- Home

- »

- Advanced Interior Materials

- »

-

Aerospace Insulation Market Size & Share Report 2026-2033GVR Report cover

![Aerospace Insulation Market (2026 - 2033)Report]()

Aerospace Insulation Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Ceramic Materials, Fiberglass), By Product (Thermal Insulation, Acoustic Insulation), By Application (Engine, Aerostructure), By End-use, By Region, And Segment Forecasts

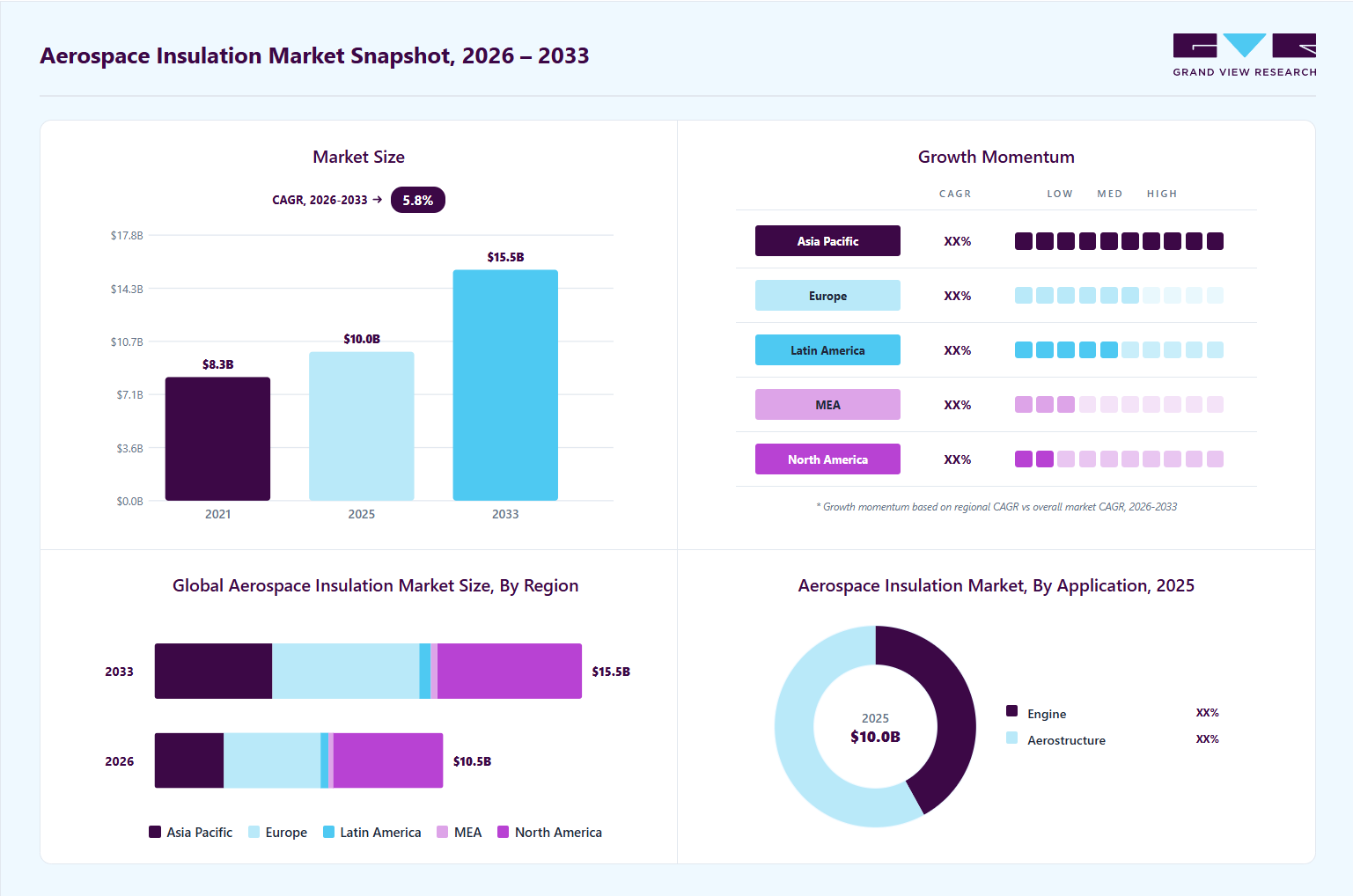

Market Size, 2025

$10.0MMarket Estimate, 2026

$10.5MMarket Forecast, 2033

$15.5MCAGR, 2026–2033

5.8%Aerospace Insulation Market Summary

The global aerospace insulation market size was valued at USD 10.0 billion in 2025 and is projected to grow from USD 10.5 billion in 2026 to USD 15.5 billion by 2033, growing at a CAGR of 5.8% from 2026 to 2033. North America dominated the global market with the largest revenue share of 38.7% in 2025. The global aerospace industry is experiencing a strong push towards lightweight components to improve fuel efficiency and reduce emissions.

Key Market Trends & Insights

- By material: Ceramic materials segment led the market with the largest revenue share of 50.1% in 2025.

- By product: Thermal insulation segment led the market with the largest revenue share of 66.7% in 2025.

- By application: Aerostructure segment led the market with the largest revenue share of 58.0% in 2025.

- By end-use: Commercial segment led the market with the largest revenue share of 59.6% in 2025.

Regional Highlights

- Largest regional market: North America (38.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The aerospace insulation market in the U.S. held the largest share in the North America region in 2025.

Market Size & Forecast

- Market Size in 2025: USD 10.0 Billion

- Estimated Market Size in 2026: USD 10.5 Billion

- Projected Market Size by 2033: USD 15.5 Billion

- CAGR (2026-2033): 5.8%

Aerospace insulation materials, such as advanced composites and foams, play a critical role in achieving these goals by minimizing aircraft weight while maintaining thermal and acoustic performance. Airlines and aircraft manufacturers are increasingly adopting high-performance insulation to comply with regulatory frameworks and reduce operational costs. This shift is significantly driving the demand for innovative insulation materials across commercial, military, and business aviation sectors.Governments and international aviation authorities have imposed stringent regulations regarding cabin safety, fire resistance, and thermal management. Materials used in aerospace insulation must meet specific standards, such as FAR 25.853 for flammability and toxicity. These regulatory requirements have accelerated innovation in insulation materials that not only enhance passenger safety but also meet environmental standards. As compliance becomes more critical in aircraft design and retrofitting, the demand for certified insulation products continues to grow.

