 2024.

Market Size & Forecast

- 2024 Market Size: USD 23.7 Billion

- 2030 Projected Market Size: USD 42.73 Billion

- CAGR (2025-2030): 10.0%

- Asia Pacific: Largest market in 2024

These techniques allow manufacturers to create complex, lightweight parts layer-by-layer, which is especially valuable in the aerospace, automotive, and medical sectors. The precision of lasers ensures high-quality builds with minimal waste and enables rapid prototyping and customization. As 3D printing becomes more widely adopted, the role of laser processing in additive manufacturing will continue to expand.

")

The renewable energy sector, especially solar panel manufacturing, has begun to adopt laser processing for its precision and ability to enhance energy capture efficiency. Laser scribing and cutting are used in photovoltaic cell manufacturing, enabling higher panel efficiency by creating finer and more precise structures. Additionally, lasers assist in the production of energy storage devices, such as lithium-ion batteries, which are essential for renewable energy storage. This trend is expected to grow as renewable energy gains importance globally, driving demand for high-precision laser solutions.

The rising demand of Industry 4.0, laser processing systems are increasingly integrated into automated production lines, improving efficiency and consistency. In smart factories, lasers contribute to high-speed, precise operations that minimize human intervention, supporting scalable and cost-effective manufacturing. Automated laser processing systems are designed to be more adaptable and reliable, reducing downtime and enhancing production throughput. As industries adopt more automation, the demand for laser processing technology compatible with IoT and smart systems will expand.

The electronics industry is a major driver of the market, especially in areas requiring precise cutting, engraving, and marking. With the rise in demand for miniaturized electronic components, lasers offer unparalleled accuracy for intricate designs. This is particularly critical for smartphones, wearables, and microchips, where laser-based methods enhance efficiency and product reliability. As manufacturers aim for smaller and more complex devices, the adoption of laser processing in electronics is expected to increase.

Laser processing has become integral to automotive manufacturing, where it’s used for welding, cutting, and marking parts. The trend is amplified by the automotive sector’s shift toward electric vehicles (EVs), which require specialized laser applications in battery production and lightweight material processing. Lasers allow for faster, cleaner cuts and welds, essential for EV efficiency and safety standards. This shift is likely to drive the demand for advanced laser processing solutions tailored to the automotive industry.

Product Insights

The gas lasers segment led the market in 2024, accounting for over 65% of the global revenue. Laser cutting is increasingly used for processing metals and alloys, allowing for fast, precise cuts with minimal waste. This trend is driven by industries such as automotive, aerospace, and construction, where accurate metal cutting is critical for structural integrity and efficiency. Fiber lasers are popular for their ability to cut high-strength metals like stainless steel, aluminum, and titanium. Additionally, laser cutting reduces the need for post-processing, making it an attractive option for high-volume production lines. As manufacturers demand tighter tolerances and better edge quality, laser cutting technology will continue to evolve, supporting faster and cleaner cuts.

The fiber lasers segment is predicted to foresee the highest growth in the coming years. Fiber lasers are also finding a strong foothold in additive manufacturing, where they play a key role in processes like selective laser melting (SLM) and laser sintering. Fiber lasers offer the high energy density needed for melting powdered metals and polymers, allowing for precise, layer-by-layer builds that are essential in 3D printing. Their stability and ability to work with various materials make them an asset for creating customized parts in automotive, aerospace, and healthcare sectors. As 3D printing becomes more prevalent, the role of fiber lasers in additive manufacturing will continue to grow. This trend is helping industries innovate with lightweight and complex structures while maintaining structural integrity.

Process Insights

The material processing segment accounted for the largest market revenue share in 2024. Laser processing is essential for metals due to its ability to achieve precise cuts, welds, and engravings, which are highly valued in the automotive and aerospace industries. As these sectors increasingly prioritize lightweight metals like aluminum and titanium to improve fuel efficiency, lasers provide a non-contact, clean processing method that maintains material integrity. In automotive, lasers are used for welding and cutting critical components like frames and engine parts, while aerospace uses lasers for creating complex, high-strength structures. These applications demand precision and consistency, which laser processing delivers at high speeds. As lightweight metals gain traction, the use of laser processing in metals will continue to expand significantly.

The micro-processing segment is predicted to foresee the significant growth rate in the coming years. The semiconductor industry relies heavily on laser micro-processing to produce microchips, wafers, and circuit boards, where precision is paramount. Lasers enable highly accurate cutting, dicing, and marking on semiconductor materials like silicon and gallium arsenide without causing micro-cracks or heat damage. This is especially relevant with the transition to smaller semiconductor nodes, where the accuracy of laser processing is crucial for maintaining functionality. As demand for smaller, faster, and more efficient chips grows, especially for AI, 5G, and IoT applications, the semiconductor sector's investment in laser micro-processing technology will intensify. The trend toward advanced packaging techniques, such as wafer-level and chip-scale packaging, also enhances the importance of laser micro-processing in this industry.

