- Home

- »

- Next Generation Technologies

- »

-

5G Fixed Wireless Access Market Size Report, 2026-2033GVR Report cover

![5G Fixed Wireless Access Market (2026 - 2033)Report]()

5G Fixed Wireless Access Market (2026 - 2033)

Size, Share & Trends Analysis Report By Offering (Hardware, Services), By Operating Frequency (Sub-6 GHz, 24-39 GHz), By Demography (Urban, Semi-Urban), By Application (Residential, Commercial), By Region, And Segment Forecasts

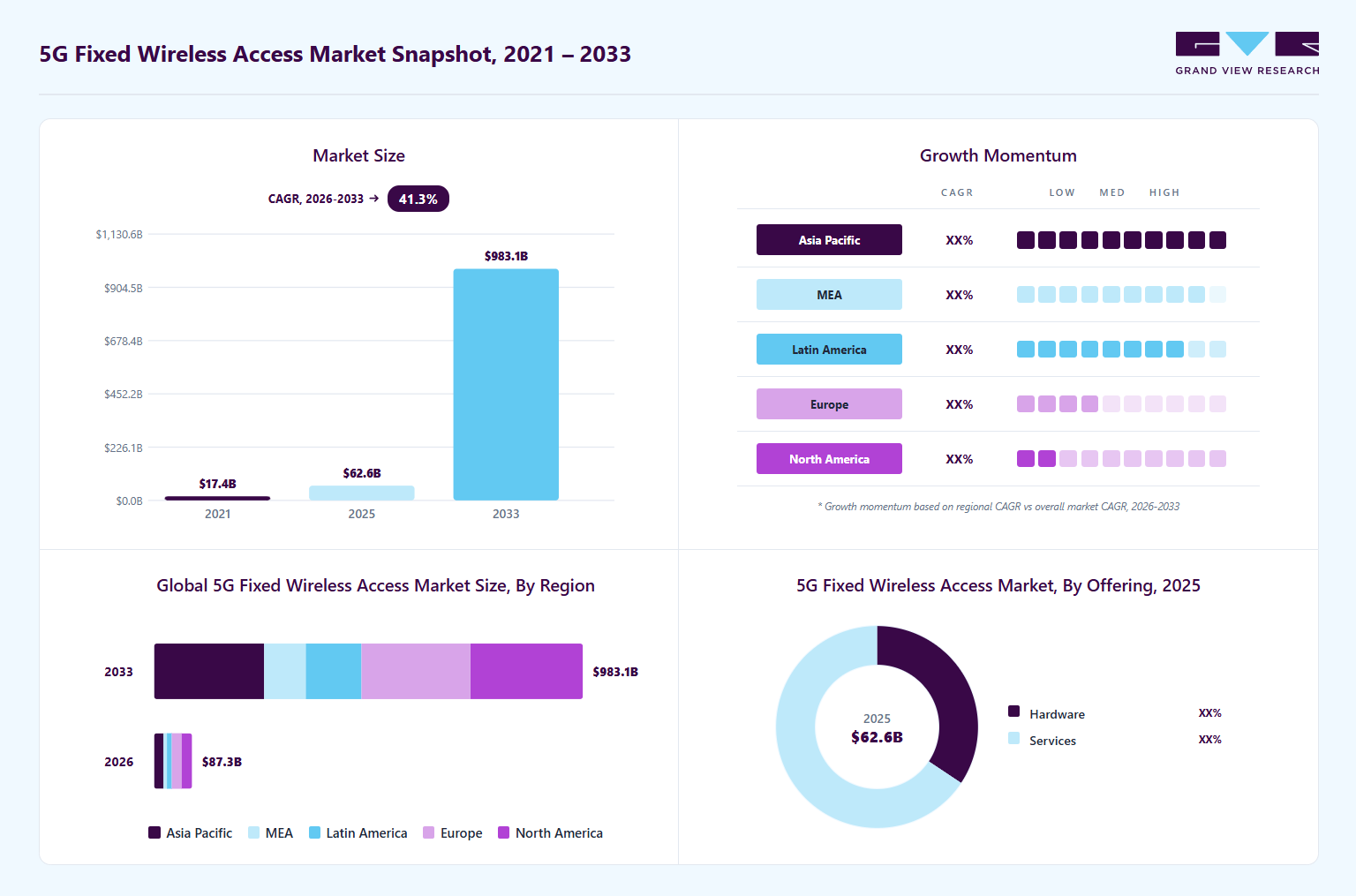

Market Size, 2025

$62.6BMarket Estimate, 2026

$87.3BMarket Forecast, 2033

$983.1BCAGR, 2026–2033

41.3%5G Fixed Wireless Access Market Summary

The global 5g fixed wireless access market size was valued at USD 62.6 billion in 2025 and is projected to grow from USD 87.3 billion in 2026 to USD 983.1 billion by 2033, at a CAGR of 41.3% from 2026 to 2033. The market in North America dominated with a revenue share of 27.7% in 2025. The rising need for high-speed internet access, as well as the increased usage of innovative technologies such as the millimeter-wave and Internet of Things (IoT) in 5G fixed wireless access (FWA) are driving the market growth.

Key Market Trends & Insights

- By offering: Services segment held the largest market share of 65.6% in 2025.

- By operating frequency: Sub-6 GHz segment held the largest market share in 2025.

- By demography: Urban segment held the largest market share in 2025.

- By application: Residential segment held the largest market share of 35.6% in 2025.

Regional Highlights

- Largest regional market: North America (27.7% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 62.6 Billion

- Estimated market size in 2026: USD 87.3 Billion

- Projected market size by 2033: USD 983.1 Billion

- CAGR (2026-2033): 41.3%

5G FWA technology uses the capabilities of 5G networks to offer high-speed internet services to households and businesses without the need for physical fiber connections. At the same time, the trend toward remote work and online learning is likely to boost the demand for high-speed internet access. This is projected to fuel additional expansion in the market as solution providers continue to explore cost-effective solutions to address the rising demand for high-speed internet access.")

