- Home

- »

- Next Generation Technologies

- »

-

Quick Commerce Market Size And Share Report, 2026-2033GVR Report cover

![Quick Commerce Market Size, Share & Trends Report]()

Quick Commerce Market (2026 - 2033) Size, Share & Trends Analysis Report By Product Category (Grocery & Staples, Packaged Food & Snacks, Personal Care & Beauty), By Delivery Payment (Online, Cash), By Delivery (Instant Delivery), By Region, And Segment Forecasts

Market Size, 2025

$244.7BMarket Estimate, 2026

$297.5BMarket Forecast, 2033

$1,303.5BCAGR, 2026–2033

23.5%Quick Commerce Market Summary

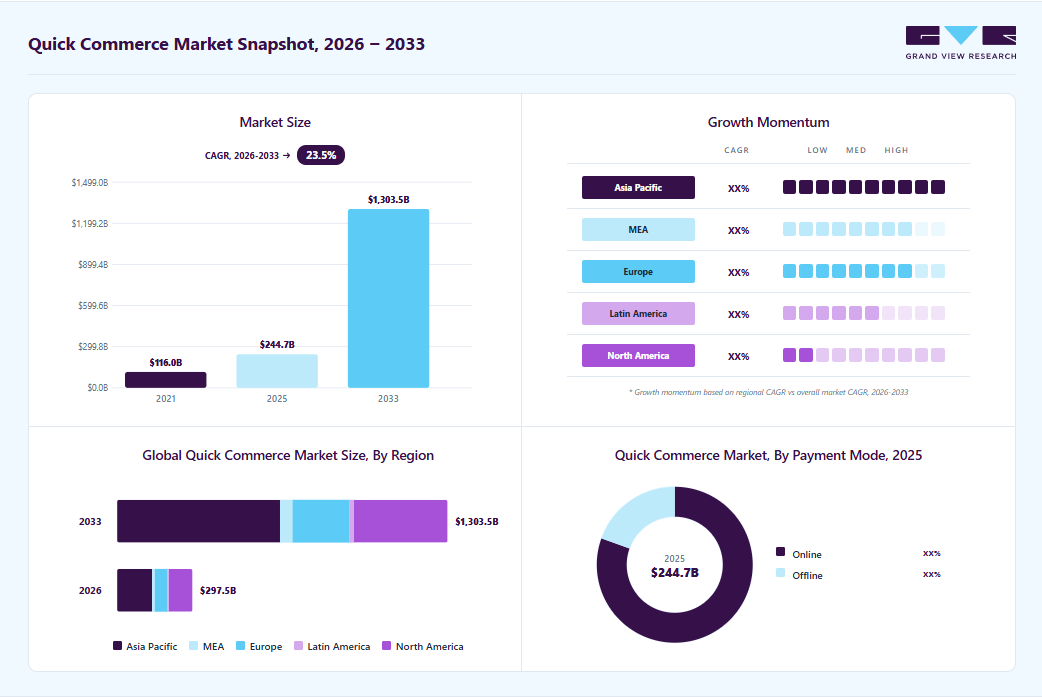

The global quick commerce market size was valued at USD 244.7 billion in 2025 and is projected to grow from USD 297.5 billion in 2026 to USD 1,303.5 billion by 2033, at a CAGR of 23.5% from 2026 to 2033, driven by the rising consumer preference for ultra-fast delivery services and on-demand convenience. The market in Asia Pacific dominated with a revenue share of 45.8% in 2025. Modern consumers, particularly in urban areas, increasingly expect groceries, personal care products, pharmaceuticals, and daily essentials to be delivered within minutes rather than hours or days.

Key Market Trends & Insights

- By product: Grocery & staples segment held the largest market share of 33.7% in 2025.

- By delivery payment: Online segment held the largest market share in 2025.

- By delivery: Instant delivery segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (45.8% revenue share, 2025)

- By country: China held a substantial market share in 2025

Market Size & Forecast

- Market size in 2025: USD 244.7 Billion

- Estimated market size in 2026: USD 297.5 Billion

- Projected market size by 2033: USD 1,303.5 Billion

- CAGR (2026-2033): 23.5%

The widespread penetration of smartphones, mobile applications, and digital payment ecosystems is also supporting quick commerce industry expansion. Increasing internet accessibility and growing consumer familiarity with app-based commerce platforms have enabled quick commerce companies to scale their customer base rapidly across developed and emerging economies. Advanced mobile interfaces, AI-driven recommendation engines, real-time inventory visibility, and frictionless payment systems are enhancing customer engagement and improving repeat purchase rates. In addition, the growing integration of loyalty programs, subscription-based delivery models, and personalized offers is strengthening customer retention and increasing order frequency.")

