- Home

- »

- Next Generation Technologies

- »

-

Fraud Detection And Prevention Market Report, 2026-2033GVR Report cover

![Fraud Detection and Prevention Market (2026 - 2033)Report]()

Fraud Detection and Prevention Market (2026 - 2033)

Size, Share, & Trend Analysis By Component(Solution, Services), By Application (Identity Theft, Money Laundering, Payment Fraud), By Enterprise Size, By Vertical, By Region, And Segment Forecasts,

Market Size, 2025

$35.3BMarket Estimate, 2026

$40.4BMarket Forecast, 2033

$129.4BCAGR, 2026–2033

18.1%Fraud Detection and Prevention Market Summary

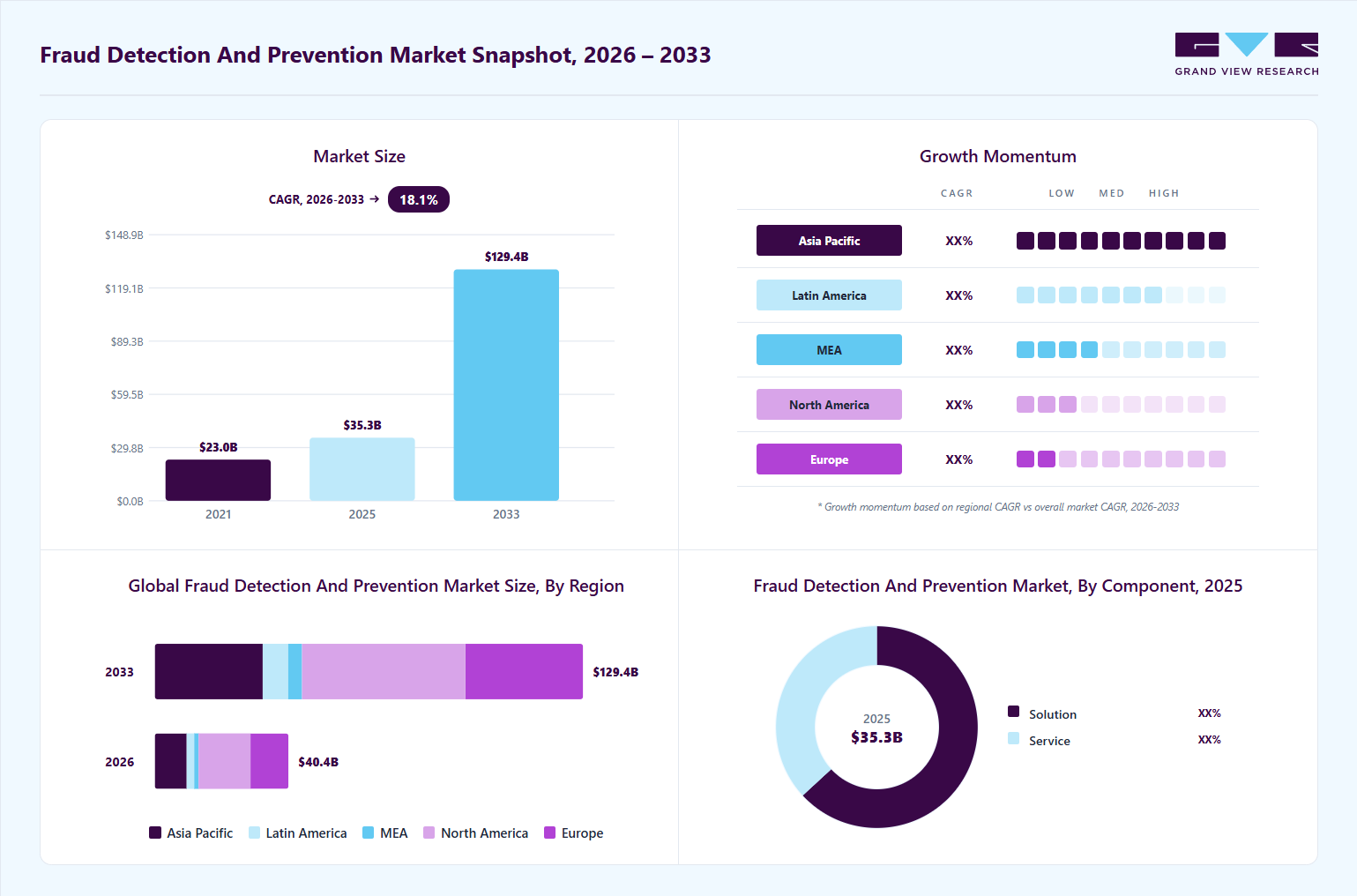

The global fraud detection and prevention market size was valued at USD 35.3 billion in 2025 and is projected to grow from USD 40.4 billion in 2026 to USD 129.4 billion by 2033, at a CAGR of 18.1% from 2026 to 2033. North America dominated the global market with the largest revenue share of 39.0% in 2025. The global market is witnessing rapid expansion driven by the sharp rise in digital transactions, online banking, e-commerce, and real-time payment systems.

Key Market Trends & Insights

- By component: Solution segment led the market with the largest revenue share of 63.1% in 2025.

- By application: Payment fraud segment accounted for the largest market revenue share in 2025.

- By enterprise size: Large enterprises segment accounted for the largest market revenue share in 2025.

- By vertical: BFSI segment accounted for the largest market revenue share in 2025.

Regional Highlights

- Largest regional market: North America (39.0% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 35.3 Billion

- Estimated market size in 2026: USD 40.4 Billion

- Projected market size by 2033: USD 129.4 Billion

- CAGR (2026-2033): 18.1%

Organizations across BFSI, retail, healthcare, telecom, and government sectors are increasingly investing in AI-driven fraud analytics platforms to combat sophisticated cyber threats and financial fraud. The growing adoption of cloud-based fraud prevention solutions, coupled with stricter regulatory compliance requirements such as AML, KYC, PSD2, and GDPR, is further accelerating market growth. One of the most significant trends shaping the market is the increasing use of Generative AI and deepfake technologies by cybercriminals. Fraudsters are leveraging AI-powered phishing, synthetic identities, voice cloning, and fake document generation to bypass traditional security systems across both the broader fraud detection and prevention industry and the online fraud detection market. Industry reports indicate that more than 50% of modern fraud incidents now involve AI-enabled manipulation, forcing enterprises to deploy advanced behavioral analytics, biometric authentication, and real-time anomaly-detection solutions.