Numerous 5G FWA access solution providers are focusing on releasing advanced solutions to accommodate the rising demand from various consumers globally. For instance, Mavenir, a telecommunications software company, launched its Fixed Wireless Access (FWA) solution that supports 5G Non-Standalone (NSA), 5G Standalone (SA), and 4G deployments. Mavenir stated that its FWA system also supports massive Multiple Input Multiple Output (MIMO) radio technology and 5G millimeter-wave (mmWave) frequency bands. According to Mavenir, several clients, including RINA Wireless, 360 Communications, and Triangle Communications in the U.S., have implemented their FWA solution.

The expansion of 5G coverage is expected to drive the growth of the market. With the advent of 5G technology, FWA has become a popular option for delivering high-speed internet to homes and businesses in areas where fiber or cable infrastructure is limited. With 5G, wireless connectivity can be delivered at gigabit speeds, making it a viable alternative for wired broadband services. As 5G networks continue to expand and reach more users there will be an increase in the adoption of the 5G FWA technology, particularly in areas where wired infrastructure is limited or non-existent.

Private networks are becoming increasingly crucial for enterprises that need to ensure secure and reliable connectivity. With 5G FWA, enterprises can set up private networks that are not reliant on wired infrastructure, making them more flexible and easier to deploy. As a result, it is expected that there will be an increase in the adoption of 5G FWA for private networks, particularly in industries such as manufacturing, logistics, and energy. Moreover, the integration of 5G FWA with edge computing is also expected to revolutionize industries such as healthcare, manufacturing, and transportation and create new use cases for smart cities and homes.

The growth of the Internet of Things (IoT) and smart home devices also drives demand for high-speed broadband connectivity, thereby contributing to market growth. With 5G FWA, devices can be connected directly to the internet and communicate with each other in real time without the need for a wired connection. This creates a more connected and efficient home environment, where devices can communicate with each other to automate tasks and improve the user experience. Service providers are developing specialized 5G FWA packages for IoT and smart home devices to meet the unique needs of these markets. However, 5G FWA technology can be expensive to deploy, particularly for service providers who need to build out new infrastructure, which is a significant factor that is expected to impact the market growth.