")

The global increase in air travel, particularly in emerging economies, is propelling the need for new aircraft and fleet modernization. As airlines expand their fleets to accommodate the rising number of passengers, the demand for aerospace insulation for both new builds and refurbishments has surged. Additionally, aircraft retrofitting projects aimed at enhancing comfort and energy efficiency are contributing to the steady demand for advanced insulation solutions, further stimulating market growth.

Ongoing research and development in aerospace insulation technologies have resulted in the introduction of next-generation materials such as aerogels, ceramic fibers, and vacuum insulation panels. These advanced materials offer superior thermal and acoustic insulation properties while reducing bulk and weight. Technological innovations are allowing manufacturers to meet the evolving requirements of modern aircraft cabins, cargo holds, engines, and fuselage components, thus playing a crucial role in expanding the market's scope and application areas.

Market Dynamics

The Aerospace Insulation Market is experiencing significant growth due to increasing aircraft production, rising demand for fuel-efficient and lightweight aerospace components, growing investments in commercial and military aviation, and stringent safety and thermal management requirements. Aerospace insulation materials play a critical role in controlling cabin temperatures, reducing noise, improving fire protection, and enhancing overall aircraft performance. The expansion of global air passenger traffic, fleet modernization programs, and increasing aircraft deliveries are further supporting market growth. Additionally, advancements in high-performance insulation materials, including ceramic-based insulation, fiberglass, mineral wool, and advanced polymer composites, enabling improved thermal resistance, weight reduction, and compliance with evolving aerospace safety standards.

The increasing focus on lightweight aircraft design and fuel efficiency is a major factor driving the aerospace insulation market. Aircraft manufacturers are continuously seeking advanced materials that can reduce overall aircraft weight while maintaining high levels of thermal insulation, acoustic performance, and fire resistance. Aerospace insulation materials help improve energy efficiency by minimizing heat transfer, reducing environmental control system loads, and enhancing passenger comfort. The growing production of next-generation commercial aircraft, business jets, and military aircraft is creating strong demand for advanced insulation solutions.

