- Home

- »

- Advanced Interior Materials

- »

-

Limestone Market Size, Share & Growth Report, 2026-2033GVR Report cover

![Limestone Market (2026 - 2033)Report]()

Limestone Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (High Calcium, Magnesian), By End-use (Building & Construction, Iron & Steel, Agriculture, Chemical), By Region (North America, Europe, Asia Pacific), And Segment Forecasts

Market Size, 2025

$84.6BMarket Estimate, 2026

$90.5BMarket Forecast, 2033

$141.3BCAGR, 2026–2033

6.6%Limestone Market Summary

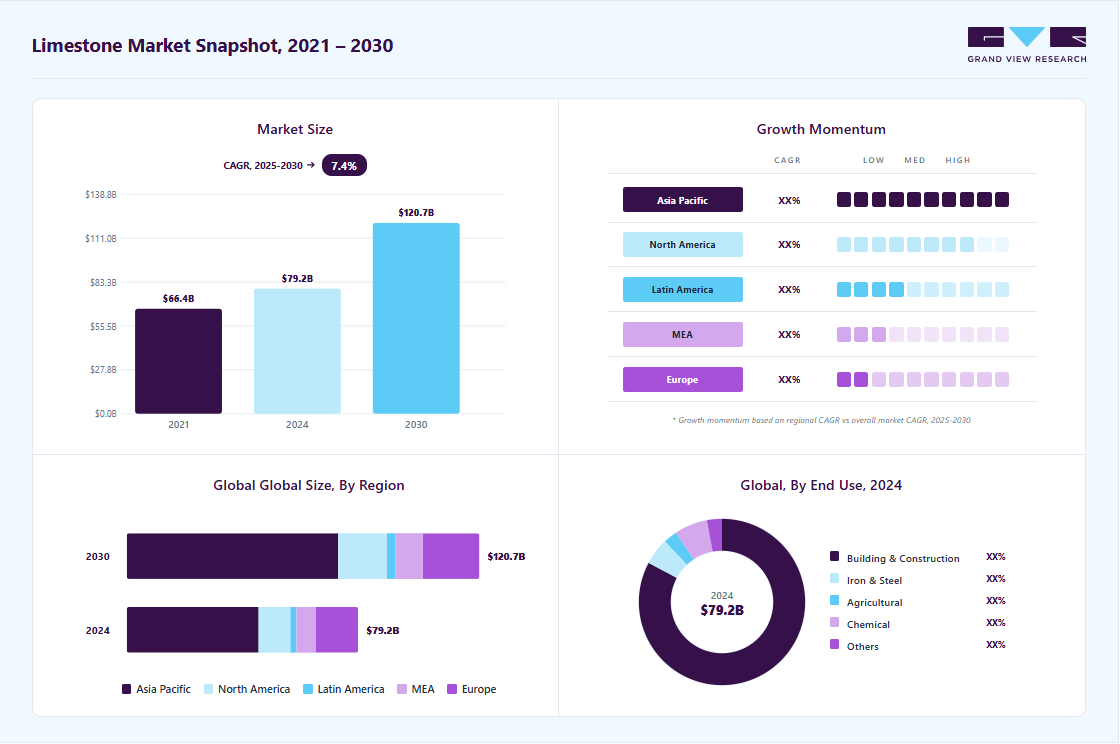

The global limestone market size was valued at USD 84.6 billion in 2025 and is projected to grow from USD 90.5 billion in 2026 to USD 141.3 billion by 2033, at a CAGR of 6.6% from 2026 to 2033. Asia Pacific held the largest global revenue share of 57.4 in 2025. Growing investments in infrastructure development, urbanization, residential and commercial construction projects, and expanding cement and steel production activities are driving limestone demand worldwide.

Key Market Trends & Insights

- By product: High calcium limestone held the largest revenue share of 78.8% in 2025.

- By end use: Building & construction held the largest market share of 82.7% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (57.4% revenue share, 2025)

- By country: China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 84.6 Billion

- Estimated market size in 2026: USD 90.5 Billion

- Projected market size by 2033: USD 141.3 Billion

- CAGR (2026-2033): 6.6%

The limestone industry is witnessing significant growth due to increasing demand from construction, cement manufacturing, steel production, agriculture, and environmental applications. Limestone serves as a critical raw material for cement and concrete production, making it indispensable for infrastructure development, urbanization, and industrial expansion worldwide. Rising investments in residential and commercial construction projects, transportation networks, and public infrastructure are significantly driving limestone consumption across both developed and emerging economies.")