Market Dynamics

The rising deployment of standalone (SA) 5G networks and the expansion of high-speed broadband connectivity infrastructure are driving the growth of the 5G fixed wireless access (FWA) industry by enabling service providers to deliver fiber-like internet speeds with lower deployment costs and faster rollout timelines. Telecom operators are increasingly investing in 5G standalone architecture, millimeter-wave (mmWave) spectrum, Massive MIMO technologies, beamforming systems, and cloud-native core networks to enhance wireless broadband coverage and network performance. The growing demand for high-speed internet services across residential, commercial, industrial, and remote locations is further accelerating the adoption of 5G FWA solutions, particularly in regions where fiber-optic infrastructure remains limited or economically unfeasible.

The increasing shift toward digital lifestyles, remote work environments, online education platforms, video streaming services, cloud gaming, and connected smart home ecosystems is significantly increasing broadband consumption globally. In addition, telecom providers are increasingly utilizing 5G FWA as a cost-effective alternative to fiber deployments to rapidly expand broadband penetration in rural and underserved areas. The integration of edge computing, AI-driven network optimization, network slicing, and private wireless networks is also enhancing the performance and scalability of 5G FWA deployments for enterprise and industrial applications.

High infrastructure deployment costs and spectrum-related challenges are restraining the growth of the market by increasing the operational and capital expenditure requirements for telecom operators and service providers. The deployment of 5G FWA networks requires significant investments in spectrum acquisition, base stations, small cells, fiber backhaul connectivity, Massive MIMO antennas, and advanced customer premises equipment (CPE). In addition, mmWave-based 5G deployments require dense network architectures due to limited signal propagation and reduced penetration capabilities, which further increases infrastructure complexity and deployment expenses.

The growing adoption of private 5G networks and industrial digital transformation initiatives is creating significant growth opportunities for the market by increasing the demand for secure, high-speed, and low-latency wireless connectivity solutions across enterprise environments. Industries such as manufacturing, mining, oil & gas, utilities, transportation, logistics, healthcare, and smart cities are increasingly deploying private 5G FWA networks to support mission-critical operations, industrial automation, autonomous systems, and real-time data processing applications. The ability of 5G FWA technology to provide flexible and rapidly deployable broadband connectivity without extensive wired infrastructure is further accelerating enterprise adoption.

Market Concentration & Characteristics

The 5G fixed wireless access (FWA) market industry is moderately concentrated, with the presence of several global telecommunications equipment providers, network infrastructure companies, chipset manufacturers, and wireless broadband service providers accounting for a significant share of the market. Leading companies compete based on network performance, spectrum capabilities, customer premises equipment (CPE) portfolios, geographic coverage, pricing strategies, and the ability to deliver high-speed and low-latency broadband connectivity solutions. Major market participants dominate the industry through strong 5G infrastructure portfolios, extensive operator partnerships, advanced radio access network (RAN) technologies, and continuous investments in cloud-native networking, mmWave solutions, and AI-driven network optimization platforms.

Strategic collaborations, spectrum partnerships, product launches, mergers and acquisitions, and long-term agreements between telecom operators and infrastructure vendors are common across the industry as companies aim to strengthen their market presence and expand 5G broadband coverage. Leading players are increasingly focusing on integrating advanced technologies such as Massive MIMO, beamforming, Open RAN, AI-enabled network management, edge computing, and cloud-native 5G core platforms to improve network efficiency, scalability, and service quality. In addition, the increasing adoption of private 5G networks, industrial automation, smart city infrastructure, and IoT-enabled applications is encouraging market participants to expand enterprise-focused FWA solutions and next-generation wireless edge connectivity platforms.

Offering Insights

The services segment accounted for the largest share of 65.6% in 2025. With the increasing proliferation of data-intensive applications and the rise of the Internet of Things (IoT), businesses and consumers are demanding faster and more reliable connectivity. The low latency and high bandwidth of 5G FWA networks make them an ideal solution for meeting these demands, and service providers are rapidly expanding their offerings to meet this demand. In addition to basic connectivity, service providers are offering value-added services, such as cloud-based services which can be accessed remotely, enterprise connectivity, IoT services, and more. As these services become more widespread, the services segment of the 5G FWA market is expected to grow and account for a substantial market share in the future.