Rapid urbanization and increasing population density in metropolitan regions are also key contributors to the market’s growth. High-density urban environments create favorable operating conditions for quick commerce providers by enabling shorter delivery radii and improved fleet utilization. The expansion of middle-class populations, rising disposable incomes, and changing consumption patterns in emerging economies such as India, Southeast Asia, Latin America, and the Middle East are further accelerating demand for instant delivery services. Consumers are increasingly prioritizing convenience-oriented retail solutions, creating strong opportunities for quick commerce platforms to expand into tier-1 and tier-2 cities globally.

Market Dynamics

The rapid expansion of dark stores, micro-fulfillment centers, and hyperlocal logistics infrastructure is significantly driving the growth of the global quick commerce market. Companies are aggressively investing in strategically located fulfillment hubs to reduce delivery timelines and improve inventory availability for high-frequency consumer purchases. The growing need for 10-30-minute delivery services across groceries, pharmaceuticals, electronics, and personal care categories is encouraging retailers and logistics providers to expand dense urban fulfillment networks. In addition, advancements in route optimization, AI-driven demand forecasting, and real-time inventory management are improving operational efficiency and enabling faster order processing.

For instance, in May 2026, Shadowfax announced plans to expand its dark store network and strengthen quick commerce infrastructure to support projected revenue growth. The company stated that increased investments in hyperlocal fulfillment capabilities and rapid delivery infrastructure were aimed at capitalizing on rising demand for faster retail and e-commerce delivery services.

Increasing regulatory intervention related to gig worker welfare, rider safety, and labor rights is emerging as a major challenge for quick commerce providers globally. The pressure to deliver products within extremely short timeframes has raised concerns regarding unsafe driving practices, excessive workload pressures, and inadequate worker protections for delivery personnel. Governments and labor organizations across several regions are increasingly scrutinizing delivery timelines, compensation structures, and employment practices within the gig economy ecosystem.

For instance, in December 2025, the Indian government reportedly urged major quick commerce platforms including Blinkit, Zepto, Swiggy, and Zomato to reconsider aggressive “10-minute delivery” commitments following concerns related to rider safety and working conditions. Several platforms subsequently reduced emphasis on strict delivery timelines after discussions with regulatory authorities.

Market Concentration & Characteristics

The global quick commerce industry is moderately concentrated, with the presence of major e-commerce companies, food delivery platforms, retail conglomerates, and hyperlocal logistics providers alongside emerging regional startups specializing in ultra-fast delivery services. Leading companies maintain strong market positions through extensive dark store networks, advanced logistics infrastructure, strategic partnerships with retailers and FMCG brands, and large customer ecosystems across urban and metropolitan regions. These players offer integrated quick commerce capabilities including instant grocery delivery, pharmacy fulfillment, food and beverage distribution, household essentials delivery, and AI-enabled last-mile logistics services, creating significant barriers to entry due to high operational costs, dense fulfillment network requirements, advanced technology investments, and the need for efficient hyperlocal supply chain management.

In terms of market characteristics, the industry is highly technology-driven and operationally intensive, supported by rapid advancements in artificial intelligence, predictive analytics, route optimization, warehouse automation, and real-time inventory management technologies. Rising consumer demand for convenience-oriented retail experiences, increasing smartphone penetration, and the expansion of digital payment ecosystems are significantly accelerating quick commerce adoption globally. In addition, the market is characterized by aggressive dark store expansion, increasing investments in micro-fulfillment infrastructure, growing integration of electric delivery fleets, and continuous enhancement of delivery speed capabilities ranging from 10-minute to 30-minute fulfillment models. Companies are increasingly focusing on customer retention, subscription-based loyalty programs, personalized shopping experiences, and data-driven operational efficiency to strengthen competitive positioning.

Product Category Insights

The grocery & staples segment dominated the market and accounted for the revenue share of 33.7% in 2025 due to the increasing consumer preference for instant access to daily essentials, fresh produce, packaged foods, dairy products, beverages, and household necessities. Rising urbanization, busy lifestyles, and growing dependence on convenience-oriented shopping are encouraging consumers to shift from traditional retail visits toward app-based rapid grocery delivery platforms. The high purchase frequency and recurring demand associated with essential grocery items make this category particularly suitable for quick commerce business models, enabling companies to drive repeat orders and improve customer retention.

