- Home

- »

- Advanced Interior Materials

- »

-

Ceramic Matrix Composites Market Size Report, 2026-2033GVR Report cover

![Ceramic Matrix Composites Market (2026 - 2033)Report]()

Ceramic Matrix Composites Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Oxides, Silicon Carbide, Carbon), By Application (Aerospace, Defense, Hypersonic Missiles, Energy & Power, Electrical & Electronics), By Region, And Segment Forecasts

Market Size, 2025

$8.8BMarket Estimate, 2026

$9.8BMarket Forecast, 2033

$23.4BCAGR, 2026–2033

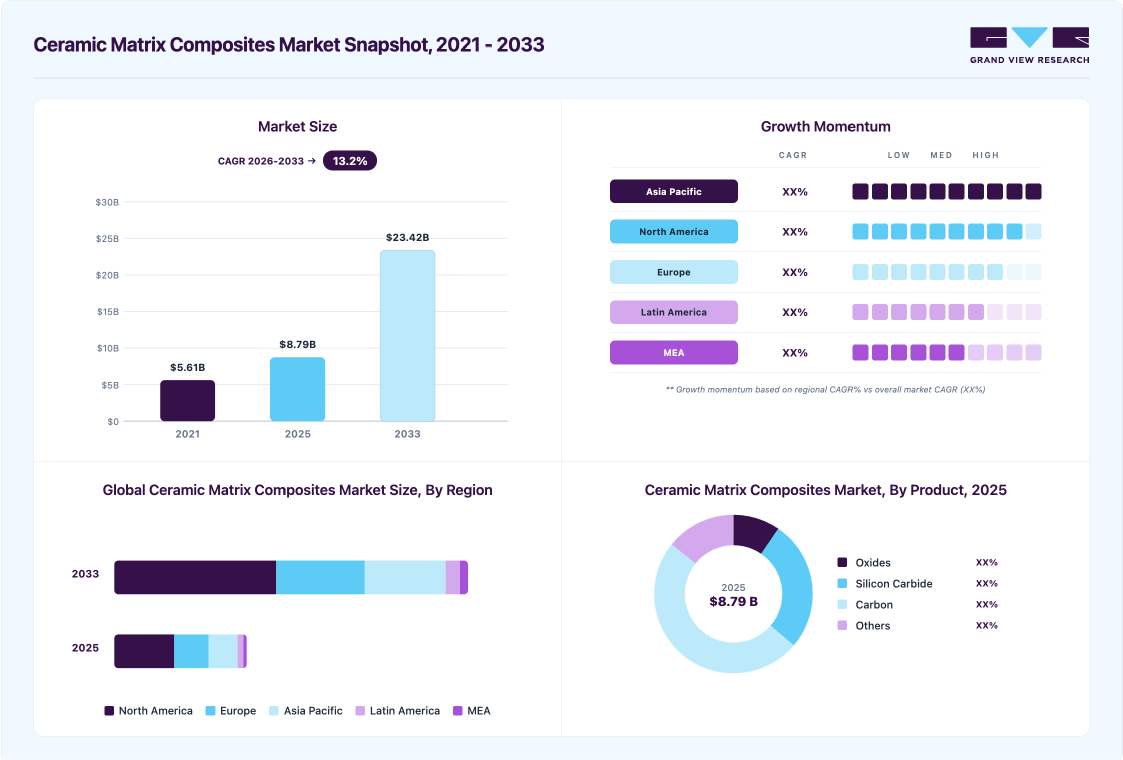

13.2%Ceramic Matrix Composites Market Summary

The global ceramic matrix composites market size was valued at USD 8.8 billion in 2025 and is projected to grow from USD 9.8 billion in 2026 to USD 23.4 billion by 2033, at a CAGR of 13.2% from 2026 to 2033. The North America held the largest share of 45.3% of the global market in 2025, driven by increasing demand for lightweight and high-performance materials across various industries.

Key Market Trends & Insights

- By product: Silicon carbide segment is expected to grow at the fastest CAGR of 13.9% from 2026 to 2033.

- By application: Hypersonic missiles segment is expected to grow at the fastest CAGR of 14.7% from 2026 to 2033.

Regional Highlights

- Largest regional market: North America (45.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. led the North America market in 2025.

Market Size & Forecast

- Market size in 2025: USD 8.8 Billion

- Estimated market size in 2026: USD 9.8 Billion

- Projected market size by 2033: USD 23.4 Billion

- CAGR (2026-2033): 13.2%

One of the primary drivers is the rising adoption of ceramic matrix composites (CMCs) in aerospace and defense applications. These composites offer superior mechanical properties, including high-temperature resistance, low weight, and enhanced durability, making them ideal for aircraft engine components, thermal protection systems, and missile applications.The growing emphasis on fuel efficiency and environmental regulations has further accelerated the use of CMCs in commercial aircraft, as they help reduce fuel consumption and emissions while improving overall operational efficiency.

