- Home

- »

- Next Generation Technologies

- »

-

High Performance Computing Market Size Report, 2026-2033GVR Report cover

![High Performance Computing Market (2026 - 2033)Report]()

High Performance Computing Market (2026 - 2033)

Size, Share, & Trends Analysis Report By Component (Servers, Storage, Software, Services, Cloud), By Deployment (On-premise, Cloud), By End Use, By Region, And Segment Forecasts

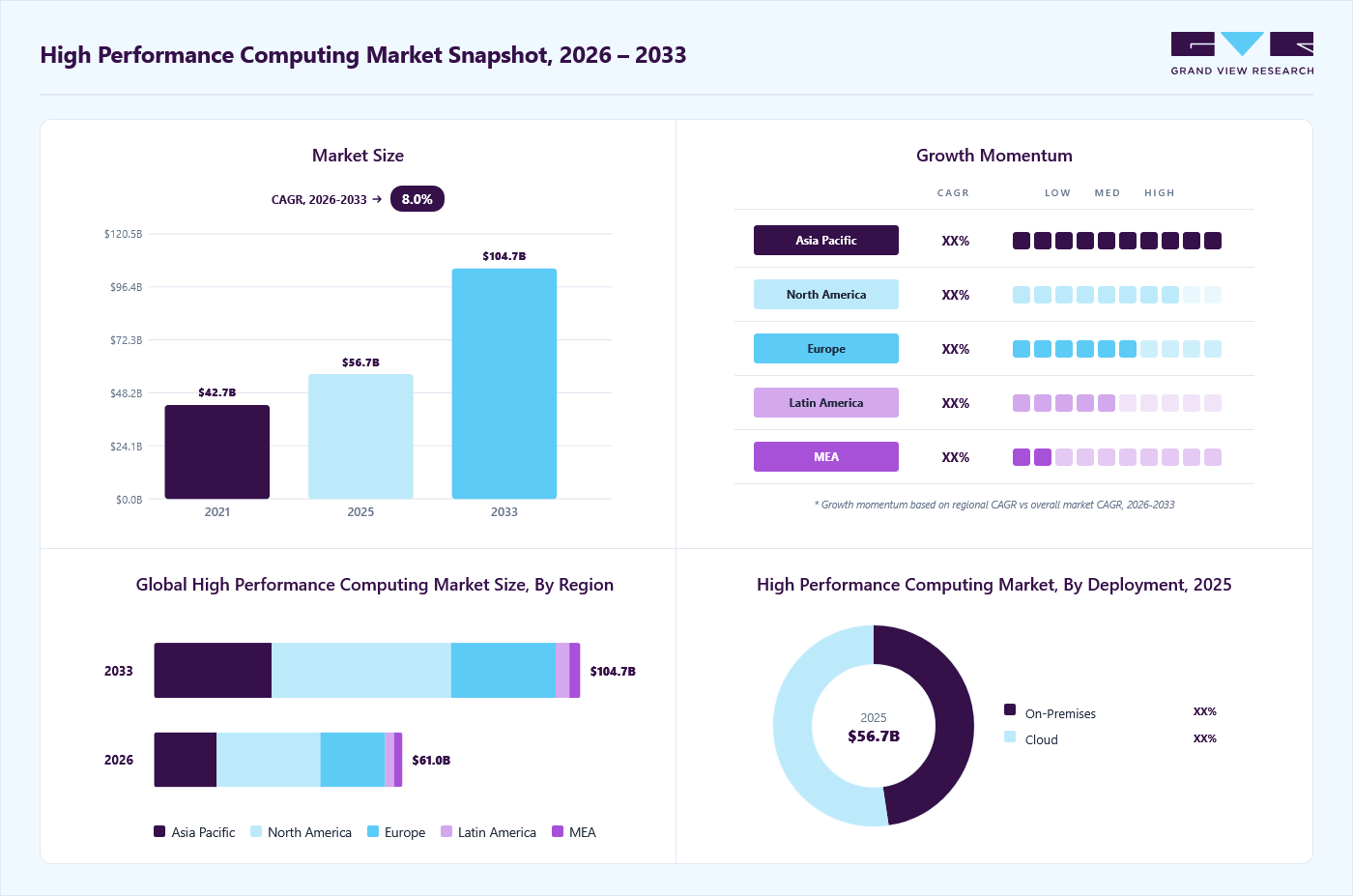

Market Size, 2025

$56.7BMarket Estimate, 2026

$61.0BMarket Forecast, 2033

$104.7BCAGR, 2026–2033

8.0%High Performance Computing Market Summary

The global high performance computing market size was valued at USD 56.7 billion in 2025 and is projected to grow from USD 61.0 billion in 2026 to USD 104.7 billion by 2033, at a CAGR of 8.0% from 2026 to 2033. The market in North America dominated with a revenue share of 41.6% in 2025. This growth is driven by factors such as technological advancements and increased demand across various sectors. One of the primary growth drivers is the growing need for computational power in scientific research and complex simulations.

