- Home

- »

- Conventional Energy

- »

-

Oil Refining Market Size, Share & Trends Report, 2026-2033GVR Report cover

![Oil Refining Market (2026 - 2033)Report]()

Oil Refining Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Fuel Oil, Light Distillates, Middle Distillates), By Fuel Type (Gasoline, Kerosene, Liquefied Petroleum Gas, Gasoil), By Complexity Type, By End-use, By Region, And Segment Forecasts

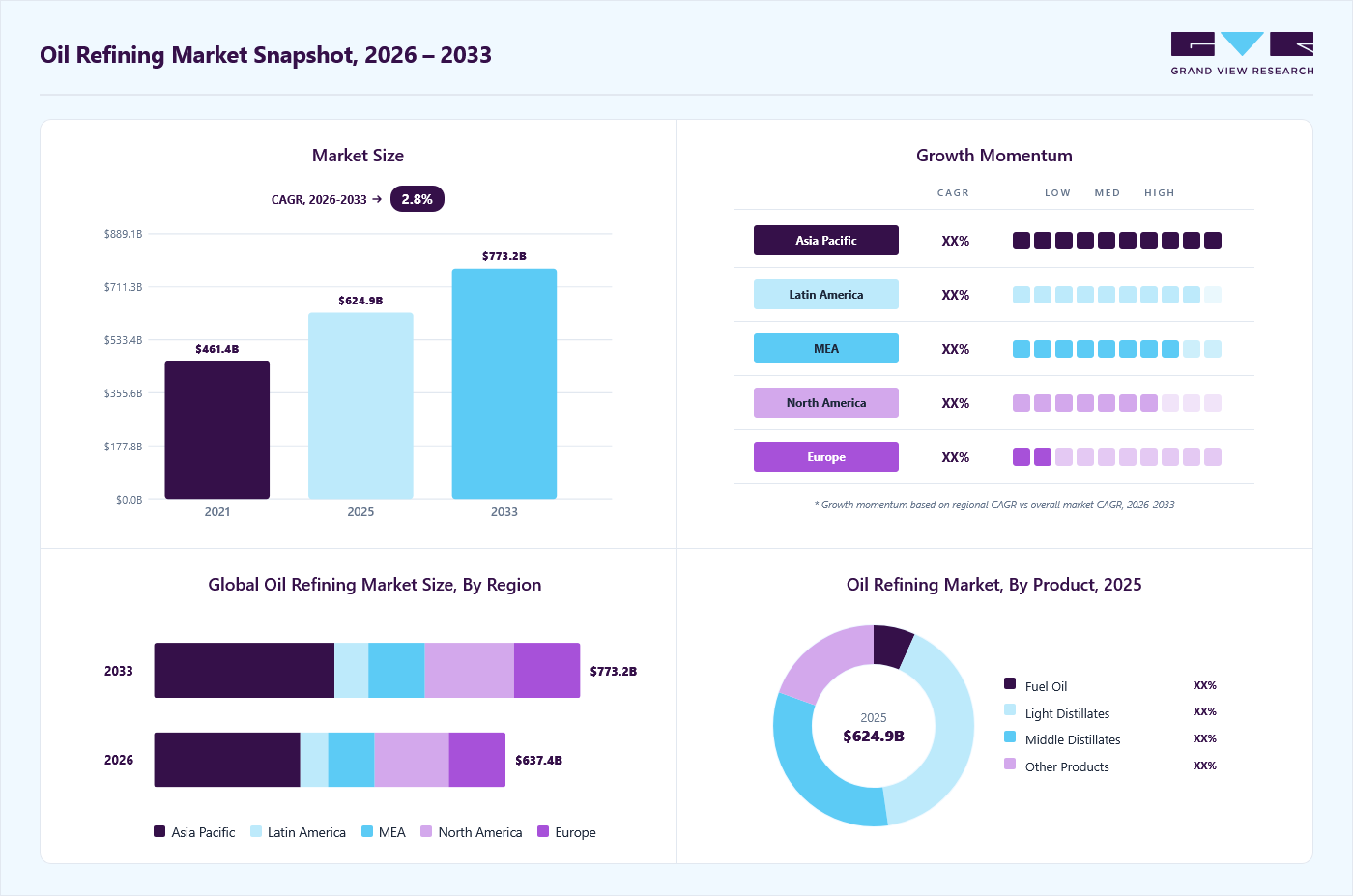

Market Size, 2025

$624.9BMarket Estimate, 2026

$637.4BMarket Forecast, 2033

$773.2BCAGR, 2026–2033

2.8%Oil Refining Market Summary

The global oil refining market size was valued at USD 624.9 billion in 2025 and is projected to grow from USD 637.4 billion in 2026 to USD 773.2 billion by 2033, at a CAGR of 2.8% from 2026 to 2033. The Asia Pacific held the largest share of 41.5% of the global market in 2025. The market is witnessing steady expansion, driven by increasing global demand for transportation fuels and petrochemical feedstock.

