- Home

- »

- HVAC & Construction

- »

-

Hyperscale Data Center Market Size, Industry Report, 2030GVR Report cover

![Hyperscale Data Center Market (2025 - 2030)Report]()

Hyperscale Data Center Market (2025 - 2030)

Size, Share & Trends Analysis Report By Component (Hardware, Software, Services), By Power Capacity (20 MW To 50 MW, 50 MW To 100 MW), By Enterprise Size, By End-use, By Region, And Segment Forecasts

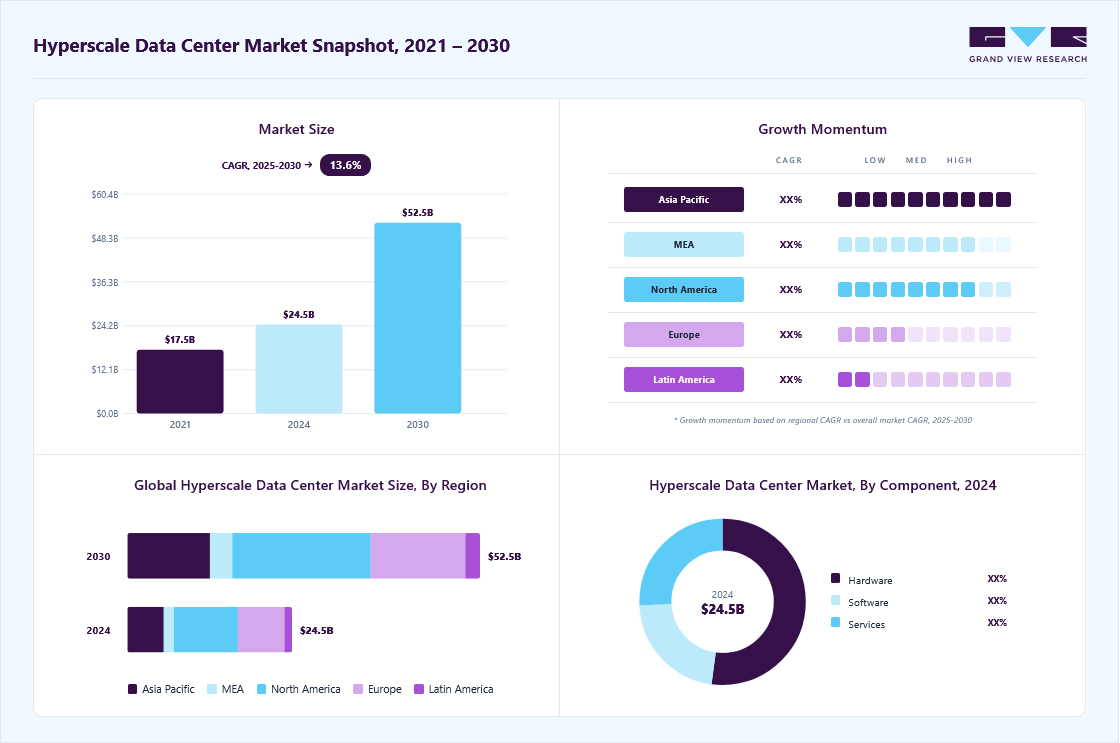

Market Size, 2024

$24.5BMarket Estimate, 2026

$31.4BMarket Forecast, 2030

$52.5BCAGR, 2025–2030

13.6%Hyperscale Data Center Market Summary

The global hyperscale data center market size was estimated at USD 24.5 billion in 2024 and is projected to reach USD 52.5 billion by 2030, growing at a CAGR of 13.6% from 2025 to 2030, driven by the rapid expansion of cloud computing, artificial intelligence (AI), and big data analytics. As organizations shift from traditional data centers to cloud-based infrastructure, the demand for large-scale, high-performance computing environments has surged.

Key Market Trends & Insights

- North America hyperscale data center market dominated globally with a share of nearly 38.0% in 2024.

- The hyperscale data center market in the U.S. is expected to grow significantly at a CAGR of 13.6% from 2025 to 2030.

- By component, the hardware segment dominated the market with a revenue share of over 50.0% in 2024.

- By power capacity, the 50 MW to 100 MW segment dominated the market with a revenue share of over 33.0% in 2024.