")

The growing investments in energy and power generation sectors also contribute to market expansion. CMCs are widely utilized in gas turbines, nuclear reactors, and other high-temperature applications where traditional metal alloys fail to perform efficiently. The increasing global focus on clean energy, along with advancements in power generation technologies, has led to higher adoption of CMCs in industrial gas turbines and renewable energy systems. Their ability to enhance efficiency, reduce maintenance costs, and withstand extreme conditions positions them as a critical material in modern energy solutions.

Furthermore, ongoing research and development (R&D) activities and technological advancements are playing a crucial role in the market’s growth. Leading manufacturers and research institutions are actively engaged in developing advanced CMCs with improved properties and cost-effective production techniques. The introduction of innovative fabrication methods, such as additive manufacturing and hybrid CMC processing, is expected to enhance the scalability and affordability of these materials, further driving their adoption across diverse applications.

Market Dynamics

Growing demand for fuel-efficient aircraft and advanced defense systems is significantly driving the adoption of ceramic matrix composites (CMCs) across the aerospace and defense sectors. CMCs offer superior properties such as high-temperature resistance, lightweight structure, corrosion resistance, and improved mechanical strength compared to conventional metal alloys. These characteristics make them highly suitable for applications including aircraft engines, turbine components, thermal protection systems, exhaust nozzles, and braking systems. Increasing focus on reducing aircraft weight and improving engine efficiency is accelerating the integration of CMC components in next-generation aerospace platforms.

In addition, rising investments in military modernization programs and space exploration activities are further supporting market growth. Aerospace manufacturers are increasingly utilizing CMCs to improve operational efficiency and enhance performance under extreme operating conditions. The growing production of commercial aircraft, expansion of defense aviation fleets, and increasing adoption of advanced propulsion technologies are expected to continue generating strong demand for ceramic matrix composites over the forecast period.

The high manufacturing cost and complex production process associated with ceramic matrix composites (CMCs) are major factors restraining market growth. Production of CMCs involves advanced fabrication techniques, expensive raw materials, and lengthy processing cycles, which significantly increase overall production costs compared to conventional metal alloys and traditional ceramic materials. In addition, challenges related to machining, quality control, and scalability limit large-scale commercial adoption across cost-sensitive industries. These factors may hinder wider penetration of CMCs, particularly in applications where budget constraints and availability of lower-cost alternatives remain key purchasing considerations.

Market Concentration & Characteristics

The global ceramic matrix composites (CMC) industry exhibits a moderate to high market concentration, with a few dominant players such as General Electric, Rolls-Royce, and SGL Carbon holding significant market shares. The degree of innovation in this market is high, driven by advancements in manufacturing techniques such as additive manufacturing and infiltration processing, which enhance CMC properties like thermal resistance and durability. In addition, there is an increasing focus on mergers, acquisitions, and strategic collaborations as companies seek to strengthen their supply chains and expand their technological expertise. The impact of regulations is considerable, particularly in aerospace and defense applications, where stringent standards related to material performance and environmental sustainability influence product development and commercialization.

The presence of service substitutes for CMCs, such as metal alloys and polymer-based composites, remains a limiting factor in certain applications, but CMCs continue to gain preference due to their superior strength-to-weight ratio and thermal stability. The end use concentration is predominantly in aerospace, automotive, energy, and industrial sectors, with aerospace leading due to the increasing adoption of CMCs in aircraft engines and structural components. As industries seek lightweight, high-performance materials to improve fuel efficiency and reduce emissions, the demand for CMCs is expected to increase, further shaping market dynamics.

Product Insights

The carbon segment led the market and accounted for the largest revenue share of 49.5% in 2025, driven by increasing demand for lightweight and high-strength materials across various industries. Carbon-based ceramic matrix composites offer exceptional mechanical properties, including high-temperature resistance, excellent thermal stability, and a superior strength-to-weight ratio. These characteristics make them highly suitable for aerospace, defense, and automotive applications, where reducing weight while maintaining structural integrity is a critical requirement. The growing emphasis on fuel efficiency and emission reduction in the transportation sector further propels the adoption of carbon-based CMCs, as they contribute to improved performance and lower environmental impact.

