- Home

- »

- Next Generation Technologies

- »

-

Structured Cabling Market Size & Share Report, 2026-2033GVR Report cover

![Structured Cabling Market (2026 - 2033)Report]()

Structured Cabling Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product Type (Copper Cables, Fiber Optic Cables), By Application (LAN, Data Center), By Vertical (Government, Industrial), By Region, And Segment Forecasts

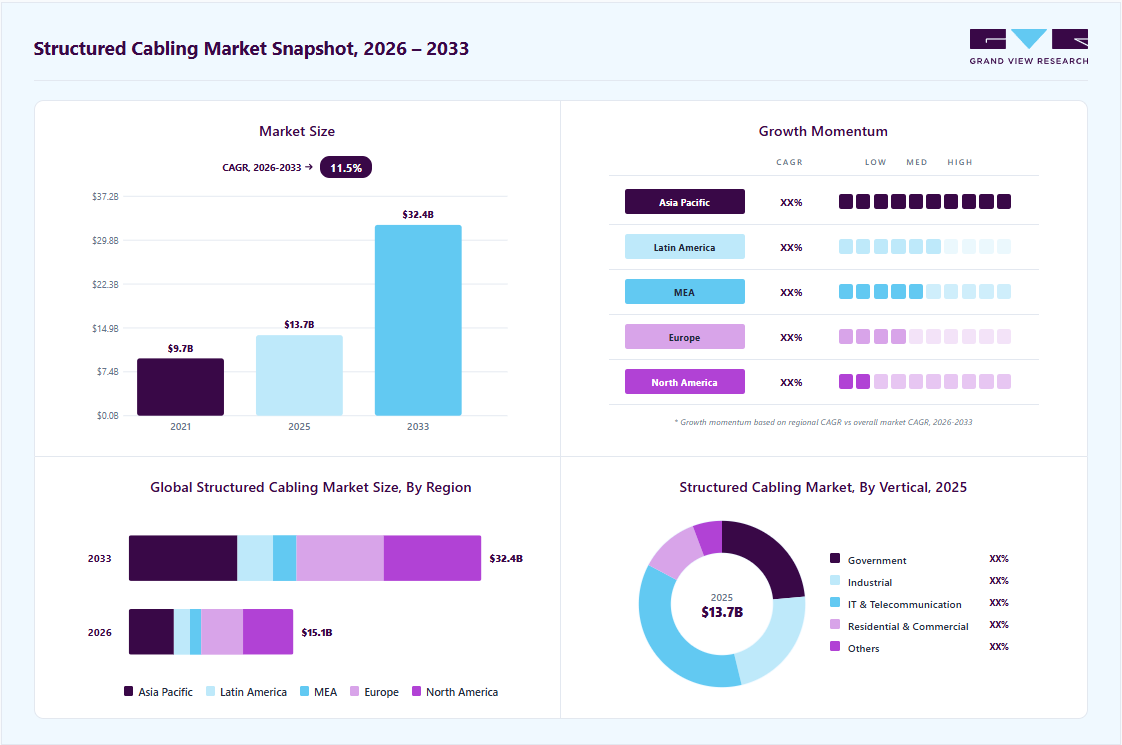

Market Size, 2025

$13.7BMarket Estimate, 2026

$15.1BMarket Forecast, 2033

$32.4BCAGR, 2026–2033

11.5%Structured Cabling Market Summary

The global structured cabling market size was valued at USD 13.7 billion in 2025 and is projected to grow from USD 15.1 billion in 2026 to USD 32.4 billion by 2033, growing at a CAGR of 11.5% from 2026 to 2033. North America dominated the global market with the largest revenue share of 31.0% in 2025. The market is growing due to the increasing demand for high-speed network connectivity, expansion of data center infrastructure, deployment of 5G networks, and rising adoption of smart buildings and digital transformation initiatives aimed at improving communication efficiency, network performance, and operational reliability.

