- Home

- »

- Pharmaceuticals

- »

-

Insulin Market Size, Share & Growth Report, 2026-2033GVR Report cover

![Insulin Market (2026 - 2033)Report]()

Insulin Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Rapid-Acting Insulin, Long-Acting Insulin, Combination Insulin, Biosimilar), By Application, By Type, By Distribution Channel, By Region, And Segment Forecasts

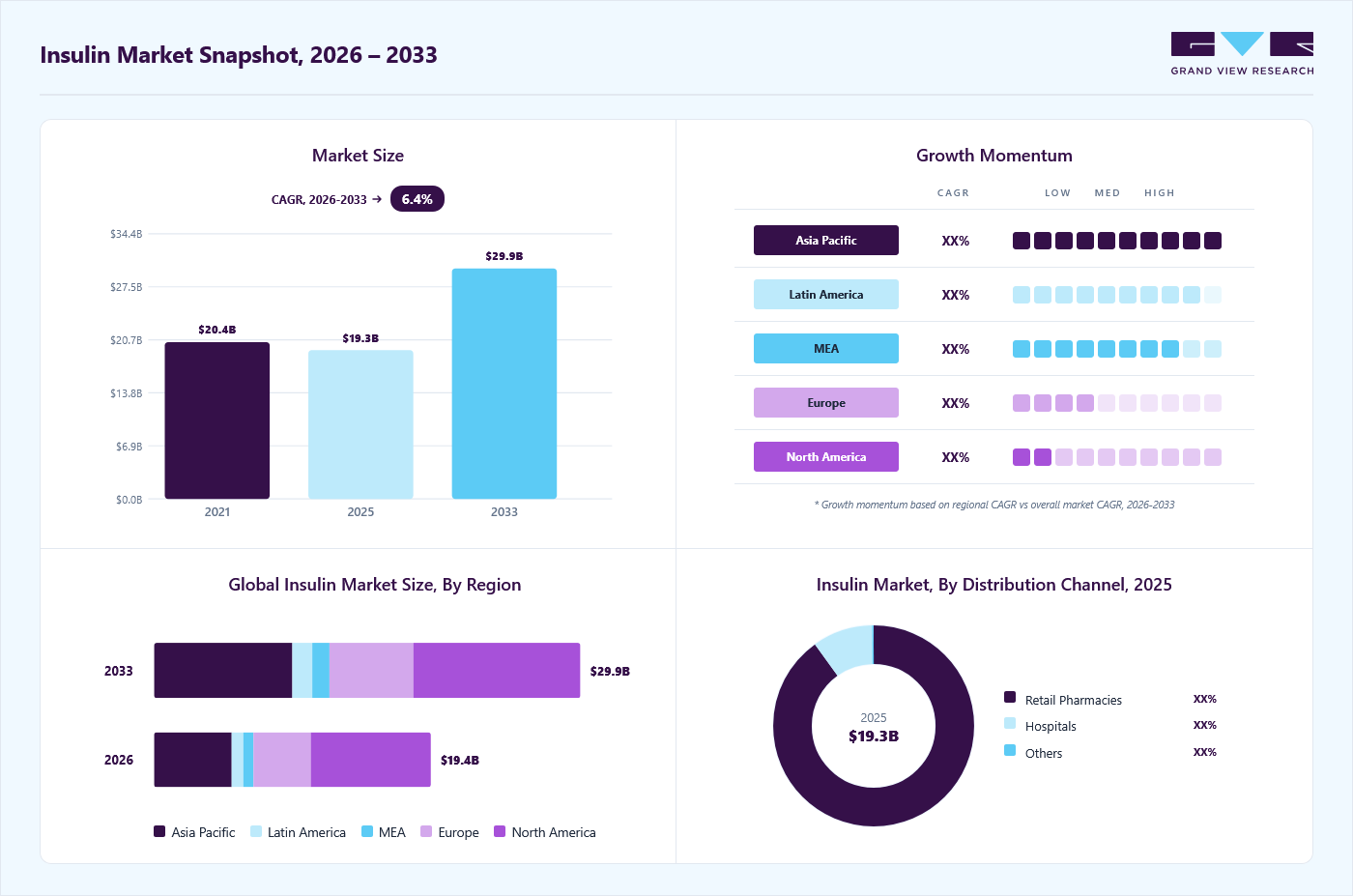

Market Size, 2025

$19.3BMarket Estimate, 2026

$19.4BMarket Forecast, 2033

$29.9BCAGR, 2026–2033

6.4%Insulin Market Summary

The global insulin market size was valued at USD 19.3 billion in 2025 and is projected to grow from USD 19.4 billion in 2026 to USD 29.9 billion by 2033, growing at a CAGR of 6.4 % from 2026 to 2033. North America dominated the market with the largest revenue share of 44.0% in 2025. Advances in formulations, such as rapid-acting and long-acting, enhance treatment options and patient adherence.

