- Home

- »

- Next Generation Technologies

- »

-

Optical Transceivers Market Size Report, 2026-2033GVR Report cover

![Optical Transceivers Market (2026 - 2033)Report]()

Optical Transceivers Market (2026 - 2033)

Size, Share & Trends Analysis Report By Form Factor, By Data Rate, By Fiber Type, By Connector, By Protocol, By Distance, By Wavelength, By Application, By Region, And Segment Forecasts

Market Size, 2025

$15.4BMarket Estimate, 2026

$17.4BMarket Forecast, 2033

$36.2BCAGR, 2026–2033

11.1%Optical Transceivers Market Summary

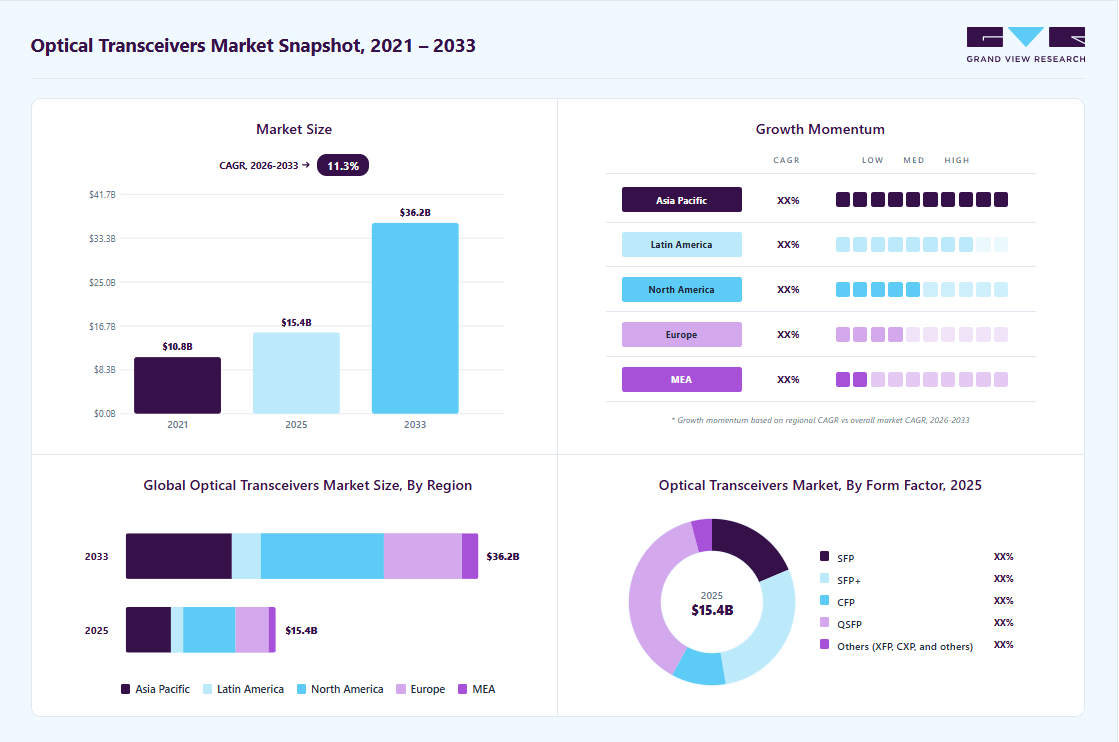

The global optical transceivers market size was valued at USD 15.4 billion in 2025 and is projected to grow from USD 17.4 billion in 2026 to USD 36.2 billion by 2033, at a CAGR of 11.1% from 2026 to 2033. North America dominated the market with the largest revenue share of 37.1% in the global market in 2025. The growth of the increasing adoption of high-speed optical modules for AI and cloud workloads, rising upgrades from legacy networks to advanced 100G to 800G architectures, expanding deployment of fiber-based connectivity across enterprise and telecom networks, and accelerating demand for energy-efficient optical components in modern data center environments.

Key Market Trends & Insights

- By form factor: The QSFP segment held the largest market share of 37.9% in 2025.

- By fiber type: The single-mode fiber (SMF) segment held the largest market share of 51.9% in 2025.