Key Market Trends & Insights

- By Product Type: Copper Cables segment led the Market and held the largest revenue share of over 48.0% in 2025.

- By Application: LAN segment led the Market and held the largest revenue share of over 80.0% in 2025.

- By Vertical: IT & Telecommunication is expected to grow at the fastest CAGR of over 12.7% from 2026 to 2033.

Regional Highlights

- Largest regional market: North America (31.0% revenue share, 2025)

- Fastest growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 13.7 Billion

- Estimated market size in 2026: USD 15.1 Billion

- Projected market size by 2033: USD 32.4 Billion

- CAGR (2026-2033): 11.5%

The market comprises a range of cables and hardware components that form the backbone of telecommunication infrastructure. This infrastructure enables the transmission of voice, video, and data signals across networks. A reliable connection depends on various connecting devices and cabling systems that ensure seamless communication. Structured cabling systems are essential for building efficient and scalable network environments. These systems support consistent performance and ease of management across enterprise communication setups. Structured cabling providers are moving toward offering complete, end-to-end service integration.")

Local companies are bundling global cabling hardware with advisory, deployment, and ongoing support services. This approach improves efficiency and simplifies infrastructure management for end users. It also enables faster implementation and greater alignment with client needs. The trend is driving demand for flexible, full-suite cabling solutions that combine global quality with localized service delivery. For instance, in November 2024, TechAccess, a service- and solutions-oriented company in Dubai, partnered with Siemon to deliver advanced structured cabling and IT infrastructure solutions across South Africa. This partnership enables TechAccess to offer Siemon’s high-performance passive network technologies for data centers and smart buildings in the region.

The structured cabling market is undergoing a notable shift toward high-speed transmission systems, particularly Cat 6A, Cat 7, and fiber-optic solutions. This change is driven by the explosive growth in data consumption, driven by cloud computing, AI applications, and high-definition video streaming. These advanced cabling systems support greater bandwidth, reduced interference, and improved data integrity, making them ideal for large-scale enterprise networks and hyperscale data centers. As organizations scale their IT infrastructure to accommodate more devices and real-time analytics, older cabling standards are being phased out. The need for future-ready, high-performance connectivity probably to drive this trend forward.

Smart buildings are increasingly dependent on structured cabling systems to support interconnected devices, sensors, and automated systems. The widespread use of IoT technologies in lighting, security, HVAC, and energy management increases the demand for cabling capable of continuous, low-latency data transfer. Structured cabling offers a centralized, scalable, and reliable network foundation to power intelligent building functions. It enables simplified device integration, remote monitoring, and efficient space utilization. This trend is particularly strong in commercial real estate, healthcare, and educational institutions. As urban development moves toward sustainability and digital management, demand for structured cabling in smart buildings is likely to grow.

Market Dynamics

The structured cabling market is witnessing significant growth as organizations increasingly invest in high-performance network infrastructure to support digital transformation, cloud computing, data centers, smart buildings, and next-generation communication technologies. Structured cabling systems provide a standardized and scalable framework for transmitting voice, data, video, and other communication signals across commercial, industrial, residential, and institutional environments. These solutions include copper cabling, fiber optic cabling, connectors, patch panels, racks, and cable management systems that enable reliable and efficient network connectivity. The growing demand for high-speed data transmission, network scalability, and seamless communication is driving adoption across various industry verticals.

The structured cabling market is experiencing substantial growth due to the increasing demand for high-speed connectivity and the rapid expansion of data center infrastructure worldwide. Organizations are generating and processing unprecedented volumes of data, creating a strong need for robust and scalable network systems capable of supporting cloud services, artificial intelligence workloads, IoT devices, and real-time analytics. Structured cabling solutions provide the foundation for efficient network performance, enabling businesses to manage growing bandwidth requirements while ensuring reliability and flexibility.

