- Home

- »

- Conventional Energy

- »

-

LNG Bunkering Market Size And Share Report, 2026-2033GVR Report cover

![LNG Bunkering Market (2026 - 2033)Report]()

LNG Bunkering Market (2026 - 2033)

Size, Share & Trends Analysis Report By Bunkering Type (Portable Tank, Ship-To-Ship), By Vessel Type (Ferries, Tankers, Cruise Ships, Bulk & General Cargo), By Infrastructure Type (Onshore Terminals, Small-Scale LNG Infrastructure), By Region, And Segment

Market Size, 2025

$1.8BMarket Estimate, 2026

$2.3BMarket Forecast, 2033

$12.5BCAGR, 2026–2033

26.9%LNG Bunkering Market Summary

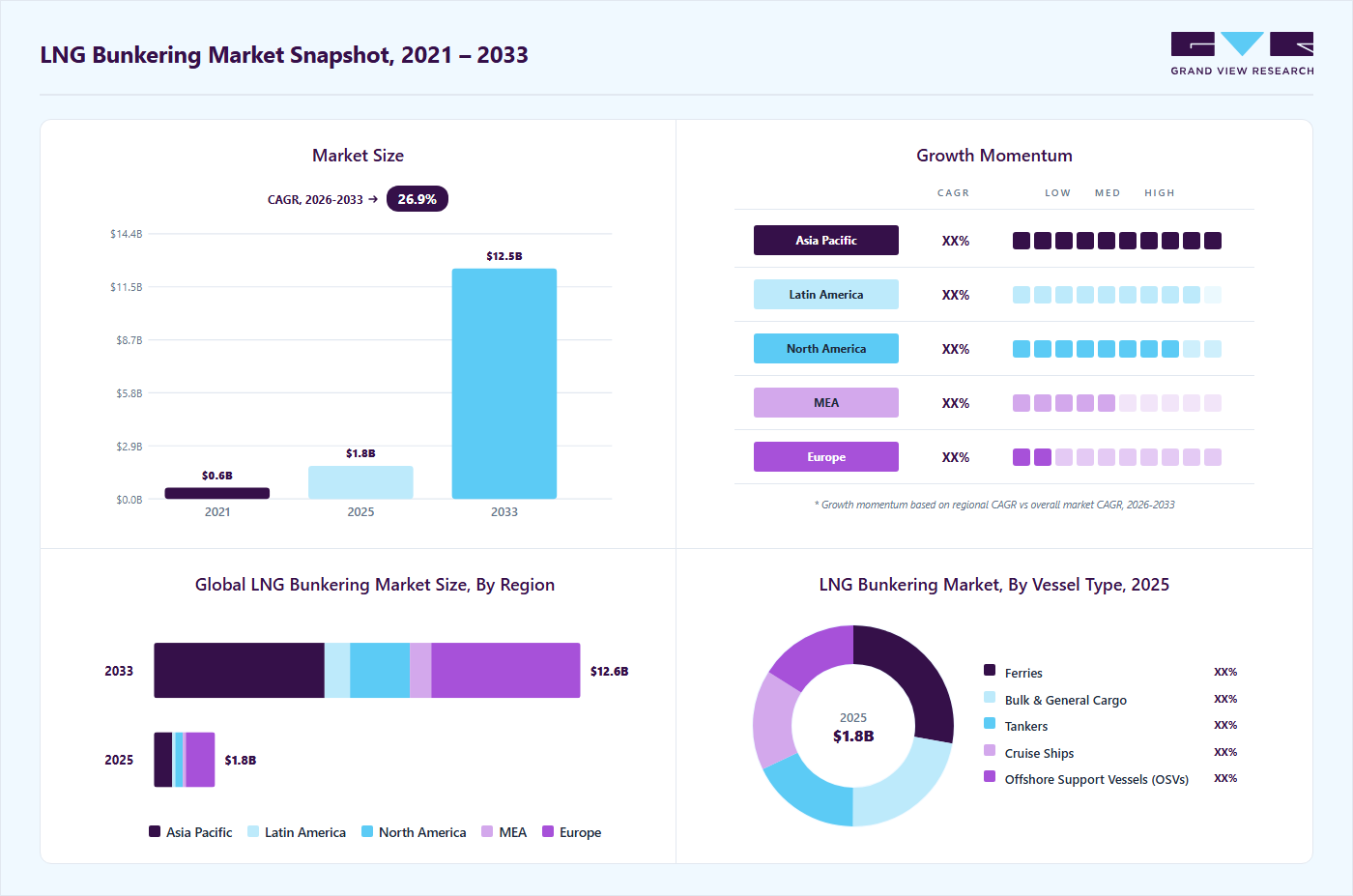

The global LNG bunkering market size was valued at USD 1.8 billion in 2025 and is projected to grow from USD 2.3 billion in 2026 to USD 12.5 billion by 2033, at a CAGR of 26.9% from 2026 to 2033. Europe held the largest revenue share of 48.0% of the global market in 2025. The market is witnessing strong growth as shipping companies, port authorities, and energy providers increasingly shift toward cleaner marine fuels to comply with stringent environmental regulations.

Key Market Trends & Insights

- By bunkering type: Ship-to-ship (STS) segment held the largest market share of 52.0% in 2025.

- By vessel type: Ferries segment held the largest market share of 28.0% in 2025.

- By infrastructure type: Onshore terminals segment held the largest market share of 58.0% in 2025.

Regional Highlights

- Largest regional market: Europe (48.0% market share, 2025)

- Fastest-growing regional market: Asia Pacific (31.6% CAGR, 2026–2033)

- By Country: The Netherlands held the largest share of Europe in 2025.

Market Size & Forecast

- Market size in 2025: USD 1.8 Billion

- Estimated market size in 2026: USD 2.3 Billion

- Projected market size by 2033: USD 12.5 Billion

- CAGR (2026–2033): 26.9%

Continuous investments in bunkering infrastructure, including Ship-to-Ship (STS) and Truck-to-Ship (TTS) operations, along with advancements in LNG storage, transfer, and handling technologies, are supporting the transition from conventional marine fuels to more efficient and lower-emission energy solutions.