Furthermore, rising environmental concerns and stringent emission reduction targets are encouraging airlines and aircraft manufacturers to adopt lightweight materials that improve fuel economy and lower operating costs. The expansion of low-cost carriers, increasing air travel demand, and ongoing fleet replacement programs are further accelerating aircraft production worldwide. As aerospace companies continue investing in innovative lightweight materials and energy-efficient aircraft technologies, demand for aerospace insulation is expected to increase significantly over the coming years.

The aerospace insulation market faces challenges related to stringent certification requirements, complex testing procedures, and high manufacturing costs. Aerospace insulation materials must comply with rigorous aviation safety standards concerning fire resistance, smoke toxicity, thermal performance, durability, and environmental exposure. Achieving certification from aviation regulatory authorities often requires extensive testing and validation processes, increasing product development timelines and costs.

The growing development of sustainable aviation technologies and next-generation aircraft platforms is creating substantial growth opportunities for the aerospace insulation market. Increasing investments in electric aircraft, hybrid-electric propulsion systems, urban air mobility vehicles, and hydrogen-powered aircraft are generating demand for advanced thermal and acoustic insulation materials capable of supporting new aircraft architectures. These emerging platforms require highly efficient insulation solutions to manage heat, improve safety, and optimize system performance.

Market Concentration & Characteristics

The aerospace insulation market exhibits distinct structural characteristics shaped by innovation intensity, regulatory mandates, and end user dynamics. A high degree of innovation defines the competitive landscape, with manufacturers investing heavily in advanced materials such as aerogels, nanocomposites, and lightweight foams to meet evolving demands for energy efficiency, fire safety, and noise reduction. This innovation is crucial for compliance with strict international aviation regulations set by bodies like the FAA and EASA, which govern material flammability, toxicity, and environmental impact. As a result, market players with strong R&D capabilities and proprietary technologies are better positioned to gain a competitive advantage and secure contracts with aircraft OEMs and defense organizations.

In terms of market concentration, the aerospace insulation industry is relatively consolidated, with a few major players catering to large aircraft manufacturers and MRO (maintenance, repair, and overhaul) providers. The level of mergers and acquisitions is moderately high, driven by the need to strengthen technological portfolios and global supply chains. End user concentration is also significant, as aerospace insulation suppliers typically serve a small number of large customers such as Boeing, Airbus, and national defense agencies. The threat of substitutes remains low due to the specialized performance requirements in aviation, further reinforcing the importance of certified, application-specific insulation materials.

Analyst Perspective

The aerospace insulation market is transitioning from a traditional insulation materials segment toward a technology-driven market focused on lightweighting, thermal efficiency, fire safety, and next-generation aerospace platforms. The strongest growth opportunities are emerging from commercial aircraft fleet expansion, military modernization programs, urban air mobility vehicles, electric and hybrid-electric aircraft, and increasing investments in space exploration. The key differentiator for companies will not be insulation material availability alone, but their ability to develop lightweight, high-performance, and regulatory-compliant solutions while maintaining cost competitiveness and manufacturing scalability.

Players with advanced material technologies, strong relationships with aircraft OEMs, extensive certification capabilities, diversified aerospace exposure, and global supply chain networks are likely to capture premium margins and long-term growth opportunities. In contrast, smaller and less diversified participants may remain vulnerable to lengthy qualification cycles, stringent regulatory requirements, raw material price fluctuations, high development costs, and intense competition from established aerospace material suppliers.

Material Insights

Based on material, the ceramic materials segment led the market with the largest revenue share of 50.1% in 2025 and is expected to grow at a CAGR of 6.3% over the forecast period, driven by its exceptional thermal resistance and stability under extreme conditions. Ceramics can withstand high operating temperatures, making them ideal for applications in aircraft engines, exhaust systems, and heat shields. As aircraft designs evolve toward higher engine efficiency and compactness, the need for insulation materials that can perform reliably in elevated thermal environments is becoming increasingly critical.