The personal care & beauty segment is anticipated to grow at the fastest CAGR during the forecast period due to increasing consumer demand for convenience-driven purchasing of skincare, cosmetics, hygiene products, haircare items, and wellness essentials. Consumers, particularly millennials and Gen Z populations, are increasingly using quick commerce platforms for instant access to premium and daily-use beauty products, driven by rising beauty consciousness, social media influence, and growing preference for on-demand retail experiences.

Delivery Payment Insights

The online segment dominated the market and accounted for the largest revenue share in 2025, driven by the increasing adoption of digital wallets, UPI platforms, contactless payment systems, and mobile banking applications. Consumers increasingly prefer seamless and cashless transaction methods for instant delivery purchases because of their speed, convenience, and enhanced transaction security. The widespread penetration of smartphones, rising internet accessibility, and government initiatives promoting digital payments in several countries are further accelerating online payment adoption across quick commerce platforms.

The offline segment is expected to grow at a significant CAGR during the forecast period. The offline payment segment continues to support the growth of the global market, particularly in emerging economies where a significant portion of consumers still prefer cash-based transactions and have limited access to digital banking services. Cash-on-delivery remains an important payment option for first-time online shoppers and consumers in semi-urban and tier-2 or tier-3 regions, as it provides greater trust, transaction transparency, and purchasing flexibility.

Delivery Insights

The instant delivery segment dominated the market and accounted for the largest revenue share in 2025 due to rising consumer demand for ultra-fast fulfillment of groceries, food, medicines, personal care items, and household essentials within minutes. Increasing urbanization, busy lifestyles, and growing preference for convenience-oriented shopping experiences are encouraging consumers to rely on rapid delivery platforms for immediate purchasing needs. Quick commerce companies are aggressively expanding dark store networks, micro-fulfillment centers, and AI-enabled last-mile logistics systems to reduce delivery timelines and improve order accuracy.

The scheduled delivery segment is expected to grow at a significant CAGR over the forecast period due to increasing consumer demand for greater flexibility, convenience, and planned purchasing of groceries, household essentials, pharmacy products, and bulk orders. Many consumers prefer scheduled delivery options for routine or non-urgent purchases as they allow better control over delivery timing and reduce the need for immediate availability during order fulfillment. Businesses and working professionals also increasingly utilize scheduled deliveries to align purchases with their daily routines and avoid missed deliveries.

Regional Insights

North America Quick Commerce Market Trends

North America quick commerce industry held a significant share in the global market in 2025, driven by the strong penetration of digital commerce platforms, high consumer spending capacity, and increasing demand for convenience-oriented retail services. Consumers across the region are increasingly adopting app-based instant delivery services for groceries, pharmacy products, ready-to-eat meals, and household essentials due to fast-paced lifestyles and growing preference for time-saving shopping experiences.

U.S. Quick Commerce Market Trends

The quick commerce industry in the U.S. is expected to grow significantly at a CAGR of 14.2% from 2026 to 2033, due to the rapid expansion of dark store infrastructure and increasing investments by major technology-enabled delivery platforms. Companies are aggressively enhancing hyperlocal fulfillment capabilities, integrating AI-powered route optimization, and expanding rapid grocery delivery partnerships with retailers and convenience store chains.

Asia Pacific Quick Commerce Market Trends

Asia Pacific quick commerce industry dominated the global market with the largest revenue share of 45.8% in 2025, due to rapid urbanization, rising middle-class populations, and increasing smartphone and internet penetration across emerging economies. Countries across the region are witnessing strong growth in app-based retail ecosystems due to changing consumer lifestyles, increasing disposable incomes, and rising preference for instant delivery of groceries, food, healthcare products, and daily essentials.

The Japan quick commerce market is expected to grow rapidly in the coming years, driven by the country’s aging population and growing demand for highly convenient home delivery services. Consumers increasingly prefer fast and reliable delivery platforms for groceries, medicines, and ready-to-eat meals due to busy work cultures and rising single-person households

The China quick commerce market held a substantial market share in 2025, due to the country’s developed digital ecosystem and the dominance of super-app-based commerce platforms. Consumers widely use integrated platforms combining payments, food delivery, social commerce, and instant retail services, enabling seamless adoption of rapid delivery models.