The LNG bunkering industry is experiencing robust growth, driven by the growing need for cleaner, more compliant marine fuel solutions amid evolving environmental regulations. The rising pressure to reduce sulfur emissions and greenhouse gases, coupled with stricter norms set by the International Maritime Organization, is accelerating the adoption of LNG as a viable alternative to conventional marine fuels. In addition, the expansion of LNG bunkering infrastructure, including Ship-to-Ship (STS), Truck-to-Ship (TTS), and terminal-based operations, is enabling ports and shipping companies to enhance fuel availability and improve operational efficiency.

")

Furthermore, the rapid transition toward low-emission fuels in the maritime sector, including container shipping, cruise, and tanker segments, is significantly influencing market expansion. LNG bunkering plays a critical role in ensuring a reliable fuel supply for LNG-powered vessels while supporting compliance with global emission standards. Technological advancements, particularly in cryogenic storage, transfer systems, and bunkering vessel design, are improving operational safety, flexibility, and scalability. Simultaneously, ongoing investments in port infrastructure, along with increasing focus on sustainability and energy efficiency, are reinforcing the strategic importance of LNG bunkering in enabling a cleaner, more resilient, and future-ready maritime energy ecosystem.

Drivers, Opportunities & Restraints

The primary driver of the LNG bunkering market is the growing need to adopt cleaner marine fuel alternatives in response to stringent environmental regulations across the shipping industry. Government policies and international mandates introduced by the International Maritime Organization, including sulfur emission limits and greenhouse gas reduction targets, are accelerating the transition away from heavy fuel oil toward LNG-based solutions. LNG is increasingly recognized as a viable bridge fuel due to its ability to significantly reduce sulfur oxides (SOx), nitrogen oxides (NOx), and overall carbon emissions. In addition to regulatory compliance, the economic viability of LNG is further supporting its adoption, as it offers improved fuel efficiency and lower long-term operational costs compared to conventional marine fuels.