- By application: The telecommunication segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (37.1% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 15.4 Billion

- Estimated market size in 2026: USD 17.4 Billion

- Projected market size by 2033: USD 36.2 Billion

- CAGR (2026-2033): 11.1%

The demand for high-speed optical modules is accelerating as data centers and telecom operators shift away from legacy 10G/40G technologies. AI training clusters, cloud workloads, and hyperscale platforms are driving a rapid transition toward 100G, 200G, 400G, and emerging 800G transceivers. Enterprises now place greater emphasis on throughput efficiency, scalability, and long-term network readiness during fiber network refresh cycles. This market transition is unlocking a multi-year upgrade wave, improving revenue visibility for component suppliers. As high-speed connectivity becomes a core infrastructure priority, next-generation optical transceivers are evolving into the primary performance enabler of modern networks.

")

The optical transceivers industry is prioritizing energy-efficient modules as enterprises and telecom operators face rising power and operational costs. Vendors are rapidly innovating low-power DSPs, thermally optimized designs, and compact form factors to reduce the total cost of ownership. Growing adoption of green data center strategies is accelerating demand for energy-optimized 400G and 800G modules. This shift toward efficiency is strengthening the business case for modernizing aging optical infrastructure. As sustainability and cost optimization become board-level imperatives, energy-efficient transceivers are emerging as a central focus in strategic procurement.

The expansion of fiber networks by telecom operators is driven by the 5G rollout, small-cell densification, and increasing backhaul demands. Emerging fiber-deep architectures require long-reach, high-performance optical modules to ensure consistent and scalable connectivity across metro and access networks. Operators are prioritizing DWDM-enabled, coherent, and high-bandwidth transceivers to handle rising traffic loads. This wave of modernization is driving strong procurement momentum for 25G, 50G, 100G, and coherent optical modules. As telecom networks evolve to support next-generation mobility and broadband infrastructure, optical transceivers remain a critical driver of long-term industry growth.

Form Factor Insights

The QSFP segment significantly contributed to market growth in 2025, accounting for over 63% of global revenue, owing to its central role in high-density data transmission. Adoption accelerated as hyperscale data centers increasingly deployed 400G and 800G QSFP modules to build scalable, power-efficient architectures. Rising cloud traffic further supported momentum, with QSFP-DD and QSFP56 emerging as preferred form factors for next-generation switching platforms. Telecom operators also expanded their investments in 5G backhaul and metro networks, driving additional demand for QSFP-based coherent and pluggable optics. As enterprises continue modernizing their network cores, QSFP modules are expected to sustain strong growth and remain a primary catalyst for the expansion of high-bandwidth optical infrastructure.

The SFP+ segment is expected to grow at a significant CAGR during the forecast period, driven by rising demand for cost-efficient, low-power optical modules across enterprise networks, access layers, and short-reach data center interconnects. The increasing adoption of 10G upgrades in SMBs and campus networks is further driving deployment as organizations transition away from legacy copper-based links. The segment is also benefiting from the proliferation of edge data centers, where compact and power-optimized SFP+ modules deliver reliable performance for distributed workloads. Growing investments in fiber-based broadband and FTTx infrastructure are creating additional momentum, particularly in emerging markets. As network operators seek scalable and budget-friendly solutions, SFP+ modules remain a preferred choice for balancing performance, efficiency, and affordability.

Data Rate Insights

The less than 10 GBPS segment accounted for a significant share of market revenue in 2025, driven by its continued adoption in legacy enterprise networks that prioritize cost efficiency and reliability over ultra-high bandwidth. The segment benefited from steady replacement-cycle demand as organizations refreshed aging copper and fiber infrastructure without transitioning to higher-priced, high-speed alternatives. Expanding deployments in industrial automation environments also supported growth, leveraging low-speed transceivers for stable, hard-wired connectivity. Momentum remained strong due to broad compatibility with existing switches, routers, and access-layer networking equipment. Overall, sustained demand from cost-sensitive markets reinforced the segment’s relevance despite the industry’s broader shift toward high-speed optical modules.

The more than 100 GBPS segment is expected to grow at the highest CAGR over the forecast period, driven by telecom operators’ transition toward 5G-Advanced and early 6G-ready backbone modernization. Carriers are increasingly deploying 200G and 400G coherent modules across metro, regional, and long-haul networks to accommodate rising fronthaul and backhaul bandwidth demands. Accelerated fiber densification, expanded edge computing footprints, and ongoing small-cell rollout are further amplifying the need for high-capacity optical links. Vendors are also introducing cost-optimized pluggable coherent optics, making large-scale deployments of >100 GBPS more commercially viable. Collectively, these advancements position the >100 GBPS segment as a foundational enabler of next-generation telecom infrastructure.

