- Home

- »

- Plastics, Polymers & Resins

- »

-

Molded Pulp Packaging Market Size Report, 2026-2033GVR Report cover

![Molded Pulp Packaging Market (2026 - 2033)Report]()

Molded Pulp Packaging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Source (Wood Pulp, Non-Wood Pulp), By Molded Type (Thermoformed, Transfer), By Product, By Application, By Region, And Segment Forecasts

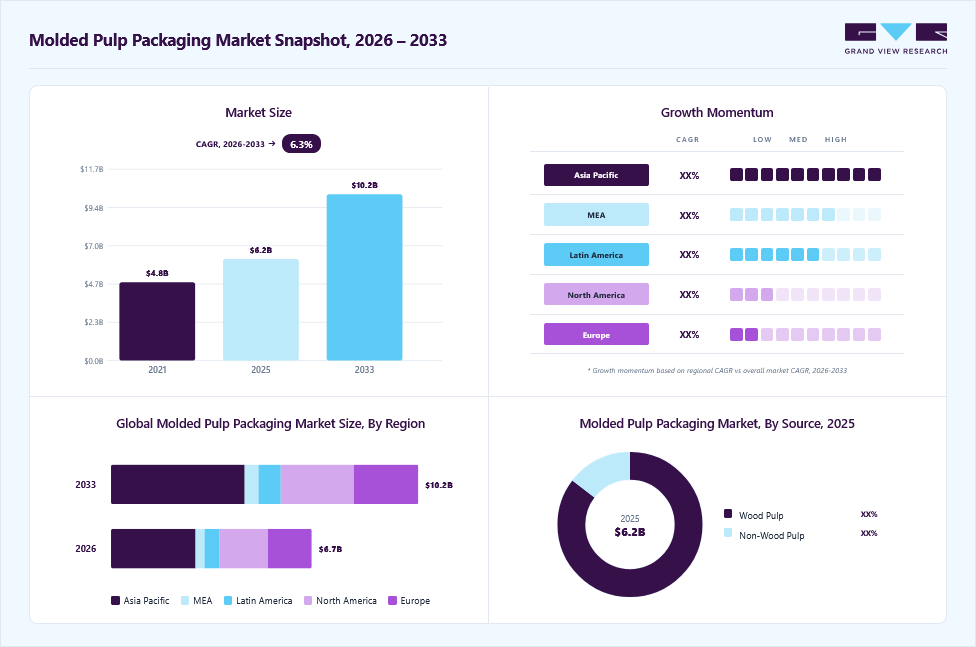

Market Size, 2025

$6.2BMarket Estimate, 2026

$6.7BMarket Forecast, 2033

$10.2BCAGR, 2026–2033

6.3%Molded Pulp Packaging Market Summary

The global molded pulp packaging market size was valued at USD 6.2 billion in 2025 and is projected to grow from USD 6.7 billion in 2026 to USD 10.2 billion by 2033, at a CAGR of 6.3% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 41.0% in 2025. The industry is driven by the global transition toward sustainable and plastic-free packaging, supported by regulatory restrictions on single-use plastics and strong consumer demand for eco-friendly materials.

Key Market Trends & Insights

- By source: Wood pulp segment accounted for over 85.0% of the revenue share in the year 2025.

- By molded type: Transfer molded segment type held the largest market share of over 56.0% in 2025.

- By product: Tray segment dominated the market with over 41.0% revenue share in 2025.

- By application: Food packaging emerged as a dominating segment with a market share of over 44.0% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (41.0% revenue share, 2025)

- By country: The China held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 6.2 Billion

- Estimated market size in 2026: USD 6.7 Billion

- Projected market size by 2033: USD 10.2 Billion

- CAGR (2026-2033): 6.3%

Additionally, rapid growth in e-commerce, food delivery, and protective packaging for electronics and FMCG products is increasing the adoption of molded pulp due to its durability, biodegradability, and cost-efficiency. Strong retail demand underpins volume growth for molded pulp packaging because brick-and-mortar assortments continue to require sustainable primary and secondary packaging at scale. Supermarket private-label lines and quick-service food programs are increasingly specifying molded pulp trays and clamshells to meet retailer ESG scorecards and plastic-reduction mandates, which creates predictable, high-volume tenders that justify CAPEX on automated molding lines. For converters, this dynamic translates into longer contract tenors, higher minimum order volumes and better amortization of tooling costs, while also shifting commercial conversations from price-only to total-life-cycle cost and verified sustainability. Regional procurement differences, such as stringent recyclability rules in Europe versus cost sensitivity in APAC, mean manufacturers must offer SKU portfolios that balance certified wood pulp and lower-cost non-wood blends to win retailer listings.")