")

Another major trend shaping the fraud detection market is the shift from rule-based fraud management systems toward AI/ML-powered adaptive fraud orchestration platforms. Enterprises are increasingly adopting integrated platforms that combine transaction monitoring, identity verification, risk scoring, and behavioral biometrics into unified fraud-prevention ecosystems. Financial institutions are also deploying real-time fraud detection engines that analyze billions of transactional data points within milliseconds to reduce false positives and improve customer experience. This transition is especially prominent in the digital banking, fintech, payment processing, and online fraud detection markets.

Regionally, North America continues to dominate the fraud detection and prevention industry due to high cybersecurity spending and advanced banking infrastructure, while Asia Pacific is emerging as the fastest-growing region driven by rapid fintech expansion and increasing digital payment adoption in countries such as India and China. In addition, the market is witnessing growing investments in behavioral biometrics, AI-native fraud intelligence, and identity verification technologies as organizations attempt to counter increasingly sophisticated multi-step fraud attacks and fraud-as-a-service ecosystems. This further strengthens the broader fraud prevention market, as enterprises increasingly focus on proactive risk mitigation and end-to-end protection strategies rather than solely on post-incident detection.

Market Dynamics

The growing need to reduce financial losses, identity theft, and digital fraud is becoming a major driving factor for the market growth. Organizations across the banking, healthcare, retail, e-commerce, government, and education sectors are adopting advanced fraud-prevention solutions to identify suspicious activities in real time and improve customer trust. The rapid increase in online transactions, digital payment systems, and remote applications has also raised the risk of cyber fraud, creating strong demand for AI-based monitoring, identity verification, behavioral analytics, and automated risk assessment technologies. Businesses are focusing on strengthening security frameworks while ensuring smooth user experiences, which is further supporting market growth.