The hardware segment is expected to grow at a significant CAGR during the forecast period. Improved Customer Premises Equipment (CPE) and access units are an important trend driving the growth of the hardware segment in the market. CPE refers to the hardware devices that are located on the customer's premises, such as modems or routers, and are used to connect to the 5G FWA network. Hardware manufacturers are investing in developing improved CPE to meet the needs of consumers and businesses. Additionally, the ability of the CPEs to integrate with smart home features to control smart home devices, such as thermostats, security cameras, and lighting, is a significant factor driving the segment's growth.

Operating Frequency Insights

The Sub-6 GHz segment held the largest market share in 2025. The ability of the Sub-6 GHz operating frequency to offer enhanced coverage through obstacles like buildings and walls more effectively and offer better connectivity for indoor and outdoor environments is a major factor driving the segment growth. Sub-6 GHz spectrum has better propagation characteristics, which is particularly important for indoor coverage, where higher frequency bands can struggle to provide consistent and reliable signal strength. Moreover, by using the Sub-6 GHz operating frequency for 5G FWA deployments, network operators can provide high-speed, low-latency internet connectivity to remote areas without the need for extensive fiber infrastructure.

The 24-39 GHz segment is expected to grow at the fastest CAGR during the forecast period. The rising demand for high bandwidth availability for better internet connectivity is a major factor driving the segment growth. The 24-39 GHz operating frequency offers higher bandwidth compared to the Sub-6 GHz spectrum which means that it can provide faster internet speeds and support a greater number of devices simultaneously. Moreover, the 24-39 GHz spectrum has lower latency which makes them important for applications that require real-time responsiveness, such as online gaming and video conferencing.

Demography Insights

The urban segment dominated the market in 2025. Several factors such as increasing demand for high-speed broadband, growing adoption of smart city initiatives, rising number of connected devices, and advancements in the 5G technology are the major factors driving the growth of the 5G FWA solutions in urban areas. With the increasing reliance on internet-based services, the demand for high-speed broadband in urban areas has significantly increased. Moreover, as the number of connected devices is expected to increase significantly in the coming years, particularly in urban areas, 5G FWA solutions can support a large number of connected devices, which is essential for applications such as the Internet of Things (IoT) and smart home automation.

The semi-urban segment is projected to grow at the fastest CAGR over the forecast period. Students in semi-urban areas require high-speed internet access to participate in virtual classrooms and access educational resources. 5G FWA solutions can provide a reliable and fast internet connection, which is essential for online learning. At the same time, the rising adoption of e-commerce is on the rise in semi-urban areas, which has created a need for reliable internet access, making it an ideal option for consumers who need to shop online. Such factors bode well for the growth of the segment over the forecast period.

Application Insights

The residential segment dominated the market in 2025. Factors such as the growing adoption of smart home technology, the rise in remote work and telecommuting, and the rising demand for high-speed broadband are the major factors contributing to the segment growth. As more people rely on internet-based services for work, entertainment, and communication, there is a growing demand for high-speed broadband in residential areas. 5G FWA provides faster internet speeds and more reliable connectivity than traditional wired broadband services, making it an attractive option for residential consumers. Such factors bode well for the growth of the segment in the forecast period.

The commercial segment is expected to rise significantly over the forecast period. The growing advancements in IoT technology and the increasing adoption of video conferencing solutions are significant factors driving the segment growth. As businesses rely more on cloud-based services, the demand for high-speed internet is growing. 5G FWA can provide faster internet speeds and more reliable connectivity than traditional wired broadband services, making it an attractive option for commercial consumers, Moreover, due to the rise of remote work, the use of video conferencing is becoming more common in commercial applications.

Regional Insights

The North America 5G fixed wireless access industry accounted for 27.7% share of the overall market in 2025. Rising investments in 5G infrastructure is a major factor driving regional growth. North America is seeing significant investments in 5G infrastructure, including the deployment of small cells, fiber-optic cables, and other network components. Moreover, the North American government is supporting the deployment of 5G technology through various initiatives and policies aimed at improving network infrastructure. Such factors bode well for the region's growth over the forecast period.

