- Home

- »

- Advanced Interior Materials

- »

-

Copper Mining Market Size, Share & Growth Report, 2026-2033GVR Report cover

![Copper Mining Market (2026 - 2033)Report]()

Copper Mining Market (2026 - 2033)

Size, Share & Trends Analysis Report By End Use (Building & Construction, Transportation, Consumer Products, Electrical & Electronics, Machinery & Equipment), By Region, And Segment Forecasts

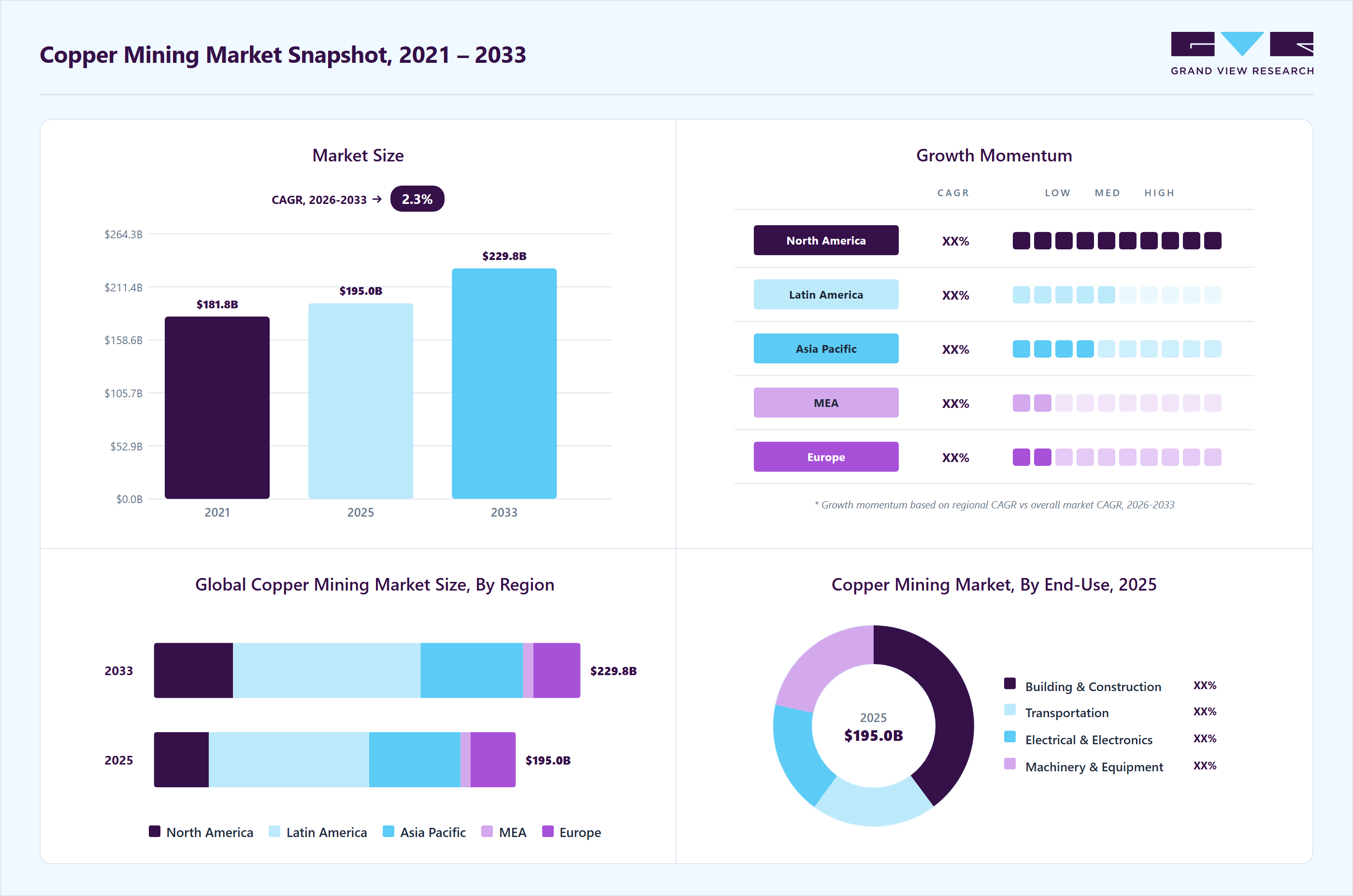

Market Size, 2025

$195.0BMarket Estimate, 2026

$195.8BMarket Forecast, 2033

$229.8BCAGR, 2026–2033

2.3%Copper Mining Market Summary

The global copper mining market size was valued at USD 195.0 billion in 2025 and is projected to grow from USD 195.8 billion in 2026 to USD 229.8 billion by 2033, at a CAGR of 2.3% from 2026 to 2033. The Latin America market held the largest share of 44.3% of the global market in 2025. This steady growth is primarily driven by rising demand from electrification trends, including electric vehicles, renewable energy infrastructure, and power grid expansion.

Key Market Trends & Insights

- By end use: The building and construction segment accounted for the largest share of the market in 2025.

Regional Highlights

- Largest regional market: Latin America (44.3% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 195.0 Billion

- Estimated market size in 2026: USD 195.8 Billion

- Projected market size by 2033: USD 229.8 Billion

- CAGR (2026-2033): 2.3%

However, market expansion is likely to be constrained by declining ore grades, high capital investment requirements, and prolonged project development timelines. Sustainability has become a central focus in the copper mining industry, with companies increasingly adopting environmentally responsible practices to reduce their carbon footprint and comply with stringent regulations. Mining operators are investing in renewable energy integration, water recycling systems, and tailings management solutions to minimize environmental impact. In addition, there is a growing emphasis on responsible sourcing and ESG compliance, driven by investor expectations and downstream industries seeking low-carbon copper for applications such as electric vehicles and clean energy systems.")

Technological advancements are playing a critical role in enhancing efficiency, safety, and productivity across copper mining operations. The adoption of automation, artificial intelligence, and advanced data analytics is enabling real-time monitoring, predictive maintenance, and optimized resource extraction. Furthermore, innovations such as autonomous haulage systems, ore-sorting technologies, and digital twin models are helping mining companies improve recovery rates while reducing operational costs. These advancements are particularly important in addressing challenges such as declining ore grades and increasing operational complexity.