The silicon carbide segment is expected to grow at the fastest CAGR of 13.9% over the forecast period, driven by its superior properties such as high-temperature resistance, excellent strength-to-weight ratio, and exceptional wear and corrosion resistance. These characteristics make SiC-based CMCs highly desirable in industries such as aerospace, defense, automotive, and energy. In the aerospace sector, the increasing demand for lightweight yet durable materials to enhance fuel efficiency and performance in aircraft engines and structural components is a key driver. Silicon carbide CMCs are being increasingly utilized in next-generation jet engines due to their ability to withstand extreme temperatures while reducing overall engine weight, leading to improved efficiency and lower emissions.

Application Insights

The aerospace segment dominated the market and accounted for the largest revenue share of 43.8% in 2025. CMCs offer superior mechanical properties, including high-temperature resistance, enhanced toughness, and reduced weight compared to traditional metal alloys. These advantages contribute to improved fuel efficiency and overall performance in both commercial and military aerospace applications. With stringent environmental regulations and industry-wide efforts to reduce carbon emissions, the aerospace sector is increasingly adopting CMCs to enhance engine efficiency and structural durability while minimizing fuel consumption.

The hypersonic missiles segment is expected to grow at the fastest CAGR of 14.7% over the forecast period, driven by advancements in aerospace and defense technologies. One of the primary drivers is the increasing demand for hypersonic weapons due to their strategic advantages in modern warfare. Hypersonic missiles, which travel at speeds exceeding Mach 5, require materials that can withstand extreme temperatures and mechanical stress. CMCs, known for their high thermal stability, superior strength-to-weight ratio, and resistance to oxidation, are essential for ensuring the structural integrity and performance of these missiles during high-speed flights. The enhanced durability and lightweight nature of CMCs contribute to improved maneuverability and fuel efficiency, making them a preferred material in the development of next-generation hypersonic missile systems.

Regional Insights

North America ceramic matrix composites industry dominated the global market and accounted for the largest revenue share of 45.3% in 2025. Advancements in manufacturing technologies are contributing to the rapid growth of the CMC market in North America. Cutting-edge techniques such as additive manufacturing, automated fiber placement, and advanced sintering processes are making the production of CMCs more cost-effective and scalable. These improvements enhance the material’s mechanical properties while reducing production costs, allowing for broader adoption across multiple industries. With ongoing research focused on optimizing manufacturing efficiency and reducing defects, the commercialization of CMCs is expected to accelerate further.

U.S. Ceramic Matrix Composites Market Trends

The ceramic matrix composites (CMC) industry in the U.S. is driven by the growing aerospace industry. CMCs are highly sought after for their exceptional ability to withstand high temperatures and mechanical stresses, making them ideal for aerospace components such as turbine engines, thermal shields, and high-performance airframes. The advancement of commercial and military aerospace projects, such as next-generation aircraft, space exploration technologies, and hypersonic vehicles, has created a demand for materials with superior thermal resistance and lightweight. CMCs' ability to improve fuel efficiency and performance in extreme conditions makes them a key material in modern aerospace engineering, boosting market growth.

Europe Ceramic Matrix Composites Market Trends

Europe's ceramic matrix composites industry focuses on sustainable energy generation, including nuclear, geothermal, and renewable sources, which has spurred demand for CMCs. CMCs offer exceptional resistance to heat and radiation, making them ideal for components used in nuclear reactors and advanced energy generation systems. Their ability to withstand high temperatures and harsh environmental conditions is essential in improving the efficiency and safety of energy production, which is crucial for Europe’s long-term energy strategy. The growing shift towards cleaner, more efficient energy sources enhances the role of CMCs in the region’s energy infrastructure.

The ceramic matrix composites industry in Germany is driven by the increasing demand of CMCs in the automotive industry, particularly in the context of electric vehicle (EV) development and high-performance vehicle components. As manufacturers focus on reducing the weight of vehicles to improve energy efficiency and reduce emissions, CMCs are being adopted for high-temperature applications such as brake discs, turbochargers, and exhaust systems. The lightweight, high-strength properties of CMCs enable improved fuel efficiency and enhanced performance in both conventional and electric vehicles. Germany’s automotive giants, including BMW, Mercedes-Benz, and Volkswagen, are increasingly investing in advanced materials like CMCs to develop next-generation automotive technologies, thereby boosting market growth.

Asia Pacific Ceramic Matrix Composites Market Trends

The Asia Pacific ceramic matrix composites industry is driven by the growth of the space exploration and satellite industry in Asia Pacific. As countries like India and China expand their space programs, there is a growing need for advanced materials that can endure the harsh conditions of space travel. Ceramic matrix composites are used in rocket nozzles, heat shields, and other critical components that must endure extreme thermal stresses and high-speed friction. The rapid development of space exploration capabilities and the increased launch frequency in Asia Pacific are expected to drive significant demand for CMCs in the region’s aerospace and space industries.