The growing focus on environmental sustainability is also supporting market growth, as limestone is widely used in water and wastewater treatment, flue gas desulfurization systems, and environmental remediation applications. In addition, increasing adoption of low-carbon blended cements and specialty calcium carbonate products is creating new opportunities for limestone producers, while expanding steel production and agricultural soil conditioning activities continue to strengthen demand across key end-use sectors.

Market Dynamics

The expansion of construction and infrastructure activities is the primary demand driver for the limestone market, as limestone is a key raw material for cement production, aggregates, road base materials, and building stone applications. Rapid urbanization, population growth, and increasing government investments in transportation networks, residential housing, commercial buildings, and industrial facilities continue to stimulate limestone consumption globally.

Large-scale infrastructure initiatives across emerging economies, particularly in the Asia Pacific and the Middle East, are generating substantial demand for cement and concrete, directly increasing limestone requirements. According to industry estimates, the global construction industry is expected to maintain steady long-term growth, supported by smart city developments, renewable energy projects, and modernization of aging infrastructure, reinforcing the critical role of limestone in the global construction value chain.

Environmental regulations and quarrying restrictions represent a significant restraint for the limestone market due to the industry's dependence on mining and extraction activities. Limestone quarrying can lead to land degradation, biodiversity loss, dust emissions, noise pollution, and impacts on local water resources, prompting governments and regulatory authorities to impose stricter permitting requirements and environmental compliance standards. In many regions, obtaining approvals for new quarry developments or expanding existing operations has become increasingly complex and time-consuming. Additionally, growing pressure to reduce carbon emissions from cement and lime production facilities increases operational costs and may limit production expansion, thereby affecting the long-term growth prospects of limestone producers.

The growing emphasis on sustainable construction and environmental protection presents a significant opportunity for the limestone market. Limestone is increasingly being utilized in blended cements to reduce clinker content and lower carbon emissions associated with cement production. Furthermore, demand for limestone-based products is rising in water and wastewater treatment, flue gas desulfurization systems, soil stabilization, and environmental remediation applications. Governments and industries worldwide are investing in emission control technologies and water infrastructure upgrades to meet stricter environmental standards, creating new growth avenues for limestone suppliers. The increasing adoption of low-carbon construction practices and circular economy initiatives is expected to further expand the use of limestone-derived materials across both industrial and environmental sectors.

Analyst Perspective

Limestone may be one of the world's oldest industrial minerals, but it remains fundamental to modern economies. Demand continues to be driven by construction, cement, and steel production, while emerging applications in low-carbon cement, water treatment, and environmental remediation are creating new growth avenues. Although environmental regulations and quarrying restrictions pose challenges, producers with high-quality reserves and integrated operations are well-positioned to benefit from ongoing infrastructure development and sustainability initiatives worldwide.

Product Insights

High calcium limestone dominated the limestone industry, accounting for 78.8% revenue share in 2025. The segment's leadership is attributed to its extensive use in cement manufacturing, construction aggregates, steelmaking, lime production, and environmental applications. High-calcium limestone is preferred across major industries due to its high calcium carbonate content, consistent quality, and suitability for producing cement clinker, quicklime, hydrated lime, and calcium carbonate products. Strong infrastructure development, urbanization, and industrial expansion across Asia Pacific and other emerging economies continue to drive substantial demand for high-calcium limestone.

Magnesian limestone is projected to register the fastest CAGR of 6.9% during the forecast period. Growth is primarily supported by increasing demand from steel manufacturing, agricultural soil conditioning, environmental treatment processes, and specialty construction applications. The presence of magnesium carbonate makes magnesian limestone particularly suitable for metallurgical operations and agricultural applications that require soil nutrient enhancement and pH regulation. Rising agricultural productivity initiatives and growing steel production activities are expected to further accelerate demand for magnesian limestone globally.

