- Home

- »

- Medical Devices

- »

-

Rigid Endoscopes Market Size And Share Report, 2026-2033GVR Report cover

![Rigid Endoscopes Market (2026 - 2033)Report]()

Rigid Endoscopes Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Laryngoscopes), By Angle Of View, By Product Dimension (<2 mm, 2-3.9 mm), By Product Length, By Surgical Center Size, By Surgical Center Location, By End-use, By Region, And Segment Forecasts

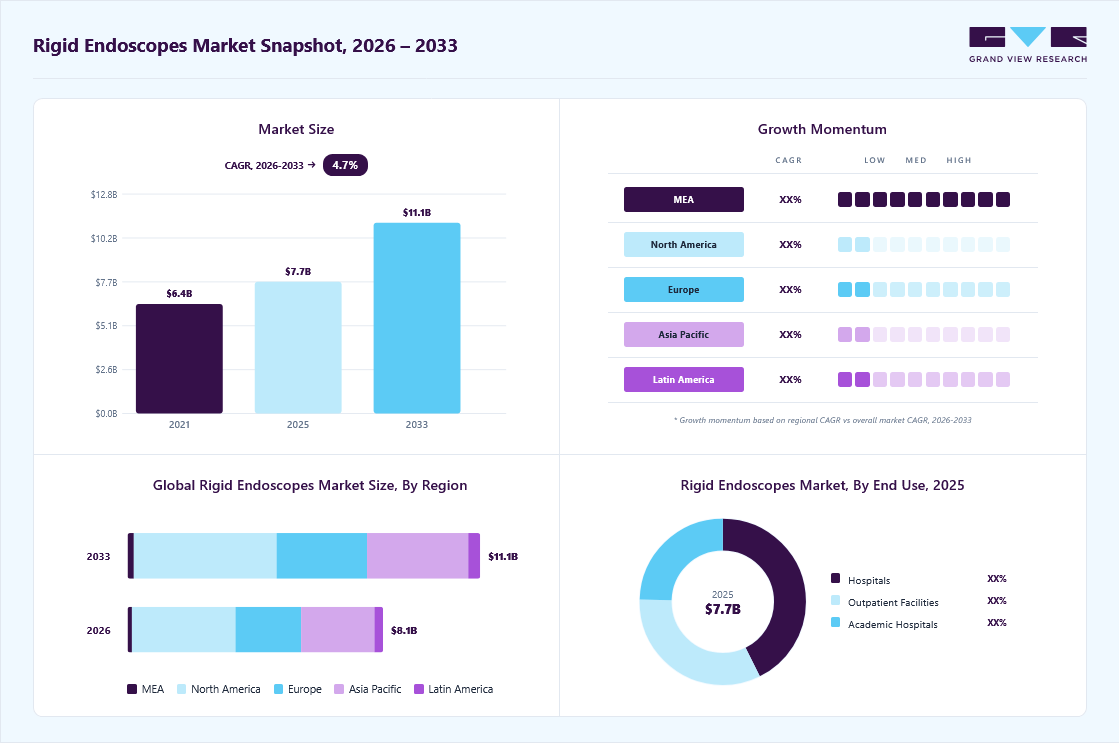

Market Size, 2025

$7.7BMarket Estimate, 2026

$8.1BMarket Forecast, 2033

$11.1BCAGR, 2026–2033

4.7%Rigid Endoscopes Market Size & Trends

The global rigid endoscopes market size was valued at USD 7.7 billion in 2025 and is projected to grow from USD 8.1 billion in 2026 to USD 11.1 billion by 2033, at a CAGR of 4.7% from 2026 to 2033. The market in North America dominated with a revenue share of 40.6% in 2025. The increasing prevalence of cancer and cancer-related mortality globally is one of the factors expected to drive the market growth.

Key Market Trends & Insights

- By product: Rigid laparoscopes segment held the largest market share of 28.7% in 2025.