Drivers, Opportunities & Restraints

The market is being propelled by strong demand from electrification, renewable energy deployment, and electric vehicle production, all of which require substantial copper intensity. This demand outlook is reflected in large-scale capital investments across the industry; for instance, on March 19, 2026, Freeport-McMoRan announced plans to advance permitting for a USD 7.5 billion expansion of its El Abra copper mine in Chile to increase long-term production capacity. Such investments highlight the strategic importance of copper in supporting global energy transition goals, particularly as governments and corporations continue to allocate significant funding toward grid modernization and clean energy infrastructure.

The market presents notable opportunities through emerging supply sources, innovative financing mechanisms, and technological advancements aimed at addressing future shortages. On April 8, 2026, a new initiative in Africa proposed a USD 100-200 million sustainability-linked financing program to formalize artisanal copper mining and integrate it into global supply chains, improving both output and traceability. In addition, the same date saw the announcement of a USD 1 billion merger to develop deep-sea mining capabilities targeting copper-rich seabed resources. These developments indicate expanding investment channels and diversification of supply, which could play a crucial role in meeting the anticipated global copper deficit.

The market continues to face constraints from environmental regulations, operational risks, and lengthy project development timelines, all of which increase costs and delay supply additions. Regulatory uncertainty remains a key challenge; for example, on April 9, 2026, Argentina approved mining reforms to encourage investment near glacier zones, raising environmental concerns and potential project delays. Moreover, environmental incidents carry significant financial and reputational risks, as seen in the February 2025 tailings dam failure in Zambia, which resulted in substantial cleanup costs and liabilities running into tens of millions of USD. These factors, combined with declining ore grades and rising capital intensity, continue to limit the pace at which new copper mining capacity can be brought online.