Key Market Trends & Insights

- By component: Servers held the largest revenue share of 33.1% in 2025.

- By deployment: Cloud held the largest revenue share of 52.4% in 2025.

- By end use: Government & defense held the largest revenue share of 26.5% in 2025.

Regional Highlights

- Largest regional market: North America (41.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- The high performance computing industry in the U.S. held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 56.7 Billion

- Estimated market size in 2026: USD 61.0 Billion

- Projected market size by 2033: USD 104.7 Billion

- CAGR (2026-2033): 8.0%

Industries such as aerospace, automotive, pharmaceuticals, and climate science depend heavily on high-performance computing (HPC) systems to simulate complex processes and analyze very large datasets. These sectors require high levels of accuracy and computational speed that conventional computing systems cannot provide, which is driving increased adoption of HPC solutions. In addition, the rapid growth of artificial intelligence (AI), machine learning (ML), and big data analytics is further boosting demand for HPC. As organizations generate and process larger volumes of data, they need advanced computing infrastructure to support real-time analytics and the training of sophisticated ML models. HPC systems deliver the parallel processing capabilities required for these data-intensive workloads, making them essential for AI development across industries such as finance, healthcare, and e-commerce.The growing adoption of cloud-based HPC services is playing a significant role in the expansion of the high-performance computing industry. Cloud service providers are delivering scalable and flexible HPC solutions that reduce the cost and complexity of adoption for small and medium-sized enterprises (SMEs). This wider availability of HPC allows organizations that previously could not afford expensive on-premise supercomputing systems to use high-performance computing to improve innovation, productivity, and operational efficiency.

")

The HPC as a Service (HPCaaS) model further supports market growth by minimizing upfront capital investment and offering on-demand scalability based on workload requirements. This flexible cost structure is encouraging more organizations to adopt HPC solutions. For instance, in April 2025, Compu Dynamics, a U.S.-based company specializing in mission-critical infrastructure and services, announced the launch of a dedicated AI and High-Performance Computing (HPC) Services division. This new unit provides comprehensive, end-to-end solutions for data centers, including system design, equipment procurement, construction, daily operations, and long-term maintenance. The offering places strong emphasis on advanced liquid cooling technologies designed specifically to meet the performance and efficiency needs of AI and HPC workloads.

In addition, rising government and institutional investments in advanced research and national supercomputing programs are driving the growth of the high-performance computing industry. Governments in major economies are allocating substantial funding to develop HPC infrastructure for critical applications such as defense, climate and weather modeling, energy innovation, genomic research, and space exploration. These initiatives are intended to enhance technological self-reliance, accelerate scientific and engineering breakthroughs, and support large-scale public research efforts. Consequently, demand for high-end HPC systems is increasing across national laboratories, academic institutions, and research centers, contributing steadily to overall market growth.

Component Insights

The servers segment held the largest revenue share of 33.1% in 2025, driven by the rising demand for high-speed and high-capacity computing infrastructure to support the increasing complexity of data-intensive workloads. As scientific research, weather forecasting, genomic sequencing, and financial modeling grow more complex, there is an urgent need for server architectures capable of processing vast volumes of data at ultra-fast speeds. HPC servers, equipped with advanced CPUs and GPUs, are built to deliver the processing power required for these applications, leading to continuous demand.

The cloud segment is expected to grow at the fastest CAGR during the forecast period, driven by the growing complexity and volume of data generated across industries such as life sciences, oil and gas, manufacturing, and financial services. These sectors require vast computing power for tasks like molecular modeling, seismic imaging, crash simulations, and risk analysis. Cloud HPC platforms provide on-demand scalability that can handle these variable and often unpredictable workloads more efficiently than fixed on-premise systems. This elasticity is particularly valuable for projects with spiky demand, where resources can be scaled up or down based on immediate requirements.

Deployment Insights

The cloud segment dominated the market with a revenue share of 52.43% in 2025, owing to the rapid technological innovation by cloud service providers. Major players such as AWS, Microsoft Azure, Google Cloud, and Oracle Cloud are continually upgrading their HPC offerings with newer chipsets such as custom-designed ARM and AI processors, high-speed interconnects, optimized storage, and managed software environments. These enhancements make cloud HPC more powerful and also easier to deploy and manage, reducing the technical barrier for organizations entering the HPC space. The On-premise segment is expected to grow at the significant CAGR over the forecast period, driven by the need for greater control, security, and customization in managing high-performance workloads. Organizations operating in highly regulated or sensitive sectors, such as defense, government, pharmaceuticals, and financial services, often choose on-premise HPC systems due to strict compliance, data sovereignty, and cybersecurity requirements. These institutions handle confidential data that cannot be exposed to third-party cloud environments, making on-premise deployment a preferred and often mandatory choice.