- By angle of view: 30° segment held the largest market share of 38.9% in 2025.

- By end-use: Hospitals segment held the largest market share of 67.4% in 2025.

Regional Highlights

- Largest regional market: North America (40.6% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 7.7 Billion

- Estimated market size in 2026: USD 8.1 Billion

- Projected market size by 2033: USD 11.1 Billion

- CAGR (2026-2033): 4.7%

For instance, according to the American Cancer Society article published in January 2025, an estimated 2,041,910 new cancer cases are expected to be diagnosed in the U.S. in 2025, with approximately 618,120 cancer-related deaths projected during the year. With the prevalence of cancer rising globally, there is a growing need for effective diagnostic and treatment procedures. Endoscopes play a crucial role in offering minimally invasive options to accurately diagnose, stage, and treat various forms of cancer.")

Market Drivers

Role of Endoscopic Procedures in Cancer Detection and Management

Endoscopic procedures, such as Endoscopic Ultrasonography (EUS) and Endoscopic Retrograde Cholangiopancreatography (ERCP), are valuable in detecting & assessing cancer in the gastrointestinal tract, lung, and other areas. These procedures allow for precise visualization of internal tissues, biopsy collection, and even removing precancerous growths or early stage tumors without open surgery. This improves patient outcomes and significantly reduces recovery times & the risk of complications associated with invasive surgical procedures.

Estimated number of new cancer cases in the U.S., 2025

Cancer Type

Male Cases

% of Total (Male)

Female Cases

% of Total (Female)

Estimated Deaths Male

Estimated Deaths Male

Prostate

313,780

29.79%

-

0.00%

35,770

-

Breast

2,800

0.27%

316,950

32.06%

510

42,170

Lung & Bronchus

110,680

10.51%

115,970

11.73%

64,190

60,540

Colon & Rectum

82,460

7.83%

71,810

7.26%

28,900

24,000

Urinary Bladder

65,080

6.18%

19,790

2.00%

12,640

4,780

Melanoma of the Skin

60,550

5.75%

44,410

4.49%

5,470

2,960

Kidney & Renal Pelvis

52,410

4.98%

28,570

2.89%

9,550

4,960

Non-Hodgkin Lymphoma

45,140

4.29%

35,210

3.56%

11,060

8,330

Thyroid

12,670

1.20%

31,350

3.17%

1,090

1,200

Oral Cavity & Pharynx

42,500

4.04%

17,160

1.74%

9,130

3,640

Leukemia

38,720

3.68%

28,170

2.85%

13,500

10,040

Pancreas

34,950

3.32%

32,490

3.29%

27,050

24,930

All sites

1,053,250

100.00%

988,660

100.00%

323,900

294,220

Source: American Cancer Society, Inc., Surveillance and Health Equity Science & GVR

Impact of Technological Advancements in Endoscopy on Early Cancer Detection

Moreover, the advancements in endoscopic technologies, including high-definition visualization and the integration of artificial intelligence (AI) for enhanced diagnosis, are making these procedures even more effective at detecting & treating cancer at its early stages. This is leading to a wider use of endoscopic methods in treating cancer, significantly contributing to the growth of endoscopy devices market.

Rising Adoption of Minimally Invasive and Keyhole Surgical Techniques

Furthermore, minimally invasive or keyhole surgeries, utilizing small incisions for the diagnosis and treatment of various conditions, are gaining widespread acceptance globally. Surgeons are increasingly favoring robotic & endoscopic surgeries over conventional open surgeries due to the numerous benefits they offer.

Benefits of Minimally Invasive Surgeries

-

Reduced Postoperative Complications: Minimally invasive surgeries significantly lower the risk of postoperative complications compared to traditional open surgeries. The smaller incisions reduce the chances of infection and other surgical complications.

-

Shorter Hospital Stay and Recovery Time: Patients undergoing minimally invasive surgeries typically experience shorter hospital stays and faster recovery times. This enhances patient comfort and reduces the burden on healthcare facilities.