A significant opportunity lies in the expanding adoption of LNG as a cleaner marine fuel across key vessel segments within the LNG bunkering ecosystem. The increasing deployment of LNG-powered container fleets, which currently represent a dominant segment, is driving the need for predictable and high-volume bunkering solutions at major global ports to support strict operational schedules and route optimization. This growing demand is encouraging investments in advanced bunkering infrastructure, particularly Ship-to-Ship (STS) and terminal-based systems, to ensure efficient and reliable fuel supply. Furthermore, tanker fleets are increasingly adopting LNG for long-haul operations due to its higher energy efficiency and cost advantages compared to conventional marine fuels. This shift is contributing to sustained demand for LNG bunkering across strategic maritime routes and trading hubs.

However, the market faces challenges related to the emergence of competitive alternative fuels and technologies. The growing adoption of alternatives such as hydrogen and biofuels, along with conventional compliance solutions like exhaust gas cleaning systems (scrubbers), is affecting the overall growth potential of LNG bunkering. The reason for this challenge lies in the evolving decarbonization landscape, where shipping companies are evaluating multiple fuel pathways to meet long-term emission-reduction targets and regulatory requirements. The presence of these alternatives also creates uncertainty in fuel investment decisions, as operators may opt for solutions that offer lower lifecycle emissions or greater future scalability.

The LNG bunkering industry faces several infrastructure-related restraints that may hamper its growth trajectory. LNG bunkering facilities are unevenly distributed, with most concentrated in major maritime hubs, limiting accessibility for vessels operating in secondary ports and on regional routes. This lack of widespread availability forces shipping operators, particularly smaller fleets, to detour from optimal routes or carry additional fuel reserves, thereby increasing operational costs and reducing overall efficiency.

Bunkering Type Insights

The ship-to-ship (STS) segment accounted for the largest market share of 52.0% in 2025, driven by the flexibility of supply methods, particularly those that reduce dependence on permanent onshore infrastructure and enable fuel delivery across a wider range of ports and locations. This flexibility allows shipping operators to access LNG bunkering services without requiring fully developed terminal facilities, supporting operations in both established hubs and emerging maritime routes. These systems are especially valuable in scenarios where fixed infrastructure is limited, enabling efficient and adaptable fuel supply to LNG-powered vessels. Additionally, LNG bunkering operations require specialized equipment, including cryogenic hoses and advanced safety systems, due to the extremely low temperatures involved.

The ship-to-ship segment is expected to grow at the fastest CAGR of 29.2% over the forecast period, driven by its widespread adoption across large-scale marine and shipping operations. STS bunkering is gaining significant traction as the maritime industry increasingly shifts toward low-emission fuels to comply with stringent environmental regulations. Its ability to deliver high-volume LNG fuel efficiently to a wide range of vessels, including container ships, tankers, and cruise liners, makes it particularly well-suited for major ports and high-traffic shipping routes.

Infrastructure Type Insights

The onshore terminals segment dominated the LNG bunkering industry, accounting for the largest revenue share of 58.0% in 2025, driven by the increasing development of integrated infrastructure solutions that support both large-scale LNG imports and small-scale marine fuel distribution. Onshore terminals are evolving into multi-functional hubs, with operators modifying jetties and storage facilities to accommodate LNG bunkering operations alongside traditional regasification activities. This infrastructure synergy enables more efficient utilization of existing assets while expanding LNG availability for marine applications. The segment is particularly prominent in regions with established LNG import terminals, where port infrastructure can be leveraged to support growing bunkering demand.

The small-scale LNG infrastructure segment is projected to grow at the fastest CAGR of 29.7% over the forecast period, driven by its growing role in supporting LNG bunkering in diverse and infrastructure-limited environments. The increasing deployment of dual-fuel vessels in ports lacking large-scale LNG facilities is accelerating the demand for flexible and decentralized bunkering solutions. Its ability to enable efficient fuel supply in smaller ports and coastal regions makes it particularly well-suited for expanding LNG adoption beyond major maritime hubs. Additionally, small-scale LNG infrastructure plays a critical role in meeting the energy needs of remote and off-grid areas, providing a cleaner, more reliable alternative for power generation in energy-interrupted regions.