For instance, in April 2026, the U.S. Department of Education introduced real-time identity fraud detection measures for FAFSA applications to reduce fraudulent student aid claims. The system uses automated risk screening, identity verification, and document authentication to identify suspicious applications while allowing genuine students to complete submissions without disruption. This development highlights how government institutions are increasingly investing in advanced fraud-prevention technologies to enhance security and reduce financial fraud. Such initiatives are expected to accelerate the adoption of fraud Detection and Prevention solutions across public and private sectors, supporting overall market expansion in the coming years.

The fraud detection and prevention industry faces a key restraint due to the sensitivity of business operations to false positives. In many industries, such as banking, insurance, and e-commerce, fraud detection systems are required to identify suspicious transactions in real time. However, when legitimate transactions are incorrectly flagged as fraud, it can lead to customer dissatisfaction, transaction delays, and potential loss of trust. This makes organizations cautious about deploying highly strict fraud detection rules. As a result, enterprises often face a trade-off between security accuracy and customer convenience, which limits aggressive implementation of advanced detection models.

As a result, many enterprises intentionally maintain balanced or relaxed fraud detection thresholds to avoid disrupting genuine customers. While this approach helps ensure a smoother customer experience, it also limits the full effectiveness of advanced fraud prevention solutions. Consequently, the need to minimize false positives acts as a restraint on the widespread adoption of highly aggressive fraud detection technologies, slowing overall market growth. In addition, organizations often require extensive tuning and monitoring of fraud models to maintain this balance, increasing operational complexity. This cautious approach further delays the full-scale automation of fraud-prevention systems across industries.

Market Concentration & Characteristics

The fraud detection and prevention industry is experiencing strong, accelerating growth, driven by the rapid expansion of digital transactions, the adoption of online services, and the increasing sophistication of cyber fraud attempts. The market remains moderately fragmented, with a mix of global cybersecurity leaders and a large number of specialized AI-driven and analytics-focused vendors. Continuous technological advancements and the rising demand for real-time fraud prevention solutions are driving organizations to invest heavily in advanced security systems, supporting sustained, high market growth across industries.

In terms of market characteristics, the degree of innovation is very high, as vendors continuously enhance AI, machine learning, and behavioral analytics capabilities to detect evolving fraud patterns. The level of mergers and acquisitions is moderately high, with larger players acquiring niche startups to strengthen their solution portfolios. Regulatory impact is strong, as compliance requirements such as KYC, AML, and data protection laws significantly influence adoption. The availability of substitutes is moderate, as some enterprises opt for in-house or bundled security solutions rather than standalone tools. Finally, end-user concentration is relatively balanced, with demand spread across BFSI, government, healthcare, retail, and education sectors, reducing dependency on any single industry.

Component Insights

The solution segment led the market with the largest revenue share of 63.1% in 2025, primarily due to the rising need for advanced, real-time, and automated tools that can effectively identify and mitigate increasingly sophisticated fraud threats across digital channels. Organizations are prioritizing end-to-end fraud management platforms that integrate AI/ML-based analytics, behavioral biometrics, transaction monitoring, and identity verification to proactively detect anomalies and reduce financial losses. The rapid expansion of digital banking, e-commerce, and payment ecosystems has further intensified demand for scalable fraud prevention solutions, especially within the online fraud detection market, where transaction volumes and attack surfaces are significantly higher. In addition, regulatory compliance requirements and the need to minimize false positives while improving customer experience are driving enterprises to invest heavily in comprehensive solution-based offerings rather than standalone services, thereby reinforcing the dominance of this segment within the broader market.

The services segment is expected to grow at the fastest CAGR during the forecast period, driven by increasing demand for managed fraud monitoring, consulting, system integration, and continuous support services across enterprises adopting advanced fraud mitigation technologies. As fraud threats become more complex and dynamic, organizations are increasingly relying on specialized service providers to design, deploy, and optimize AI-driven fraud detection frameworks rather than relying solely on in-house capabilities. This shift is particularly evident in the broader fraud prevention market, where businesses are focusing on continuous model tuning, regulatory compliance support, and real-time threat intelligence updates to keep pace with evolving attack patterns. In addition, the growing adoption of cloud-based fraud platforms and the need for seamless integration across multiple digital channels are further accelerating demand for services, making this segment the fastest-growing component of the overall fraud prevention market during the forecast period.