Furthermore, the deployment of 5G networks, smart buildings, and digital workplaces is accelerating investments in advanced fiber optic and high-performance copper cabling systems. Enterprises are increasingly upgrading legacy network infrastructure to accommodate higher transmission speeds, improved network security, and future technology integration. As businesses continue to prioritize digital transformation initiatives, the demand for structured cabling solutions is expected to increase significantly.

Despite strong growth prospects, the structured cabling market faces challenges related to high installation costs and infrastructure deployment complexities. Implementing structured cabling systems often requires significant upfront investments in cables, connectors, network hardware, design planning, and professional installation services. Large-scale deployments across commercial buildings, industrial facilities, and data centers can further increase project costs and implementation timelines.

Additionally, upgrading existing legacy infrastructure can be complex, particularly in older buildings where space constraints and compatibility issues may require extensive modifications. Organizations may also face challenges related to network downtime during installation and maintenance activities. These factors can limit adoption among small and medium-sized enterprises and cost-sensitive end users, particularly in developing markets.

The growing adoption of smart buildings, intelligent infrastructure, and Industry 4.0 technologies presents significant growth opportunities for the structured cabling market. Enterprises and governments are increasingly investing in connected environments that integrate IoT devices, building automation systems, security solutions, energy management platforms, and high-speed communication networks. Structured cabling serves as the backbone of these digital ecosystems by providing reliable connectivity and supporting seamless data exchange.

Furthermore, increasing investments in hyperscale data centers, edge computing facilities, smart cities, renewable energy projects, and 5G infrastructure are creating new opportunities for structured cabling providers. The growing shift toward fiber optic networks, driven by rising bandwidth requirements and low-latency communication needs, is further supporting market expansion. As organizations continue to modernize network infrastructure and adopt advanced digital technologies, structured cabling solutions are expected to play a critical role in enabling future-ready connectivity and long-term operational efficiency.

Market Concentration & Characteristics

The structured cabling market is moderately fragmented, characterized by the presence of numerous global network infrastructure providers, cabling manufacturers, connectivity solution vendors, and regional installers competing across commercial, industrial, residential, and data center applications. The market includes established players such as CommScope, Corning Incorporated, Belden Inc., Legrand, Panduit Corporation, Nexans, and Siemon, alongside numerous regional manufacturers, distributors, and installation service providers.

Competition is driven by product performance, fiber optic innovation, compliance with industry standards, pricing, distribution networks, and the ability to support large-scale data center, enterprises and smart building deployments. While leading players maintain strong market positions through extensive product portfolios and global presence, the large number of regional and specialized vendors contributes to a competitive and fragmented market landscape.

Analyst Perspective

The Structured Cabling Market sits at the core of the global digital infrastructure ecosystem, driven by the increasing demand for high-speed connectivity, data center expansion, cloud computing, 5G deployment, and smart building initiatives. As organizations continue to modernize their network infrastructure to support growing data traffic, IoT devices, artificial intelligence applications, and real-time communications, structured cabling has evolved from a basic connectivity solution into a strategic foundation for digital transformation. The shift toward fiber-optic networks, hyperscale data centers, and intelligent building systems is further accelerating market growth, making structured cabling a critical enabler of scalable, reliable, and future-ready communication infrastructure across commercial, industrial, and residential environments.

Product Type Insights

Based on product type, the copper cables segment led the market with the largest revenue share of 48.0% in 2025, due to their cost-effectiveness and ease of installation. They are widely used in commercial buildings and legacy systems where short-distance data transmission is sufficient. Their proven reliability and low maintenance needs continue to make them a preferred choice for many network deployments. The market benefits from mature manufacturing processes and the wide availability of compatible hardware. Despite increasing demand for higher bandwidth, copper still meets the requirements of many enterprise networks. This continued relevance supports its dominant share across multiple structured cabling applications.