End-use Insights

The machine tools segment accounted for the largest market revenue share in 2024. Fiber lasers are increasingly popular in machine tools due to their high efficiency, power output, and lower maintenance requirements compared to CO₂ lasers. These lasers offer faster processing speeds, allowing machine tools to achieve high precision even with challenging materials like metals and ceramics. Fiber lasers are also compact, making them easier to integrate into smaller or more versatile machine tools. Their reliability and energy efficiency are appealing to manufacturers looking to reduce operational costs while maintaining high productivity. This trend highlights the shift toward fiber laser technology in various machining applications, from cutting to engraving.

")

The automotive segment is expected to exhibit a significant CAGR over the forecast period. Laser cutting and engraving are being used in the automotive sector to manufacture complex parts that demand high precision, such as fuel injectors, engine blocks, and exhaust components. This precision helps meet stringent industry standards for safety and performance, ensuring consistency and reducing the need for post-processing. With lasers, manufacturers can achieve intricate designs on various materials, including metals and plastics, improving the quality and reliability of automotive components. These precise manufacturing capabilities are crucial for meeting the growing demand for high-performance parts in both conventional and electric vehicles. As vehicle design complexity increases, laser processing will play a vital role in achieving fine detail and accuracy.

Regional Insights

North America laser processing market has a significant revenue share of over 29% in 2024. North America is witnessing strong growth in laser processing, largely driven by the automotive and aerospace industries. Advanced manufacturing technologies are increasingly adopted here, with laser processing aiding in precision cutting, welding, and engraving of high-performance components. The region’s focus on innovation and adoption of smart manufacturing also boosts the demand for laser-based automation solutions.

U.S. Laser Processing Market Trends

The U.S. laser processing market is expected to grow at a CAGR from 2025 to 2030. In the U.S., the market is driven by high demand in aerospace, automotive, and medical device manufacturing. The country’s advanced R&D ecosystem encourages innovation in laser processing technologies, leading to developments in fiber and diode lasers. Additionally, growing investments in electric vehicle manufacturing are increasing the demand for laser-based welding and battery component processing in the U.S.

Europe Laser Processing Market Trends

The Europe laser processing market is expected to witness significant growth over the forecast period. Europe’s automotive and industrial sectors are key contributors to market growth, with Germany and the UK at the forefront. The push for lightweight vehicles and sustainable practices has led to increased laser use in welding and cutting lightweight materials. Additionally, the European Union’s focus on reducing carbon emissions is driving the adoption of efficient laser technologies in manufacturing.

Asia Pacific Laser Processing Market Trends

The laser processing market in the Asia Pacific region is anticipated to register the highest CAGR over the forecast period. Asia Pacific is experiencing rapid growth in laser processing due to strong demand from electronics, automotive, and semiconductor industries, particularly in China, Japan, and South Korea. The region’s robust electronics manufacturing sector benefits from laser technology’s precision and efficiency, essential for high-volume production of micro-components. Government incentives to modernize manufacturing facilities and adopt Industry 4.0 technologies further fuel growth in laser processing.

Key Laser Processing Company Insights

Key players in the market, including IPG Photonics Corporation, Trumpf GmbH + Co. KG, Bystronic Laser AG, Amada Co., Ltd., and Coherent Inc., are actively pursuing strategies to expand their market footprint and enhance their competitive position. These companies are enhancing their product portfolios through strategic partnerships, mergers, acquisitions, and collaborations, while also developing advanced technologies that integrate AI to improve contract management and operational efficiency. This approach allows them to stay ahead of the growing demand for security and transparency in the industry. By continuously advancing their technological capabilities, these companies are positioning themselves to adapt to evolving market dynamics and maintain a strong competitive edge.

-

IPG Photonics Corporation is a global leader in high-performance fiber lasers, offering solutions for cutting, welding, marking, and engraving applications. The company specializes in high-power fiber lasers that are used across multiple industries, including automotive, aerospace, and manufacturing. IPG’s products are known for their precision, reliability, and efficiency, making them ideal for high-volume industrial production. The company also invests heavily in R&D to continue advancing its laser technology and expand its market reach.

-

Trumpf GmbH + Co is a prominent provider of laser technology and industrial machine tools, with a strong focus on laser cutting, welding, and additive manufacturing. Their laser systems are widely used in industries such as automotive, aerospace, and electronics for high-precision, high-speed applications. Trumpf specializes in both solid-state and fiber lasers, offering solutions tailored to the needs of various sectors. The company is also pioneering advancements in laser-based 3D printing, further establishing its leadership in the market.