The fiberglass segment is anticipated to experience significant CAGR growth during the forecast period. Fiberglass insulation materials are widely used in aircraft fuselages, cargo compartments, and cabin interiors to minimize heat transfer and dampen noise levels. The material’s high fire resistance and compliance with stringent aviation safety regulations make it a preferred choice among OEMs and MRO providers. Additionally, the affordability and ease of fabrication of fiberglass contribute to its growing adoption in both commercial and military aviation sectors. The increasing demand for fuel-efficient aircraft further promotes the use of lightweight fiberglass insulation solutions to reduce overall aircraft weight and emissions.

Product Insights

Based on product, the thermal insulation segment led the market with the largest revenue share of 66.7% in 2025 and is expected to grow at a CAGR of 5.8% over the forecast period, driven by the critical need to maintain optimal temperature conditions within aircraft cabins and systems. In high-altitude environments, where external temperatures can drop drastically, effective thermal insulation ensures passenger comfort, crew safety, and the protection of onboard electronic and mechanical systems. Airlines and aircraft manufacturers prioritize advanced insulation materials that can withstand extreme thermal variations while minimizing heat loss or gain.

The electric insulation segment is anticipated to experience the fastest CAGR during the forecast period, driven by the increasing electrification of aircraft systems. As aerospace manufacturers shift toward more electric aircraft (MEA) to reduce emissions and improve fuel efficiency, the demand for advanced electric insulation materials has grown significantly. These materials are critical for ensuring the safety, reliability, and performance of electrical systems in both commercial and military aircraft.

End Use Insights

Based on end-use, the commercial segment led the market with the largest revenue share of 59.6% in 2025 and is expected to grow at a CAGR of 6.4% over the forecast period, driven by rising demand for enhanced passenger comfort and in-flight experience. Airlines are increasingly focusing on noise reduction, cabin temperature control, and vibration dampening to improve the quality of long-haul and short-haul flights. This has led to a surge in the adoption of advanced acoustic and thermal insulation materials that ensure quieter, safer, and more comfortable cabin environments.

The military segment is anticipated to experience significant CAGR growth during the forecast period, driven by rising defense budgets and continuous modernization of military aircraft fleets. Governments across key regions such as the United States, China, India, and NATO countries are heavily investing in upgrading fighter jets, transport aircraft, and surveillance systems. These modern aircraft demand high-performance insulation materials that offer thermal resistance, noise suppression, and protection against fire in extreme environments.

Application Insights

Based on application, the aerostructure segment led the market with the largest revenue share of 58.0% in 2025 and is expected to grow at a CAGR of 5.4% over the forecast period. Modern aircraft engines generate immense heat, making insulation essential to protect surrounding components, ensure operational stability, and prevent heat-related system failures. Advanced insulation materials such as ceramic composites and high-temperature foams help maintain engine efficiency and longevity.

The aerostructure segment is anticipated to experience significant CAGR growth during the forecast period, driven by increasing emphasis on lightweight construction and fuel efficiency. As aircraft manufacturers seek to reduce overall aircraft weight to meet stricter carbon emission regulations, the demand for advanced insulation materials within aerostructures such as fuselage, wings, and empennage-has grown significantly. These insulation materials are designed to offer thermal resistance without compromising structural integrity or increasing mass.

Regional Insights

North America dominated the aerospace insulation market with the largest revenue share of 38.7% in 2025. The market in North America is primarily driven by robust investments in defense and commercial aviation. The presence of key aircraft manufacturers, such as Boeing and Bombardier, supports steady demand for advanced thermal and acoustic insulation. Growing environmental regulations focused on reducing carbon emissions are prompting the use of lightweight insulation materials. Additionally, the region’s strong MRO (Maintenance, Repair, and Overhaul) network stimulates demand for retrofit insulation solutions. Increasing adoption of composite materials further complements market expansion.

U.S. Aerospace Insulation Market Trends

The aerospace insulation market in the U.S. held the largest share in the North America region in 2025. The U.S. aerospace insulation market is fueled by extensive defense spending and continued investment in next-generation aircraft programs, including hypersonic and unmanned aerial vehicles. NASA and the U.S. Air Force are key drivers in the use of advanced aerospace insulation for high-performance and space applications. Moreover, stringent FAA regulations for cabin comfort, safety, and energy efficiency push OEMs to innovate in thermal and acoustic insulation. The rising trend of domestic air travel post-COVID has also led to increased demand for aircraft retrofitting and refurbishing. These factors collectively reinforce market growth.