Key Market Trends & Insights

- By product: Light distillates segment held the largest market share of 40.9% in 2025.

- By complexity type: Deep conversion segment held the largest market share of 37.9% in 2025.

- By end-use: Transportation segment held the largest market share of 41.7% in 2025.

- By fuel type: Gasoil segment held the largest market share of 31.3% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (41.5% revenue share, 2025)

- By country: China held the largest share in 2025

Market Size & Forecast

- Market size in 2025: USD 624.9 Billion

- Estimated market size in 2026: USD 637.4 Billion

- Projected market size by 2033: USD 773.2 Billion

- CAGR (2026-2033): 2.8%

Accelerating urbanization and industrial growth across emerging economies are necessitating capacity additions to strengthen energy security and reduce dependence on imports. The global market is experiencing robust growth, driven by rising demand for transportation fuels, expansion in developing economies, and surging aviation traffic. As global populations grow and economies expand, particularly in emerging economies, the need for fuels for personal transport, public transit, and power generation remains a central pillar of market growth. In addition to this, a notable structural transformation is underway, with refineries increasingly integrating petrochemical production capabilities to address rising demand for plastics, textiles, and pharmaceutical products.")

Furthermore, the growing emphasis on operational efficiency and value optimization is significantly influencing market expansion. Refineries are increasingly adopting advanced technologies such as AI-based predictive maintenance and digital process control to enhance reliability, reduce downtime, and improve overall performance. The integration of refining operations with petrochemical production is also gaining momentum, enabling higher revenue generation through diversified product streams. Technological advancements in refining processes are improving efficiency, safety, and scalability across facilities.

Drivers, Opportunities & Restraints

The primary market driver is the sustained demand for transportation fuels and petrochemical feedstock in emerging economies. The transportation sector continues to be the dominant consumer of refined products. Despite the ongoing energy transition, fossil-based fuels remain indispensable for passenger vehicles, freight transportation, and commercial aviation. In response, refiners are investing in infrastructure upgrades not only to expand capacity but also to comply with increasingly strict emissions regulations and fuel quality standards. Furthermore, refineries are increasingly shifting output toward the petrochemical feedstock to diversify their revenue streams.

A significant opportunity lies in the integration of petrochemical production and the transition toward circular and low-carbon refining models within the oil refining ecosystem. Refiners are increasingly shifting from traditional fuel-centric operations to integrated complexes that produce high-value petrochemical outputs such as naphtha, propylene, and aromatics, enabling them to capture growing demand for plastics and synthetic materials. The ongoing evolution of refining infrastructure is facilitating greater product diversification and improved margin resilience. In addition, the conversion of legacy refining assets into biorefineries is gaining traction, supporting the production of Sustainable Aviation Fuel (SAF) and renewable diesel. This transition is aligned with global ESG mandates and decarbonization objectives, enhancing the long-term sustainability of the sector.

However, the market faces challenges related to supply chain disruptions and pricing volatility. Geopolitical instability has increasingly impacted global crude oil flows, particularly when conflicts disrupt tanker movements through critical chokepoints such as the Strait of Hormuz. These disruptions can significantly constrain crude availability, forcing refiners to source feedstock from alternative, often more expensive, regions. In addition, such uncertainties contribute to fluctuations in crude oil prices, increasing procurement costs, and affecting refining margins.

The market faces several regulatory restraints that may hamper its growth trajectory. Compliance with increasingly stringent environmental standards on emissions, wastewater management, and fuel sulfur content, such as those mandated under IMO 2020, is driving significant capital investment requirements for refiners. These regulations necessitate upgrades to desulfurization units and the adoption of advanced emission control technologies, increasing overall operational and compliance costs.

Product Insights

The light distillates segment accounted for the largest market share of 40.9% in 2025, driven by strong transportation demand, increasing petrochemical integration, and rising refining complexity. Compared to heavier fuels, light distillates generally produce fewer particulate emissions and are easier to atomize, resulting in more efficient combustion. Gasoline remains a key component of light distillate demand and is significantly influenced by seasonal driving trends in emerging economies. In addition, owing to their low viscosity, light distillates flow easily, making them easier to transport and suitable for use in various burners and engines without the need for extensive preheating.