Fiber optic cables are experiencing rapid growth in the structured cabling market due to their superior bandwidth and transmission speeds. They are increasingly deployed in data centers, large campuses, and environments demanding high-speed, long-distance communication. The rise of cloud computing, AI workloads, and 5G infrastructure is fueling demand for fiber-based solutions. As organizations future-proof their networks, fiber’s scalability and low latency are becoming more attractive. Improvements in installation techniques and declining costs are also contributing to greater adoption. The growth trajectory indicates fiber optics is likely to capture a larger market share in the coming years.

Application Insights

Based on application, the LAN segment led the market with the largest revenue share of 80.0% in 2025 due to their widespread use in office buildings, schools, and enterprise campuses. LAN installations rely heavily on copper cabling, which remains cost-effective and efficient for short-distance connectivity. The market benefits from standardized designs and high demand for reliable internal data transfer. As organizations continue to upgrade their networks, LAN infrastructure sees consistent investment. Integration with IP-based services like VoIP and security systems also reinforces its importance. The segment maintains a strong presence due to its essential role in day-to-day business operations.

The data center application segment is witnessing strong growth in the structured cabling market due to increasing global demand for cloud computing and hyperscale infrastructure. Fiber optic cabling is being deployed extensively to support high-speed data transmission and scalability. Rising investments in colocation and edge data centers are accelerating adoption. Operators are prioritizing low-latency, high-density cabling to meet performance and efficiency requirements. Structured cabling ensures manageability and uptime in complex environments. As digital transformation continues, data centers are becoming a major growth area for advanced cabling solutions.

Vertical Insights

Based on vertical, the Government segment led the market with the largest revenue share of 23.5% in 2025. Increasing adoption of cloud services and 5G deployments is driving infrastructure upgrades. High-bandwidth cabling solutions are essential for supporting modern digital services. Telecom operators are expanding backbone networks and data centers, fueling demand. IT firms are upgrading to support real-time analytics and automation. The sector’s dynamic and technology-driven nature continues to generate consistent market expansion. This ongoing digital transformation is pushing enterprises to invest in scalable and future-ready structured cabling systems.

The industrial sector is witnessing growing demand for structured cabling systems. Rising automation and Industry 4.0 adoption are driving the need for high-speed, reliable communication networks. Manufacturing facilities require robust cabling to connect sensors, machines, and control systems. Structured cabling ensures minimal downtime and improved operational efficiency. Harsh industrial environments are prompting investment in durable cabling solutions. The push for smart factories is accelerating structured cabling deployments across industrial setups.

Regional Insights

North America dominated the Structured Cabling Market with the largest revenue share of 31.0% in 2025, due to high adoption of advanced IT infrastructure. The region’s strong presence of data centers and tech companies boosted demand. Enterprises continue investing in high-speed networks to support digital transformation. Government initiatives in smart cities also contributed to infrastructure upgrades. The mature market environment supports consistent cabling deployments across sectors.

U.S. Structured Cabling Market Trends

The structured cabling market in the U.S. held the largest share in the North America region in 2025. This was driven by sustained investment in hyperscale data centers and cloud infrastructure. Enterprises are upgrading networks to support hybrid work and AI-enabled operations. Government and education sectors are also contributing to demand through digital transformation initiatives.

Europe Structured Cabling Market Trends

Europe maintained a strong presence in the structured cabling market, with demand rooted in smart city initiatives and data localization regulations. Germany, the UK, and France are major contributors due to their industrial base and evolving digital policies. The region is adopting fiber-optic systems to meet higher bandwidth needs. Efforts to improve energy efficiency in buildings are also driving new cabling installations.

Asia Pacific Structured Cabling Market Trends

Asia Pacific is emerging as the fastest-growing region in the structured cabling market. Rapid digitization across manufacturing, education, and logistics sectors is fueling demand. Countries such as China and India are expanding fiber infrastructure to support 5G and cloud services. Increasing adoption of IoT and automation in Southeast Asia is driving new network requirements. Government investments in smart infrastructure are reinforcing cabling deployments.