Asia Pacific Aerospace Insulation Market Trends

The Asia Pacific aerospace insulation market witnesses growth driven by rapid expansion in commercial aviation and defense modernization programs. Countries like India, South Korea, and Australia are increasingly investing in domestic aerospace manufacturing and procurement. Insulation demand is also influenced by rising passenger traffic and the need for fleet expansion by regional airlines. Furthermore, government initiatives supporting local aircraft production and partnerships with global aerospace firms are enhancing insulation technology integration. The cost-sensitive nature of the market also pushes for lightweight and affordable insulation solutions.

China aerospace insulation market benefits from the government’s push toward self-reliance in aerospace technology. Major programs such as COMAC’s C919 and ARJ21 have significantly increased demand for domestic production of insulation materials. Rapid growth in air travel and urbanization necessitates the expansion of commercial airline fleets, directly impacting insulation usage. The country’s dual focus on civilian and military aerospace sectors contributes to demand diversity. In addition, advancements in high-speed rail and space exploration further stimulate innovation in high-performance insulation.

Europe Aerospace Insulation Market Trends

Europe's aerospace insulation market is driven by its strong focus on sustainable aviation and emissions reduction. Airbus, one of the world’s largest aircraft manufacturers, leads regional adoption of advanced thermal and acoustic insulation technologies. The European Union's Green Deal and associated aviation sustainability targets are influencing insulation designs that improve fuel efficiency and reduce noise pollution. Moreover, the presence of a mature airline industry and a well-established MRO network supports ongoing demand for both OEM and retrofit insulation solutions. Continuous R&D investment enhances competitiveness.

Germany aerospace insulation market stands out as a key hub within Europe for aerospace insulation innovation, thanks to its advanced engineering capabilities and strong industrial base. The country’s collaboration between academic research institutes and aerospace OEMs fosters cutting-edge insulation material development. Demand is also driven by Germany’s involvement in major European aircraft programs, including Airbus and space missions through the European Space Agency (ESA). Additionally, domestic efforts to boost aerospace exports and improve aircraft energy efficiency contribute to steady market growth.

Central & South America Aerospace Insulation Market Trends

The Central & South America aerospace insulation market is propelled by increasing demand for regional and low-cost air travel. Brazil, home to Embraer, is a significant contributor, particularly in the regional jet segment. The need to modernize older aircraft fleets in the region encourages retrofitting, boosting demand for insulation upgrades. Although budget constraints remain, international partnerships and investments in airport infrastructure help stimulate market activity. Growing environmental awareness is also encouraging interest in sustainable insulation materials.

Middle East & Africa Aerospace Insulation Market Trends

The Middle East & Africa aerospace insulation market growth is mainly driven by the rapid expansion of airline fleets by carriers like Emirates, Qatar Airways, and Etihad. High investments in aviation infrastructure and airport modernization projects increase demand for insulated aircraft components. The region’s harsh climate necessitates effective thermal insulation for passenger comfort and equipment protection. Additionally, increasing defense budgets in the Gulf countries contribute to the demand for military aircraft insulation. Africa’s gradual aviation development, supported by foreign investment, presents long-term growth potential.

Key Aerospace Insulation Company Insights

Some key companies involved in the aerospace insulation market include Duracote Corporation, Rogers Corporation, DuPont, BASF SE, 3M, Esterline Technologies Corporation, Triumph Group Inc., Zodiac Aerospace, Evonik Industries, and Polymer Technologies Inc. Companies are expanding their business to achieve a competitive edge in the marketplace. Major companies are implementing mergers and acquisitions and establishing alliances with other leading companies to achieve this goal.

-

Duracote Corporation is a U.S.-based manufacturer specializing in advanced materials for aerospace and transportation applications. The company offers thermal, acoustic, and fire-resistant insulation materials designed to meet FAA and OEM specifications. Its Dura-THERM and Dura-Sonic product lines are widely used in aircraft interiors, cargo liners, and engine components. Duracote’s focus on lightweight, flame-retardant solutions support aircraft performance and regulatory compliance.

-

Rogers Corporation is a global materials technology company known for its high-performance foam and elastomeric products. In aerospace, it provides thermal insulation and vibration-damping solutions through its PORON and BISCO materials. These products are used in aircraft seals, gaskets, cabin insulation, and engine components. Rogers emphasizes lightweight, durable materials that enhance energy efficiency and passenger comfort.