Europe Quick Commerce Market Trends

The quick commerce industry in Europe is anticipated to register considerable growth from 2026 to 2033 due to rising urban population density and growing sustainability-focused logistics innovation. European consumers are increasingly adopting ultra-fast delivery services supported by compact urban infrastructure, enabling efficient last-mile delivery operations within short delivery radii.

The UK quick commerce market is expected to grow rapidly in the coming years, owing to the increasing integration of quick commerce into mainstream grocery retail operations. Major supermarket chains and online delivery platforms are expanding partnerships and micro-fulfillment capabilities to provide rapid delivery services for fresh produce, ready meals, and convenience products.

The Germany quick commerce market held a substantial market share in 2025 due to rising consumer demand for efficient urban grocery delivery services and increasing investments in automated fulfillment technologies. The country’s strong logistics infrastructure and advanced warehouse automation capabilities are supporting the development of highly optimized dark store operations and inventory management systems.

Key Quick Commerce Company Insights

Key players operating in the quick commerce industry are Meituan, Alibaba Group, DoorDash, Uber Technologies, and Delivery Hero. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In April 2026, Uber Technologies expanded its partnership with Block to strengthen restaurant operations and digital payment services across Uber and Uber Eats. The collaboration includes expanding Square’s Uber Eats integration into Canada, Australia, the UK, Ireland, France, and Spain, while also introducing Cash App Pay for U.S. Uber and Uber Eats users. The partnership further builds on Uber’s earlier integration of Afterpay in Australia to support flexible payment options within the quick commerce ecosystem.

-

In December 2025, DoorDash announced a partnership with OpenAI to integrate grocery shopping capabilities directly into ChatGPT. The collaboration enables users to convert recipe recommendations and meal ideas generated within ChatGPT into real-time grocery orders through the DoorDash platform. Customers can browse ingredients, place orders from nearby grocery stores, and receive deliveries within approximately one hour, strengthening DoorDash’s position in AI-driven quick commerce and conversational shopping experiences.

-

In August 2025, Delivery Hero introduced a new “Last Stop” feature designed to give delivery riders greater flexibility and control over how they end their delivery sessions. The feature allows riders to choose their preferred final delivery location before going offline. The functionality has already been launched across foodpanda operations in Hong Kong, Pakistan, and Taiwan, as well as foodora platforms in Finland, Norway, and Hungary, with broader global deployment currently underway.

Key Quick Commerce Companies:

The following key companies have been profiled for this study on the quick commerce market.

-

Alibaba (Freshippo / Hema, Ele.me)

-

BigBasket (BB Now)

-

Blinkit

-

Deliveroo

-

Delivery Hero (incl. Glovo, Foodora)

-

DoorDash

-

Flipkart Minutes

-

Getir

-

Gopuff

-

Instacart

-

JD.com

-

Meituan

-

Swiggy Instamart

-

Uber Eats

-

Zepto

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Meituan; Alibaba Group; DoorDash; Uber Technologies; Delivery Hero

- Expanding dark store networks, hyperlocal fulfillment infrastructure, and integrated last-mile delivery ecosystems across major metropolitan regions.

- Investing in AI-driven demand forecasting, warehouse automation, route optimization, subscription-based loyalty programs, and diversified instant retail offerings including groceries, pharmaceuticals, electronics, and lifestyle products.

- Strong brand recognition, large active customer bases, and extensive logistics infrastructure enabling large-scale rapid delivery operations.

- Broad operational ecosystems combining food delivery, grocery commerce, mobility, payments, and digital retail services.

- High operational complexity and rising labor, fulfillment, and infrastructure costs impacting profitability.

- Large organizational structures may reduce operational agility and slow adaptation to rapidly changing consumer preferences and hyperlocal market dynamics.

Emerging Players: Zepto; Blinkit; Gopuff; Getir

- Focusing on ultra-fast delivery models, dense dark store deployment, AI-enabled inventory optimization, and highly localized fulfillment strategies.

- Developing asset-light, technology-centric operating models designed to improve delivery efficiency and customer engagement.

- Faster execution capabilities and greater operational agility in responding to evolving customer demand and local market trends.

- Strong specialization in quick commerce operations, hyperlocal logistics, and dark store optimization.