Key Market Trends & Insights

- By product: Long-acting insulin segment led the market with the largest revenue share of 50.9% in 2025.

- By application: Type-1 diabetes segment led the market with the largest revenue share of 78.4% in 2025.

- By type: Insulin analog segment led the market with the largest revenue share of 87.5% in 2025.

- By distribution channel: Retail pharmacies segment led the market with the largest revenue share of 90.0% in 2025.

Regional Highlights

- Largest regional market: North America (44.0% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 19.3 Million

- Estimated market size in 2026: USD 19.4 Million

- Projected market size by 2033: USD 29.9 Million

- CAGR (2026-2033): 6.4%

The expected commercialization of pipeline drugs and novel insulin combinations, such as once-weekly insulins like Efsitora alfa, Icodec and IcoSema propels the demand. These investigational therapies enhance diabetes management by offering improved glycemic control and reduced injection frequency with more convenient administration options. Their success in Phase 3 trials could lead to new treatment alternatives for diabetic patients.")

The rising prevalence of diabetes, particularly type 2, drives demand for insulin therapies, expanding the market. Increased awareness, early diagnosis, and the need for lifelong treatment create a sustained need for various formulations and delivery systems. The International Diabetes Federation (IDF) highlights the growing global burden of the disease, with approximately 540 million adults aged 20-79 currently living with the condition. By 2045, this number is projected to rise to 783 million, accounting for 10.5% of the adult population. Over 90% of these individuals have type 2, driven by factors such as urbanization, aging populations, decreased physical activity, and rising obesity rates. Three-quarters of adults with diabetes reside in low- and middle-income countries, and 240 million remain undiagnosed. The IDF emphasizes the importance of preventive measures, early diagnosis, and proper care to mitigate disease complications. The IDF Diabetes Atlas serves as a key resource, providing vital statistics on diabetes prevalence, mortality, and healthcare costs globally, aiming to improve lives and prevent diabetes in at-risk populations.

The rising prevalence of obesity and related conditions like type 2 drives demand for products, fueling market growth as more individuals require effective diabetes management and treatment solutions. In 2022, 1 in 8 people globally were living with obesity, with adult obesity more than doubling since 1990. Approximately 2.5 billion adults were overweight, and 890 million lived with obesity. Childhood obesity is also rising, with 37 million children under 5 and 390 million aged 5-19 classified as overweight. Obesity results from an energy imbalance and is influenced by environmental, psychosocial, and genetic factors. It increases the risk of type 2, cardiovascular disease, and certain cancers, impacting quality of life. Preventive measures include promoting healthy diets and physical activity, with a focus on multisectoral actions to create supportive environments and enhance health systems to manage obesity effectively.

The study titled "Advances in Nanomedicine for Precision Insulin Delivery" published in July 2024 in the journal Pharmaceuticals. The article examines the advancements in nanomedicine aimed at improving delivery systems, focusing on enhancing drug stability, bioavailability, and precision targeting for disease management. Diabetes mellitus is a metabolic disorder characterized by improper glucose utilization and excessive production, leading to hyperglycemia. Its global prevalence is projected to rise to 783.2 million by 2045. Insulin therapy is essential for type 1 diabetes due to β-cell dysfunction, with intensive insulin regimens reducing microvascular complications but increasing the risk of severe hypoglycemia. Innovations in delivery, including nanomedicine approaches, enhance drug stability, bioavailability, and targeted delivery, addressing compliance issues. Future developments focus on creating advanced nanocarriers for improved management and patient outcomes. Advancements in nanomedicine for precision delivery enhance drug efficacy, improve patient adherence, and reduce complications, driving market growth by meeting increasing demand for effective management solutions.