The middle distillates segment is projected to register the fastest CAGR of 3.0% over the forecast period, driven by seasonal demand patterns. Demand often rises significantly during winter months due to increased use of distillates for heating purposes, along with higher diesel consumption across transportation sectors. Their high energy density enables efficient and powerful performance, making them particularly well-suited for heavy-duty trucking, aviation, and marine applications. In addition, sustained demand from logistics and industrial activities, coupled with the need for reliable and energy-efficient fuels, is further supporting segment growth.

Complexity Type Insights

Deep conversion accounted for the largest market share of 37.9% in 2025, driven by the need to maximize value from heavy crude and enhance overall refining profitability. Deep conversion enables refineries to upgrade bottom-of-the-barrel residues into lighter, more valuable distillates, significantly improving product yield. Key technologies such as hydrocrackers, delayed cokers, and advanced fluid catalytic cracking (FCC) units play a central role in increasing fuel output from heavier feedstocks. In addition, these units provide greater feedstock flexibility, allowing refiners to process lower-cost heavy crude as light crude becomes more expensive or constrained. Furthermore, deep conversion processes support product diversification by enabling the production of low-sulfur fuels and petrochemical feedstocks required to meet evolving environmental standards and market demand.

The deep conversion segment is projected to register the fastest CAGR of 3.1% over the forecast period, driven by rising demand for high-quality refined products in emerging economies. Deep conversion technologies enable refiners to maximize output of lighter, high-value products, making them particularly well-suited to meet this growing demand. In addition, stringent environmental regulations requiring cleaner, low-sulfur diesel and gasoline are driving substantial investments in advanced refining units, further supporting segment growth.

End-use Insights

Transportation accounted for the largest market share of 41.7% in 2025, driven by strong demand for mobility fuels across road, aviation, and marine sectors. Refined products such as gasoline, diesel, and jet fuel remain essential for passenger vehicles, freight transportation, and commercial aviation, supporting global economic activity. Compared to alternative energy sources, liquid fuels offer high energy density and established infrastructure, enabling efficient and reliable large-scale transportation. In addition, rising vehicle ownership and expanding logistics networks in emerging economies continue to drive fuel consumption, further strengthening the segment’s dominance.

The petrochemical segment is projected to register the fastest CAGR of 3.7% over the forecast period of 2026-2033, driven by rising demand for plastics and resins across a wide range of end-use industries. Demand is increasing significantly due to the expanding use of petrochemical derivatives in packaging, automotive, construction, and consumer goods. The ongoing industrialization of mega-refineries is further enabling integrated production of petrochemical feedstocks, enhancing value creation. In addition, the strategic shift by refiners toward petrochemical integration to sustain margins amid the growing impact of electric vehicles on fuel consumption is further supporting segment growth.

Fuel Type Insights

Gasoil accounted for the largest market revenue share of 31.3% in 2025, driven by strong industrial expansion, rising freight transportation demand, and ongoing geopolitical supply risks. Gasoil remains a critical fuel for heavy-duty applications, supporting logistics, construction, and industrial operations across both developed and emerging economies. Its widespread use in commercial transportation and off-road equipment reinforces its position as a key market segment. In addition, fluctuations in global supply dynamics and increasing reliance on diesel for economic activities are further contributing to the sustained growth of the gasoil segment.

The liquefied petroleum gas (LPG) segment is projected to register the fastest CAGR of 3.3% over the forecast period, supported by the transition to cleaner cooking fuels, industrial petrochemical demand, and government subsidies that improve access in developing economies. The surge in investments in this segment is primarily driven by rising consumption of LPG across residential, commercial, and industrial applications, along with its increasing use as a cleaner alternative to traditional solid and liquid fuels. Furthermore, the growing focus on energy accessibility and supply diversification is supporting the expansion of LPG production and export infrastructure, particularly in emerging economies with increasing energy demand.

Regional Insights

Asia Pacific oil refining market accounted for the largest revenue share of 41.5% in 2025, driven by rapid urbanization, economic expansion, and rising energy demand. Expanding middle-class populations and large-scale infrastructure development across countries are the key drivers of demand for transportation fuels and industrial materials. Several countries in the region are also strengthening domestic refining capabilities to support energy security and reduce import dependence. Moreover, a structural shift toward petrochemical integration is underway, with refineries increasingly aligned with the production of plastics, textiles, and pharmaceutical inputs to enhance value creation.