Fiber Type Insights

The single-mode fiber (SMF) segment accounted for the significant market revenue share in 2025, propelled by the growing transition toward high-capacity long-haul and metro networks. Telecom operators increasingly favored SMF solutions to support escalating bandwidth requirements driven by 5G densification and cloud connectivity. Enterprises and hyperscale data centers accelerated SMF adoption to enhance backbone scalability and reduce latency within distributed compute environments. Vendors expanded their SMF-optimized transceiver portfolios, reinforcing demand for next-generation coherent and pluggable optics. This shift positioned SMF as a strategic enabler of high-performance digital infrastructure across global markets.

The multimode fiber (MMF) segment is expected to grow at the highest CAGR during the forecast period, driven by increasing deployment of short-reach, high-density interconnects in next-generation data centers. Its ability to deliver cost-effective high-speed transmission positions MMF as the preferred option for enterprises modernizing campus, edge, and distributed network environments. The ongoing transition to 40G, 100G, and 400G multimode transceivers is accelerating adoption, particularly in hyperscale facilities. Rising digitalization in BFSI, healthcare, and retail sectors is also boosting demand, supported by MMF’s lower installation, maintenance, and operational overheads. Moreover, continued advancements in VCSEL-based optical modules are enhancing performance and strengthening the commercial viability of multimode fiber solutions.

Connector Insights

The lucent connector (LC) segment accounted for a significant share of market revenue in 2025, driven by its compact connector design that supports high-density port configurations in modern networking environments. The industry’s shift toward space-efficient data center architectures has solidified LC as the preferred interface for next-generation optical systems. Growing deployments of high-speed transceivers, particularly within cloud and colocation facilities, are further accelerating LC adoption. Its low-loss performance and high reliability continue to support large-scale fiber rollouts across enterprise and telecom networks. As organizations prioritize scalability and operational efficiency, the LC connector remains a critical component of network modernization initiatives.

The multi-fiber push-on/pull-off (MPO) segment is expected to grow at the highest CAGR over the forecast period, driven by rising demand for high-density interconnects within hyperscale and cloud data center environments. This growth is further accelerated by the rapid adoption of 200G, 400G, and 800G transceiver modules, which depend on multi-fiber connectivity to support very high bandwidth requirements. Enterprises are increasingly selecting MPO connectors for their ability to simplify cable management and reduce operational complexity in large-scale network architectures. The shift toward parallel optics and modular fiber infrastructures is creating significant opportunities for MPO-based transceivers and connectivity solutions. In addition, the expanding deployment of AI and ML workloads, which require ultra-fast east-west traffic movement, is strengthening long-term demand for MPO technologies.

Protocol Insights

The Ethernet segment accounted for a significant share of market revenue in 2025, driven by the rapid modernization of network infrastructures across telecom, data center, and enterprise settings. Growing adoption of high-speed Ethernet transceivers is accelerating market expansion as operators move away from legacy copper-based systems toward scalable optical connectivity. The segment is also supported by rising demand for seamless cloud access, low-latency data transfer, and high-bandwidth applications enabled by AI, IoT, and big data workloads. Enterprises favor Ethernet-based optical solutions for their cost efficiency, interoperability, and support for future network upgrades. With digital transformation initiatives gaining momentum worldwide, Ethernet optical transceivers are becoming a central foundation of next-generation network architectures, reinforcing long-term growth for this segment.

The CWDM/DWDM segment is expected to grow at a significant CAGR over the forecast period, driven by rising demand for high-capacity optical links across metro and long-haul networks. Operators are adopting wavelength-division multiplexing technologies to maximize spectral efficiency and postpone costly fiber buildouts. The shift toward 5G, cloud connectivity, and bandwidth-intensive enterprise services is further accelerating DWDM deployment as networks evolve toward scalable, multi-terabit architectures. Vendors are integrating advanced modulation techniques, software-defined optical controls, and coherent optics to improve performance and reduce operational complexity. This growing momentum positions the CWDM/DWDM segment as a key driver of the optical transceiver market, enabling operators to manage rapidly increasing data traffic sustainably.

