- Home

- »

- Homecare & Decor

- »

-

Glamping Market Size, Share & Trends Report 2026-2033GVR Report cover

![Glamping Market (2026 - 2033)Report]()

Glamping Market (2026 - 2033)

Size, Share & Trends Analysis Report By Accommodation (Cabins & Pods, Tents, Yurts, Treehouses), By Age Group (18 - 32, 33 - 50, 51 - 65, Above 65 years), By Booking Mode, By Region, And Segment Forecasts

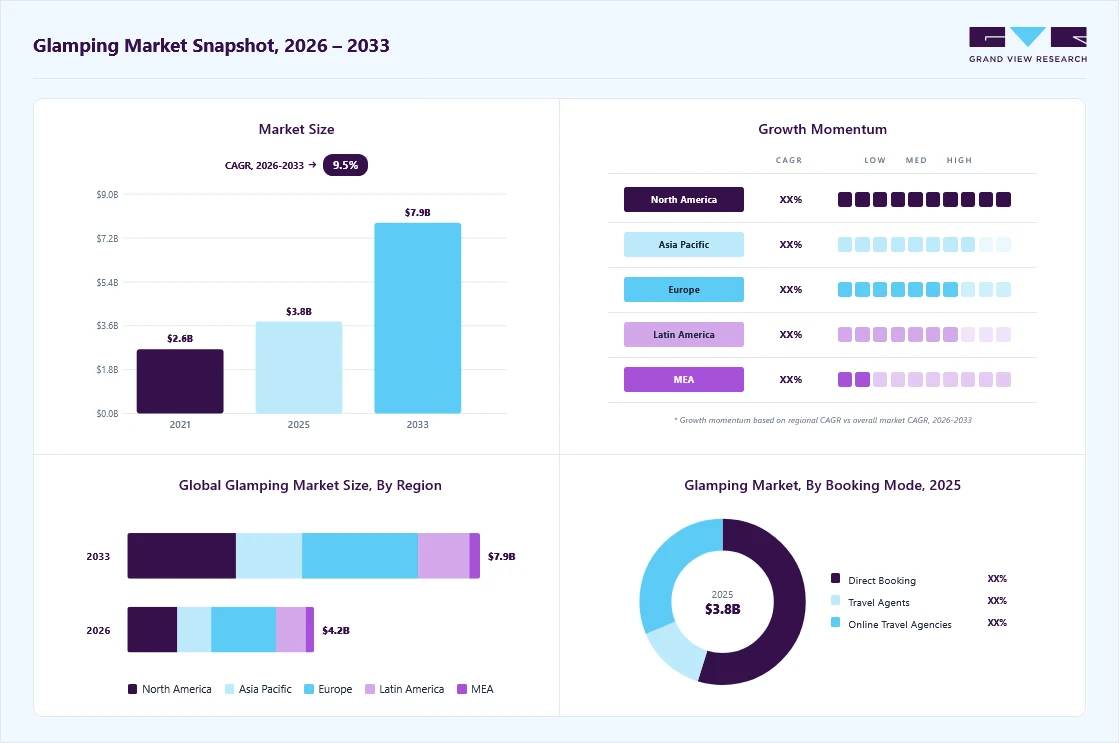

Market Size, 2025

$3.8BMarket Estimate, 2026

$4.2BMarket Forecast, 2033

$7.9BCAGR, 2026–2033

9.5%Glamping Market Summary

The global glamping market size was valued at USD 3.8 billion in 2025 and is projected to grow from USD 4.2 billion in 2026 to USD 7.9 billion by 2033, at a CAGR of 9.5% from 2026 to 2033. The market in Europe dominated with a revenue share of 35.0% in 2025. This growth is primarily driven by the increasing demand for luxury outdoor experiences that combine the appeal of nature with modern comforts, particularly among millennials and eco-conscious travelers.

Key Market Trends & Insights

- By accommodation: Cabins & pods segment held the largest market share of 43.0% in 2025.

- By age group: 18 to 32 age group segment held the largest market share of 43.9% in 2025.

- By booking mode: Direct bookings segment held the largest market share of 54.7% in 2025.