Market Dynamics

The insulin market is influenced by the growing prevalence of diabetes and the increasing need for therapies that improve treatment accessibility and support long-term disease management. Market participants are focusing on the development and commercialization of biosimilar insulin products to address cost-related barriers and expand product availability across healthcare systems. The market is also witnessing efforts to diversify insulin portfolios through regulatory approvals and product launches across both developed and emerging markets. For instance, in February 2025, Sanofi received U.S. FDA approval for Merilog (insulin-aspart-szjj), the first rapid-acting insulin biosimilar approved in the U.S. The product was approved as a biosimilar to NovoLog (insulin aspart) for improving glycemic control in adults and pediatric patients with diabetes mellitus. The approval added a new biosimilar product to the rapid-acting insulin category. Such regulatory developments are contributing to the expansion of biosimilar insulin offerings and increasing the availability of insulin treatment options across key markets. The increasing requirement for insulin-based therapy is expected to support market expansion over the forecast period.

The insulin market is primarily driven by the increasing prevalence of diabetes worldwide, resulting in a larger patient population requiring long-term insulin therapy. Rising rates of obesity, sedentary lifestyles, and aging populations continue to contribute to the incidence of both type 1 and type 2 diabetes. As diagnosis rates improve and treatment guidelines emphasize early glycemic control, demand for insulin products is increasing across hospital, retail, and specialty care settings. The need for sustained blood glucose management has supported the utilization of basal, rapid-acting, and premixed insulin formulations. According to the International Diabetes Federation, approximately 589 million adults were living with diabetes globally in 2025, indicating a substantial patient population requiring ongoing diabetes management. In response, healthcare systems are expanding diabetes screening, diagnosis, and treatment programs to improve disease management and reduce the risk of diabetes-related complications. The increasing number of diagnosed patients and the continued requirement for insulin-based treatment are contributing to prescription demand across multiple healthcare settings. These factors are expected to support the growth of the insulin market over the forecast period.

The insulin market faces challenges related to pricing pressure and reimbursement restrictions across several healthcare systems. Insulin manufacturers are operating in an environment where payers and regulatory authorities are implementing measures to control diabetes treatment expenditures, particularly for insulin analogs. In major markets, reimbursement decisions and formulary placement can influence product uptake, limiting the use of higher-priced insulin products. The growing availability of biosimilar insulin products has also intensified competition across key insulin segments, contributing to pricing pressure within the market. Furthermore, procurement programs and tender-based purchasing mechanisms in several countries prioritize cost-effective treatment options, creating challenges for premium-priced formulations. These market dynamics can affect manufacturers' pricing strategies and commercial performance. In November 2025, researchers from Yale School of Medicine reported that 37% of surveyed insulin users experienced insulin rationing due to high costs, insurance delays, or pharmacy shortages. The findings indicate that affordability and access barriers continue to affect insulin utilization despite ongoing pricing reforms and patient support initiatives. Such factors may influence treatment adherence and access to insulin therapy, thereby affecting market growth during the forecast period.

The development of reduced-frequency insulin therapies presents an opportunity for companies operating in the insulin market. Current insulin regimens often require daily administration, creating a treatment burden for patients requiring long-term diabetes management. As a result, manufacturers are investing in insulin formulations designed to extend dosing intervals while maintaining glycemic control. Reduced-frequency therapies have the potential to improve treatment adherence and expand available options within diabetes care. This trend is supporting the development of next-generation insulin products designed to reduce dosing frequency without compromising therapeutic outcomes. For instance, in March 2025, Novo Nordisk reported results from the ONWARDS clinical program evaluating insulin icodec, a once-weekly basal insulin for individuals with diabetes. The study demonstrated HbA1c reductions comparable to those achieved with once-daily basal insulin therapies while maintaining a safety profile consistent with established insulin treatments. The findings highlighted the potential of insulin icodec to reduce injection frequency from seven injections per week to one injection per week. Such developments indicate increasing industry focus on extended-duration insulin formulations and are expected to create opportunities for product differentiation and portfolio expansion within the insulin market.

Analyst Perspective

The insulin market is characterized by continuous product development focused on improving glycemic control, treatment convenience, and patient access. Market competition is centered on expanding insulin portfolios across rapid-acting, long-acting, and combination insulin categories, while increasing emphasis is being placed on biosimilar insulin commercialization and reduced-frequency dosing regimens. Leading manufacturers leverage established brands, global manufacturing networks, and reimbursement coverage to maintain their market position, whereas regional and biosimilar-focused companies compete through cost-effective offerings and expansion into underserved markets. Continued investments in next-generation insulin formulations, delivery devices, and manufacturing capabilities are expected to support market expansion and create opportunities for both established participants and emerging innovators within the market.