Key Aerospace Insulation Companies:

The following are the leading companies in the aerospace insulation market. These companies collectively hold the largest market share and dictate industry trends.

- Duracote Corporation

- Rogers Corporation

- Dupont

- BASF SE

- 3M

- Esterline Technologies Corporation

- Triumph Group Inc.

- Zodiac Aerospace

- Evonik Industries

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (DuPont, BASF SE, 3M, Rogers Corporation, Evonik Industries)

Focus on long-term contracts with aircraft OEMs and defense contractors.

Invest heavily in R&D for lightweight, fire-resistant, and high-temperature insulation materials.

Expand global manufacturing and certification capabilities to meet aerospace standards.

Strong brand recognition, established aerospace certifications, and extensive distribution networks.

Broad product portfolios covering thermal, acoustic, and electrical insulation requirements.

Significant financial resources enabling continuous innovation and capacity expansion.

Higher operational costs and complex organizational structures can slow innovation cycles.

Dependence on large aerospace programs may expose revenues to aircraft production fluctuations.

Lengthy product qualification and approval processes increase time-to-market.

Emerging Players (Duracote Corporation, Esterline Technologies Corporation, Zodiac Aerospace)

Target specialized insulation applications and niche aerospace programs.

Emphasize customized solutions and rapid product development cycles.

Form partnerships with aerospace suppliers and technology developers to gain market access.

Greater flexibility in addressing unique customer requirements and emerging aerospace technologies.

Ability to focus on advanced materials such as aerogels, specialty composites, and next-generation insulation systems.

Faster decision-making and responsiveness to evolving aerospace design needs.

Limited production scale and lower bargaining power with major OEMs.

Smaller R&D budgets compared to global industry leaders.

Challenges in obtaining certifications and achieving widespread adoption across commercial aerospace platforms.

Aerospace Insulation Market Report Scope

Report Attribute

Details

Market size in 2025

USD 10.0 billion

Estimated market size in 2026

USD 10.5 billion

Projected market size by 2033

USD 15.5 billion

Growth rate

CAGR of 5.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, product, application, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; Brazil

Key companies profiled

Duracote Corporation; Rogers Corporation; Dupont; BASF SE; 3M; Esterline Technologies Corporation; Triumph Group Inc.; Zodiac Aerospace; Evonik Industries

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Aerospace Insulation Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global aerospace insulation market report based on material, product, application, end use and region:

-

Material Outlook (Revenue, USD Million, 2021 - 2033)

-

Ceramic Materials

-

Mineral Wool

-

Foamed Plastics

-

Fiberglass

-

Others

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Thermal Insulation

-

Acoustic Insulation

-

Electric Insulation

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Engine

-

Aerostructure

-

-

End use Outlook (Revenue, USD Million, 2021 - 2033)

-

Commercial

-

Military

-

Business & General Aviation

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Central & South America

-

Brazil

-

-

Middle East & Africa

-

Research Methodology

The aerospace insulation market market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each aerospace insulation segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Material

Revenue capture definition

Ceramic Materials

Revenue generated from the sale of ceramic-based aerospace insulation materials used for thermal protection, fire resistance, and high-temperature applications in aircraft and spacecraft. This segment captures revenues from ceramic insulation products supplied to aircraft manufacturers, maintenance providers, and aerospace component suppliers requiring lightweight, heat-resistant materials for engines, exhaust systems, thermal barriers, and critical aerospace structures across commercial, military, business aviation, and space applications.

Mineral Wool

Revenue generated from the sale of mineral wool aerospace insulation materials utilized for thermal and acoustic insulation in aerospace systems. This segment captures revenues from mineral wool products supplied to aircraft manufacturers and aerospace OEMs requiring effective heat management, sound attenuation, and fire-resistant insulation solutions for cabins, fuselage structures, equipment compartments, and auxiliary systems across various aerospace platforms.

Foamed Plastic

Revenue generated from the sale of foamed plastic insulation materials used in aerospace applications requiring lightweight thermal and acoustic performance. This segment captures revenues from polyurethane, polyimide, polyethylene, and other aerospace-grade foamed insulation products supplied to aircraft manufacturers, interior system providers, and maintenance organizations for cabin insulation, environmental control systems, and structural components across commercial and military aircraft.