End Use Insights

The building and construction segment accounted for the largest share of the market in 2025, primarily due to copper’s extensive use in electrical wiring, plumbing systems, roofing, and HVAC applications. Rapid urbanization, particularly in emerging economies such as India and Southeast Asia, continues to drive demand for residential and commercial infrastructure, thereby sustaining high copper consumption. In addition, increasing investments in smart cities, green buildings, and energy-efficient infrastructure are further strengthening demand, as copper is a critical material for efficient power distribution and sustainable construction solutions.

The machinery and equipment segment is expected to register the fastest growth over the forecast period, driven by rising industrial automation and the expansion of manufacturing activities globally. Copper is widely used in industrial machinery, motors, transformers, and heavy equipment due to its superior electrical conductivity and durability. The growing adoption of advanced manufacturing technologies, including robotics and automated systems, is significantly increasing the need for high-performance copper components. Furthermore, the ongoing shift toward electrified industrial equipment and energy-efficient machinery is expected to accelerate copper demand within this segment.

Regional Insights

The North America copper mining industry is characterized by stable production, strong regulatory oversight, and increasing focus on supply chain security. The region is witnessing renewed investments in domestic mining and processing capacities to reduce reliance on imports, particularly in the context of energy transition and critical mineral strategies. Canada and the U.S. are emphasizing sustainable mining practices and ESG compliance, while also supporting exploration activities through policy incentives. In addition, the growing demand from electric vehicles, renewable energy, and grid modernization projects continues to support long-term copper consumption in the region.

U.S. Copper Mining Market Trends

The U.S. copper mining industry represents a key market within North America, driven by rising investments in infrastructure modernization, clean energy, and domestic manufacturing. Federal initiatives supporting critical minerals development are encouraging new mining projects and expansions of existing operations. However, the market faces challenges related to lengthy permitting processes and environmental regulations, which can delay project timelines. Despite this, increasing demand from sectors such as defense, electronics, and electric mobility is expected to sustain steady growth in copper mining and processing activities.

Asia Pacific Copper Mining Market Trends

Asia Pacific copper mining industry dominated the global market in terms of consumption, led by China, India, and Southeast Asian countries. Rapid industrialization, urbanization, and infrastructure development are the primary growth drivers in the region. China remains the largest consumer and processor of copper, supported by its extensive manufacturing base and renewable energy expansion. Meanwhile, India and ASEAN countries are emerging as high-growth markets due to increasing investments in construction, power generation, and transportation infrastructure. The region also benefits from growing exploration activities and government support for mining sector development.

Europe Copper Mining Market Trends

Europe’s copper mining industry is relatively mature but is gaining momentum due to the region’s strong push toward decarbonization and circular economy principles. The European Union is prioritizing secure and sustainable sourcing of critical raw materials, including copper, to support renewable energy systems, electric mobility, and digital infrastructure. Recycling plays a significant role in meeting demand, with a high share of secondary copper production. However, limited domestic mining capacity and strict environmental regulations continue to drive reliance on imports, creating opportunities for strategic partnerships and investments in external supply chains.

Latin America Copper Mining Market Trends

Latin America copper mining industry is the largest copper-producing region globally, with countries such as Chile and Peru accounting for a significant share of global output. The region benefits from abundant mineral reserves, well-established mining infrastructure, and strong export orientation. Ongoing investments in mine expansions and new project developments continue to support production growth. However, the market is influenced by political and regulatory uncertainties, community opposition, and environmental concerns, which can impact project timelines and investment flows.

Middle East & Africa Copper Mining Market Trends

The Middle East & Africa copper mining industry is emerging as a promising market, driven by increasing exploration activities and foreign investments. African countries such as the Democratic Republic of Congo and Zambia hold substantial copper reserves and are witnessing growing interest from global mining companies. Governments in the region are focusing on improving mining policies, infrastructure, and investment frameworks to attract capital. In addition, the Middle East is investing in downstream processing and diversification strategies, which may further support regional copper demand. Despite this potential, challenges such as political instability, infrastructure gaps, and regulatory risks remain key considerations.

Key Copper Mining Company Insights

Some of the key players operating in the market include Freeport-McMoRan Inc., Codelco, among others.