Product Insights

Based on product, the long-acting insulin segment led the market with the largest revenue share of 50.9% in 2025 due to its crucial role in managing diabetes. These products provide stable and prolonged glucose control, reducing the risk of hypoglycemia and enhancing patient adherence. The growing prevalence of Type 2, combined with an increasing preference for convenient dosing regimens, drives demand for long-acting formulations. Innovations in long-acting insulin products, including improved formulations that offer better pharmacokinetics and ease of use, further bolster this segment. As healthcare providers prioritize effective and reliable diabetes management, long-acting insulin continues to capture a substantial market share.

The biosimilar insulin segment is projected to expand at a lucrative CAGR during the forecast period, driven by increasing demand for cost-effective management solutions. As healthcare systems seek to reduce expenses, biosimilars offer a more affordable alternative to branded insulins while maintaining similar efficacy and safety profiles. The growing prevalence of diabetes, alongside the patent expirations of several major products, is facilitating the entry of biosimilars into the market. Additionally, supportive regulatory frameworks and increased awareness among healthcare providers and patients about biosimilars are expected to fuel this segment's growth, enhancing accessibility to therapies.

Application Insights

Based on application, the Type-1 diabetes segment led the market with the largest revenue share of 78.4% in 2025, driven by the rising incidence of this autoimmune condition among children and adults. As Type 1 requires lifelong therapy for blood glucose management, the demand for various formulations, including rapid-acting, long-acting, and combination insulins, continues to grow. Advances in delivery systems, such as pumps and pens, further support this segment's expansion. Increased awareness of diabetes management and improvements in healthcare access are also contributing to the rising adoption of these therapies among individuals with Type 1, solidifying its position as the largest application segment.

The Type 2 Diabetes Mellitus segment is projected to be the fastest-growing application area in the market, driven by the rising prevalence of this metabolic disorder globally. Factors contributing to this growth include increasing obesity rates, sedentary lifestyles, and an aging population. Unlike Type 1 diabetes, Type 2 can often be managed with lifestyle changes initially, but many patients eventually require these therapies. The growing awareness of diabetes management and advancements in formulations and delivery systems are expected to fuel demand. Additionally, government initiatives promoting education and treatment accessibility will further support the expansion of this segment.

Type Insights

Based on type, the insulin analog segment led the market with the largest revenue share of 87.5% in 2025 due to its advantages over human insulin. Analog insulins, including rapid-acting and long-acting formulations, offer improved glycemic control and flexibility in managing blood sugar levels. Their pharmacokinetic profiles enable patients to tailor insulin administration around meal times, reducing the risk of hypoglycemia and enhancing overall treatment adherence. With the rising prevalence of diabetes and increasing patient awareness of effective management, the demand for analog is expected to grow. Additionally, ongoing innovations in formulation and delivery technologies are likely further to propel this segment's dominance in the market.

The human insulin segment is expected to experience the highest growth rate in the market due to several factors. As awareness of diabetes management increases, more patients and healthcare providers recognize the efficacy and affordability of human insulin. This segment is particularly appealing in emerging markets where cost constraints are significant. Additionally, introducing more convenient delivery methods, such as prefilled pens and pumps, enhances patient adherence. These elements combined are likely to drive a robust growth trajectory for the segment during the forecast period, catering to the rising demand for effective treatments.

Distribution Channel Insights

Based on distribution channel, the retail pharmacies segment led the market with the largest revenue share of 90.0% in 2025. This dominance is attributed to the widespread accessibility of products through retail channels, making it convenient for patients to obtain their medications. Retail pharmacies often offer a range of types, including rapid-acting, long-acting, and biosimilar options, catering to diverse patient needs. Furthermore, initiatives to improve affordability and awareness of diabetes management have led to increased foot traffic in retail pharmacies, solidifying their role as a primary source for insulin therapy among individuals with diabetes.

The others segment, encompassing online pharmacies, is anticipated to experience the fastest growth during the forecast period. The increasing adoption of e-commerce and telehealth services has made such products more accessible to patients who prefer the convenience of online shopping. This segment benefits from a growing trend of patients seeking affordable and discreet options for their diabetes management. Additionally, online pharmacies often provide competitive pricing, home delivery services, and extensive product offerings, further driving their popularity and growth in the market.

Regional Insights

North America dominated the insulin market with the largest revenue share of 44.0% in 2025 due to several key factors. High prevalence rates of dry eye syndrome, driven by aging populations and increased screen time, contribute significantly to market growth. The region benefits from advanced healthcare infrastructure, which supports the rapid adoption of innovative treatments and advanced diagnostic tools. Additionally, the strong market presence of leading pharmaceutical companies and a high rate of consumer awareness further boost market expansion.