The expanding e-commerce channel is intensifying demand for molded-fiber dunnage and protective inserts because online fulfillment prioritizes damage reduction and sustainable outbound packaging. E-tailers and 3PLs increasingly replace EPS and plastic void-fill with engineered pulp cushions that pass ISTA transit tests while reducing post-consumer waste, making molded fiber the preferred option for higher-value consumer electronics and delicate goods. This channel also increases SKU complexity and shorter lead times, pushing converters toward distributed manufacturing and vendor-financed tooling to be commercially competitive for national e-commerce programs. As a result, companies that can offer standardized, high-precision protective inserts with proven drop-performance capture higher-margin, repeatable business from marketplaces and OEMs.

Logistics and omnichannel retail trends amplify molded fiber demand by incentivizing nearshoring and regional inventory models to reduce lead times and freight emissions. Retailers prefer local or regional converters to avoid extended transit exposure and to meet sustainability procurement metrics tied to scope-3 emissions, which drives capacity investments in APAC and LATAM regional hubs. Channel consolidation, where distributors offer integrated inventory and digital ordering, favors converters that support EDI/VMI and provide product passports (PCR%, CO₂e) at the SKU level. For manufacturers, the commercial opportunity lies in coupling regional capacity with digital sales enablement and service-level guarantees to win multi-channel retail programs that span online, offline and foodservice fulfilment.

Industry Concentration & Characteristics

The industry is fundamentally driven by the global transition toward sustainable and plastic-free packaging. Stringent environmental regulations, corporate ESG goals, and rising consumer preference for biodegradable packaging are accelerating the adoption of molded fiber solutions across foodservice, e-commerce, electronics, and FMCG sectors. Its compostable and recyclable nature positions molded pulp as a strategic replacement for petroleum-based plastics and foams.

The industry is closely dependent on continuous access to wastepaper, bagasse, bamboo fiber, and agricultural residues. Regions rich in fiber resources, such as Asia Pacific, have a cost advantage through lower raw material and production sourcing. However, price volatility in recycled paper pulp and supply chain fluctuations influence production economics and global cost competitiveness.

Source Insights

The wood pulp segment accounted for over 85.0% of the revenue share in the year 2025. This is owing to its abundant availability, cost-effectiveness, and customizable to have different depths, sizes, and shapes to fit various food items, which also makes it a popular choice for packaging manufacturers. Wood pulp molded packaging has a wide application in various end-use industries. For instance, it is widely used in the food & beverage industry as it offers excellent protection for food products during shipping and storage.

The non-wood pulp segment is anticipated to record the highest growth rate of 7.5% during the forecast period. The growth of the non-wood pulp segment is owing to the growing concern about deforestation. This pulp is produced with non-wood cellulosic plant material or agricultural waste such as cereal straws, grasses, sugarcane, and others. This is gaining popularity in the production of pulp due to its high availability, lower cost, and growing concerns about deforestation.

Molded Type Insights

The transfer molded segment type held the largest market share of over 56.0% in 2025. Transfer molded pulp has a wide application in the food packaging industry due to the hygroscopic property of the material and air permeability, which results in the longer shelf life of beverages and food products that are to be further shipped. Moreover, molded pulp packaging protects from shocks that cause breakage or damage to the products, especially fruits, vegetables & eggs, and non-alcoholic, and alcoholic beverages.

The thermoformed segment is anticipated to grow at the fastest CAGR of 7.4% over the forecast period. This is attributed to the rising concerns about the environmental impact of single-use plastics, which resulted in a shifting trend of consumers from plastic thermoformed packaging to sustainable molded thermoformed pulp packaging.

Product Insights

The tray segment dominated the market with over 41.0% revenue share in 2025, owing to the wide application of these trays in food packaging and food service industries. These trays are molded pulp trays that are widely used for packaging of eggs in retail distribution channels, as they provide protection from breakage and keep the product safe.

Molded pulp clamshells are projected to grow at a fast CAGR of 7.2% over the forecast period. Eggs are either packed in plastic clamshells or in molded pulp clamshells. The demand for plastic clamshells has been declining for the past few years owing to the increasing demand for molded pulp clamshells. This can be attributed to the convenience, in terms of carrying and disposing of, offered by molded pulp clamshells.