-

Decreased Blood Loss: These surgeries result in less blood loss during procedures, which is crucial for patient safety and recovery.

-

Economic Viability: Minimally invasive surgeries are often more cost-effective than open surgeries. The shorter hospital stays and quicker recoveries reduce overall healthcare costs, making these procedures economically viable alternatives.

The rigid endoscopes industry is rapidly evolving, driven by increasing regulatory approvals from the U.S. Food and Drug Administration and frequent new product launches. Technological advancements in imaging and minimally invasive technologies are improving procedural accuracy and patient outcomes, while expanding clinical applications. Moreover, manufacturers are strengthening R&D efforts to deliver more advanced and efficient endoscopic solutions.

List of FDA-approved rigid endoscopes and visualization system or device

Year of Approval

Company

Product Name

Description

September 2025

Outlook Surgical

Inova 1 Towerless Endoscope System

Obtained FDA 510(k) clearance for a hybrid endoscope system that combines features of rigid and flexible endoscopes for enhanced surgical visualization, one-handed operation, and HD imaging without bulky external towers. This is positioned for clinical use starting early 2026.

May 2025

Olympus Corporation

EZ1500 Series with EDOF technology

Received FDA 510(k) clearance for advanced imaging endoscopes equipped with Extended Depth of Field (EDOF) technology as part of the EVIS X1 endoscopy system, offering improved visualization with wide range focus and less need for focal adjustments.

January 2024

EndoSound

EndoSound’s Vision system

Integrates ultrasound imaging with endoscopy to enhance diagnostic capabilities.

December 2023

IQ Endoscopes

Q Vision G-100 (First-Generation Gastroscope)

Designed for gastrointestinal endoscopy, for visualization and treatment of the GI tract.

These advancements highlight a significant shift in the market, with a growing number of FDA approvals and product launches improving patient safety and driving market growth.

Expansion of Healthcare Infrastructure Driving Endoscopy Demand

The growing number of healthcare centers, such as hospitals, oncology specialty clinics, and cancer centers, is increasing the need for rigid endoscopes, which is expected to drive market growth. The number of endoscopies being performed in hospitals is growing with the increase in hospital facilities. The number of hospitals is increasing in most countries, including the U.S., the UK, Italy, Spain, China, India, Brazil, South Africa, and the UAE. According to American Hospital Association, there are 6,120 hospitals in the U.S. in 2024. Similarly, there were 1,300 hospitals in Canada. The European Union has around 15,000 hospitals. Moreover, the UK has 1148 hospitals as of August 2023.

Strategic Investments and Industry Consolidation Trends

In addition, many players in the market are increasingly investing in developing new products and continuously improving existing products. For instance, in October 2023, Foresight Group (Foresight), an investment company, announced a USD 6.69 million investment along with USD 1.67 million from Clydesdale Bank in Clearview Endoscopy Limited. This company repairs, services, and maintains rigid and flexible endoscopes. The company offers its services to customers across Ireland and the UK.

Market Concentration & Characteristics

The rigid endoscopes industry is experiencing moderate innovation driven by incremental improvements in optical clarity, illumination, and ergonomic design. Technological advancements such as high-definition and 4K imaging, fluorescence-assisted visualization, and digital image enhancement are improving surgical accuracy and diagnostic outcomes. Collaboration between optics and software developers is enabling real-time visualization upgrades. However, innovation adoption is constrained by high equipment costs, sterilization requirements, and compatibility challenges with existing operating room systems.

The rigid endoscopes industry is witnessing moderate merger and acquisition activity, focused on acquiring specialized firms in optical engineering, imaging technologies, and minimally invasive tools to enhance product portfolios and innovation capabilities. Moreover, key players are increasingly engaging in licensing and strategic collaborations with smaller technology companies to access emerging solutions while managing risk and supporting steady market expansion.