U.S. 5G Fixed Wireless Access Industry Trends

The U.S. 5G fixed wireless access industry held a dominant position in 2025.As traditional broadband infrastructure, such as fiber, often proves costly and time-consuming to deploy in these regions, FWA has emerged as a cost-effective and scalable alternative.

Europe 5G Fixed Wireless Access Industry Trends

The 5G Fixed Wireless Access (FWA) industry in Europe is propelled by the region's growing emphasis on enhancing broadband connectivity and closing the digital divide. With a significant portion of rural areas still underserved by traditional fiber or cable networks, FWA presents a cost-effective and efficient alternative for delivering high-speed internet. European Union initiatives, such as the Digital Decade targets, are driving investments in advanced network infrastructure, including 5G FWA, to achieve widespread gigabit connectivity by 2030. Additionally, the increasing reliance on remote work, e-learning, and digital entertainment is fueling demand for flexible and scalable broadband solutions, positioning FWA as a key component of Europe’s digital strategy.

The German 5G fixed wireless access industry is expected to experience significant growth in the coming years, driven by the German government’s “Gigabit Germany” initiative aims to provide high-speed internet to rural and underserved regions, where traditional broadband options are often limited or unavailable.

Asia Pacific 5G Fixed Wireless Access Industry Trends

The Asia Pacific 5G fixed wireless industry held a significant share in 2025. Countries such as China, India, and Japan are taking charge, each focusing on addressing specific connectivity challenges. Urban areas are seeing increased demand for high-speed alternatives to traditional broadband, while rural regions benefit from FWA's cost-effectiveness and ease of deployment. Government-backed digital initiatives, rising smartphone penetration, and the surge in data consumption from activities like video streaming, remote work, and IoT adoption are fueling growth. The Asia-Pacific region’s diverse economies and widespread investments in 5G infrastructure position it as a global hub for FWA innovation and deployment.

The China 5G fixed wireless access industry held a substantial market share in 2025. China's 5G Fixed Wireless Access (FWA) market is driven by the country’s rapid deployment of 5G networks and its commitment to being a global leader in next-generation connectivity. With robust government support and significant investments by leading telecom providers, such as China Mobile, China Telecom, and China Unicom, FWA is being deployed to enhance broadband penetration, particularly in rural and remote areas. The growing adoption of smart cities, industrial IoT, and advanced digital services is further fueling demand for high-speed internet solutions, making FWA a critical component of China’s broader 5G strategy.

The India 5G fixed wireless access industry held a significant share in 2025. India's 5G FWA market is experiencing rapid growth, driven by the country’s increasing focus on improving digital infrastructure and closing the connectivity gap. Telecom operators such as Jio and Bharti Airtel are investing heavily in 5G rollouts, targeting both urban and rural areas where traditional wired broadband is limited. Government initiatives, including the "Digital India" program, are accelerating the adoption of cost-effective technologies like FWA to bring high-speed internet to underserved regions.

Key 5G Fixed Wireless Access Company Insights

Some of the major players in the 5G fixed wireless access industry include Verizon Communications Inc., Huawei Technologies Co., Ltd., Nokia, and Telefonaktiebolaget LM Ericsson, among others. These companies are at the forefront of driving advancements in 5G FWA technology, leveraging strategic initiatives such as partnerships, acquisitions, and investments in research and development to strengthen their market positions. By expanding their product portfolios and collaborating with key stakeholders, they aim to address the rising demand for reliable, high-speed broadband solutions in both urban and rural markets. Their focus on innovation is crucial in enabling cost-effective deployment and improved connectivity to support the growing reliance on data-intensive applications across industries.

-

Verizon Communications Inc. has emerged as a prominent company in the 5G FWA space, with its "5G Home Internet" and "5G Business Internet" offerings providing high-speed connectivity to underserved areas. Verizon continues to invest heavily in expanding its 5G Ultra Wideband network while collaborating with technology providers to enhance the user experience. Its focus on millimeter wave (mmWave) technology enables faster data speeds and improved capacity, making it a strong player in the FWA market.