- By enterprise size, the large enterprises segment dominated the market with the largest revenue share of over 73.0% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 24.54 Billion

- 2030 Projected Market Size: USD 52.54 Billion

- CAGR (2025-2030): 13.6%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Hyperscale data centers, known for their ability to scale efficiently and support vast volumes of data and computing workloads, are the backbone of cloud service providers such as Amazon Web Services, Microsoft Azure, and Google Cloud. These providers continue to invest heavily in building and expanding their global data center footprints to meet escalating user demand and ensure low-latency, high-availability services.The proliferation of digital services and content consumption also contributes significantly to the hyperscale data center industry. The rise of video streaming, gaming, e-commerce, and social media platforms has created a need for infrastructure that can support massive amounts of data storage and real-time processing. Hyperscale facilities offer the scalability, redundancy, and energy efficiency needed to meet these demands while reducing operational costs per unit of computing. Moreover, the rollout of 5G networks and the growth of Internet of Things (IoT) applications are generating more data at the edge, prompting hyperscale operators to invest in edge data centers and hybrid architectures to process data closer to the source.

")

Companies across industries are undergoing digital transformation, moving core operations to the cloud to improve agility, scalability, and cost-efficiency. This shift fuels demand for Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and hybrid cloud models, all of which rely on the capacity and scale of hyperscale data centers. Enterprises are increasingly relying on hyperscalers for hosting and also for analytics, security, and business continuity.

Sustainability and energy efficiency are also shaping the growth of the hyperscale data center industry. Operators are increasingly prioritizing renewable energy sources, advanced cooling techniques, and automation to reduce carbon footprints and operational costs. Governments and regulatory bodies are supporting these efforts with favorable policies and incentives, further fueling market expansion. Moreover, advancements in server technologies, storage solutions, and virtualization are enabling greater efficiency and higher density deployments, making hyperscale models more attractive across various industries, including finance, healthcare, and retail.

Component Insights

The hardware segment dominated the market with a revenue share of over 50.0% in 2024, driven by rising data privacy concerns and regulatory pressures that are influencing the hardware landscape as well. To ensure compliance with regional data laws and security protocols, hyperscale data centers are incorporating hardware-level encryption, secure boot processes, and advanced physical security mechanisms. These hardware innovations are crucial for maintaining data integrity and building trust among enterprise clients, thereby acting as a strong driver for continued investment and innovation in the hardware segment. The hardware segment is further bifurcated into hardware, servers, enterprise network equipment, PDU, and UPS.

The software segment is anticipated to grow at a CAGR of 15.4% during the forecast period, owing to the growing need for intelligent data center management through software-defined infrastructure. Software-defined networking (SDN), software-defined storage (SDS), and software-defined data centers (SDDC) are enabling hyperscale operators to manage resources more dynamically and cost-effectively. These technologies offer centralized control and policy-driven automation, which are critical for maintaining operational efficiency in increasingly complex infrastructures. The software segment is further bifurcated into DCIM, virtualization, and others.

Power Capacity Insights

The 50 MW to 100 MW segment dominated the market with a revenue share of over 33.0% in 2024. As hyperscale providers extend their reach into emerging markets and secondary data center hubs, they require facilities with substantial power capacities to ensure redundancy, low latency, and high availability. The 50 MW to 100 MW range allows operators to future-proof their infrastructure while accommodating regional data sovereignty laws and connectivity requirements.

The 150 MW and above segment is expected to grow at a significant CAGR over the forecast period. Hyperscale providers are increasingly consolidating their data center footprints by replacing multiple smaller facilities with fewer but larger and more efficient mega campuses. These data center parks, often built in phases, allow for long-term expansion while leveraging economies of scale in construction, operations, and energy procurement. This makes the 150 MW+ range particularly appealing for cloud giants looking to establish future-ready infrastructure capable of sustaining exponential growth for a decade or more.

Enterprise Size Insights

The large enterprises segment dominated the market with the largest revenue share of over 73.0% in 2024, driven by the escalating demand for digital transformation, data-intensive applications, and scalable cloud infrastructure. As large organizations across industries, such as banking, manufacturing, telecommunications, and healthcare, adopt cloud-first strategies, they increasingly rely on hyperscale data centers to manage massive volumes of data, ensure application resilience, and support global business operations.

The small and medium-sized enterprises (SMEs) segment is expected to grow at a significant CAGR over the forecast period due to the widespread adoption of Software-as-a-Service (SaaS), Infrastructure-as-a-Service (IaaS), and Platform-as-a-Service (PaaS) offerings. These services, hosted in hyperscale data centers, enable SMEs to adopt flexible IT infrastructures that scale with business growth, allowing them to respond quickly to market changes and customer demands.

End Use Insights

The cloud service provider segment dominated the market with a revenue share of over 63.0% in 2024. Major cloud service providers such as Amazon Web Services (AWS), Microsoft Azure, Google Cloud, and Alibaba Cloud are investing heavily in hyperscale data centers to accommodate growing customer workloads, ensure high availability, and expand their global presence. These providers require massive, scalable infrastructure to support an ever-expanding portfolio of services such as virtual machines, databases, AI/ML platforms, and analytics tools, all of which are hosted in hyperscale facilities.