U.S. Insulin Market Trends

The insulin market in the U.S. held the largest share in the North America region in 2025 due to a high incidence of diabetes, particularly Type 2 diabetes, coupled with increasing demand for advanced therapies such as rapid-acting and long-acting insulin. The presence of leading pharmaceutical companies, extensive research, and innovation in analogs and biosimilars further strengthened the market. Additionally, favorable reimbursement policies, strong healthcare infrastructure, and the growing adoption of combination products contributed to the market’s growth.

Europe Insulin Market Trends

The insulin market in Europe is experiencing notable growth due to increasing awareness of diabetes management and the rising prevalence of both Type 1 and Type 2 diabetes. Enhanced healthcare infrastructure demand for advanced therapies such as long-acting and rapid-acting insulin. The market also benefits from the growing adoption of biosimilars, which offer cost-effective alternatives. Favourable reimbursement policies and a strong focus on innovation, particularly in delivery systems, contribute to this growth. Major distribution channels include hospitals, retail pharmacies, and other healthcare providers, ensuring widespread access.

The UK insulin market is a major player in the Europe region due to its well-established healthcare system, widespread diabetes screening programs, and strong government support for diabetes management. The National Health Service (NHS) provides broad access to both human insulin and insulin analogs, contributing to increased demand. Additionally, adopting biosimilar products, combined with favorable reimbursement structures, enhances affordability and accessibility.

Insulin market in Germany hold a significant market share due to its advanced healthcare infrastructure and increasing prevalence of diabetes, especially Type 2 diabetes. Strong government initiatives to promote diabetes awareness and early diagnosis have boosted the demand for rapid-acting and long-acting products. Germany’s focus on research and development in biosimilar and innovative delivery systems such as pens has further driven market growth.

Asia Pacific Insulin Market Trends

The Asia-Pacific insulin market is rapidly expanding, driven by rising diabetes prevalence across populous countries like India and China. Growing healthcare awareness, improving healthcare infrastructure, and increasing adoption of analogs are key drivers in the region. Many countries in Asia-Pacific are also focusing on cost-effective biosimilar options, making treatments more affordable. Additionally, increasing urbanization and sedentary lifestyles further fuel the regional demand for therapies.

China’s insulin market is experiencing significant growth due to the country’s large diabetic population, particularly those with Type 2 diabetes. Government health initiatives to improve diabetes care and a strong focus on expanding healthcare access in both urban and rural areas are key market drivers. The adoption of biosimilar has increased, making therapies more affordable. China also benefits from substantial investment in R&D and the local production, reducing import dependency.

Insulin market in Japan is well-established, with a high rate of diabetes awareness and management, especially for Type 1. The country’s aging population and high prevalence of diabetes-related complications have driven demand for advanced therapies, including long-acting and rapid-acting . Japan is also a leader in adopting innovative delivery systems, such as pumps and continuous glucose monitors.

Brazil Insulin Market Trends

The Brazil insulin market is expanding due to the rising prevalence of diabetes, particularly Type 2 diabetes, driven by lifestyle changes and increasing obesity rates. Government initiatives aimed at improving diabetes management, including distributing free insulin through public health programs, contribute to market growth. Brazil is also seeing a shift toward insulin analogs and biosimilars, providing more treatment options for patients.

MEA Insulin Market Trends

The MEA insulin market is growing steadily, fuelled by a rising incidence of diabetes, particularly in urban areas with increasing rates of obesity and sedentary lifestyles. Governments across the region are investing in diabetes awareness and management programs, leading to greater demand for insulin, including both human insulin and analogs.

Saudi Arabia insulin market is a major player in the region due to its high prevalence of diabetes and strong government efforts to address the growing health issue. The country has invested in improving diabetes care and expanding access to both human insulin and insulin analogs. Additionally, the adoption of advanced delivery systems and biosimilar has been on the rise, making treatment more accessible and affordable.

Key Insulin Company Insights

The competitive landscape of the insulin market is dominated by major global players such as Novo Nordisk, Sanofi, and Eli Lilly, who led in product innovation and market share. These companies continuously invest in research and development, focusing on next-generation therapies, such as biosimilars and analogs, to meet the growing demand. Emerging players in regions like Asia-Pacific are increasingly gaining traction by offering cost-effective biosimilar products, intensifying competition. Strategic partnerships, mergers, and acquisitions are common as companies aim to expand their product portfolios and global reach.