Huawei Technologies Co., Ltd. is leveraging its expertise in telecommunications to drive 5G FWA adoption globally. The company offers an extensive portfolio of FWA solutions designed to deliver high-speed broadband to rural and hard-to-reach areas. Huawei's strategic investments in R&D and its partnerships with telecom operators worldwide underline its commitment to enabling seamless connectivity. Its innovations in Massive MIMO and AI-based optimization have further enhanced the efficiency of its FWA offerings.

Key 5G Fixed Wireless Access Companies:

The following key companies have been profiled for this study on the 5G fixed wireless access market.

-

Huawei Technologies Co., Ltd.

-

Telefonaktiebolaget LM Ericsson

-

Nokia

-

Samsung

-

Inseego Corp.

-

Qualcomm Technologies, Inc

-

Intel Corporation

-

MediaTek Inc.

-

COMMSCOPE

-

Verizon Communications Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Huawei Technologies Co., Ltd., Telefonaktiebolaget LM Ericsson, Samsung, Verizon Communications Inc.

- Mature players focus on deploying integrated 5G FWA ecosystems supported by advanced radio access network (RAN) infrastructure, extensive spectrum assets, cloud-native core networks, and large-scale broadband service capabilities.

- Strategies emphasize expansion of standalone 5G networks, mmWave deployments, Open RAN integration, AI-enabled network optimization, and partnerships with telecom operators.

- Strong global telecom infrastructure presence with extensive 5G network deployment capabilities and large broadband subscriber bases.

- Ability to provide end-to-end FWA solutions including network infrastructure, chipsets, spectrum capabilities, customer premises equipment (CPE).

- High infrastructure deployment costs and spectrum acquisition expenses may impact profitability and return on investment.

- Regulatory restrictions, cybersecurity concerns, and geopolitical trade limitations in certain regions may affect market expansion and vendor adoption.

Emerging Players: Inseego Corp., Qualcomm Technologies, Inc, Intel Corporation, MediaTek Inc., COMMSCOPE

- Emerging and specialized players focus on developing advanced FWA chipsets, indoor and outdoor CPE devices, wireless access technologies, edge computing platforms, and enterprise broadband connectivity solutions.

- Strategies emphasize cost-efficient deployments, software-defined networking, AI-enabled wireless optimization.

- Strong focus on innovation in semiconductor platforms, CPE technologies, wireless edge computing, and AI-driven connectivity solutions.

- Faster product development cycles and flexibility in addressing niche FWA applications including enterprise connectivity, industrial IoT, and private 5G networks.

- Limited ownership of telecom infrastructure and spectrum assets compared with global telecom operators and network equipment leaders.

- • Dependence on telecom operator partnerships and broader 5G network expansion for market growth opportunities.

Recent Developments

-

In April 2026, Nokia announced that Inseego will acquire Nokia’s Fixed Wireless Access (FWA) CPE business, subject to regulatory approvals and customary closing conditions. The acquisition is expected to nearly double Inseego’s revenue and strengthen its position in the global wireless broadband market across fixed wireless, mobile broadband, and cloud-managed connectivity solutions. As part of the agreement, both companies plan to collaborate on joint go-to-market initiatives and innovation programs focused on 6G, wireless edge computing, AI-driven connectivity, and carrier 5G monetization opportunities. Nokia will receive an equity stake in Inseego and make an additional investment, bringing its ownership interest to approximately 11%, reflecting a long-term strategic partnership between the two companies. The initiative also aligns with Nokia’s broader strategy to simplify its operations and focus on AI-driven network infrastructure and next-generation connectivity solutions.

-

In February 2025, AxyomCore launched its cloud-native 5G Core solution designed specifically for Fixed Wireless Access (FWA) services to help service providers address rising broadband demand. The company stated that the platform combined both 5G and 4G technologies, including SMF/PGW-C control plane and UPF/PGW-U user plane functionalities, to deliver high capacity, strong throughput, scalability, and improved quality of service for FWA deployments. The solution was developed to support mobile service providers in expanding broadband connectivity across rural and high-growth urban areas while enabling high-performance internet access for millions of subscribers. AxyomCore highlighted that the growing adoption of 5G FWA services in the U.S., with hundreds of thousands of new subscribers added quarterly, was driving demand for scalable and efficient wireless broadband infrastructure solutions.