Application Insights

Building & construction emerged as the largest end-use segment in the limestone market, accounting for 82.7% revenue share in 2025. Limestone remains a fundamental raw material for cement production, concrete manufacturing, road construction, infrastructure projects, and building aggregates. Rapid urbanization, population growth, and increasing investments in residential, commercial, and public infrastructure projects continue to support strong limestone consumption. The segment's dominance reflects the indispensable role of limestone in modern construction and infrastructure development worldwide.

The chemical segment is expected to witness the fastest growth, registering a CAGR of 7.6% during the forecast period. Growth is driven by increasing utilization of limestone in the production of precipitated calcium carbonate (PCC), ground calcium carbonate (GCC), lime-based chemicals, glass manufacturing, and various industrial processing applications. Expanding demand from paper, plastics, paints, coatings, water treatment, and environmental industries is further supporting segment growth. Additionally, the growing use of limestone-derived products in emission control technologies and sustainable industrial processes is expected to create significant opportunities for chemical-grade limestone producers.

Regional Insights

Asia Pacific is the largest and fastest-growing limestone market globally, driven by rapid urbanization, industrialization, and substantial investments in infrastructure development across major economies such as China, India, Japan, Indonesia, and Vietnam. The region accounts for most of the global cement production, making construction the primary driver of limestone consumption. Expanding transportation networks, smart city projects, residential developments, and industrial facilities continue to support demand for limestone-based cement and aggregates.

The China limestone market is expected to grow during the forecast period. China remains one of the largest consumers of limestone worldwide, driven by its extensive cement, construction, and steel industries. Although the pace of real estate development has moderated in recent years, ongoing investments in transportation infrastructure, renewable energy projects, and industrial modernization continue to sustain limestone demand. The country's steel sector remains a major consumer of limestone for metallurgical applications, while increasing environmental regulations are driving its use in flue gas desulfurization and wastewater treatment systems. The growing adoption of sustainable building materials is also supporting demand for limestone-based blended cement products.

North America Limestone Market Trends

The North America limestone industry is driven by strong demand from construction, infrastructure rehabilitation, steel manufacturing, and environmental applications. Government investments in transportation networks, bridges, roads, and public infrastructure continue to support aggregate and cement consumption, thereby increasing limestone demand. Additionally, limestone plays a critical role in water treatment facilities and flue gas desulfurization systems used by power plants and industrial facilities to comply with environmental regulations. The region also benefits from well-established quarrying operations and advanced mining technologies that ensure a stable supply of high-quality limestone.

U.S. Limestone Market Trends

The U.S. represents the largest market in North America, supported by extensive construction activity, robust cement production, and significant demand from the steel and chemical industries. Federal infrastructure funding programs and investments in residential and commercial construction have increased the consumption of crushed limestone aggregates. The country also utilizes limestone extensively in agricultural applications to improve soil quality and in environmental projects involving wastewater treatment and emissions control.

Europe Limestone Market Trends

The Europe limestone industry is characterized by stable demand from construction, cement manufacturing, steel production, and environmental remediation activities. Stringent environmental regulations have encouraged the adoption of limestone-based solutions for water treatment, flue gas cleaning, and industrial emission reduction. The region's focus on sustainable construction and carbon reduction initiatives has also increased the use of limestone in blended cements, which helps lower clinker content and reduce carbon emissions. Ongoing renovation and modernization of aging infrastructure across Western and Central Europe continue to support market growth.

Latin America Limestone Market Trends

The Latin America limestone industry’s growth is primarily driven by infrastructure development, residential construction, mining activities, and cement production. Countries such as Brazil, Mexico, Chile, and Colombia are witnessing increasing investments in transportation networks, urban infrastructure, and industrial facilities, which support limestone consumption. The region's agricultural sector also contributes to demand using agricultural lime for soil conditioning and productivity enhancement. Additionally, growing mining and metallurgical operations across several countries create a steady demand for limestone in mineral processing and metal extraction activities.

Middle East & Africa Limestone Market Trends

The Middle East & Africa limestone industry is supported by large-scale infrastructure projects, urban development programs, and expanding industrial sectors. In the Middle East, significant investments in smart cities, tourism infrastructure, commercial developments, and transportation projects are driving demand for cement and construction aggregates derived from limestone. Across Africa, rapid population growth, urbanization, and government-led infrastructure initiatives are increasing construction activity and cement consumption.

Key Limestone Company Insights

Some of the key players operating in the market include CARMEUSE and Lhoist.