The market is growing at the fastest rate of 3.0% CAGR, supported by ongoing investments in refining capacity expansion, petrochemical integration, and advanced digital technologies aimed at enhancing operational efficiency and reliability. The increasing adoption of integrated refining-petrochemical complexes, alongside the modernization of existing facilities with AI-based monitoring and process optimization systems, is improving productivity and margin resilience. This positions the Asia Pacific region as a leading and highly developed market for oil refining. In addition, rising industrial fuel consumption, coupled with strong demand for petrochemical products such as plastics and synthetic materials, continues to reinforce the Asia Pacific’s dominant position in the global market.

China Oil Refining Market Trends

The oil refining market in China represents a major contributor, driven by strong energy security priorities, rapid industrialization, and extensive petrochemical integration. Under its strategic planning framework, including the 14th Five-Year Plan, the country emphasizes maintaining stable refining capacity to ensure a consistent energy supply, with the continued utilization of independent “teapot” refineries to support economic stability. China’s expanding urban population and industrial infrastructure are sustaining robust demand for transportation and industrial fuels.

Europe Oil Refining Market Trends

The oil refining market in Europe is experiencing steady growth, driven by supply chain disruptions, evolving trade dynamics, and a heightened focus on energy security. Escalating geopolitical tensions in the Middle East and restricted flows through critical maritime chokepoints have created a tight supply environment, prompting countries across the region to diversify sourcing strategies and strengthen refining supply networks. In addition, shifting geopolitical dynamics, particularly Western sanctions on Russia, have significantly altered global trade flows, positioning India as a key supplier of refined fuels to Europe. Supportive policies and strategic initiatives focused on supply security, trade diversification, and infrastructure resilience are further reinforcing the region’s refining market growth.

North America Oil Refining Market Trends

The oil refining market in North America is experiencing steady growth, supported by abundant feedstock availability and ongoing technological modernization. Refineries across the region are increasingly investing in advanced hydrocracking and coking units, along with AI-based predictive maintenance systems, to enhance processing capabilities and minimize operational downtime. Government support, favorable regulatory frameworks, and strategic investments by industry players are further driving the modernization and efficiency of refining operations across the region.

Latin America Oil Refining Market Trends

The oil refining market in Latin America is experiencing steady growth, supported by abundant crude reserves, evolving regulatory frameworks, and increasing emphasis on domestic value addition. The region holds significant oil reserves and continues to increase production, supporting long-term refining potential. In addition, regulatory and environmental mandates are driving refinery modernization, with countries like Brazil and Mexico advancing ultra-low sulfur fuel standards to improve air quality and public health outcomes. Although regulatory complexities and infrastructure challenges persist, ongoing investments in upgrading refining capabilities and improving fuel quality continue to support stable long-term market expansion across the region.

Middle East & Africa Oil Refining Market Trends

The oil refining market in MEA is expanding steadily, driven by rising aviation demand and increasing focus on energy security. Countries across the region are positioning themselves as global aviation hubs, necessitating higher production of jet fuel to support growing passenger and cargo traffic. This growth is further supported by ongoing investments in refining capacity and infrastructure upgrades aimed at enhancing self-sufficiency. Governments are increasingly prioritizing domestic refining capabilities to reduce reliance on imported refined products while meeting rising energy demand, thereby strengthening the region’s refining ecosystem.

Key Oil Refining Company Insights

Some of the key participants in the global market include Valero Energy Corporation, Marathon Petroleum Corporation, Phillips 66, HF Sinclair Corporation, PBF Energy Inc., Delek US Holdings, Sunoco LP, OMV AG, Repsol S.A., and SK Innovation. These companies are increasingly focusing on enhancing refining efficiency and optimizing cost structures while ensuring long-term operational reliability. In addition, strategic initiatives such as technological innovation, capacity expansion, and integration with petrochemical production are enabling them to strengthen their market position and influence industry dynamics.

Their operations typically encompass crude oil refining, fuel production, petrochemical manufacturing, storage, transportation, and distribution to ensure an efficient and reliable energy supply. Industry leaders are placing strong emphasis on advanced refining technologies such as hydrocracking, fluid catalytic cracking, and coking units to improve yield and process heavier crude efficiently. Significant investments are being directed toward the modernization of refining infrastructure, desulfurization technologies, and emission control systems to meet stringent environmental standards and enhance fuel quality. The integration of digital solutions such as artificial intelligence, predictive maintenance, and advanced process control systems is enabling real-time optimization, improved asset utilization, and enhanced operational reliability.