Application Insights

The payment fraud segment accounted for the largest market revenue share in 2025, driven by the exponential rise in digital payment transactions across online banking, e-commerce platforms, and real-time payment systems. Increasing instances of card-not-present (CNP) fraud, account takeover attacks, and unauthorized transaction activities have significantly heightened the need for advanced fraud monitoring and prevention solutions. Financial institutions and payment service providers are increasingly deploying AI/ML-based analytics, behavioral authentication, and real-time transaction scoring to detect and prevent fraudulent activities more effectively. This dominance is further reinforced by the rapid growth of the online fraud detection market, where high transaction volumes and evolving attack techniques necessitate continuous innovation in fraud prevention capabilities across digital payment ecosystems.

The identity theft segment is expected to grow at the fastest CAGR during the forecast period, driven by the increasing sophistication of cybercriminal activities, including synthetic identity creation, account takeover attacks, and credential-based fraud, across digital platforms. The rapid expansion of online banking, e-commerce, and digital payment ecosystems has further heightened exposure to identity-related risks, prompting enterprises to invest heavily in advanced verification technologies, biometric authentication, and AI-powered risk-scoring systems. As organizations strengthen their security posture to protect customer data and financial transactions, demand in the broader fraud prevention market is accelerating, making identity theft one of the most critical and fast-growing focus areas in the evolving landscape.

Enterprise Size Insights

The large enterprises segment accounted for the largest market revenue share in 2025, primarily due to their extensive digital infrastructure, high transaction volumes, and greater exposure to sophisticated cyber threats and financial fraud. These organizations typically operate across multiple geographies and digital channels, necessitating advanced, scalable, and integrated fraud management systems powered by AI, machine learning, and real-time analytics. In addition, large enterprises have stronger financial capabilities and regulatory compliance requirements, enabling them to invest heavily in comprehensive fraud detection and risk management solutions. Their proactive approach toward cybersecurity modernization and continuous monitoring further reinforces their dominance within the broader fraud detection software market, as they prioritize minimizing financial losses and safeguarding customer trust at scale.

The SMEs segment is expected to grow at the fastest CAGR during the forecast period, driven by the increasing digitization of small and medium-sized businesses and their rising exposure to cyber threats such as payment fraud, phishing, and identity theft. As SMEs rapidly adopt cloud-based platforms, digital payment systems, and e-commerce channels, the need for affordable, scalable, and easy-to-deploy fraud detection solutions is accelerating. In addition, the growing availability of subscription-based, AI-powered fraud prevention tools is enabling SMEs to implement advanced security measures without requiring large upfront investments. This shift is significantly contributing to the expansion of the fraud detection and prevention ecosystem, as vendors increasingly tailor solutions to meet the cost sensitivity and operational constraints of SMEs in the global market.

Vertical Insights

The BFSI segment accounted for the largest market revenue share in 2025, primarily due to the sector’s high exposure to financial crimes, large transaction volumes, and stringent regulatory compliance requirements. Banks, insurance companies, and financial service providers are among the earliest adopters of advanced fraud detection technologies such as AI/ML-based analytics, real-time transaction monitoring, and behavioral biometrics to safeguard sensitive customer data and financial assets. The rapid expansion of digital banking, mobile payments, and fintech ecosystems has further intensified fraud risks, compelling BFSI organizations to continuously invest in robust security frameworks. As a result, BFSI remains the most dominant end-user segment in the global market, driven by the critical need to prevent financial losses and maintain customer trust in an increasingly digital financial environment.

The retail & e-commerce segment is expected to register at the fastest CAGR during the forecast period, driven by the rapid expansion of online shopping platforms, increasing digital payment adoption, and rising instances of payment fraud, account takeover, and identity theft. As consumers increasingly shift toward mobile commerce and omnichannel retail experiences, retailers are facing higher exposure to sophisticated cyber threats across checkout systems and digital wallets. This has led to strong demand for AI/ML-powered fraud detection tools, real-time transaction monitoring, and behavioral analytics to minimize chargebacks and fraudulent activities. In addition, the growth of the online fraud detection market is accelerating investments in advanced fraud prevention solutions, as e-commerce companies prioritize secure, seamless customer experiences while maintaining trust and reducing revenue leakage.