- Ability to rapidly experiment with pricing strategies, delivery models, and customer engagement initiatives compared to larger incumbents.

- Limited profitability due to high cash burn, aggressive discounting, and continuous infrastructure expansion requirements.

- Dependence on external funding, strategic partnerships, and dense urban demand concentration for sustaining growth.

- •Lower geographic diversification and weaker financial resilience compared to established multinational platform operators.

Quick Commerce Market Report Scope

Report Attribute

Details

Market size in 2025

USD 244.7 billion

Estimated market size in 2026

USD 297.5 billion

Projected market size by 2033

USD 1,303.5 billion

Growth rate

CAGR of 23.5% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Product category; delivery payment; delivery; region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Alibaba (Freshippo / Hema, Ele.me); BigBasket (BB); Blinkit; Deliveroo; Delivery Hero (incl. Glovo, Foodora); DoorDash; Flipkart Minutes; Getir; Gopuff; Instacart; JD.com; Meituan; Swiggy Instamart; Uber Eats; Zepto

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Quick Commerce Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global quick commerce market report based on product category, delivery payment, delivery, and region.

-

Product Category Outlook (Revenue, USD Billion, 2021 - 2033)

-

Grocery & Staples

-

Packaged Food & Snacks

-

Personal Care & Beauty

-

Pharmacy / Health & Wellness

-

Small Electronics & Accessories

-

Fashion & Lifestyle

-

Household Products

-

Others

-

-

Delivery Payment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Online

-

Cash

-

-

Delivery Outlook (Revenue, USD Billion, 2021 - 2033)

-

Instant Delivery

-

Scheduled Delivery

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customization

This report has been delivered with the following in-depth customizations

Client Request

Customization Delivered

Value Adds

Quick commerce pricing and delivery business model analysis

Study of pricing structures for instant grocery delivery, subscription-based delivery memberships, surge pricing models, platform commission structures, and hyperlocal fulfillment fees.

Benchmarking of inventory-led, marketplace-led, dark store-led, and hybrid quick commerce operating models across key regions.

Supported pricing strategy optimization and profitability assessment.

Identified competitive monetization trends and customer retention strategies.

Enabled strategic evaluation of dark store versus partner-retailer fulfillment models.

Dark store infrastructure and hyperlocal logistics network assessment

Research on dark store expansion strategies, micro-fulfillment center deployments, warehouse automation technologies, and urban logistics infrastructure developments.

Analysis of their impact on delivery efficiency, inventory optimization, and rapid order fulfillment capabilities.

Identified strategic urban clusters supporting future quick commerce demand.

Supported long-term fulfillment network expansion and operational planning.

Highlighted infrastructure bottlenecks and emerging opportunities in high-density metropolitan markets.

Consumer behavior and category expansion analysis in quick commerce

Study of evolving consumer purchasing behavior across groceries, pharmaceuticals, electronics, beauty products, and lifestyle categories within quick commerce platforms.

Analysis of average order value trends, repeat purchase behavior, and convenience-driven consumption patterns.

Identified high-growth product categories and customer engagement opportunities.

Supported targeted product assortment and expansion strategies.

Enabled demand forecasting and customer acquisition optimization.

Frequently Asked Questions About This Report

The global quick commerce market is expected to grow at a CAGR of 23.5% from 2026 to 2033, reaching USD 1,303.5 billion.

Key factors include rising consumer demand for ultra-fast delivery and on-demand convenience, widespread penetration of smartphones, mobile applications, and digital payment ecosystems. Modern consumers, particularly in urban areas, increasingly expect groceries, personal care products, pharmaceuticals, and daily essentials to be delivered within minutes rather than hours or days.

Key players include Alibaba (Freshippo / Hema, Ele.me); BigBasket (BB); Blinkit; Deliveroo; Delivery Hero (incl. Glovo, Foodora); DoorDash; Flipkart Minutes; Getir; Gopuff; Instacart; JD.com; Meituan; Swiggy Instamart; Uber Eats; Zepto.

Asia Pacific dominated with a 45.8% revenue share in 2025.

The grocery & staples led with a 33.7% revenue share in 2025, while personal care & beauty is the fastest-growing category.

Online held the largest revenue share in 2025, while offline is the significant-growing payment.

Instant delivery segment held the largest revenue share in 2025.

The global quick commerce market size was valued at USD 244.7 billion in 2025 and is estimated at USD 297.5 billion for 2026.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.