As global demand for transportation fuels and petrochemical feedstock continues to evolve, and energy security remains a key priority, companies operating in the market are prioritizing capacity optimization, supply chain resilience, and diversification of feedstock sources. Strategic collaborations, vertical integration across the value chain, and increasing investments in emerging economies are key growth strategies adopted by industry participants. Furthermore, shifting market dynamics, including the growing integration of petrochemicals, tightening environmental regulations, and advancements in refining technologies, are reshaping the competitive landscape. Continuous innovation in refining processes and digitalization is expected to enhance market competitiveness and support the sustained market growth.

Key Oil Refining Companies:

The following key companies have been profiled for this study on the oil refining market.

- Valero Energy Corporation

- Marathon Petroleum Corporation

- Phillips 66

- HF Sinclair Corporation

- PBF Energy Inc.

- Delek US Holdings

- Sunoco LP

- OMV AG

- Repsol S.A.

- SK Innovation

Recent Developments

-

In 2025, Sunoco LP and SunocoCorp LLC announced the completion of the acquisition of Parkland Corporation, along with the commencement of trading in SunocoCorp LLC common units. This strategic move aligns with the company’s objective to strengthen its downstream portfolio, expand its refining and fuel distribution footprint, and enhance its presence across key markets.

-

In 2026, Galp and Moeve announced a merger aimed at consolidating their refining and energy operations. This initiative is in line with their strategy to improve operational efficiencies, achieve economies of scale, and strengthen their competitive positioning within the evolving global market.

Oil Refining Market Report Scope

Report Attribute

Details

Market Definition

The market refers to the global revenue generated from the processing of crude oil into refined petroleum products such as gasoline, diesel, jet fuel, and other derivatives through refining operations across various end-use industries.

Market size value in 2026

USD 637.4 billion

Revenue forecast in 2033

USD 773.2 billion

Growth rate

CAGR of 2.8% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Product, fuel type, complexity type, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; India; Australia; Japan; South Korea; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

Valero Energy Corporation; Marathon Petroleum Corporation; Phillips 66; HF Sinclair Corporation; PBF Energy Inc.; Delek US Holdings; Sunoco LP; OMV AG; Repsol S.A.; SK Innovation

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Oil Refining Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global oil refining market report based on product, fuel type, complexity type, end-use, and region:

-

Product Outlook (Revenue, USD Billion, 2021 - 2033)

-

Fuel Oil

-

Light Distillates

-

Middle Distillates

-

Other Products

-

-

Fuel Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Gasoline

-

Kerosene

-

Liquefied Petroleum Gas

-

Gasoil

-

Other Fuels

-

-

Complexity Type Outlook (Revenue, USD Billion, 2021 - 2033)

-

Hydro-skimming

-

Topping

-

Conversion

-

Deep Conversion

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Marine Bunker

-

Transportation

-

Aviation

-

Petrochemical

-

Agriculture

-

Electricity

-

Residential & Commercial

-

Rail & Domestic Waterways

-

Other End Uses

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Australia

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The deep conversion segment led with a 37.9% revenue share in 2025 and is projected to register the fastest CAGR of 3.1% over the forecast period.

The transportation segment led with a 41.7% revenue share in 2025, while the petrochemical segment is the fastest-growing.

Gasoil segment held the largest share (over 31.0%) in 2025, while the liquefied petroleum gas (LPG) segment is the fastest-growing.

Asia Pacific dominated with a 41.5% revenue share in 2025.

The global oil refining market was estimated at USD 624.9 billion in 2025 and is expected to reach USD 637.4 billion in 2026.

The global oil refining market is expected to grow at a compound annual growth rate of 2.8% from 2026 to 2033 to reach USD 773.2 billion by 2033.

The light distillates segment led with a 40.9% revenue share in 2025, while the middle distillates segment is the fastest-growing.

Some of the key players operating in the global oil refining market include Valero Energy Corporation, Marathon Petroleum Corporation, Phillips 66, HF Sinclair Corporation, PBF Energy Inc., Delek US Holdings, Sunoco LP, OMV AG, Repsol S.A., SK Innovation, among others.

The key factors driving the growth of the global oil refining market include increasing global demand for transportation fuels and petrochemical feedstock. Accelerating urbanization and industrial growth across emerging economies are necessitating capacity additions to strengthen energy security and reduce dependence on imports.

About the Author(s)

Conventional Energy Research Team

Energy & Power · Conventional EnergyThis report was authored by the conventional energy research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the conventional energy segment of the energy & power industry. All findings are based on proprietary energy & power databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.