Vessel Type Insights

The ferries segment dominated the LNG bunkering industry, accounting for the largest revenue share of 28.0% in 2025, driven by the increasing adoption of LNG as a marine fuel across ferry operations, particularly in Europe and Asia Pacific, where decarbonization targets are accelerating the shift toward cleaner energy solutions. Ferries represent a key segment of the market, supported by strong regulatory frameworks, government incentives, and the need for reliable, low-emission fuel alternatives for short-distance and coastal routes. Their predictable operating patterns and frequent refueling requirements make them well-suited for LNG adoption.

The tankers segment is projected to register the fastest CAGR of 30.2% over the forecast period, supported by the increasing adoption of LNG as a marine fuel and the growing transition toward dual-fuel vessel technologies. The number of LNG-powered ships is expected to grow significantly, with tankers and container vessels leading the way as operators prioritize fuel efficiency and compliance with emissions regulations. LNG bunkering plays a critical role in supporting these vessels by providing a reliable, scalable fuel supply across major shipping routes.

Regional Insights

Europe dominated the LNG bunkering market, accounting for approximately 48.0% of the global revenue share in 2025, driven by ambitious climate targets and strong regulatory support for cleaner marine fuel adoption. Stringent emission norms established by the International Maritime Organization, along with regional decarbonization policies, are accelerating the transition away from conventional fuels toward LNG across the maritime sector. Countries across the region are actively expanding LNG use in shipping, supported by well-established port infrastructure, extensive bunkering networks, and favorable government initiatives to reduce greenhouse gas emissions and enhance energy security. Continuous investments in LNG bunkering vessels, terminal upgrades, and integrated fuel supply systems further reinforce the growth of the market in Europe. The presence of mature maritime trade routes and high vessel traffic is enabling consistent demand for LNG as a cleaner alternative fuel. Additionally, strong policy alignment, technological advancements, and a well-developed infrastructure ecosystem are positioning Europe as the leading and most advanced global market.

Netherlands LNG Bunkering Market Trends

The Netherlands LNG bunkering market holds the largest share of Europe, driven by strong regulatory support aligned with International Maritime Organization and European Union decarbonization targets, as well as a well-established maritime infrastructure. The country has positioned itself as a central LNG bunkering hub due to its strategic geographic location and advanced port ecosystem. The presence of major ports, such as the Port of Rotterdam, the largest port in Europe, is critical to supporting LNG bunkering activities, with consistently rising bunkering volumes and a growing number of LNG-powered vessels. Continuous investments in bunker barges, storage facilities, and terminal expansions are further strengthening supply capabilities and operational efficiency. Additionally, the Netherlands is actively expanding its small-scale LNG infrastructure and fostering collaborations across the maritime value chain to accelerate the adoption of cleaner marine fuels.

Asia Pacific LNG Bunkering Market Trends

Asia Pacific is expected to grow at the fastest CAGR of 31.6% from 2026 to 2033, primarily driven by stringent maritime emissions regulations from the International Maritime Organization, the rapid expansion of LNG-fueled vessel fleets, and significant infrastructure investments across major maritime hubs. The growing shift toward cleaner marine fuels, driven by regulatory requirements and sustainability goals, is accelerating the adoption of LNG bunkering across key shipping routes and port ecosystems in the region. Additionally, continuous investments in port infrastructure, bunkering vessels, and storage facilities are enhancing fuel accessibility and operational efficiency, positioning the Asia Pacific as a leading and rapidly evolving market for LNG bunkering solutions.

The growth of the regional market is further supported by the rising demand for cleaner energy alternatives and the ongoing transition toward low-emission maritime operations. However, market expansion faces challenges from geopolitical uncertainties, fluctuations in LNG prices, and increasing competition from alternative fuels such as hydrogen and biofuels. Despite these constraints, sustained investments in LNG infrastructure and the growing adoption of LNG-powered vessels continue to strengthen the region’s role as a key hub for LNG bunkering development.