End Use Insights

The government & defense segment dominated the market revenue share of 26.45% in 2025. The need for advanced data processing, national security, and technological competitiveness drives the market growth. One of the primary growth drivers is the increasing reliance on HPC for defense simulations, cryptographic analysis, and real-time intelligence processing. Military operations today are data-intensive, requiring rapid analysis of surveillance data, satellite imagery, cybersecurity threats, and battlefield simulations. HPC enables defense agencies to process vast amounts of data quickly and accurately, enhancing decision-making and strategic planning capabilities.

The manufacturing segment is expected to grow at a significant CAGR over the forecast period. The increasing reliance on advanced simulations, modeling, and digital design is driving market growth. One of the key growth drivers is the adoption of Computer-Aided Engineering (CAE), Computational Fluid Dynamics (CFD), and Finite Element Analysis (FEA) for designing and testing products virtually. These computational methods require immense processing power, which HPC systems provide, enabling manufacturers to reduce physical prototyping costs, accelerate time-to-market, and improve product performance.

Regional Insights

North America dominated the high performance computing market with a revenue share of over 41.6% in 2025. The presence of a large number of leading technology companies and research institutions that demand cutting-edge computational power drives the market growth.

The region benefits from substantial investments in AI, big data analytics, and cloud computing infrastructure. In addition, the strong emphasis on defense and national security programs fuels significant HPC adoption for simulation, cryptography, and threat analysis.

U.S. High Performance Computing Market Trends

The high performance computing market in the U.S. dominated in 2025, and it is expected to grow significantly from 2026 to 2033. The market growth is driven by government funding in scientific research, energy, and healthcare sectors. Agencies like the Department of Energy (DOE), NASA, and the Department of Defense (DoD) are investing heavily in HPC to accelerate climate modeling, genomics, and advanced weaponry research.

Asia Pacific High Performance Computing Market Trends

The high performance computing market in the Asia Pacific is growing at the fastest CAGR from 2026 to 2033 due to growing industrialization, increasing R&D investments, and the proliferation of cloud services. Many countries in this region are focusing on building smart cities, enhancing healthcare with AI, and advancing semiconductor design, all of which require HPC. In addition, government initiatives to strengthen supercomputing capabilities and foster digital economies play a crucial role.

China high performance computing market held a significant market share in 2025, due to government initiatives aimed at technological self-reliance and leadership in supercomputing. The country leads globally in the number of supercomputers, driven by investments in AI, big data, and scientific research. China also focuses on leveraging HPC for smart manufacturing, urban planning, and national security.

The high performance computing market in Japanis expected to grow rapidly in the coming years. This is driven by advancements in robotics, automotive, and electronics manufacturing, which rely on HPC for product design, simulations, and AI integration. The country also places a strong focus on disaster prediction and management, using HPC to run complex climate and seismic models.

Europe High Performance Computing Market Trends

The high performance computing market in Europe is growing at a significant CAGR from 2026 to 2033, supported by close collaboration among European countries. Initiatives such as the European High-Performance Computing Joint Undertaking (EuroHPC) are helping build a shared, pan-European HPC infrastructure across the region. Europe’s strong focus on sustainability is also increasing the use of HPC for energy-efficient computing and climate change research. In addition, growing adoption of HPC in the manufacturing and automotive sectors, particularly for digital twin applications and product development, is further driving market growth.

The UK high performance computing market is expected to grow rapidly over the coming years. The traditional 9-to-5 work structure is increasingly shifting toward freelance and project-based employment, enabling professionals to work independently and select flexible assignments. The UK’s advanced digital infrastructure and strong economy support this transition, positioning the country as an important market for high-performance computing. These platforms enable businesses to access specialized skills on a short-term basis while providing freelancers with new work opportunities, benefiting both sides.

The high performance computing market in Germanyheld a notable market share in 2025, supported by its strong industrial foundation and focus on Industry 4.0. The country’s manufacturing and automotive industries widely use HPC for advanced simulations, digital twin applications, and supply chain optimization. Germany also makes substantial investments in energy research, particularly in renewable energy and smart grid development, where HPC is used to evaluate complex energy systems. In addition, government funding programs aimed at innovation and digital transformation are further accelerating the adoption of HPC across multiple sectors.