Regional Highlights

- Largest regional market: Europe (35.0% revenue share, 2025)

- By country: UK held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 3.8 Billion

- Estimated market size in 2026: USD 4.2 Billion

- Projected market size by 2033: USD 7.9 Billion

- CAGR (2026-2033): 9.5%

The rise in disposable income, coupled with the desire for unique travel experiences, has further spurred the market. Moreover, the growing trend of sustainable tourism and the preference for eco-friendly accommodation are pushing both consumers and operators to embrace glamping.The glamping market is experiencing rapid growth, fueled by the increasing demand for luxury outdoor experiences, particularly from eco-conscious travelers and millennials seeking unique travel options. The rise of new operators, 28% of which are in their first year, demonstrates the growing interest in this space, as highlighted by the Glamping Americas 2023 State of the Industry Report. With businesses such as Quaint Glamping and Mitten Getaways Glamping Co. set to launch, the industry is poised for further expansion.

")

Strategic positioning near natural attractions, such as state and national parks, enhances guest experiences by combining luxury with outdoor exploration. Around 51% of glamping sites are located near state parks in the U.S., and 33% are adjacent to national parks, offering visitors a blend of nature and comfort. In addition, sustainability and technology integration are expected to play a critical role in the future of the glamping industry. Eco-friendly practices, along with the use of digital solutions for seamless booking, are becoming key factors for both operators and travelers.

The hectic lifestyles of consumers today include long working hours and less time for relaxation. De-stressing and relaxation are considered to be the main factors propelling the growth of the glamping market. This need for a healthy lifestyle, along with the trend of eco-tourism, has created a high demand for an active and outdoors régime, which in turn, likely have a positive impact on the market over the forecast period.

Sustainable glamping is emerging as a key trend that combines luxury with environmental responsibility, catering to eco-conscious travelers seeking nature-centric experiences. Glamping operators are increasingly integrating sustainability across their operations by adopting eco-friendly construction materials, renewable energy sources, and low-impact building techniques. The use of natural and reclaimed materials, such as wood and bamboo, allows structures to blend with the natural environment while reducing ecological impact. Collectively, these practices enable glamping sites to deliver high-end outdoor accommodations while preserving natural landscapes and local ecosystems.

Accommodation Insights

Cabins & pods accounted for a revenue share of over 43% in 2025. This is mainly due to the growing preference for more permanent, sturdy, and comfortable glamping accommodations. This shift is largely driven by glampers seeking a "home-away-from-home" experience with modern conveniences such as insulated walls, heating, air conditioning, and full bathrooms. Cabins and pods offer a level of privacy, security, and comfort comparable to hotels, making them highly attractive to families and couples.

The demand for tent accommodation is expected to grow at a CAGR of 10.6% from 2026 to 2033, driven by the rising demand for a more immersive and traditional camping experience. Modern glamping tents often feature high-end interiors, including plush beds and en suite bathrooms, while still offering a closer connection to nature than cabins or pods. The rise in eco-conscious travel and the desire for unique, customizable outdoor experiences ranging from safari tents to yurts continues to fuel demand for luxury tent accommodations, particularly in remote, picturesque locations.

Age Group Insights

Glamping among the 18 to 32 age group accounted for a revenue share of 43.9% in 2025, which is largely driven by millennials and Gen Z’s inclination toward unique, experience-based travel. These younger generations prioritize adventure, nature, and social media-friendly experiences, which glamping fulfills with its blend of outdoor settings and luxury accommodations. The growth in online searches, influencer-driven content, and a shift toward eco-conscious travel also contribute to glamping's popularity within this demographic. Moreover, flexible work arrangements and the rise of "workcations" enable younger travelers to combine remote work with leisure, further boosting glamping demand among this age group.

The demand for glamping among the 33 to 50 age group is projected to grow at a CAGR of 10.2% from 2026 to 2033, attributed to a different set of motivations. This demographic, typically more financially stable and often traveling with family, is drawn to glamping for its comfort, privacy, and upscale amenities that traditional camping lacks. As wellness and relaxation become key aspects of midlife travel, glamping offers the perfect balance between connecting with nature and enjoying luxurious conveniences such as spa treatments, farm-to-table dining, and wellness retreats. Moreover, this age group is increasingly seeking family-friendly vacation options that provide a mix of outdoor activities and comfort, driving further growth in demand.