Additionally, advancements in delivery systems further intensify the competition within the market. Many companies opting for geographical expansion, strategic collaborations, and partnerships in emerging and economically favorable regions through mergers and acquisitions. For instance, in February 2022, Biocon announced the acquisition of Viatris’ biosimilar portfolio for USD 3.335 billion. This acquisition strengthened Biocon’s biosimilar product portfolio and improved its revenue generation.

Key Insulin Companies:

The following key companies have been profiled for this study on the insulin market.

-

Novo Nordisk A/S

-

Eli Lilly and Company

-

Sanofi

-

Biocon Ltd

-

Wockhardt

-

Boehringer Ingelheim International GmbH

-

Julphar

-

United Laboratories International Holdings Limited

-

Tonghua Dongbao Pharmaceutical Co. Ltd.

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Novo Nordisk A/S, Eli Lilly and Company, Sanofi)

Focus on maintaining leadership in the insulin market through portfolio expansion across rapid-acting, long-acting, and next-generation insulin products. Invest in clinical development programs for reduced-frequency insulin therapies, advanced delivery devices, and digital diabetes management solutions. Strengthen market access through reimbursement agreements, healthcare provider engagement, and large-scale global manufacturing operations.

Extensive insulin product portfolios, strong physician adoption, established reimbursement coverage, global commercial infrastructure, and significant manufacturing capacity. Strong presence across North America, Europe, Asia-Pacific, and other major insulin markets supported by long-term clinical evidence and brand recognition.

Exposure to pricing reforms, payer negotiations, and increasing competition from biosimilar insulin manufacturers. Dependence on mature insulin franchises in developed markets may limit revenue expansion opportunities.

Emerging and Regional Players (Biocon, Tonghua Dongbao Pharmaceutical Co. Ltd., Wockhardt, Julphar, United Laboratories International Holdings Limited)

Focus on biosimilar insulin commercialization, regional market expansion, and cost-competitive manufacturing. Pursue regulatory approvals, technology partnerships, and government procurement contracts to increase market penetration. Expand production capabilities to address demand for affordable insulin products across emerging markets.

Competitive pricing, lower manufacturing costs, growing biosimilar insulin portfolios, and strong positions within regional healthcare markets. Ability to participate in public healthcare tenders and address affordability-driven demand.

Limited presence in high-value developed markets, lower brand recognition among prescribers, and dependence on regulatory approvals for international expansion. Smaller commercial infrastructure compared to multinational insulin manufacturers may restrict market reach.

Recent Developments

-

In January 2024, Novo Nordisk concluded the COMBINE 3 phase 3a trial, evaluating IcoSema, a combination of basal insulin icodec and semaglutide administered once weekly. The study found that IcoSema effectively reduced HbA1c levels and was comparable to daily insulin glargine U100 and insulin aspart. The treatment also resulted in significant weight reduction and fewer hypoglycemia incidents. This suggests IcoSema could streamline diabetes management by replacing daily injections with a single weekly dose. Additional findings from the broader COMBINE program are expected later in the year.

-

In September 2023, Novo Nordisk partnered to boost human insulin production in South Africa, to provide affordable insulin throughout Africa. The initiative aims to reach 4.1 million individuals with Type 1 and Type 2 diabetes by 2026. This effort aligns with the African Union's Pharmaceutical Manufacturing Plan, addressing the rising need for diabetes care across a continent where 24 million adults are living with the condition. Through the iCARE program, insulin will be distributed to health authorities at a cost of USD 3 per vial, focusing on increasing local production, distribution, and equitable access to treatment.

-

In March 2023, Eli Lilly announced a 70% reduction in prices for its most commonly prescribed insulins and capped out-of-pocket costs for patients at USD 35 per month. Effective May 1, 2023, the list price of Insulin Lispro will be USD 25 per vial. These measures aim to improve insulin accessibility for people with diabetes amid rising costs in the healthcare system.