Regional Insights

North America dominated the global fraud detection and prevention market with the largest revenue share of 39.0% in 2025, primarily driven by the strong presence of advanced financial infrastructure, early adoption of AI/ML-based fraud detection technologies, and high transaction volumes across digital banking, fintech, and e-commerce platforms. The region also benefits from stringent regulatory frameworks and compliance requirements, such as AML and data protection laws, that compel organizations to invest heavily in robust fraud-prevention systems. In addition, the increasing sophistication of cyber threats and rising incidents of payment fraud and identity theft have further accelerated the deployment of real-time monitoring and analytics solutions, reinforcing North America’s dominant position in the global market.

U.S. Fraud Detection and Prevention Market Trends

The fraud detection and prevention market in the U.S. accounted for the largest market revenue share in North America in 2025, driven by the country’s highly advanced digital financial ecosystem, widespread adoption of online banking and digital payment platforms, and the presence of a large number of BFSI institutions and fintech companies. The increasing frequency and sophistication of cyberattacks, including payment fraud, identity theft, and account takeover incidents, have further compelled organizations to invest heavily in AI/ML-powered fraud detection systems and real-time monitoring solutions. In addition, stringent regulatory requirements and compliance standards, along with strong cybersecurity spending and rapid adoption of cloud-based security platforms, continue to reinforce the U.S. dominance in the global market.

The Mexico fraud detection and prevention market is witnessing steady growth, driven by the rapid expansion of digital banking, increasing adoption of online payment systems, and rising penetration of e-commerce platforms across the country. As financial transactions increasingly shift to digital channels, the incidence of fraud, including card-not-present (CNP) fraud, identity theft, and account takeover attacks, is also rising, creating strong demand for advanced fraud mitigation solutions. Financial institutions and fintech companies are increasingly deploying AI/ML-based analytics, behavioral monitoring, and real-time transaction screening tools to enhance security and reduce financial losses. In addition, growing financial inclusion, expansion of mobile wallets, and increasing cross-border digital transactions are further supporting the development of the Mexican market, including the broader online fraud detection market ecosystem.

Europe Fraud Detection and Prevention Market Trends

The fraud detection and prevention market in Europe is anticipated to register at a significant CAGR from 2026 to 2033, driven by the rising incidence of cyber fraud, increasing adoption of digital banking and contactless payments, and the rapid expansion of fintech ecosystems across the region. Strengthening regulatory frameworks such as GDPR, PSD2, and evolving anti-money laundering directives are compelling financial institutions and enterprises to invest in advanced fraud detection technologies, including AI/ML-based analytics, behavioral biometrics, and real-time transaction monitoring systems. In addition, the growing sophistication of online fraud schemes and identity theft attacks is accelerating demand for proactive fraud prevention strategies, further supporting the steady expansion of the market across Europe during the forecast period.

The UK fraud detection and prevention market is driven by the increasing prevalence of authorized push payment (APP) fraud, rising sophistication of cyberattacks targeting digital banking and fintech platforms, and the rapid expansion of real-time payment systems. In addition, strong regulatory oversight and compliance requirements, along with widespread adoption of open banking frameworks, are encouraging financial institutions to deploy advanced AI/ML-based fraud detection solutions, behavioral analytics, and real-time transaction monitoring systems. The continued growth of digital financial services and increasing focus on customer trust and security are further accelerating demand, thereby supporting robust expansion of the UK market.

The fraud detection and prevention market in France is witnessing strong growth, driven by the rapid expansion of digital payment systems, increasing adoption of online banking and e-commerce platforms, and a rising number of sophisticated cyber fraud incidents targeting financial institutions and consumers. In addition, stringent regulatory frameworks such as GDPR and ongoing EU-level initiatives for anti-money laundering (AML) and payment security are compelling organizations to strengthen their fraud prevention capabilities. Financial institutions and enterprises are increasingly deploying AI/ML-based fraud detection tools, behavioral analytics, and real-time transaction monitoring systems to enhance security and reduce financial losses, thereby accelerating the growth of the French market.