Key High Performance Computing Company Insights

Some of the key companies operating in the high performance computing industry, include Advanced Micro Devices, Inc., Amazon Web Services, Inc., Atos SE, Cisco Systems, Inc., Dell Inc., Fujitsu, among others are some of the leading market participants.

-

Amazon Web Services (AWS) is one of the leading cloud service providers offering scalable, on-demand computing infrastructure. In the high-performance computing (HPC) market, AWS delivers managed HPC services, high-performance cloud instances (e.g., EC2 with Elastic Fabric Adapter), and tools like AWS Parallel Computing Service and AWS ParallelCluster to support large-scale simulations, data analytics, and scientific workloads in the cloud.

-

Atos SE is a global digital transformation company based in France, providing end-to-end IT solutions including cloud, cybersecurity, and high-performance computing across 69 countries. In the HPC market, Atos offers supercomputing systems, HPC-as-a-service, and cloud-enabled HPC platforms such as the Nimbix Supercomputing Suite to support compute-intensive workloads and scientific research.

Key High Performance Computing Companies:

The following key companies have been profiled for this study on the high performance computing market.

- Advanced Micro Devices, Inc

- Amazon Web Services, Inc.

- Atos SE

- Cisco Systems, Inc.

- Dell Inc.

- Fujitsu

- Hewlett Packard Enterprise Development LP

- IBM Corporation

- Inspur, Inc.

- Intel Corporation

- Lenovo

- Microsoft

- NEC Corporation

- NVIDIA Corporation

- Supermicro, Inc.

Recent Developments

-

In November 2025, NVIDIA and Japan’s national research institute RIKEN announced the integration of two new GPU-accelerated supercomputers built on NVIDIA GB200 NVL4 technology to advance scientific AI and quantum computing research. One system will support AI-for-science workloads and the other will focus on quantum research, together featuring 2,140 NVIDIA Blackwell GPUs and high-speed Quantum-X800 InfiniBand networking, strengthening Japan’s HPC infrastructure.

-

In November 2025, Equinix and Lenovo helped Merck KGaA in Germany launch a new high-performance computer at an Equinix AI-ready data center. Using Lenovo ThinkSystem servers with advanced liquid cooling, this HPC system is built to accelerate research and innovation in life sciences, healthcare, and electronics, combining private and public cloud resources to handle large, complex computing tasks efficiently.

-

In March 2025, Hewlett-Packard Enterprise Development LP, in collaboration with the European Space Agency (ESA), opened a cutting-edge high-performance computing facility, Space HPC, at ESA’s ESRIN center in Italy. This advanced infrastructure is set to accelerate ESA’s research initiatives and foster innovation across the European space sector, supporting future missions in space exploration and Earth observation.

High Performance Computing Market Report Scope

Report Attribute

Details

Market size in 2025

USD 56.7 billion

Estimated market size in 2026

USD 61.0 billion

Projected market size by 2033

USD 104.7 billion

Growth rate

CAGR of 8.0% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, deployment, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Advanced Micro Devices, Inc.; Amazon Web Services, Inc.; Atos SE; Cisco Systems, Inc.; Dell Inc.; Fujitsu; Hewlett Packard Enterprise Development LP; IBM Corporation; Inspur, Inc.; Intel Corporation; Lenovo; Microsoft; NEC Corporation; NVIDIA Corporation; Supermicro, Inc.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global High Performance Computing Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global high performance computing market report based on component, deployment, end use, and region.

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Servers

-

Storage

-

Networking Devices

-

Software

-

Services

-

Cloud

-

Others

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cloud

-

On-premise

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Gaming

-

Media & Entertainment

-

Retail

-

Transportation

-

Government & Defense

-

Education & Research

-

Manufacturing

-

Healthcare & Bioscience

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global high-performance computing market was estimated at USD 56.7 billion in 2025 and is expected to reach USD 61.0 billion in 2026.

Some key players operating in the high performance computing market include Advanced Micro Devices, Inc, Amazon Web Services, Inc., Atos SE, Cisco Systems, Inc., Dell Inc., Fujitsu, Hewlett Packard Enterprise Development LP, IBM Corporation, Inspur, Inc., Intel Corporation, Microsoft, NVIDIA Corporation, Supermicro, Inc.

Key factors driving the growth of the high-performance computing market include technological advancements and increased demand across various sectors. One of the primary growth drivers is the growing need for computational power in scientific research and complex simulations.

The servers segment led with a 33.1% revenue share in 2025.

Cloud held the largest revenue share 52.4% in 2025.

Government & defense held the largest share (over 26.5%) in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The global high-performance computing market is expected to grow at a compound annual growth rate of 8.0% from 2026 to 2033, reaching USD 104.7 billion by 2033.

North America held the largest share, over 41.6%, in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.