The technology provider segment is expected to grow at a significant CAGR over the forecast period. Technology providers, including semiconductor companies, hardware manufacturers, software vendors, and AI model developers, are heavily reliant on hyperscale infrastructure to design, test, deploy, and deliver their solutions at scale. As these firms push the boundaries of performance and speed in areas such as artificial intelligence (AI), machine learning (ML), quantum computing, and immersive technologies (AR/VR), they require vast and high-density computing environments that hyperscale data centers are uniquely equipped to offer.

Regional Insights

North America hyperscale data center market dominated globally with a share of nearly 38.0% in 2024, driven by the aggressive adoption of cloud-based services by large enterprises and public sector institutions. With companies rapidly moving their IT workloads to the cloud to gain scalability, flexibility, and cost benefits, hyperscale providers such as AWS, Microsoft Azure, and Google Cloud are continuously expanding their infrastructure.

U.S. Hyperscale Data Center Market Trends

The hyperscale data center market in the U.S. is expected to grow significantly at a CAGR of 13.6% from 2025 to 2030, owing to the strong presence of global tech giants and their continued investment in AI, big data analytics, and enterprise SaaS platforms. These firms are generating vast amounts of data and also require high-performance infrastructure to process and analyze it. As a result, there is consistent construction of hyperscale facilities, particularly in major tech hubs such as Northern Virginia, Silicon Valley, and Dallas.

Europe Hyperscale Data Center Market Trends

The hyperscale data center market in Europe is anticipated to register a considerable CAGR from 2025 to 2030 due to the increasing demand for data sovereignty and compliance with the EU's General Data Protection Regulation (GDPR). To meet these regulatory requirements, hyperscale cloud providers are setting up localized data centers to ensure that user data remains within European borders. This regulatory pressure has led to the proliferation of hyperscale infrastructure in countries such as Ireland, the Netherlands, and Sweden, where governments are supportive and offer competitive advantages in energy pricing and digital infrastructure.

The UK hyperscale data center market is expected to grow rapidly in the coming years due to the government's push for smart cities and digital services across public administration, healthcare, and transportation. These initiatives require low-latency, scalable infrastructure, propelling demand for hyperscale data centers.

The Germany hyperscale data center market held a substantial market share in 2024. German manufacturers and engineering firms are increasingly integrating IoT, automation, and AI into their operations. These technologies require massive data processing and real-time analytics, which hyperscale facilities can provide. Additionally, Germany's emphasis on data protection and its central location in Europe make it a strategic location for building large-scale, compliant data centers.

Asia Pacific Hyperscale Data Center Market Trends

Asia Pacific hyperscale data center market is expected to be the fastest-growing market at a CAGR of 14.7% from 2025 to 2030, due to the rapid digitalization across emerging economies is a major growth driver. From fintech and e-commerce to mobile gaming and smart manufacturing, digital platforms are becoming foundational to economic growth. Hyperscale data centers are critical in supporting these platforms, especially as mobile-first populations generate vast quantities of data.

The hyperscale data center market in Japan is expected to grow rapidly in the coming years, owing to the integration of AI and high-performance computing (HPC) in sectors such as automotive, electronics, and logistics. Japanese firms require ultra-low latency and scalable compute resources, which hyperscale providers are increasingly offering. Additionally, with an aging IT workforce, automation and outsourcing to hyperscale platforms help bridge operational gaps for large enterprises.

The China hyperscale data center market held a substantial market share in 2024, due to the government's aggressive push toward cloud computing, digital sovereignty, and national AI strategies. Transformation initiatives by the government, such as New Infrastructure, have spurred massive investment in hyperscale data centers. Moreover, domestic technology companies such as Alibaba Cloud, Tencent Cloud, and Huawei Cloud are scaling up infrastructure to support cloud-native services, smart cities, and public sector digitization, all of which require hyperscale capabilities to meet internal demand and regulatory expectations.

Key Hyperscale Data Center Company Insights

Key players operating in the hyperscale data center industry are Amazon Web Services, Inc.,Google, Inc., Microsoft,Alibaba, NTT Ltd., NVIDIA Corporation, Tencent, and Vertiv Group Corp. These companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In January 2025, Oracle unveiled the Exadata X11M, the newest iteration of its Exadata platform, offering major advancements in performance for AI, analytics, and online transaction processing (OLTP) workloads. Designed to handle mission-critical operations more efficiently, the X11M system features intelligent power management and optimized performance, enabling organizations to process data faster while using fewer systems.