Asia Pacific Fraud Detection and Prevention Market Trends

The fraud detection and prevention market in theAsia Pacific is expected to register at the fastest CAGR from 2026 to 2033, driven by rapid digital transformation, explosive growth in digital payments, and increasing adoption of online banking, e-commerce, and mobile-first financial services across emerging economies. The region is witnessing a surge in fraud incidents, including identity theft, payment fraud, and account takeover attacks, which is compelling enterprises and financial institutions to invest heavily in advanced fraud detection and prevention solutions. In addition, strong fintech expansion, government-led digitalization initiatives, and rising penetration of AI/ML-based security technologies are further accelerating market adoption. The growing importance of real-time transaction monitoring and the expansion of the online fraud detection market are also contributing significantly to the Asia Pacific’s position as the fastest-growing region in the global market.

The China fraud detection and prevention market is driven by the massive expansion of digital payment ecosystems, rapid adoption of e-commerce and mobile banking platforms, and increasing exposure to sophisticated cyber fraud risks such as identity theft, phishing, and payment fraud. The country’s highly digitized economy, supported by large-scale fintech innovation and AI-driven financial services, is further accelerating the deployment of advanced fraud detection solutions. In addition, the growing regulatory focus on cybersecurity, data protection, and financial risk management is compelling enterprises and financial institutions to invest in real-time monitoring systems and AI/ML-based fraud-prevention technologies, thereby strengthening the overall growth trajectory of the China market.

Latin America Fraud Detection and Prevention Market Trends

The fraud detection and prevention market in Latin America is experiencing a strong transformation driven by the rapid digitalization of financial services, rising adoption of mobile banking, and the accelerated growth of e-commerce and real-time payment systems such as PIX in Brazil and similar instant payment frameworks across the region. As digital transaction volumes increase, the region is witnessing a sharp rise in fraud incidents, including identity theft, payment fraud, phishing, and account takeover attempts, prompting enterprises to invest more in advanced fraud analytics and real-time monitoring solutions. This is also strengthening the broader online fraud detection market, as organizations focus on securing high-risk digital channels and reducing financial losses.

Key Fraud Detection and Prevention Company Insight

Key players operating in the fraud detection and prevention industry are ACI Worldwide, Accertify, BAE Systems Applied Intelligence, Bottomline Technologies, Experian, and others. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In April 2026, ACI Worldwide and Kinexys (J.P. Morgan) collaborated to integrate real-time account and payee verification into payment flows to help banks detect and prevent fraud before transactions are completed. This strengthens fraud prevention against rising authorized push payment (APP) scams in instant payment systems by validating recipient details upfront.

-

In March 2026, Accertify’s new Attack State Intelligence capability enhances fraud prevention by detecting coordinated login attacks, credential stuffing, and account takeover (ATO) attempts in real time. It continuously analyzes login behavior across web, mobile, and API channels and compares it with normal traffic patterns to identify anomalies linked to bot-driven and automated attack campaigns.

Key Fraud Detection and Prevention Companies

The following key companies have been profiled for this study on the fraud detection and prevention market.

-

ACI Worldwide

-

Accertify

-

BAE Systems Applied Intelligence

-

Bottomline Technologies

-

Experian

-

Feedzai

-

FICO

-

Fiserv

-

IBM

-

LexisNexis Risk Solutions

-

Mastercard

-

NICE Actimize

-

Oracle

-

SAP

-

TransUnion

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Fiserv, Inc.; Corp.; Oracle; SAP SE; SAS Institute Inc.; Experian Information Solutions, Inc.