Booking Mode Insights

Direct bookings accounted for a revenue share of 54.7% in 2025. One major driver is the increasing reliance on glamping operators' direct websites, which often offer personalized services, exclusive deals, and greater transparency in terms of pricing and amenities. These platforms provide a more tailored customer experience, allowing travelers to communicate specific requests and customize their stay directly with the host. Additionally, many glamping providers promote direct bookings by offering perks such as loyalty discounts, early check-ins, or complimentary upgrades, incentivizing travelers to bypass third-party platforms.

Bookings on online travel agencies are projected to grow at a CAGR of 10.3% from 2026 to 2033 in the glamping market. The rising demand for unique travel experiences has made glamping an appealing alternative to traditional hotels, particularly among millennials and Gen Z, who favor immersive, eco-friendly, and luxury stays. OTAs, with their wide reach and convenience, capitalize on this trend by offering diverse glamping options, ranging from high-end treehouses to safari tents. In addition, the increasing digitalization of travel booking platforms enhances user accessibility and ease, contributing to the surge in OTA-based glamping reservations. The use of AI-driven personalization on these platforms also plays a crucial role in matching travelers with suitable accommodations, further driving growth.

Regional Insights

The glamping market in Europe accounted for a share of 35.0% of the global market in 2025. One major factor driving the European glamping market is the increasing focus on sustainability, with many glamping sites adopting eco-friendly practices like using renewable energy and sustainable materials. This allows travelers to enjoy nature without a negative environmental impact. Technology is also playing a larger role in glamping, with innovations like smart tents and cabins, high-speed internet in remote locations, and virtual reality experiences that enhance the outdoor adventure while keeping guests connected and entertained.

UK Glamping Market Trends

The UK glamping market is expected to grow at a CAGR of 8.2% from 2026 to 2033, driven by a combination of structural demand shifts and supply-side enhancements. Rising consumer preference for experiential and nature-based travel, particularly among millennials and urban households, continues to support demand for accommodation formats that blend outdoor experiences with comfort and convenience. Growth is further supported by the continued strength of domestic tourism in the UK, driven by cost-conscious travel behavior, sustainability awareness, and a growing inclination toward staycations. Glamping sites benefit from this trend in the country, as they are typically located in scenic, rural, or coastal areas that appeal to short-break travelers.

North America Glamping Market Trends

The glamping market in North America is expected to grow at a CAGR of 11.7% from 2026 to 2033. The North America glamping market has seen significant growth in recent years, largely driven by an increasing demand for upscale outdoor experiences. A new report from Kampgrounds of America highlights that 34% of new campers in 2023 opted for glamping, up from 18% in 2021. This growing interest has brought 15.6 million new participants into the sector over the past five years.

A variety of glamping accommodations have emerged across the U.S., offering travelers unique experiences. These range from restored Airstream trailers to yurts and cabins, often situated in scenic locations like private homesteads and ranches. These luxury camping options provide amenities that are not traditionally associated with camping, such as mattresses, upscale bath products, and air conditioning, catering to those seeking nature without sacrificing comfort. Properties such as Eastwind Hotels in New York's Catskills offer year-round glamping experiences, combining outdoor activities like skiing and hiking with high-end accommodations. The trend also includes features such as wellness programs and "digital detox" experiences, appealing to urban dwellers looking to unplug and reconnect with nature.

Asia Pacific Glamping Market Trends

The Asia Pacific glamping market is expected to grow at a CAGR of 10.0% from 2065 to 2033. One of the growing trends in Asia is the emphasis on wellness, with many glamping sites offering activities like yoga, meditation, and spa treatments. These experiences cater to the increasing demand for personal well-being and mindfulness, providing guests with a holistic retreat in nature. Family-friendly glamping options are on the rise in countries like Japan and India, offering larger accommodations, kid-friendly programs, and pet-friendly amenities, making glamping an appealing option for families and those traveling with pets.

Key Glamping Company Insights

The glamping market is characterized by its fragmented nature. The fragmented nature of the glamping market is largely due to the presence of a mix of small, independent operators and larger, established companies. The glamping market caters to a wide variety of travelers, from luxury-seeking tourists to eco-conscious adventurers. Many smaller, niche businesses have emerged, each offering unique, personalized experiences. These independent operators focus on boutique, local glamping experiences, such as yurts, safari tents, and treehouses, catering to specific customer preferences. Larger, more established players, on the other hand, offer standardized luxury glamping experiences across multiple locations, leading to a fragmented market structure.