Fiberglass

Revenue generated from the sale of fiberglass-based aerospace insulation materials designed for thermal protection, acoustic control, and fire resistance. This segment captures revenues from fiberglass insulation products supplied to aerospace OEMs, aircraft interior manufacturers, and maintenance service providers requiring durable, lightweight insulation solutions for fuselage sections, cabins, cargo areas, and aircraft equipment compartments.

Others

Revenue generated from the sale of other aerospace insulation materials, including aerogels, advanced polymer composites, silica-based materials, and specialty insulation products not categorized under ceramic materials, mineral wool, foamed plastic, or fiberglass. This segment captures revenues from innovative insulation solutions supplied to aerospace manufacturers and technology developers seeking enhanced thermal performance, weight reduction, and multifunctional insulation capabilities for advanced aerospace applications.

Segment - Product

Revenue capture definition

Thermal Insulation

Revenue generated from the sale of aerospace thermal insulation products designed to minimize heat transfer and maintain temperature stability within aircraft and aerospace systems. This segment captures revenues from insulation solutions supplied to aircraft manufacturers, engine producers, and aerospace integrators requiring thermal management for engines, cabins, fuselage structures, environmental control systems, and high-temperature aerospace components.

Acoustic Insulation

Revenue generated from the sale of aerospace acoustic insulation products used to reduce noise transmission and improve passenger and crew comfort. This segment captures revenues from sound-absorbing and noise-dampening insulation solutions supplied to aircraft OEMs, cabin interior manufacturers, and aerospace maintenance providers for use in passenger cabins, cockpit areas, fuselage structures, and aircraft interior systems.

Electric Insulation

Revenue generated from the sale of aerospace electrical insulation products used to protect electrical systems, wiring networks, and electronic components from heat, electrical leakage, and environmental exposure. This segment captures revenues from insulation materials supplied to aerospace electronics manufacturers, aircraft OEMs, and system integrators requiring safe and reliable electrical protection solutions for avionics, power distribution systems, sensors, and next-generation electric aircraft platforms.

Segment - Application

Revenue capture definition

Engine

Revenue generated from the sale of aerospace insulation materials used in aircraft and spacecraft engine systems requiring thermal protection, fire resistance, and operational efficiency. This segment captures revenues from insulation products supplied to engine manufacturers, aerospace OEMs, and maintenance providers for turbines, nacelles, exhaust systems, engine compartments, and propulsion-related components across commercial, military, and business aviation applications.

Aerostructure

Revenue generated from the sale of aerospace insulation materials utilized in aircraft structural components, including fuselage sections, wings, floor panels, bulkheads, and cargo compartments. This segment captures revenues from insulation solutions supplied to aerospace manufacturers and structural component suppliers requiring thermal control, acoustic management, moisture protection, and fire safety performance throughout aircraft structures.

Segment - End Use

Revenue capture definition

Commercial

Revenue generated from the sale of aerospace insulation materials used in commercial aviation aircraft, including passenger aircraft, cargo aircraft, and regional jets. This segment captures revenues from insulation products supplied to commercial aircraft manufacturers, airlines, maintenance organizations, and aerospace suppliers requiring thermal, acoustic, and fire protection solutions to enhance passenger comfort, safety, and operational efficiency.

Military

Revenue generated from the sale of aerospace insulation materials used in military aircraft, helicopters, unmanned aerial vehicles, and defense aerospace systems. This segment captures revenues from insulation solutions supplied to defense contractors, military aircraft manufacturers, and government agencies requiring high-performance thermal, acoustic, and fire-resistant materials capable of operating under demanding mission and environmental conditions.

Business & General Aviation

Revenue generated from the sale of aerospace insulation materials used in business jets, private aircraft, turboprops, light aircraft, and general aviation platforms. This segment captures revenues from insulation products supplied to aircraft manufacturers, charter operators, and aviation service providers seeking lightweight, high-performance thermal and acoustic solutions that improve cabin comfort, safety, and aircraft efficiency.