North America LNG Bunkering Market Trends

The North America region is witnessing steady growth in the LNG bunkering industry, driven by the operational cost advantages associated with LNG-powered vessels. Despite higher initial costs associated with vessel retrofitting or new builds, LNG offers lower long-term fuel and maintenance costs than conventional marine fuels or scrubber-based compliance systems. This economic benefit, along with increasing focus on emission reduction and energy efficiency, is reinforcing the adoption of LNG bunkering and strengthening North America’s position as a steadily expanding market.

Latin America LNG Bunkering Market Trends

Latin America is expected to witness steady growth over the forecast period, driven by increasing investments in port infrastructure and the rising need for cleaner marine fuel alternatives. The region is witnessing a gradual transition toward LNG adoption across shipping operations, supported by efforts to upgrade existing port facilities to accommodate bunkering methods such as Ship-to-Ship (STS) and Truck-to-Ship (TTS). This shift is enabling greater fuel accessibility and supporting the development of flexible bunkering networks across key maritime locations. Increasing focus on modernizing port ecosystems, along with the adoption of scalable and cost-effective bunkering solutions, is strengthening LNG deployment across regional shipping routes.

Middle East & Africa LNG Bunkering Market Trends

The Middle East & Africa (MEA) LNG bunkering industry is expanding rapidly, driven by its strategic location along major global shipping routes, including the Suez Canal and the Strait of Hormuz. The growing need for cleaner marine fuel alternatives, driven by stringent environmental mandates and pressure to reduce emissions, is accelerating the adoption of LNG bunkering across the region. Governments and port authorities are investing heavily in upgrading infrastructure in key hubs such as the United Arab Emirates and Oman to support efficient LNG supply and distribution for maritime operations.

Key LNG Bunkering Company Insights

Some of the key participants in the global LNG bunkering market include Shell plc, TotalEnergies SE, Gasum Oy, ENGIE SA, Gazprom Neft, Titan LNG, Peninsula Petroleum, Nauticor GmbH, FueLNG Pte Ltd, and Harvey Gulf International Marine. These companies collectively hold the largest market share and play a critical role in shaping industry trends and competitive dynamics. They are increasingly focusing on the adoption of cleaner marine fuels, including bio-LNG, and implementing methane emission reduction strategies to align with the stringent standards set by the International Maritime Organization. Additionally, significant investments are being directed toward expanding bunkering infrastructure, particularly Ship-to-Ship (STS) and Truck-to-Ship (TTS) capabilities, to enhance fuel accessibility, improve operational flexibility, and support supply across both major hubs and remote ports.

Their operations typically encompass the development and deployment of integrated LNG bunkering solutions, including fuel supply logistics, storage systems, and advanced transfer technologies to ensure safe and efficient marine fuel delivery. Industry leaders are increasingly emphasizing the use of advanced cryogenic storage systems and digital monitoring platforms to optimize fuel handling, maintain quality, and improve operational efficiency. The integration of technologies such as real-time monitoring, predictive maintenance, and automated control systems is enabling enhanced asset performance, reduced downtime, and improved supply chain coordination across bunkering operations.

As global demand for low-emission marine fuels intensifies and decarbonization targets become more stringent, companies operating in the LNG bunkering industry are prioritizing infrastructure expansion, supply chain integration, and geographic diversification. Strategic collaborations among fuel suppliers, shipping companies such as CMA CGM, and port authorities are becoming increasingly common to build resilient, efficient bunkering networks. Furthermore, evolving maritime energy dynamics, including the transition toward cleaner fuels and flexible fuel distribution models, are reshaping the competitive landscape. Continuous advancements in bunkering technologies, storage systems, and LNG logistics are expected to enhance market competitiveness and support the sustained market growth.

Key LNG Bunkering Companies:

The following key companies have been profiled for this study on the LNG bunkering market.