Key Structured Cabling Company Insights

Some of the key companies in the Structured Cabling industry include ABB Ltd, Belden Inc., Corning Incorporated, Furukawa Electric Co., Ltd., Legrand SA, TE Connectivity Ltd., and others. Organizations are focusing on increasing customer base to gain a competitive edge in the industry. Therefore, key players are taking several strategic initiatives, such as mergers and acquisitions, and partnerships with other major companies.

-

ABB Ltd has been advancing its structured cabling offerings through integrated electrical and data systems. The company focuses on smart building solutions, enabling efficient data transmission across enterprise environments. ABB is expanding its product portfolio with modular cabling infrastructure for seamless scalability. Emphasis is being placed on high-speed connectivity and energy-efficient designs. Strategic projects across industrial automation and commercial buildings continue to drive its market presence.

-

Corning Incorporated is innovating in high-performance fiber-optic cabling systems tailored for data centers and hyperscale environments. The company is investing in solutions that support AI workloads, 5G infrastructure, and edge computing. Corning's EDGE™ and EDGE8® solutions offer modularity and fast deployment. Its focus on low-loss, high-density fiber technology enhances network capacity. The firm is also partnering with service providers to accelerate digital infrastructure rollouts.

Key Structured Cabling Companies

The following key companies have been profiled for this study on the structured cabling market.

-

ABB Ltd

-

Belden Inc.

-

CommScope Holding Company, Inc.

-

Corning Incorporated

-

Furukawa Electric Co., Ltd.

-

Legrand SA

-

Nexans

-

Schneider Electric

-

Siemens AG

-

TE Connectivity Ltd.

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (CommScope Holding Company, Inc., Corning Incorporated, Belden Inc., Legrand SA, Nexans, TE Connectivity Ltd., Furukawa Electric Co., Ltd.)

- They expand structured cabling portfolios through acquisitions, strategic partnerships, and investments in advanced fiber optic and copper connectivity technologies.

- Invest in AI-enabled network monitoring, smart cabling systems, and high-bandwidth fiber optic technologies to improve network scalability and operational efficiency.

- Strong global distribution networks, extensive product portfolios, established customer relationships, and significant investments in connectivity and network infrastructure R&D.

- Ability to deliver scalable and high-performance cabling infrastructure for data centers, smart buildings, telecom networks, and industrial facilities strengthens market competitiveness.

- Integration with legacy network infrastructure and existing cabling systems can slow the adoption of advanced structured cabling technologies.

- Complex installation requirements and high infrastructure upgrade costs may delay deployment of modern structured cabling solutions.

Emerging Players (ABB Ltd., Schneider Electric, Siemens AG)

- Integration challenges with legacy network infrastructure and outdated cabling systems can limit the adoption of advanced structured cabling technologies.

- Strict industry standards and complex infrastructure upgrade processes may delay large-scale deployment of modern structured cabling solutions.

- Faster development cycles support rapid adoption of advanced structured cabling technologies, including fiber optic networks, smart cabling systems, AI-enabled network monitoring, and high-speed connectivity solutions.

- Flexible and customer-focused strategies help differentiate solutions in niche applications such as hyperscale data centers, smart buildings, industrial automation, and telecom infrastructure networks.

- Limited financial resources and smaller operational scale can restrict investments in advanced structured cabling technologies, fiber optic infrastructure, and global expansion initiatives.

- Lower brand visibility and a limited enterprise and telecom customer base may reduce competitiveness in large-scale data center, smart building, and network infrastructure projects.

Recent Developments

-

In June 2025, CommScope Holding Company, Inc. launched its FiberREACH and CableGuide 360 solutions to address growing structured cabling needs. These offerings deliver high-power PoE and enhanced cable management for faster, denser, and more reliable enterprise network deployments.

-

In November 2024, Nexans partnered with BIMobject, a global digital content platform in Sweden, to integrate its products into Building Information Modeling (BIM), enabling early-stage inclusion in construction design. This partnership supports Nexans’ strategy to drive digital transformation in cabling and enhance efficiency, safety, and sustainability in building projects.