-

In December 2024, Amazon Web Services, Inc. unveiled advanced data center innovations to meet rising AI demands while boosting energy efficiency and sustainability. Key upgrades include simplified power and cooling systems, liquid and multimodal cooling for high-density AI hardware, and software-driven rack optimization to reduce energy waste. AWS also introduced a new power shelf and enhanced control systems for better monitoring and diagnostics. These improvements increase computing power per site and reduce the need for additional data centers, supporting both performance and environmental goals.

-

In May 2024, Microsoft launched its first hyperscale cloud data center region in Mexico, marking a significant step in expanding its cloud infrastructure across Latin America. The new region comprises multiple data centers and is designed to deliver secure, scalable, and high-performance cloud services with the added benefit of in-country data residency and reduced latency.

Key Hyperscale Data Center Companies:

The following are the leading companies in the hyperscale data center market. These companies collectively hold the largest market share and dictate industry trends.

- Alibaba

- Amazon Web Services, Inc.

- Arista Networks, Inc.

- Digital Realty Trust

- Equinix, Inc.

- Ericsson, Inc.

- Google, Inc.

- IBM Cloud

- Intel Corporation

- Microsoft

- NTT Ltd.

- NVIDIA Corporation

- Oracle

- Rittal LLC

- Tencent Cloud

- Vertiv Group Corp.

Hyperscale Data Center Market Report Scope

Report Attribute

Details

Market size in 2025

USD 27.7 billion

Revenue forecast in 2030

USD 52.5 billion

Growth Rate

CAGR of 13.6% from 2025 to 2030

Actual data

2018 - 2024

Forecast period

2025 - 2030

Quantitative units

Revenue in USD billion and CAGR from 2025 to 2030

Report enterprise size

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, power capacity, enterprise size, end use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Alibaba; Amazon Web Services, Inc.; Arista Networks, Inc.; Digital Realty Trust; Equinix, Inc.; Ericsson, Inc.; Google, Inc.; IBM Cloud; Intel Corporation; Microsoft; NTT Ltd.; NVIDIA Corporation; Oracle; Rittal LLC; Tencent Cloud; Vertiv Group Corp

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Hyperscale Data Center Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global hyperscale data center market report based on component, power capacity, enterprise size, end use, and region:

-

Component Outlook (Revenue, USD Billion, 2018 - 2030)

-

Hardware

-

Servers

-

Enterprise network equipment

-

PDU

-

UPS

-

-

Software

-

DCIM

-

Virtualization

-

Others

-

-

Services

-

Managed Infrastructure Services

-

Hosting Services

-

Support Services

-

Professional services

-

-

-

Power Capacity Outlook (Revenue, USD Billion, 2018 - 2030)

-

20 MW to 50 MW

-

50 MW to 100 MW

-

100 MW to 150 MW

-

150 MW and above

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2018 - 2030)

-

Large Enterprises

-

Small and Medium Enterprises (SMEs)

-

-

End Use Outlook (Revenue, USD Billion, 2018 - 2030)

-

Cloud Service Provider

-

Technology Provider

-

Telecom

-

Healthcare

-

BFSI

-

Retail & E-commerce

-

Entertainment & Media

-

Energy

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global hyperscale data center market size was estimated at USD 24.54 billion in 2024 and is expected to reach USD 27.73 billion in 2025.

The global hyperscale data center market is expected to grow at a compound annual growth rate of 13.6% from 2025 to 2030 to reach USD 52.54 billion by 2030.

North America dominated the hyperscale data center market with a share of nearly 39.0% in 2024, driven the aggressive adoption of cloud-based services by large enterprises and public sector institutions. With companies rapidly moving their IT workloads to the cloud to gain scalability, flexibility, and cost benefits, hyperscale providers such as AWS, Microsoft Azure, and Google Cloud are continuously expanding their infrastructure.

Some key players operating in the hyperscale data center market include Alibaba, Amazon Web Services, Inc., Arista Networks, Inc., Digital Realty Trust, Equinix, Inc., Ericsson, Inc., Google, Inc., IBM Cloud, Intel Corporation, Microsoft, NTT Ltd., NVIDIA Corporation, Oracle, Rittal LLC, Tencent Cloud, Vertiv Group Corp

Key factors driving market growth include the rapid expansion of cloud computing, artificial intelligence (AI), and big data analytics. As organizations shift from traditional data centers to cloud-based infrastructure, the demand for large-scale, high-performance computing environments has surged.

About the Author(s)

HVAC & Construction Research Team

Technology · HVAC & ConstructionThis report was authored by the hvac & construction research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the hvac & construction segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.