Key Glamping Companies:

The following key companies have been profiled for this study on the glamping market.

- Under Canvas

- Collective Retreats

- Tentrr

- Eco Retreats

- Baillie Lodges

- Nightfall Camp Pty Ltd.

- Tanja Lagoon Camp

- Wildman Wilderness Lodge

- Paperbark Camp

- Hoshino Resorts

Recent Developments

-

In October 2025, Country Glamping on the River in Lobelville, Tennessee, launched an owner-financing program that lets buyers purchase luxury riverfront lots within its 776-acre glamping resort with low down payments and flexible terms, including financing for land, utilities, and structures such as tiny homes, domes, cabins, or RV sites. Owners can use the property personally or enroll it in the company’s turnkey short-term rental and management system to generate passive income, while the project emphasizes eco-friendly development and aims to boost local tourism and jobs in the region.

-

In September 2024, Quaint Glamping is launching in Twin Mountain, New Hampshire, offering year-round outdoor luxury experiences. The site is expected to feature 15 dome-like structures with modern amenities such as full bathrooms, kitchenettes, and event spaces. This launch aims to cater to the increasing demand for winter glamping.

-

In September 2023, Starlight Haven in Hot Springs, Arkansas, expanded its glamping resort, adding luxurious options like safari tents, geodesic domes, and treehouses. The resort emphasizes sustainability and offers eco-friendly practices while integrating digital services for guest convenience.

Glamping Market Report Scope

Report Attribute

Details

Market size in 2025

USD 3.8 billion

Market size value in 2026

USD 4.2 billion

Revenue forecast in 2033

USD 7.9 billion

Growth rate (Revenue)

CAGR of 9.5% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Accommodation, age group, booking mode, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Germany; UK; France; Italy; Netherlands; China; Japan; India; Australia; Brazil; Argentina; South Africa; UAE

Key companies profiled

Under Canvas; Collective Retreats; Tentrr; Eco Retreats; Baillie Lodges; Nightfall Camp Pty Ltd.; Tanja Lagoon Camp; Wildman Wilderness Lodge; Paperbark Camp; Hoshino Resorts

Customization

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Glamping Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the global glamping market on the basis of accommodation, age group, booking mode, and region.

-

Accommodation Outlook (Revenue, USD Million, 2021 - 2033)

-

Cabins & Pods

-

Tents

-

Yurts

-

Treehouses

-

Others

-

-

Age Group Outlook (Revenue, USD Million, 2021 - 2033)

-

18 - 32 years

-

33 - 50 years

-

51 - 65 years

-

Above 65 years

-

-

Booking Mode Outlook (Revenue, USD Million, 2021 - 2033)

-

Direct Booking

-

Travel Agents

-

Online Travel Agencies

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Netherlands

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

UAE

-

-

Frequently Asked Questions About This Report

Key factors that are driving the glamping market growth include a rise in eco-tourism and consumer inclination toward adventure travel and the rising popularity of wellness tourism owing to the increasing number of travelers.

The global glamping market size was valued at USD 3.8 billion in 2025 and is estimated at USD 4.2 billion for 2026.

The global glamping market is expected to grow at a CAGR of 9.5% from 2026 to 2033, reaching USD 7.9 billion.

Europe dominated with a 35.0% revenue share in 2025.

Key players include Under Canvas, Collective Retreats, Tentrr, Eco Retreats, Baillie Lodges, Nightfall Camp Pty Ltd., Tanja Lagoon Camp, Wildman Wilderness Lodge, and Paperbark Camp.

The cabins & pods segment led with a 43.0% revenue share in 2025.

The 18 to 32 age group segment led with a 43.9% revenue share in 2025.

The direct bookings segment led with a 54.7% revenue share in 2025.

About the Author(s)

Homecare & Decor Research Team

Consumer Goods · Homecare & DecorThis report was authored by the homecare & decor research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the homecare & decor segment of the consumer goods industry. All findings are based on proprietary consumer goods databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.