-

CARMEUSE, established in 1860 and headquartered in Belgium, is one of the world's leading producers of limestone, lime, and mineral-based solutions serving a wide range of industrial, environmental, and construction applications. The company offers an extensive portfolio of high-calcium limestone, dolomitic limestone, quicklime, hydrated lime, and specialty mineral products used across steel manufacturing, construction, water treatment, agriculture, and environmental markets. With a vast network of quarries, processing facilities, and distribution operations across Europe, North America, Africa, and Asia, CARMEUSE has established itself as a key global supplier of high-quality limestone and lime products.

-

Lhoist, established in 1889 and headquartered in Belgium, is one of the world's largest producers of lime, dolime, and limestone-based solutions for industrial, environmental, and agricultural applications. The company provides a comprehensive portfolio of limestone, quicklime, hydrated lime, and mineral products that support industries such as steel, mining, construction, chemicals, water treatment, and environmental protection. Through its extensive reserve base, advanced processing technologies, and operations spanning multiple continents, Lhoist has positioned itself as a leading global supplier of high-performance limestone and lime products.

-

Imerys, established in 1880 and headquartered in France, is a global leader in specialty minerals and industrial mineral solutions, with a strong presence in the limestone and calcium carbonate value chain. The company offers a broad range of ground calcium carbonate (GCC), precipitated calcium carbonate (PCC), and limestone-derived mineral products serving construction, paper, plastics, paints, coatings, pharmaceuticals, and environmental applications. Supported by a global network of mineral reserves, processing plants, and research facilities, Imerys has developed a strong market position as a leading supplier of value-added limestone and mineral-based solutions worldwide.

Key Limestone Companies

The following key companies have been profiled for this study on the limestone market.

-

CARMEUSE

-

CEMEX S.A.B. de C.V.

-

Graymont Limited

-

Heidelberg Materials AG

-

Holcim Group

-

Imerys

-

Lhoist

-

Mineral Technologies Inc.

-

Mississippi Lime Company

-

National Lime & Stone Company

Competitive Benchmarking

Operating Strategies

Competitive Edge

Considerations

Mature Players: CARMEUSE; Lhoist; Holcim Group; Heidelberg Materials AG; CEMEX S.A.B. de C.V.; Imerys

- Mature participants in the limestone market typically operate large-scale, vertically integrated businesses encompassing limestone quarrying, crushing, processing, lime production, cement manufacturing, aggregates, and specialty mineral products. Their strategies focus on securing long-term limestone reserves, optimizing production efficiency, expanding downstream value-added offerings, and maintaining strong relationships with construction, steel, chemical, environmental, and industrial customers.

- These companies emphasize continuous investment in quarry development, processing technologies, sustainability initiatives, logistics infrastructure, and geographic expansion to support long-term demand across multiple end-use industries.

- These companies benefit from extensive mineral reserve ownership, diversified product portfolios, strong distribution networks, and established customer relationships across global markets. Their scale enables cost-efficient production, supply reliability, and the ability to serve large infrastructure, construction, and industrial projects.

- Strong financial resources, technical expertise, and vertically integrated operations further strengthen their competitive positioning in both commodity and specialty limestone applications.

- Mature participants face challenges associated with environmental regulations, permitting requirements, carbon emission reduction targets, and increasing sustainability expectations from customers and regulators.

- Additionally, fluctuations in construction activity, energy costs, transportation expenses, and regional economic conditions can influence profitability and long-term operational planning.

Growing / Specialized Players: Mineral Technologies Inc.; Mississippi Lime Company; National Lime & Stone Company; GCCP Resources Limited

- Specialized participants in the limestone market focus on selected high-value applications such as calcium carbonate products, industrial lime, specialty minerals, aggregates, and regional limestone supply. Their strategies emphasize product quality, application-specific solutions, operational efficiency, and targeted expansion within niche end-use sectors including paper, plastics, water treatment, agriculture, mining, and specialty industrial applications. These companies often pursue growth through technical specialization, regional market expansion, and development of value-added limestone-derived products.

- Competitive strengths include expertise in specialized limestone processing, strong regional market presence, customer-focused product development, and the ability to serve niche industrial applications requiring specific material characteristics. Their focused operating models often provide greater flexibility, faster decision-making, and stronger technical support for application-specific customer requirements.