Insulin Market Report Scope

Report Attribute

Details

Market size in 2025

USD 19.3 billion

Estimated market size in 2026

USD 19.4 billion

Projected market size by 2033

USD 29.9 billion

Growth rate

CAGR of 6.4% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, type, distribution channel, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; Russia; Iceland; Finland; China; Japan; India; South Korea; Australia; Thailand; Singapore; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait; Israel

Key companies profiled

Novo Nordisk A/S, Eli Lilly and Company, Sanofi, Biocon Ltd, Wockhardt, Boehringer Ingelheim International GmbH, Julphar, United Laboratories International Holdings Limited, Tonghua Dongbao Pharmaceutical Co. Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Insulin Market Report Segmentation

This report forecasts revenue growth at country levels and provides an analysis on the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global insulin market report based on product, application, type, distribution channel, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Rapid-Acting Insulin

-

Long-Acting Insulin

-

Combination Insulin

-

Biosimilar

-

Others

-

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Human Insulin

-

Insulin Analog

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Type 1 Diabetes Mellitus

-

Type 2 Diabetes Mellitus

-

-

Distribution Channel Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals

-

Retail Pharmacies

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Research Methodology

The insulin market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each insulin segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Product

Revenue capture definition

Rapid-Acting Insulin

Includes revenue generated from rapid-acting insulin products used to manage postprandial blood glucose levels. This segment covers insulin lispro, insulin aspart, insulin glulisine, and other rapid-acting insulin formulations marketed in vials, cartridges, and prefilled pens. This segment excludes long-acting insulin, combination insulin products, and non-insulin diabetes therapies.

Long-Acting Insulin

Includes revenue generated from basal insulin products designed to provide extended glucose control. This segment covers insulin glargine, insulin detemir, insulin degludec, insulin icodec, and other long-acting insulin formulations marketed in vials, cartridges, and prefilled pens. This segment excludes rapid-acting insulin, combination insulin products, and non-insulin diabetes therapies.

Combination Insulin

Includes revenue generated from insulin products containing two or more insulin components within a single formulation. This segment covers premixed human insulin products and premixed insulin analog formulations, including biphasic insulin aspart and insulin lispro mixtures. This segment excludes standalone rapid-acting insulin products and standalone long-acting insulin products.

Biosimilar Insulin

Includes revenue generated from biosimilar insulin products approved as reference product alternatives through biosimilar regulatory pathways. This segment covers biosimilar insulin aspart, biosimilar insulin glargine, biosimilar insulin lispro, and other biosimilar insulin formulations. This segment excludes originator insulin products.

Others

Includes revenue generated from insulin products not classified under rapid-acting, long-acting, combination, or biosimilar insulin categories. This segment covers regular human insulin, NPH insulin, concentrated insulin formulations, and other insulin products that do not fall within the defined product segments.

Segment - Type

Revenue capture definition

Human Insulin

Includes revenue generated from recombinant human insulin products. This segment covers regular human insulin, NPH insulin, and premixed human insulin formulations marketed for diabetes management. This segment excludes insulin analog products.

Insulin Analog

Includes revenue generated from insulin analog products developed to provide modified pharmacokinetic profiles. This segment covers rapid-acting, long-acting, ultra-long-acting, and premixed insulin analog formulations. This segment excludes recombinant human insulin products.

Segment - Application

Revenue capture definition

Type 1 Diabetes Mellitus

Includes insulin products prescribed for the treatment and management of Type 1 Diabetes Mellitus across all insulin classes and formulations. This segment covers rapid-acting insulin, long-acting insulin, combination insulin, human insulin, insulin analogs, and other insulin products utilized by patients diagnosed with Type 1 Diabetes Mellitus. This segment excludes insulin use associated with Type 2 Diabetes Mellitus and other indications.

Type 2 Diabetes Mellitus

Includes insulin products prescribed for the treatment and management of Type 2 Diabetes Mellitus across all insulin classes and formulations. This segment covers basal insulin, prandial insulin, premixed insulin, human insulin, insulin analogs, and other insulin products utilized by patients diagnosed with Type 2 Diabetes Mellitus. This segment excludes insulin use associated with Type 1 Diabetes Mellitus and other indications.

Segment -Distribution Channel

Revenue capture definition

Hospitals

Includes revenue generated from insulin products purchased and dispensed through public hospitals, private hospitals, academic medical centers, hospital pharmacies, inpatient care facilities, and hospital-affiliated outpatient centers. This segment excludes retail pharmacies, online pharmacies, mail-order pharmacies, specialty pharmacies, and other non-hospital distribution channels.

Retail Pharmacies

Includes revenue generated from insulin products dispensed through chain pharmacies, independent pharmacies, community pharmacies, drugstores, and supermarket pharmacies for outpatient use. This segment excludes hospital procurement channels, specialty pharmacies, government distribution programs, and online pharmacy sales.

Others

Includes revenue generated from insulin products distributed through online pharmacies, mail-order pharmacies, specialty pharmacies, diabetes clinics, government procurement programs, military healthcare systems, public health distribution programs, and other alternative distribution channels not classified under hospitals or retail pharmacies.