Distance Insights

The short distance segment accounted for the significant market revenue share in 2025, driven by the rapid expansion of high-density data centers requiring cost-effective and energy-efficient optical links. The growing adoption of cloud computing and AI workloads has accelerated demand for short-reach interconnects that support high-bandwidth, low-latency communication within racks. Enterprises increasingly prioritize scalable, plug-and-play short-distance transceivers to modernize LAN and campus network architectures. Vendors strengthened their portfolios with compact form factors such as SFP+, QSFP+, and QSFP28 to cater to next-generation server and switch upgrades. As digital transformation deepens across industries, the short-distance category remains a foundational driver of intra-data-center connectivity investments.

The long distance segment is expected to grow at a significant CAGR over the forecast period, driven by the rapid expansion of long-haul fiber infrastructure supporting national backbone upgrades and cross-border connectivity projects. Rising demand for high-capacity optical links in telecom operators' core networks is accelerating investments in long-reach transceivers with strong signal integrity. The rollout of 5G backhaul and the development of 6G-ready transport networks are further increasing the need for long-distance optical modules capable of supporting higher wavelengths and advanced modulation formats. Enterprises and cloud providers are also deploying long-reach solutions to strengthen inter-data-center and metro-regional connectivity frameworks. As bandwidth needs climb across digital economies, the long-distance optical transceiver segment will remain a key driver of scalable, future-ready network infrastructure.

Wavelength Insights

The 1310 nm band segment accounted for the significant market revenue share in 2025, driven by its strong suitability for short to medium-reach optical links in high-density network environments. Demand continues to rise as organizations upgrade to higher-speed transceivers that rely on the 1310 nm wavelength for improved signal integrity and lower dispersion. The segment also benefits from widespread adoption in data center interconnects and enterprise networks where consistent performance and lower power consumption are key priorities. The increasing deployment of 100G, 200G, and 400G modules based on 1310 nm optics is further accelerating their growth across modern digital infrastructures.

The 1550 nm band segment is expected to grow at a significant CAGR over the forecast period, propelled by its strong suitability for long-distance optical transmission with minimal signal loss. Advancements in coherent optics and enhanced dispersion management are further driving adoption across high-capacity backbone and metro networks. The wavelength’s ability to support higher data rates with superior reach makes it a preferred choice for scaling next-generation optical infrastructures. Increasing deployment of high-speed modules for cloud connectivity, data transport, and backbone upgrades continues to strengthen demand for 1550 nm solutions.

Application Insights

The telecommunication segment accounted for the largest market revenue share in 2025, fueled by the growing need for high-capacity optical links to manage rising data volumes across mobile and fixed networks. Continuous upgrades to backbone and metro layers are accelerating the adoption of high-speed optical transceivers. Service providers are focusing on improving network scalability, reducing latency, and supporting cloud, streaming, and enterprise workloads. The transition toward fiber-rich architectures is further strengthening demand across long-haul, metro, and access networks. Expanding investments in next-generation network modernization continue to position telecommunications as the dominant segment in the optical transceivers market.

The data centers segment is expected to grow at a significant CAGR over the forecast period, driven by rising requirements for high-bandwidth connections to support AI computing, cloud services, and large-scale enterprise applications. Expanding use of distributed compute architectures is increasing the need for optical modules that deliver higher speeds and improved energy efficiency. Operators are upgrading to advanced transceiver technologies to enhance network reliability, reduce latency, and streamline data traffic across complex workloads. Continued investment in new facility builds and modernization of existing network infrastructure is further strengthening demand for high-performance optical transceivers in the data center segment.

Regional Insights

The North America optical transceivers market is anticipated to account for over 37% of revenue in 2025, driven by accelerated cloud migration, rapid expansion of AI workloads, and widespread modernization of data center networks. Growing deployment of 400G and 800G transceivers across hyperscale facilities continues to strengthen regional demand. Telecom operators are also upgrading transport networks to support higher bandwidth for 5G expansion and fiber-to-the-home growth. Increasing investment from major technology companies reinforces North America’s position as a global hub for high-speed optical connectivity.

U.S. Optical Transceivers Market Trends

The U.S. optical transceivers market is expected to grow significantly in 2025, fueled by surging demand for AI data center interconnects and the shift toward high-capacity optical networking. Enterprises and cloud providers are accelerating upgrades from legacy 10G and 40G links to 100G, 400G, and emerging 800G modules to support intensive digital workloads. The country is also witnessing rising adoption of silicon photonics and advanced DSP technologies that improve energy efficiency and support multiterabit architectures. Increasing investment in hyperscale facilities, edge computing hubs, and fiber backbone expansion continues to reinforce the U.S. leadership in optical connectivity.