- Compared with larger global producers, specialized players generally operate with narrower geographic reach, smaller reserve bases, and more concentrated customer exposure. Their growth may be influenced by regional construction activity, industrial demand cycles, and competitive pressures from larger integrated producers. Expanding production capacity, geographic diversification, and broadening end-use exposure remain important priorities for strengthening long-term competitiveness.

Recent Developments

-

In March 2026, Holcim completed the acquisition of a majority stake in Cementos Pacasmayo, a leading Peruvian building materials producer. The acquisition enhances Holcim’s access to limestone, cement, and aggregates markets in Peru and supports the company’s long-term growth strategy across Latin America.

-

In October 2025, Imerys signed an agreement to acquire SB Mineração, a leading Brazilian producer of ground calcium carbonate (GCC), to strengthen its industrial minerals portfolio and expand its footprint in Latin America. The acquisition enhances Imerys' position in the limestone and calcium carbonate value chain and improves its ability to serve growing demand from the polymers, paints, coatings, and construction sectors across Brazil and neighboring markets.

-

In September 2025, Carmeuse Group acquired a 97.1% controlling stake in Cementos Bío Bío (CBB), a leading Chilean producer of lime, cement, and concrete products. The acquisition expands Carmeuse's presence in South America and strengthens its exposure to the mining, construction, and industrial sectors across Chile, Peru, and Argentina. The transaction aligns with the company's strategy to increase its participation in high-growth limestone and lime markets.

Limestone Market Report Scope

Report Attribute

Details

Market definition

The market size represents the apparent consumption of limestone across various applications for a particular year.

Market size in 2025

USD 84.6 billion

Estimated market size in 2026

USD 90.5 billion

Projected market size by 2033

USD 141.3 billion

Growth Rate

CAGR of 6.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 – 2024

Forecast period

2026 - 2033

Quantitative Units

Volume in kilotons, revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Volume forecast, revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Product, end use, region

Regional Scope

North America; Europe; Asia Pacific; Central & South Africa; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK: China; Japan; India; South Korea; Indonesia; Bangladesh; Brazil

Key companies profiled

CARMEUSE; CEMEX S.A.B. de C.V.; Graymont Limited; Heidelberg Materials AG; Holcim Group; Imerys; Lhoist; Mineral Technologies Inc.; Mississippi Lime Company; National Lime & Stone Company

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Limestone Market Report Segmentation

This report forecasts revenue and volume growth at the global, regional & country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global limestone market report based on product, end use, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million/Billion, 2021 - 2033)

-

High Calcium

-

Magnesian

-

-

End Use Outlook (Volume, Kilotons; Revenue, USD Million/Billion, 2021 - 2033)

-

Building & Construction

-

Iron & Steel

-

Agriculture

-

Chemical

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million/Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Indonesia

-

South Korea

-

Bangladesh

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

South Africa

-

UAE

-

Kuwait

-

-

Research Methodology

Segment Definition

Segment – Product

Revenue capture definition

High Calcium

Includes high-calcium limestone containing predominantly calcium carbonate (typically above 95% CaCO₃), used in cement manufacturing, lime production, steelmaking, water treatment, flue gas desulfurization, construction aggregates, and chemical processing applications. Revenue is generated from the sale of quarried, crushed, ground, and processed high-calcium limestone products across industrial and construction sectors.

Magnesian

Includes magnesian and dolomitic limestone containing significant levels of magnesium carbonate, used in steel production, agriculture, construction materials, refractory applications, soil conditioning, and environmental treatment processes. Revenue is generated from the production and sale of magnesian limestone, dolomitic limestone, and related mineral products serving industrial, agricultural, and infrastructure markets.

Segment – End Use

Revenue capture definition

Building & Construction

Covers limestone consumption in cement manufacturing, concrete production, construction aggregates, road base materials, asphalt mixtures, dimension stone, and other infrastructure and building applications. Revenue is generated from limestone products supplied to residential, commercial, industrial, and civil construction projects.

Iron & Steel

Includes limestone used as a fluxing agent in blast furnaces, basic oxygen furnaces, electric arc furnaces, and other metallurgical processes to remove impurities during iron and steel production. Revenue is generated from limestone supplied to integrated steel plants, mini-mills, and metal processing facilities.