Application Insights

Food packaging emerged as a dominating application for the molded pulp packaging application segment with a market share of over 44.0% in 2025. Molded pulp packaging is mainly used for the packaging of fruits, vegetables, and eggs. Clamshells and trays are considered the primary packaging types for eggs due to the low price and cushioning offered. In addition, molded pulp trays and clamshells offer the extended shelf life of the eggs, keeping them fresh through the ventilation provided in this packaging.

The electronics application is expected to witness a CAGR of 7.5% over the forecast period, owing to high demand from the packaging of sensitive electronic devices such as laptops, smartphones, and others. The electronics require molded pulp packaging to transport and store delicate electronic devices that keep them safe from any external damage, which is anticipated to drive the demand for molded pulp packaging products.

Regional Insights

North America molded pulp packaging market is growing primarily due to strong sustainability regulations and rising consumer preference for eco-friendly packaging alternatives. Governments in the U.S. and Canada have implemented stringent policies aimed at reducing single-use plastics and promoting circular economy practices. For instance, several U.S. states, such as California, New York, and Washington, have banned expanded polystyrene (EPS) foam packaging, prompting food service and consumer goods companies to adopt molded fiber solutions. In Canada, the federal government’s Single-Use Plastics Prohibition Regulations, introduced under the Zero Plastic Waste Agenda, further encourage businesses to replace plastic packaging with compostable or recyclable fiber-based alternatives. These policies are creating a favorable environment for molded pulp packaging producers such as Huhtamaki North America, Sabert Corporation, and Pactiv Evergreen, who are expanding production capacity and product lines in response to regional demand.

U.S. Molded Pulp Packaging Market Trends

The foodservice industry plays a central role in driving U.S. demand for molded pulp packaging. Major quick-service and casual dining chains, such as McDonald’s, Starbucks, Panera Bread, and Sweetgreen, are replacing plastic and foam containers with molded pulp alternatives to meet corporate sustainability goals and consumer expectations. The surge in online food delivery services and meal-kit platforms, including Uber Eats, DoorDash, and HelloFresh, has also increased demand for lightweight, stackable, and compostable packaging. In addition, molded fiber versatility, ranging from egg cartons and fruit trays to high-end food bowls and cup carriers, makes it an attractive solution for brands seeking both functionality and sustainability.

Asia Pacific Molded Pulp Packaging Market Trends

The molded pulp packaging market in Asia Pacific held the largest market share of over 41.0% in 2025 and is witnessing strong growth as it is expected to grow at the fastest CAGR of 6.8% during the forecast period. This dominance is due to exponential growth in sustainable packaging demand across fast-moving consumer goods (FMCG), foodservice disposables, and electronics. Countries in the region, especially China, India, Japan, and Southeast Asia, are heavily shifting toward biodegradable packaging due to government bans on single-use plastics and rising sustainability expectations from both consumers and brands. Large-scale manufacturing capabilities, low production costs, and an abundance of agricultural residues suitable for molding (bagasse, bamboo fiber, wheat straw) make Asia Pacific the most cost-competitive and resource-rich hub for molded pulp production.

In addition, China supplies molded pulp packaging on a global scale for electronics giants, toy manufacturers, small appliance OEMs, and lifestyle brands due to its deep automation capabilities and competitive pricing. The shift of global electronics packaging suppliers toward fiber-based cushioning materials has created a multiplier effect, leading to accelerating investments by Chinese molders into precision tooling and transfer molding technologies. Strong government initiatives to expand biodegradable alternatives make China the most influential contributor to global market growth.

Europe Molded Pulp Packaging Market Trends

Europe’s well-established industrial infrastructure and technological capabilities support large-scale production and innovation in molded pulp packaging. The presence of advanced machinery, automated production lines, and R&D centers enables manufacturers to produce high-quality molded fiber products efficiently and at competitive costs. Collaborative initiatives, such as Stora Enso’s partnerships with foodservice chains to develop sustainable packaging solutions, highlight how Europe leverages both policy support and technological advancement to dominate the market. This combination of regulatory backing, consumer preference, and industrial sophistication makes Europe a key driver in the global molded pulp packaging.

Key Molded Pulp Packaging Company Insights

Key players operating in the molded pulp packaging market are undertaking various initiatives to strengthen their presence and increase the reach of their products and services. Strategies such as expansion activities and partnerships are key in propelling the market growth.

Key Molded Pulp Packaging Companies:

The following are the leading companies in the molded pulp packaging market. These companies collectively hold the largest market share and dictate industry trends.