Europe Optical Transceivers Market Trends

The Europe optical transceivers market is expected to grow significantly over the forecast period, supported by growing investments in digital transformation, data center expansion, and cross-border fiber network development. European telecom operators are upgrading long-haul and metro optical networks to handle rising internet traffic and enterprise cloud usage. The increasing adoption of 400G and 800G modules among colocation and cloud providers is driving strong demand. Government initiatives promoting energy-efficient infrastructure are also encouraging the use of advanced optical transceiver technologies.

Asia Pacific Optical Transceivers Market Trends

The Asia Pacific optical transceivers market is anticipated to register the highest CAGR of over 14% during the forecast period, driven by the rapid expansion of hyperscale data centers, AI deployments, and national broadband programs across China, Japan, India, and Southeast Asia. Massive growth in mobile data consumption and 5G rollouts is accelerating the adoption of high-speed optical modules in telecom networks. Regional manufacturers are scaling production of 100G, 200G, 400G, and 800G transceivers at competitive costs, boosting global supply. Increasing government support for digital infrastructure development continues to push optical transceiver demand across emerging economies.

Key Optical Transceivers Company Insights

Some key companies in the optical transceivers industry are Coherent Corp., INNOLIGHT, Accelink Technology Co. Ltd., Cisco Systems, Inc., Broadcom Inc. and others

-

Coherent Corp. is suppliers of optical components and transceiver technologies, serving data centers, telecom networks, and AI cluster connectivity. The company specializes in advanced photonic devices, high-speed optical modules, coherent optics, and laser solutions used across cloud, 5G, and high-performance computing markets. Its transceivers are widely adopted for 400G, 800G, and emerging 1.6T applications, supported by strong vertical integration in chips, packaging, and optics. Coherent’s scale and deep engineering expertise make it a central player in enabling next-generation digital networks.

-

Accelink Technology Co. Ltd. is the optical communication equipment manufacturer in China, specializing in high-performance transceiver modules for telecom carriers, 5G networks, and data centers. The company produces a full range of optical modules including SFP, QSFP, and coherent optical solutions used in metro, long-haul, and backbone networks. Accelink is recognized for its strong R&D in photonic integration, high-speed modulation, and optical component design. Its extensive product portfolio positions it as a key supplier for both telecom operators and cloud infrastructure providers.

Key Optical Transceivers Companies:

The following key companies have been profiled for this study on the optical transceivers market.

- Coherent Corp.

- INNOLIGHT

- Accelink Technology Co. Ltd.

- Cisco Systems, Inc.

- Broadcom Inc.

- Lumentum Operations LLC

- Sumitomo Electric Industries, Ltd.

- Fujitsu Optical Components Limited

- Intel Corporation

- Eoptolink Technology Inc., Ltd.

Recent Developments

-

In October 2025, Credo introduced its ZeroFlap optical transceivers aimed at improving reliability in AI and high-performance networks. The products use the company's PILOT platform to monitor link quality, manage in-band messaging, and capture detailed telemetry to prevent link flaps. Credo is also contributing its ZeroFlap specification to a new Open Compute Project workstream that it co-leads with Oracle to help establish reliability standards for optical modules. The new transceivers, available for sampling, support 400G, 800G, and 1.6T speeds to meet the demands of large-scale AI infrastructure.

-

In September 2025, NEC introduced a 25 Gb/s SFP28 bidirectional optical transceiver that supports transmission up to 80 km on a single fiber. The module uses a high-output laser and high high-sensitivity receiver to achieve a 30 dB link budget, enabling long distance communication even on aging or high-loss fiber. It reduces fiber requirements through bidirectional WDM and consumes only 2.5 W, which is about 20 percent lower than typical products in this class. The transceiver is compatible with standard SFP ports for seamless upgrades from 10 Gb/s systems, and shipments are planned to begin at the end of November 2025.

-

In April 2025, Jabil introduced a 1.6 terabit pluggable transceiver designed to meet rising demand for high bandwidth connectivity in data centers and AI infrastructures. The module delivers either dual 800G Ethernet or Infiniband links or a single 1.6T link using a silicon photonics engine that operates at 200 Gbps per lane. It provides improved power efficiency while maintaining the reliability performance of Jabil's earlier 400G and 800G products. The transceiver is aimed at supporting the rapid scaling of next-generation computing and networking environments.