-

Freeport-McMoRan Inc., established in 1987, is one of the world’s largest publicly traded copper producers, with significant mining operations in North and South America as well as Indonesia. The company produces copper, gold, and molybdenum, supplying essential materials for infrastructure, energy, and industrial applications. Freeport-McMoRan focuses on large-scale, long-life assets, operational efficiency, and the adoption of advanced mining technologies to enhance productivity and sustainability.

-

Codelco (Corporación Nacional del Cobre de Chile), established in 1976, is the world’s largest copper producer and a state-owned enterprise of Chile. The company operates some of the largest copper mines globally, including Chuquicamata and El Teniente, and plays a critical role in global copper supply. Codelco emphasizes resource optimization, mine modernization, and sustainable mining practices while contributing significantly to Chile’s economy.

-

BHP Group Limited, established in 1885, is a leading global resources company with a strong presence in copper mining alongside iron ore, coal, and other commodities. The company operates major copper assets such as the Escondida mine in Chile, one of the largest copper mines in the world. BHP focuses on portfolio diversification, operational excellence, and investments in future-facing commodities, including copper, to support global decarbonization and electrification trends.

Key Copper Mining Companies:

The following key companies have been profiled for this study on the copper mining market.

- Anglo American plc

- Antofagasta plc

- BHP Group

- Codelco

- First Quantum Minerals

- Freeport-McMoRan

- Glencore

- KGHM Polska Miedź

- Southern Copper Corporation

- Zijin Mining

Recent Developments

-

In March 2026, Freeport-McMoRan announced plans to seek permits for a USD 7.5 billion expansion of its El Abra copper mine in Chile, aimed at significantly increasing long-term production capacity.

-

In April 2026, First Quantum Minerals received authorization from the Panamanian government to process and export stockpiled copper ore from its Cobre Panamá mine, allowing partial resumption of operations following earlier shutdowns.

-

In April 2026, a USD 1 billion merger was announced between American Pacific Mining Corp. and Metallic Minerals Corp. to create a diversified critical minerals platform with exposure to copper and other strategic resources.

Copper Mining Market Report Scope

Report Attribute

Details

Market definition

Market size is typically calculated based on the total production volume multiplied by the average price per ton of copper ore, concentrates, or refined copper products.

Market size in 2025

USD 195.0 Billion

Estimated market size in 2026

USD 195.8 billion

Projected market size by 2033

USD 229.8 billion

Growth rate

CAGR of 2.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative Units

Volume in Kilotons, Revenue in USD Million, and CAGR from 2026 to 2033

Report coverage

Volume & revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

End use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Russia; China; India; Indonesia; Philippines; Australia; Brazil; Chile; Peru

Key companies profiled

Anglo American plc; Antofagasta plc; BHP Group; Codelco; First Quantum Minerals; Freeport-McMoRan; Glencore; KGHM Polska Miedź; Southern Copper Corporation; Zijin Mining

Customization scope

Free report customization (equivalent to up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Copper Mining Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global copper mining market report based on end use, and region:

-

End Use Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Building & Construction

-

Transportation

-

Consumer Products

-

Electrical & Electronics

-

Machinery & Equipment

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

Europe

-

Russia

-

-

Asia Pacific

-

China

-

India

-

Indonesia

-

Philippines

-

Australia

-

-

Latin America

-

Brazil

-

Chile

-

Peru

-

-

Middle East & Africa

-

Frequently Asked Questions About This Report

Latin America dominated with a 44.3% revenue share in 2025.

The global copper mining market size was valued at USD 195.0 billion in 2025 and is estimated at USD 195.8 billion for 2026.

The global copper mining market is expected to grow at a CAGR of 2.3% from 2026 to 2033, reaching USD 229.8 billion by 2033.

The building & construction is expected to hold the dominant revenue share in 2025, driven by strong demand for copper in electrical wiring, plumbing, and infrastructure development.

Key players include Anglo American plc; Antofagasta plc; BHP Group; Codelco; First Quantum Minerals; Freeport-McMoRan; Glencore; KGHM Polska Miedź; Southern Copper Corporation; Zijin Mining.

The copper mining market is driven by rising demand from electrification, including electric vehicles, renewable energy, and power grid expansion, due to copper’s high conductivity. Increasing urbanization, infrastructure development, and growth in digital and industrial applications are supporting sustained demand.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.