- Shell plc

- TotalEnergies SE

- Gasum Oy

- ENGIE SA

- Gazprom Neft

- Titan LNG

- Peninsula Petroleum

- Nauticor GmbH

- FueLNG Pte Ltd

- Harvey Gulf International Marine

Recent Developments

-

In July 2025, TotalEnergies SE and CMA CGM launched a logistics joint venture to develop LNG bunkering infrastructure in Rotterdam, including plans to deploy an LNG bunkering vessel by 2028. This initiative aligns with the company’s strategy to expand its presence in key maritime hubs, strengthen integrated fuel supply capabilities, and support the growing demand for cleaner marine fuels.

-

In April 2026, NYK Line acquired a 50% stake in Avenir LNG from Stolt-Nielsen, enhancing its position in the LNG bunkering value chain. This move reflects the company’s focus on expanding bunkering opportunities, strengthening access to fuel supplies, and supporting the growing adoption of LNG-powered vessels across global shipping routes.

LNG Bunkering Report Scope

Report Attribute

Details

Market Definition

The LNG bunkering market refers to the global revenue generated from the supply, storage, and fueling of liquefied natural gas (LNG) as a marine fuel for various vessel types, supported by the development and operation of bunkering infrastructure such as terminals, bunker vessels, and related logistics across ports and shipping routes.

Market size value in 2025

USD 1.8 billion

Estimated Market size in 2026

USD 2.3 billion

Projected Market size by 2033

USD 12.5 billion

Growth rate

CAGR of 26.9% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Bunkering type, vessel type, infrastructure type, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Australia; Japan; South Korea; Brazil; UAE

Key companies profiled

Shell plc; TotalEnergies SE; Gasum Oy; ENGIE SA; Gazprom Neft; Titan LNG; Peninsula Petroleum; Nauticor GmbH; FueLNG Pte Ltd; Harvey Gulf International Marine

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global LNG Bunkering Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global LNG bunkering market report based on bunkering type, vessel type, infrastructure type, and region:

-

Bunkering Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Ship-To-Ship (STS)

-

Truck-To-Ship (TTS)

-

Port-To-Ship (PTS)

-

Portable Tank

-

-

Vessel Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Ferries

-

Bulk & General Cargo

-

Tankers

-

Cruise Ships

-

Offshore Support Vessels (OSVs)

-

-

Infrastructure Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Onshore Terminals

-

Floating Storage Units (FSU/FSRU-based)

-

Small-Scale LNG Infrastructure

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Australia

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global LNG bunkering market was estimated at USD 1.8 billion in 2025 and is expected to reach USD 2.3 billion in 2026.

The global LNG bunkering market is expected to grow at a compound annual growth rate of 26.9% from 2026 to 2033 to reach USD 12.5 billion by 2033.

The ship-to-ship (STS) segment held the largest market share of 52.0% in 2025, and it is also projected to grow at the fastest CAGR of 29.2%.

Some of the key participants in the global LNG bunkering market include Shell plc, TotalEnergies SE, Gasum Oy, ENGIE SA, Gazprom Neft, Titan LNG, Peninsula Petroleum, Nauticor GmbH, FueLNG Pte Ltd, Harvey Gulf International Marine, among others.

The key factors driving the growth of the global LNG bunkering market include the increasing demand for cleaner marine fuel alternatives driven by stringent environmental regulations and decarbonization targets across the shipping industry. The implementation of emission norms by the International Maritime Organization is accelerating the shift from conventional fuels such as heavy fuel oil toward LNG-based solutions..

The ferries segment dominated with a revenue share of 28.0% in 2025, while the tankers segment is projected to grow fastest.

The onshore terminals segment held the largest market share of 58.0% in 2025, while the small-scale LNG infrastructure segment is projected to grow at the fastest CAGR of 29.7%.

Europe dominated the global market with approximately 48.0% of the revenue share in 2025.

Asia Pacific is expected to grow at the fastest CAGR of 31.6% from 2026 to 2033.

About the Author(s)

Conventional Energy Research Team

Energy & Power · Conventional EnergyThis report was authored by the conventional energy research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the conventional energy segment of the energy & power industry. All findings are based on proprietary energy & power databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.