-

In March 2025, Broadcom introduced two new products, Sian3 and Sian2M, expanding its 200G per lane DSP PHY portfolio for next-generation network systems. These solutions are designed to support the growing performance needs of hyperscale data centers and AI infrastructure. The new devices help enable higher speed optical and electrical connections while improving power efficiency for large-scale deployments. With this launch, Broadcom strengthens its position in delivering advanced connectivity technology for future multiterabit network architectures.

Optical Transceivers Market Report Scope

Report Attribute

Details

Market size in 2025

USD 15.4 billion

Estimated market size in 2026

USD 17.4 billion

Projected market size by 2033

USD 36.2 billion

Growth rate

CAGR of 11.1% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion/million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Form Factor, data rate, fiber type, connector, protocol, distance, wavelength, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; Australia; South Korea; Brazil; UAE; South Africa; KSA

Key companies profiled

Coherent Corp.; INNOLIGHT; Accelink Technology Co. Ltd.; Cisco Systems, Inc.; Broadcom Inc.; Lumentum Operations LLC; Sumitomo Electric Industries, Ltd.; Fujitsu Optical Components Limited; Intel Corporation; Eoptolink Technology Inc., Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Optical Transceivers Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global optical transceivers market report based on form factor, data rate, fiber type, connector, protocol, distance, wavelength, application, and region.

-

Form Factor Outlook (Revenue, USD Million, 2021 - 2033)

-

Small Form-factor Pluggable (SFP)

-

Small Form-factor Pluggable Plus (SFP+)

-

C Form-factor Pluggable (CFP)

-

Quad Small Form-factor Pluggable (QSFP)

-

Others

-

-

Data Rate Outlook (Revenue, USD Million, 2021 - 2033)

-

Less than 10 Gbps

-

10 Gbps to 40 Gbps

-

41 Gbps to 100 Gbps

-

More than 100 Gbps

-

-

Fiber Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Single-mode Fiber (SMF)

-

Multimode Fiber (MMF)

-

-

Connector Outlook (Revenue, USD Million, 2021 - 2033)

-

Lucent Connector (LC)

-

Subscriber Connector (SC)

-

Multi-Fiber Push-On/Pull-Off (MPO)

-

Registered Jack-45 (RJ-45)

-

-

Protocol Outlook (Revenue, USD Million, 2021 - 2033)

-

Ethernet

-

Fiber Channel

-

CWDM / DWDM

-

FTTx

-

Others

-

-

Distance Outlook (Revenue, USD Million, 2021 - 2033)

-

Short Distance

-

Long Distance

-

-

Wavelength Outlook (Revenue, USD Million, 2021 - 2033)

-

850 nm band

-

1310 nm band

-

1550 nm band

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Telecommunication

-

Data Centers

-

Enterprise Networking

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

MEA

-

UAE

-

South Africa

-

KSA

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The QSFP segment held the market with the largest revenue share of 37.9% in 2025, while SFP+ is the fastest-growing segment.

The telecommunication segment accounted for the largest market revenue share in 2025.

The single-mode fiber (SMF) segment held the market with the largest revenue share of 51.9% in 2025, while multimode fiber (MMF) is the fastest-growing segment.

The global optical transceivers market size was estimated at USD 15.4 billion in 2025 and is expected to reach USD 17.4 billion in 2026.

The global optical transceivers market is expected to grow at a compound annual growth rate of 11.1% from 2026 to 2033, reaching USD 36.2 billion by 2033.

North America dominated the optical transceivers market, accounting for over 37% in 2025, driven by accelerated cloud migration, rapid expansion of AI workloads, and widespread modernization of data center networks. Growing deployment of 400G and 800G transceivers across hyperscale facilities continues to strengthen regional demand.

Some key players operating in the optical transceivers market include Coherent Corp., INNOLIGHT, Accelink Technology Co. Ltd., Cisco Systems, Inc., Broadcom Inc., Lumentum Operations LLC, Sumitomo Electric Industries, Ltd., Fujitsu Optical Components Limited, Intel Corporation, Eoptolink Technology Inc., Ltd.

Key factors driving market growth include the increasing adoption of high-speed optical modules for AI and cloud workloads, rising upgrades from legacy networks to advanced 100G to 800G architectures, expanding deployment of fiber-based connectivity across enterprise and telecom networks, and accelerating demand for energy-efficient optical components in modern data center environments.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.