-

In January 2024, CommScope launched SYSTIMAX 2.0, introducing innovations such as GigaSPEED XL5 for multi-gigabit copper connectivity and VisiPORT for real-time port monitoring. These upgrades aim to future-proof structured cabling by enhancing performance, agility, and intelligent infrastructure management.

Structured Cabling Market Report Scope

Report Attribute

Details

Market size in 2025

USD 13.6 billion

Estimated market size in 2026

USD 15.1 billion

Projected market size by 2033

USD 32.4 billion

Growth rate

CAGR of 11.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product type, application, vertical, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; U.K; France; China; Japan; India; South Korea; Australia; Brazil; KSA; South Africa; UAE;

Key companies profiled

ABB Ltd., Belden Inc., CommScope Holding Company, Inc., Corning Incorporated, Furukawa Electric Co., Ltd., Legrand SA, Nexans, Schneider Electric, Siemens AG, TE Connectivity Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Structured Cabling Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global structured cabling market in terms of product type, application, vertical, and region.

-

Product Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Copper Cables

-

Fiber Optic Cables

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

LAN

-

Data Center

-

-

Vertical Outlook (Revenue, USD Million, 2021 - 2033)

-

Government

-

Industrial

-

IT & Telecommunication

-

Residential & Commercial

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Product Type

Revenue capture definition

Copper Cables

Revenue is generated through the supply and deployment of copper-based structured cabling solutions used for data transmission, voice communication, local area networking (LAN), and Power over Ethernet (PoE) applications across commercial buildings, enterprise networks, educational institutions, industrial facilities, and data centers.

Fiber Optic Cables

Revenue is generated through the supply and deployment of fiber optic cabling solutions used for high-speed data transmission, broadband connectivity, telecommunications networks, hyperscale and colocation data centers, enterprise networks, and 5G infrastructure.

Others

Revenue is generated through the sale and deployment of structured cabling components and accessories, including connectors, patch panels, racks, cabinets, cable trays, faceplates, outlets, cable management systems, and related installation hardware. These products support the efficient organization, management, and performance of network infrastructure across commercial buildings, industrial facilities, data centers, educational institutions, and telecommunications environments.

Segment - Application

Revenue capture definition

LAN

Revenue is generated through the installation and deployment of structured cabling solutions that support LAN connectivity in commercial, industrial, educational, healthcare, and government facilities. Additional revenue comes from network upgrades, expansion projects, maintenance services, and high-speed communication infrastructure deployments.

Data Center

Revenue is generated through the deployment of structured cabling infrastructure that supports data center networking, storage, and communication systems. Moreover, revenue comes from fiber optic and copper cabling installations, network expansion projects, high-density connectivity solutions, and ongoing maintenance and infrastructure upgrades.

Segment - Vertical

Revenue capture definition

Government

Revenue opportunities stem from the deployment of structured cabling infrastructure across government agencies, public institutions, defense facilities, and administrative buildings. Additional revenue is supported by network modernization initiatives, secure communication systems, smart governance projects, cybersecurity-focused infrastructure upgrades, and long-term maintenance and support contracts aimed at enhancing connectivity, security, and operational efficiency.

Industrial

Revenue in this segment is driven by the adoption of structured cabling systems that enable seamless connectivity across manufacturing plants, production facilities, warehouses, and industrial campuses. Growth is further supported by investments in industrial automation, smart manufacturing, machine-to-machine communication, Industrial IoT networks, and factory modernization projects that require reliable and scalable network infrastructure.

IT & Telecommunication

Revenue within this segment is primarily derived from the deployment of structured cabling infrastructure that supports high-speed data transmission, telecommunications networks, cloud computing environments, and enterprise connectivity solutions. Market growth is further fueled by investments in 5G network expansion, data center development, broadband infrastructure upgrades, and next-generation communication technologies requiring reliable and scalable network architectures.