China’s ceramic matrix composites (CMC) industry is driven by China’s increasing focus on advancing manufacturing technologies, which plays a crucial role in expanding the CMC market. The country has invested heavily in improving CMC production techniques, including automated fiber placement, additive manufacturing, and more efficient processing methods. These innovations have reduced production costs and improved the scalability of CMCs for industrial use, making them more accessible for a range of applications in defense, aerospace, and other high-performance industries. As these manufacturing advancements continue, the market for CMCs is expected to expand significantly.

Latin America Ceramic Matrix Composites Market Trends

The ceramic matrix composites industry in Latin America is witnessing demand with the automotive industry’s shift towards electric and hybrid vehicles. As the region adopts more stringent environmental regulations aimed at reducing carbon emissions, automotive manufacturers are under pressure to innovate. CMCs offer significant advantages in this regard, providing lightweight solutions that help reduce the overall weight of vehicles, thereby improving fuel efficiency and reducing emissions. The high-temperature resistance and low thermal expansion properties of CMCs make them ideal for use in electric vehicle batteries and power electronics, further expanding their application in the automotive sector.

Middle East & Africa Ceramic Matrix Composites Market Trends

The ceramic matrix composites industry in MEA is driven by the rapid industrialization and infrastructure development in the Middle East, especially in countries such as the UAE and Saudi Arabia, which also plays a vital role in driving the demand for CMCs. As urbanization and industrial activity continue to expand across the region, there is a growing need for advanced materials that can support the construction of high-performance machinery, reactors, and components used in various industries. The increasing number of large-scale construction projects, particularly in the field of high-speed rail, commercial aviation, and energy, requires the use of CMCs for parts that demand high durability, thermal stability, and lightweight characteristics. With governments in the region pushing for further industrialization, there is an increased reliance on advanced materials like CMCs to support the growth of infrastructure projects.

Key Ceramic Matrix Composites Company Insights

Some of the key players operating in the market include3M, COI Ceramics, Inc.

-

3M offers a range of high-performance products such as ceramic fibers, resins, and matrices. These products are widely used in aerospace, automotive, and defense applications, where high-temperature resistance, durability, and lightweight properties are essential. 3M's CMC solutions are designed to meet the demands of industries that require advanced materials for critical, high-performance applications.

-

COI Ceramics, Inc. is a leading manufacturer specializing in advanced ceramic products, including ceramic matrix composites. The company focuses on providing CMC solutions for aerospace, defense, and industrial applications. COI Ceramics offers CMCs based on silicon carbide (SiC) and carbon matrices, which are known for their superior heat resistance, strength, and thermal conductivity. These products are used in components such as thermal protection systems, missile components, and turbine blades, where high temperature and mechanical stress resistance are crucial.

Coorstek, Inc., General Electric Company are some of the emerging market participants in the ceramic matrix composites industry.

-

Coorstek, Inc. is a major player in the manufacturing of advanced ceramics and CMCs, supplying a wide range of products for industries including aerospace, defense, and energy. Coorstek’s ceramic matrix composites are used for high-performance applications where reliability and durability are critical. They offer products like ceramic fibers and SiC-based composites, which are particularly suited for turbine engines, missile components, and industrial applications that require high thermal resistance and mechanical strength.

-

General Electric Company (GE) is a multinational conglomerate with a strong presence in the aerospace and defense sectors. In the ceramic matrix composites industry, GE provides high-performance CMC products primarily for the aerospace industry, such as SiC-based composites used in turbine blades, thermal protection systems, and other critical aerospace components. GE’s CMC solutions are known for their superior performance under extreme temperature conditions and are integral to the development of next-generation jet engines and high-efficiency propulsion systems.

Key Ceramic Matrix Composites Companies:

The following key companies have been profiled for this study on the ceramic matrix composites market.

- 3M Company

- COI Ceramics, Inc.

- Coorstek, Inc.

- General Electric Company

- Kyocera Corporation

- Lancer Systems LP

- SGL Carbon Company

- Ultramet, Inc.

- Ube Industries, Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: 3M; COI Ceramics, Inc.; SGL Carbon Company; Ube Industries, Ltd.