Others

Revenue generated from the sale of aerospace insulation materials used in aerospace applications not categorized under commercial, military, or business and general aviation sectors, including spacecraft, satellites, launch vehicles, urban air mobility platforms, and specialized aerospace systems. This segment captures revenues from advanced insulation solutions supplied to space agencies, aerospace technology developers, and emerging aviation manufacturers requiring specialized thermal and environmental protection capabilities.

Estimation Model

Layer Name

Key Question

Description

Aircraft Production & Fleet Expansion Analysis

How large is the addressable demand base for aerospace insulation materials?

Assesses global aircraft production, fleet size, aircraft deliveries, fleet modernization activities, and retirement trends across commercial, military, business aviation, and space sectors. This layer establishes the potential demand for aerospace insulation based on aircraft manufacturing volumes and aerospace industry expansion.

Insulation Penetration & Application Analysis

How extensively are insulation materials utilized across aerospace platforms?

Evaluates the adoption and usage intensity of thermal, acoustic, and electrical insulation across key aircraft applications including engines, aerostructures, cabins, cargo compartments, avionics systems, and propulsion components. This layer determines insulation consumption per aircraft platform and application area.

Material Mix & Technology Assessment

Which insulation materials contribute to market revenues and how is the material mix evolving?

Analyzes demand distribution among ceramic materials, mineral wool, foamed plastics, fiberglass, aerogels, and other advanced insulation materials. The assessment considers performance requirements, regulatory compliance, lightweighting trends, fire resistance standards, and technological advancements influencing material selection across aerospace programs.

Revenue Modeling & Market Validation

What is the total market value generated from aerospace insulation sales?

Quantifies market revenues by integrating aircraft production data, insulation consumption patterns, material pricing, replacement demand, aftermarket requirements, and regional aerospace manufacturing activity. The final market size is validated through manufacturer revenues, supplier analysis, aerospace spending trends, and expert interviews to ensure accurate estimation and forecasting.

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Defense Modernization & Military Aviation Demand Assessment

Evaluated insulation demand generated by military aircraft procurement programs, defense modernization initiatives, fighter jet production, rotorcraft upgrades, and unmanned aerial vehicle development across key defense spending countries.

Helps clients identify defense-driven growth opportunities, prioritize high-investment regions, and align product development strategies with long-term military aviation requirements.

Regulatory Compliance & Aerospace Certification Benchmarking

Conducted detailed assessment of FAA, EASA, military aviation standards, fire safety regulations, smoke and toxicity requirements, thermal performance standards, and aircraft certification processes influencing aerospace insulation material adoption across major regions.

Supports market entry and expansion strategies by identifying regulatory barriers, certification requirements, compliance costs, and opportunities in regions with favorable aerospace manufacturing and aviation safety frameworks.

Competitive Landscape & OEM Procurement Strategy Assessment

Analyzed procurement trends of leading aircraft manufacturers, insulation supplier positioning, strategic partnerships, product differentiation strategies, certification advantages, and innovation developments across the aerospace insulation value chain.

Supports competitive positioning, partnership development, customer acquisition strategies, and identification of market gaps that can generate long-term revenue opportunities.

Frequently Asked Questions About This Report

The aerospace insulation market size was estimated at USD 10.0 billion in 2025 and is expected to reach USD 10.5 billion in 2026.

The aerospace insulation market is expected to grow at a CAGR of 5.8% from 2026 to 2033 to reach USD 15.5 billion by 2033.

The thermal insulation segment dominated the global aerospace insulation market, accounting for a revenue share of 66.7% in 2025, driven by the critical need to maintain optimal temperature conditions within aircraft cabins and systems.

Some of the key players operating in the aerospace insulation market include Duracote Corporation; Rogers Corporation; Dupont; BASF SE; 3M; Esterline Technologies Corporation; Triumph Group Inc.; Zodiac Aerospace, and Evonik Industries.

Commercial segment led the market with the largest revenue share of 59.6% in 2025 while military is segment is second fastest growing market

North America dominated with a 38.7% revenue share in 2025.

Ceramic materials segment led the market with the largest revenue share of 50.1% in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key factors driving the aerospace insulation market include increasing aircraft production, growing demand for lightweight and fuel-efficient aircraft, stringent aviation fire safety regulations, rising commercial and military aviation investments, and advancements in high-performance thermal and acoustic insulation materials.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.