Residential & Commercial

Revenue in this segment is generated by the installation of structured cabling systems in residential complexes, office buildings, retail establishments, hospitality facilities, and mixed-use developments. Demand is supported by the increasing adoption of smart building technologies, high-speed internet connectivity, integrated security systems, building automation solutions, and growing investments in modern construction and infrastructure projects.

Others

Revenue in this segment is supported by the deployment of structured cabling solutions across sectors such as education, healthcare, transportation, utilities, and public infrastructure.

Estimation Model

Layer Name

Key Question

Description

Infrastructure Demand Layer

Who requires structured cabling solutions?

Identify demand across enterprises, data centers, telecom operators, government facilities, industrial plants, healthcare institutions, educational campuses, and commercial buildings that require reliable network connectivity and communication infrastructure.

Network Deployment Layer

Who can deploy structured cabling systems?

Apply factors such as new construction activity, data center investments, smart building adoption, digital transformation initiatives, and network modernization projects to determine the addressable market for structured cabling solutions.

Adoption Layer

Who actively implements structured cabling infrastructure?

Apply enterprise network upgrade rates, fiber-optic migration trends, 5G deployment activity, cloud infrastructure expansion, and smart facility adoption benchmarks to estimate the number of organizations actively investing in structured cabling systems.

Monetization Layer

How much revenue is generated?

Multiply active deployment projects by spending on copper cabling, fiber optic cabling, connectors, patch panels, racks, installation services, maintenance contracts, and network infrastructure upgrades to estimate total market revenue.

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Data Center Infrastructure & Connectivity Assessment

Conducted a comprehensive analysis of hyperscale, colocation, enterprise, and edge data center deployments, evaluating demand for copper and fiber optic structured cabling, network architecture trends, and bandwidth requirements across global markets.

Helps stakeholders identify high-growth infrastructure segments, evaluate investment opportunities, and understand future connectivity requirements driven by cloud computing, AI workloads, and digital transformation initiatives.

Enterprise Network Modernization & End-User Adoption Analysis

Evaluated structured cabling adoption trends across IT & telecommunications, government, industrial, healthcare, education, and commercial sectors, including smart building integration, IoT deployments, and network upgrade initiatives.

Provides insights into key end-user demand patterns, emerging application areas, and industry-specific opportunities to support market expansion and strategic decision-making.

Technology Evolution & Competitive Landscape Assessment

Assessed advancements in fiber optic cabling, high-speed Ethernet technologies, Power over Ethernet (PoE), intelligent cabling systems, and 5G-ready network infrastructure, along with vendor strategies and competitive positioning.

Supports investment and growth strategies by identifying emerging technologies, evaluating competitive dynamics, and understanding the factors shaping long-term market development and innovation.

Frequently Asked Questions About This Report

Some key players operating in the structured cabling market include ABB; Belden Inc.; CommScope Holding Company, Inc.; Corning Incorporated; Furukawa Electric Co., Ltd.; Legrand SA; Nexans; Schneider Electric; and Siemon.

Key factors that are driving the structured cabling market growth include increased emphasis on cost and time management, growing IoT data, the need for automation of businesses, and increasing competition.

Copper cables held the largest revenue in 2025 while the Fiber Optic Cables is the fastest growing product in the market

LAN held the largest revenue in 2025 while the Data Center is the fastest growing product in the market

Government held the largest revenue in 2025 while the IT & Telecommunication is the fastest growing product in the market

Asia Pacific is the fastest growing region growing with CAGR 13.4% in forecast period 2026 to 2033

The global structured cabling market size was estimated at USD 13.6 billion in 2025 and is expected to reach USD 15.1 billion in 2026.

The global structured cabling market is expected to grow at a compound annual growth rate of 11.5% from 2026 to 2033 to reach USD 32.4 billion by 2033.

North America dominated the structured cabling market with a share of 31.0% in 2025. This is attributable to the strong presence of data centers and widespread adoption of high-speed connectivity infrastructure across the region.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.