- Focus on advanced aerospace and defense-grade CMC solutions

- Strong investments in R&D and material innovation

- Vertical integration across raw material and component manufacturing

- Strong technological expertise in high-temperature ceramic materials

- Established relationships with aerospace manufacturers & defense

- Large-scale production capabilities and global presence

- Broad product portfolio with customized application-specific solutions

- High dependency on aerospace and defense demand cycles

- High manufacturing and development costs

Emerging Players: Coorstek. Inc.; General Electric Company

- Focus on niche and high-performance CMC applications

- Targeting next-generation energy and industrial applications

- Strong innovation capabilities in specialized CMC applications

- Increasing investments in advanced manufacturing technologies

- Limited commercial-scale production compared to established players

- Narrower product portfolio in CMC segment

Recent Developments

-

In March 2025, GE Aerospace announced plans to invest nearly $1 billion in U.S. manufacturing facilities and supply chains to enhance capacity, including expanding production of ceramic matrix composite parts for next-generation engines and other advanced technologies. This includes factory upgrades across 16 states and the hiring of approximately 5,000 workers to support expanded CMC production and related innovations.

Ceramic Matrix Composites Market Report Scope

Report Attribute

Details

Market size in 2025

USD 8.8 billion

Estimated market size in 2026

USD 9.8 billion

Projected market size by 2033

USD 23.4 billion

Growth rate

CAGR of 13.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Volume in Tons, Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; China; India; Japan; South Korea; Brazil

Key companies profiled

3M Company; COI Ceramics, Inc.; Coorstek, Inc.; General Electric Company; Kyocera Corporation; Lancer Systems LP; SGL Carbon Company; Inc.; Ultramet, Inc.; Ube Industries, Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts’ working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Ceramic Matrix Composites Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global ceramic matrix composites market report based on product, application, and region.

-

Product Outlook (Volume, Tons; Revenue, USD Million, 2021 - 2033)

-

Oxides

-

Silicon Carbide

-

Carbon

-

Others

-

-

Application Outlook (Volume, Tons; Revenue, USD Million, 2021 - 2033)

-

Aerospace

-

Defense

-

Hypersonic Missiles

-

Energy & Power

-

Electrical & Electronics

-

Others

-

-

Regional Outlook (Volume, Tons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Spain

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Middle East & Africa

-

Central & South America

-

Brazil

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Opportunity Assessment

Mapping of high-growth application areas, end-use industries, and emerging demand pockets for ceramic matrix composites across aerospace & defense, energy & power, automotive, and industrial sectors. Analysis of adoption trends, whitespace opportunities, technology transition, and market attractiveness across key application segments.

Identify the most attractive growth opportunities and high-potential application areas. Reveal unmet market needs and whitespace opportunities for expansion. Support product positioning, commercialization, and long-term growth strategy development.

Competitive Benchmarking

Comparative assessment of major ceramic matrix composite manufacturers based on product portfolio, production capabilities, technological expertise, strategic partnerships, R&D focus, geographical presence, and expansion initiatives. Evaluation of competitive positioning, innovation capabilities, and strategic developments across the value chain.

Enable benchmarking against leading market participants and technology innovators. Identify competitive gaps, differentiation opportunities, and strategic advantages. Support competitive intelligence and strategic decision-making initiatives.

Regional Segmentation

Assessment of the ceramic matrix composites market across major regions. Analysis includes regional demand trends, aerospace & industrial manufacturing activities, technology adoption patterns, regulatory landscape, and country-level growth outlook.

Identify high-growth regional markets and demand centers for advanced ceramic materials. Support regional expansion and investment prioritization strategies. Enable understanding of region-specific industry trends, manufacturing ecosystem, and competitive dynamics.

Frequently Asked Questions About This Report

Some of the key players operating in the ceramic matrix composites market include 3M Company; Applied Thin Films, Inc.; CeramTec International; COI Ceramics, Inc.; Coorstek, Inc.; General Electric Company; Kyocera Corporation; Lancer Systems LP; SGL Carbon Company; StarFire Systems, Inc.; Ultramet, Inc.; Ube Industries, Ltd.

The ceramic matrix composites market is likely to be driven by increased demand from the aerospace and military, automotive, and energy and power application industries. In addition, the capacity to withstand high temperatures and tougher government fuel economy rules are expected to enhance the industry in the next years.

North America dominated with a 45.3% revenue share in 2025.

The carbon segment led with a 49.5% revenue share in 2025, while silicon carbide is the fastest-growing segment.

Aerospace held the largest share (over 43.8%) in 2025 and hypersonic missiles are the fastest-growing market.

Asia Pacific is the fastest-growing region over the forecast period.

The global ceramic matrix composites market size was estimated at USD 8.8 billion in 2025 and is expected to reach USD 9.8 billion in 2026.

The global ceramic matrix composites market is expected to grow at a compound annual growth rate of 13.2% from 2026 to 2033 to reach USD 23.4 billion by 2033.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.