Estimation Model

The Insulin Market is estimated through a comprehensive combination of secondary research, primary research, and quantitative market modeling. The study begins with extensive secondary research from sources including company annual reports, SEC filings, investor presentations, pharmaceutical databases, healthcare journals, diabetes association reports, government health statistics, and regulatory authorities. Revenue generated from insulin products by leading manufacturers is collected and analyzed, while epidemiological data such as diabetes prevalence, insulin-dependent patient population, treatment rates, and healthcare expenditure are assessed to understand market demand.

The market size is calculated using both bottom-up and top-down approaches. In the bottom-up method, insulin sales revenues from major manufacturers are aggregated across regions and product categories, including rapid-acting, short-acting, intermediate-acting, long-acting, ultra-long-acting, and premixed insulin formulations. Revenue contributions from biosimilar insulin products, insulin pens, cartridges, and vials are also incorporated. In the top-down approach, the overall diabetes therapeutics market is analyzed, and the share attributable to insulin therapy is derived using prescription volume data, treatment penetration rates, average selling prices, and regional healthcare spending patterns.

Primary research is conducted with key industry stakeholders, including pharmaceutical executives, endocrinologists, diabetologists, hospital procurement managers, distributors, and healthcare policy experts. These interviews validate market assumptions related to pricing trends, product adoption, competitive landscape, reimbursement policies, and future demand outlook. The collected data is then subjected to data triangulation, where findings from supply-side, demand-side, and macroeconomic analyses are cross-verified. Forecasting models incorporating diabetes incidence rates, aging population trends, biosimilar penetration, innovation in insulin delivery devices, and regulatory developments are subsequently applied to generate reliable market size estimates and future growth projections for the global Insulin Market.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Insulin Product Portfolio and Technology Assessment

Detailed evaluation of market dynamics across rapid-acting, long-acting, combination, human insulin, insulin analog, and biosimilar insulin segments, including adoption trends, competitive positioning, and growth opportunities.

Helps identify high-revenue product segments, commercialization opportunities, and areas of competitive differentiation.

Diabetes Treatment Landscape Assessment

Analysis of insulin utilization patterns across Type 1 Diabetes Mellitus and Type 2 Diabetes Mellitus, including treatment adoption trends, patient population dynamics, and prescribing patterns.

Supports identification of demand drivers and high-opportunity patient segments across the diabetes treatment landscape.

Insulin Delivery and Patient Management Evaluation

Assessment of insulin delivery formats, including vials, cartridges, prefilled pens, and connected insulin delivery solutions, along with their impact on treatment adoption and patient management practices.

Provides insights into evolving treatment preferences and opportunities for product differentiation.

Next-Generation Insulin Development Landscape

Evaluation of developments in biosimilar insulin products, once-weekly insulin therapies, advanced insulin formulations, and emerging diabetes management technologies.

Identifies innovation-focused growth opportunities and supports strategic investment and portfolio planning decisions.

Competitive Intelligence and Benchmarking Assessment

Comparative analysis of product portfolios, pipeline activities, manufacturing capabilities, geographic presence, pricing strategies, reimbursement access, and strategic initiatives of leading insulin market participants.

Supports market positioning, partnership evaluation, competitive intelligence, and expansion strategy development.

Frequently Asked Questions About This Report

Some of the key players in the insulin market are Novo Nordisk A/S; Eli Lilly and Company; Sanofi; Biocon Ltd; Wockhardt; Boehringer Ingelheim International GmbH; Julphar; United Laboratories International Holdings Limited; and Tonghua Dongbao Pharmaceutical Co. Ltd.

The major factors driving market growth are the rising prevalence of diabetes, rising geriatric and obese population base, and advancements in insulin delivery.

North America dominated with a 44.0% revenue share in 2025.

Type-1 diabetes segment led the market with the largest revenue share of 78.4% in 2025.

Insulin analog segment led the market with the largest revenue share of 87.5% in 2025.

The global insulin market size was valued at USD 19.3 billion in 2025 and is anticipated to reach USD 19.4 billion in 2026.

The global insulin market is expected to witness a compound annual growth rate of 6.4% from 2026 to 2033 to reach USD 29.9 billion by 2033.

Long-acting insulin segment accounted for a share of 50.9% in 2025 due to high prescription rate owing the longer duration of effect and lesser amount of injections required.

About the Author(s)

Pharmaceuticals Research Team

Healthcare · PharmaceuticalsThis report was authored by the pharmaceuticals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the pharmaceuticals segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.