- Amcor plc

- Huhtamaki

- Hartmann Packaging A/S

- CKF Inc.

- Stora Enso

- PulPac

- Genpak

- ProAmpac

- Otarapack

- Mayr-Melnhof Karton AG

- Pro-Care Packaging

- Pactiv Evergreen Inc.

- Sabert Corporation

- Henry Molded Products Inc.

- Wynalda Packaging

- Dart Container Corporation

- Jiangyin Pton Molded Fiber Products Co., Ltd

- Fuzhou QiQi Paper Products Co., Ltd.

Recent Developments

-

In June 2025, Stora Enso and Matrix Pack entered a strategic partnership to accelerate the development of sustainable formed fiber packaging. This collaboration combines Stora Enso's leadership in renewable materials with Matrix Pack's global manufacturing expertise. The partnership aims to scale up fiber-based solutions to replace conventional plastics, enhancing circularity in packaging.

-

In June 2025, ProAmpac partnered with Western Michigan University to advance its “Fiberization of Packaging” strategy, developing curbside recyclable and compostable fiber-based packaging. WMU agreed to support material innovation, helping ProAmpac meet growing sustainable packaging demand and comply with EPR regulations.

-

In June 2025, PulPac secured a EUR 20.0 million loan from the European Investment Bank to advance its Dry Molded Fiber technology. The funding will drive R&D efforts to enhance product performance and expand sustainable packaging solutions. This move aims to accelerate the shift from plastic to fiber-based packaging across industries.

Molded Pulp Packaging Market Report Scope

Report Attribute

Details

Market size in 2026

USD 6.2 billion

Estimated market size in 2026

USD 6.7 billion

Projected market size by 2033

USD 10.2 billion

Growth rate

CAGR of 6.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Source, molded type, product, application, region

Regional Scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; China; India; Japan; Brazil; Saudi Arabia

Key companies profiled

Amcor plc; Huhtamaki; Hartmann Packaging A/S; CKF Inc.; Stora Enso; PulPac; Genpak; ProAmpac; Otarapack; Mayr-Melnhof Karton AG; Pro-Care Packaging; Pactiv Evergreen Inc.; Sabert Corporation; Henry Molded Products Inc.; Wynalda Packaging; Dart Container Corporation; Jiangyin Pton Molded Fiber Products Co., Ltd; Fuzhou QiQi Paper Products Co., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail of customized purchase options to meet your exact research needs. Explore purchase options

Global Molded Pulp Packaging Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global molded pulp packaging market report on the basis of source, molded type, product, application, and region:

-

Source Outlook (Revenue, USD Million, 2021 - 2033)

-

Wood Pulp

-

Non-wood Pulp

-

-

Molded Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Thick Wall

-

Transfer

-

Thermoformed

-

Processed

-

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Trays

-

End Caps

-

Bowls & Cups

-

Clamshells

-

Plates

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Food Packaging

-

Food Service

-

Electronics

-

Healthcare

-

Industrial

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

-

Frequently Asked Questions About This Report

The key players in the molded pulp packaging market include Amcor plc; Huhtamaki; Hartmann Packaging A/S; CKF Inc.; Stora Enso; PulPac; Genpak; ProAmpac; Otarapack; Mayr-Melnhof Karton AG; Pro-Care Packaging; Pactiv Evergreen Inc.; Sabert Corporation; Henry Molded Products Inc.; Wynalda Packaging; Dart Container Corporation; Jiangyin Pton Molded Fiber Products Co., Ltd; and Fuzhou QiQi Paper Products Co., Ltd.

The molded pulp packaging market is driven by the global transition toward sustainable and plastic-free packaging, supported by regulatory restrictions on single-use plastics and strong consumer demand for eco-friendly materials.

The wood pulp segment led with a 85.0% revenue share in 2025.

Transfer molded held the largest revenue share 56.0% in 2025, while thermoformed is the fastest-growing area.

The tray segment held the largest share (over 42.3%) in 2025 and molded pulp clamshells is the fastest-growing market.

The global molded pulp packaging market was estimated at around USD 6.2 billion in the year 2025 and is expected to reach around USD 6.7 billion in 2026.

The global molded pulp packaging market is expected to grow at a compound annual growth rate of 6.3% from 2026 to 2033 to reach around USD 10.2 billion by 2033.

Food packaging emerged as the dominating application segment for molded pulp packaging due to the rapid shift toward biodegradable, plastic-free packaging across fresh produce, ready-to-eat meals, bakery products, and foodservice disposables.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.