Key Laser Processing Companies:

The following are the leading companies in the laser processing market. These companies collectively hold the largest market share and dictate industry trends.

- Altec GmbH

- Alpha Nov laser

- Amada Co., Ltd.

- Bystronic Laser AG

- Coherent Inc.

- Epilog Laser, Inc.

- Eurolaser GmbH

- Han's Laser Technology Industry Group Co., Ltd.

- IPG Photonics Corporation

- Newport Corporation (MKS Instruments, Inc.)

- LaserStar Technologies Corporation

- Coherent Inc.

- IPG Photonics Corporation

- Newport Corporation

- Trumpf GmbH + Co. KG

- Universal Laser Systems, Inc.

- Xenetech Global Inc.

Recent Developments

-

In January 2024, Coherent unveiled the OBIS 640 XT, a new red laser module that offers high output power, low noise, and excellent beam quality. This module complements their existing blue and green laser offerings, collectively enhancing the performance of high-performance SRM systems. The introduction of this product signifies Coherent's commitment to advancing laser technology for various applications.

-

In January 2024, Novanta Inc. acquired Motion Solutions, which is expected to facilitate the development of innovative intelligent subsystems by leveraging their combined technological capabilities. This acquisition aims to enhance their product offerings and create unique solutions tailored to customer needs. The integration of both companies' technologies presents exciting opportunities for future advancements in their respective markets.

-

In November 2023, IPG Photonics announced a strategic collaboration with Miller Electric Mfg. LLC to innovate in the handheld welding sector. This partnership aims to enhance laser technologies for welding applications, focusing on delivering efficient and precise solutions that meet modern demands. By combining their expertise, both companies strive to transform the landscape of handheld welding tools, ensuring reliability and improved performance for welders.

Laser Processing Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 26.56 billion

Revenue forecast in 2030

USD 42.73 billion

Growth rate

CAGR of 10.0% from 2025 to 2030

Actual data

2018 - 2024

Forecast period

2025 - 2030

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2030

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, process, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; Australia; South Korea; Brazil; UAE; South Africa; KSA

Key companies profiled

Bystronic Laser AG, Newport Corporation (MKS Instruments, Inc.); Xenetech Global Inc.; Coherent Inc.; Altec GmbH; Universal Laser Systems, Inc.; Amada Co., Ltd.; Han's Laser Technology Industry Group Co., Ltd.; Epilog Laser, Inc.; Trumpf GmbH + Co. KG; IPG Photonics Corporation; LaserStar Technologies Corporation; Alpha Nov Laser; Eurolaser GmbH.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Laser Processing Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global laser processing market based on product, process, end-use, and region:

-

Product Outlook (Revenue, USD Million; 2018 - 2030)

-

Gas Lasers

-

Solid-state Lasers

-

Fiber Lasers

-

Others

-

-

Process Outlook (Revenue, USD Million; 2018 - 2030)

-

Material Processing

-

Marking and Engraving

-

Micro-Processing

-

-

End-use Outlook (Revenue, USD Million; 2018 - 2030)

-

Automotive

-

Aerospace

-

Machine Tools

-

Electronics and Microelectronics

-

Medical

-

Packaging

-

-

Regional Outlook (Revenue, USD Million; 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

UAE

-

South Africa

-

Saudi Arabia

-

-

Frequently Asked Questions About This Report

The global laser processing market size was estimated at USD 23.69 billion in 2024 and is expected to reach USD 26.56 billion in 2025.

The global laser processing market is expected to grow at a compound annual growth rate of 10.0% from 2025 to 2030 to reach USD 442.73 billion by 2030.

Asia Pacific region dominated the laser processing market with a share of 38% in 2024. This is attributable to the government regulations that mandate the need for permanent & clear marks on consumer goods and the growing adoption of laser processing technology in the automotive sector.

Some key players operating in the laser processing market include Bystronic Laser AG, Newport Corporation (MKS Instruments, Inc.), Xenetech Global Inc., Coherent Inc., Altec GmbH, Universal Laser Systems, Inc., Amada Co., Ltd., Han's Laser Technology Industry Group Co., Ltd., Epilog Laser, Inc., Trumpf GmbH + Co. KG, IPG Photonics Corporation, LaserStar Technologies Corporation, Alpha Nov Laser, and Eurolaser GmbH

Key factors that are driving the laser processing market growth include increased usage of lasers in material processing applications across industrial & manufacturing sectors.

About the Author(s)

Electronic Devices Research Team

Semiconductors & Electronics · Electronic DevicesThis report was authored by the electronic devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the electronic devices segment of the semiconductors & electronics industry. All findings are based on proprietary semiconductors & electronics databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.