Agricultural

Covers agricultural limestone used for soil conditioning, pH correction, nutrient enhancement, livestock feed supplements, and crop productivity improvement. Revenue is generated from limestone products supplied to farms, agricultural distributors, and agribusiness operations.

Chemical

Includes limestone used in chemical manufacturing, lime production, precipitated calcium carbonate (PCC), ground calcium carbonate (GCC), glass manufacturing, paper production, plastics, paints, coatings, and other industrial chemical processes. Revenue is generated from limestone supplied as a raw material for specialty and commodity chemical applications.

Others

Covers all other limestone applications, including water and wastewater treatment, flue gas desulfurization, mining, environmental remediation, sugar refining, pharmaceuticals, and various industrial processes not included in the above categories. Revenue is generated from limestone products supplied to environmental, utility, mining, and specialty industrial sectors.

Estimation Model

Limestone Consumption Base Layer

Application Eligibility Layer

Limestone Utilization Layer

Monetisation Layer

Which industries potentially require limestone?

Which activities technically require limestone?

How much limestone is consumed?

How much revenue is generated?

Identify production volumes and activity levels across limestone-consuming industries, including construction, cement manufacturing, steel production, agriculture, chemicals, water treatment, mining, and environmental applications.

Apply industry-specific limestone intensity factors to the consumption base. This includes limestone required per ton of cement produced, limestone used as flux in steelmaking, agricultural lime application rates, and limestone demand in environmental treatment processes.

Apply region- and industry-specific utilization rates based on production technologies, operating rates, substitution levels, environmental regulations, and end-use requirements. Account for differences between high-calcium and magnesian limestone usage across applications.

Multiply limestone consumption volumes by average selling prices for crushed limestone, construction aggregates, high-calcium limestone, magnesian limestone, agricultural lime, and specialty limestone products.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

Segmentation

Detailed country- and region-level analysis covering construction activity, infrastructure investments, cement production capacity additions, steel manufacturing expansion, mining developments, urbanization trends, environmental regulations, and limestone quarrying activities across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Helps clients identify high-growth regional markets, evaluate infrastructure and industrial development trends, optimize geographic expansion strategies, and assess region-specific limestone demand across construction, steel, agriculture, and industrial applications.

Pricing Analysis

Detailed pricing assessments covering limestone quarrying costs, drilling and blasting expenses, crushing and processing costs, energy consumption, labor costs, transportation and freight charges, environmental compliance expenses, and regional pricing variations for high-calcium and magnesian limestone products.

Helps clients evaluate pricing structures, optimize procurement strategies, assess margin fluctuations, and understand the impact of energy, logistics, and operating cost changes on overall market competitiveness.

Opportunity Assessment

Strategic evaluation of emerging growth opportunities across sustainable construction materials, blended cement production, infrastructure modernization projects, steel manufacturing expansion, water and wastewater treatment facilities, flue gas desulfurization systems, agricultural soil conditioning, and specialty calcium carbonate applications.

Assists clients in identifying untapped revenue streams, evaluating future investment potential, understanding evolving end-use demand patterns, and prioritizing expansion opportunities in high-growth limestone application sectors.

Frequently Asked Questions About This Report

The key factors driving the limestone market include growth in infrastructural developments and steel production in the world.

Asia Pacific dominated the global limestone market with a revenue share of over 57.4% in 2025.

Asia Pacific is the fastest growing regional market. It is projected to register a CAGR of 7.3% over the forecast period.

China accounted for nearly 69% share of the Asia Pacific limestone market in 2025.

The high calcium limestone dominated the limestone industry, accounting for 78.8% revenue share in 2025.

The limestone market size was estimated at USD 84.6 billion in 2025 and is expected to reach USD 90.5 billion in 2026.

The limestone market is expected to grow at a compound annual growth rate of 6.6% from 2026 to 2033 to reach USD 141.3 billion by 2033.

The building & construction segment registered the largest market share of 82.7% in 2025 on account of widespread applications of limestone in the construction sectors such as cement & concrete and road base.

Some of the key players operating in the limestone market include CARMEUSE, CEMEX S.A.B. de C.V., Graymont Limited, Heidelberg Materials AG, Holcim Group, Imerys, Lhoist, Mineral Technologies Inc., Mississippi Lime Company, National Lime & Stone Company, and others.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.