- Focus on end-to-end fraud prevention platforms integrated with broader enterprise IT, banking, and security ecosystems

- Strong emphasis on enterprise contracts, regulatory compliance solutions, and long-term managed services

- Deep global client base and brand trust across BFSI, government, and large enterprises

- Highly integrated data ecosystems and advanced analytics capabilities built over decades

- Slower innovation cycles compared to agile startups

- High cost and complex deployment, making solutions less attractive for small and mid-sized businesses

Emerging Players: SEON Technologies Ltd.; Signifyd; AltexSoft; Software GmbH

- Build AI-native, cloud-first fraud detection platforms with real-time decisioning capabilities

- Target specific high-growth niches such as e-commerce fraud, fintech onboarding, and digital payments

- High agility and faster innovation cycles with rapid product enhancements

- Strong specialization in modern fraud use cases like behavioral analytics and transaction-level scoring

- Limited global scale and smaller enterprise penetration

- Lower brand recognition and weaker regulatory compliance footprint compared to established vendors

Fraud Detection and Prevention Market Report Scope

Report Attribute

Details

Market size in 2025

USD 35.3 billion

Estimated Market size in 2026

USD 40.4 billion

Projected Market size by 2033

USD 129.4 billion

Growth rate

CAGR of 18.1% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, application, enterprise size, vertical, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Southeast Asia; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

ACI Worldwide; Accertify; BAE Systems Applied Intelligence; Bottomline Technologies; Experian; Feedzai; FICO; Fiserv; IBM; LexisNexis Risk Solutions; Mastercard; NICE Actimize; Oracle; SAP; TransUnion

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Fraud Detection and Prevention Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global fraud detection and prevention market report based on component, application, deployment, enterprise size, end use, and region.

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Solution

-

Fraud Analytics

-

Authentication

-

Governance, Risk, and Compliance

-

Services

-

Professional Services

-

Managed Services

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Identity Theft

-

Money Laundering

-

Payment Fraud

-

Others

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

SMEs

-

-

Vertical Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Healthcare

-

Industrial and Manufacturing

-

IT & Telecom

-

Retail and E-commerce

-

Government and Defence

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

- Southeast Asia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Region-specific deep-dive report on the North America fraud Detection and Prevention market

Added country-level segmentation for the U.S. and Canada with separate demand dynamics

Expanded competitive landscape with North America-focused vendors and solution providers

Enabled clearer understanding of high-growth adoption zones within North America

Helped identify priority sectors (BFSI and government) for targeted market entry

Improved strategic planning for regional expansion and partnership development

Inclusion of the India-specific fraud Detection and Prevention market analysis

Integrated regulatory landscape including RBI guidelines and digital KYC requirements

Included additional key players operating in the Indian market

Provided strong visibility into one of the fastest-growing digital payment markets globally

Supported localization strategy for product deployment and compliance alignment in India

Expanded competitive intelligence, including additional emerging players and country-specific fraud detection vendors in Europe

Added emerging regional players from Germany, UK, and France

Included country-specific competitive mapping for Europe markets

Provided a more complete and realistic competitive benchmarking framework

Helped identify acquisition and partnership opportunities in emerging markets

Improved decision-making for global expansion and competitive positioning strategies

Frequently Asked Questions About This Report

The global fraud detection & prevention market size was estimated at USD 35.3 billion in 2025 and is expected to reach USD 40.4 billion in 2026.

The global fraud detection & prevention market is expected to grow at a compound annual growth rate of 18.1% from 2026 to 2033 to reach USD 129.4 billion by 2033.

Some key players operating in the fraud detection & prevention market include Total System Services, Inc; Software AG; SAS Institute Inc.; SAP SE; Oracle; IBM; Fiserv, Inc.; Experian plc; Equifax, Inc.; BAE Systems; and ACI Worldwide, Inc.

Key factors that are driving the fraud detection & prevention market growth include growing concern across industries to curb threats and financial losses stemming from cyber scams such as Distributed Denial-Of-Service (DDoS), ransomware, and malware.

The BFSI segment led the global fraud detection & prevention market and accounted for the highest revenue share of around 30% in 2025.

The solutions segment dominated the global fraud detection & prevention market, holding the largest revenue share of 63.1% in 2025.

The authentication solutions segment dominated the global fraud detection & prevention market in 2025 and accounted for more than 42.1% of the overall revenue share.

The professional services segment led the global fraud detection & prevention market and held the largest revenue share of around 69.4% in 2025.

The payment fraud application dominated the global fraud detection & prevention market and accounted for the maximum revenue share of around 53.1% in 2025.

North America dominated the fraud detection & prevention market with a share of 39.0% in 2025. This is attributable to the growing investments by enterprises in advanced fraud prevention solutions to comply with stringent government regulations, such as PCI DSS standards.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.