5G Fixed Wireless Access Market Report Scope

Report Attribute

Details

Market size in 2025

USD 62.6 billion

Estimated market size in 2026

USD 87.3 billion

Projected market size by 2033

USD 983.1 billion

Growth rate

CAGR of 41.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company market share, competitive landscape, growth factors, and trends

Segments covered

Offering, operating frequency, demography, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Huawei Technologies Co., Ltd.; Telefonaktiebolaget LM Ericsson; Nokia; Samsung; Inseego Corp.; Qualcomm Technologies, Inc; Intel Corporation; MediaTek Inc.; COMMSCOPE; Verizon Communications Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global 5G Fixed Wireless Access Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global 5G fixed wireless access market report based on offering, operating frequency, demography, application, and region.

-

Offering Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Hardware

-

Customer Premises Equipment (CPE)

-

Indoor CPE

-

Outdoor CPE

-

-

Access Units

-

Femto Cells

-

Pico Cells

-

-

-

Services

-

-

Operating Frequency Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Sub-6 GHz

-

24-39 GHz

-

Above 39 GHz

-

-

Demography Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Urban

-

Semi-Urban

-

Rural

-

-

Application Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Residential

-

Commercial

-

Industrial

-

Oil & Gas

-

Mining

-

Utility

-

Others

-

-

Government

-

-

Regional Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

5G Fixed Wireless Access (FWA) Market Opportunity Assessment

Country/region-wise fixed wireless access market sizing and growth forecasts in terms of volume (Thousand Units) and revenue (USD Million) across North America, Europe, Asia Pacific, Latin America, and MEA

Assessment of regulatory frameworks impacting 5G FWA deployment including spectrum allocation policies, broadband expansion initiatives

Identified region-specific growth opportunities in underserved broadband markets

Supported telecom operators and broadband service providers in network expansion and subscriber growth planning

5G Fixed Wireless Access Technology & Deployment Behavior Study

Analysis of enterprise and residential 5G FWA adoption patterns across standalone (SA) and non-standalone (NSA) network architectures

Evaluation of operating frequency adoption trends across Sub-6 GHz, 24-39 GHz, and above 39 GHz bands

Improved segmentation of 5G FWA demand by technology, operating frequency, deployment model, and device type

Supported product positioning strategies for CPE manufacturers, chipset providers, and telecom infrastructure vendors

Competitive Benchmarking and Strategic Positioning in the 5G Fixed Wireless Access Market

Comparative assessment of telecom operator partnerships, 5G infrastructure investments, spectrum ownership, subscriber base expansion, and broadband monetization strategies

Analysis of market share across residential, commercial, industrial, and government end-use applications

Identified competitive white spaces in rural broadband connectivity, private wireless networks, and high-frequency mmWave deployments

Supported strategic partnership development among telecom operators, infrastructure vendors, semiconductor companies, and CPE providers

Frequently Asked Questions About This Report

The services segment led with a 65.6% revenue share in 2025.

The sub-6 GHz segment held the largest revenue share in 2025, while the 24-39 GHz is the fastest-growing segment.

The urban segment held the largest revenue share in 2025, while semi-urban is the fastest-growing demography.

Residential segment dominated the market and accounted for the largest revenue share (over 35.0%) in 2025.

The global 5g fixed wireless access market size was valued at USD 62.6 billion in 2025 and is estimated at USD 87.3 billion for 2026.

The global 5g fixed wireless access market is expected to grow at a CAGR of 41.3% from 2026 to 2033, reaching USD 983.1 billion by 2033.

Key players include Huawei Technologies Co., Ltd.; Telefonaktiebolaget LM Ericsson; Nokia; Samsung; Inseego Corp.; Qualcomm Technologies, Inc; Intel Corporation; MediaTek Inc.; COMMSCOPE; Verizon Communications Inc.

Key factors driving the 5G fixed wireless access market growth include rising demand for high-speed internet, advancements in 5G technology, the rise of remote working, and the expansion of 5G network coverage.

North America dominated the 5G fixed wireless access with a share of 27.7% in 2025. Rising investments in 5G infrastructure is a major factor driving the regional growth.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.