Regulatory requirements play a key role in the rigid endoscopes industry, with strict rules covering sterilization safety, material compatibility, optical quality, and device durability. Meeting approvals such as FDA clearance, CE marking, and international quality standards increases development time and costs. Manufacturers with strong regulatory capabilities and global compliance systems benefit from faster approvals and smoother market access, giving them a competitive edge.

Product expansion in the rigid endoscopes industry is steady, focused on refining existing designs and integrating advanced visualization technologies. Manufacturers are adding scopes with different sizes and viewing angles while improving compatibility with 3D and 4K imaging systems to meet diverse surgical needs. Bundled platforms that combine endoscopes with digital imaging and instruments, along with newer robotic and compact camera innovations, are enhancing precision and expanding clinical applications.

Regional expansion in the market is being fueled by rising minimally invasive surgeries across Asia Pacific, Latin America, and the MEA. Manufacturers are strengthening local production, distribution partnerships, and surgeon training to boost market presence. Moreover, growing government healthcare investments, these efforts are improving access to advanced endoscopic technologies and accelerating adoption in emerging regions.

Product Insights

By product, the rigid laparoscopes segment dominated the market with the largest revenue share of over 28.7% in 2025. Rigid laparoscopes remain a core tool in minimally invasive surgery due to their durability, high-quality imaging, and cost-effectiveness. They support smaller incisions, faster recovery, and broad use across multiple surgical specialties. Growing demand for minimally invasive procedures, hospital upgrades, and improvements such as HD/4K optics, LED lighting, and lighter designs continues to drive steady segment growth.

The otoscopes segment is anticipated to grow at the fastest CAGR over the forecast period. Strategic initiatives by the key players drives the growth of the market. For instance, in November 202, the partnership between E.A.R. Customized Hearing and BeBird led to the launch of cordless digital otoscope kits featuring high-resolution, real-time imaging for ear exams and wax removal. Their portable, cost-effective design supports remote viewing and telemedicine, improving access and efficiency for hearing care professionals. This reflects the broader shift in the rigid endoscope market toward compact, digital, and connected diagnostic solutions.

Angle of View Insights

By angle of view, the 30°segment dominated the market with the largest revenue share of over 38.9% in 2025 and is anticipated to grow at the fastest CAGR over the forecast period. The 30° rigid scope is the most widely used angle of view in diagnostic and operative rigid endoscopy. It balances forward and lateral visualization, enabling surgeons to see around structures without physically repositioning the scope as frequently. This flexibility makes 30° scopes the standard choice in laparoscopic surgery, urology, gynecology, and general endoscopy. Devices such as the Olympus 5 mm 30° Rigid Laparoscope are used in hospitals and ambulatory centers. They are instrumental in gynecologic procedures (e.g., ovarian cystectomy, endometriosis treatment) and general surgery (e.g., cholecystectomy, hernia repair), where both central and peripheral structures need simultaneous monitoring.

The 45°segment is anticipated to grow at a significant CAGR over the forecast period. The 45° rigid endoscope is gaining traction in advanced laparoscopic, colorectal, and bariatric surgeries. This angle provides an extended oblique view, enabling surgeons to look “around corners” in deep or complex anatomical sites such as the pelvis, retroperitoneum, or upper mediastinum. This enhanced visualization is critical during dissections near sensitive structures or tight operative fields. Examples include the Olympus 5 mm 45° Laparoscope, which is designed with improved light distribution and reduced glare. In robotic and thoracoscopic setups, these scopes enable dynamic orientation without requiring frequent repositioning of the patient or instrument. They are often used with articulating camera systems or scope holders in longer procedures.

Product Dimension Insights

By product dimension, the 4-5.9 mm segment dominated the market with the largest revenue share of over 29.8% in 2025. Rigid scopes with diameters between 4 mm and 5.9 mm scopes are standard in general surgery, gynecology, urology, and thoracic procedures. The 5 mm rigid laparoscope is widely used due to its optimal balance of durability, image quality, and compatibility with standard trocar systems. Examples include the Olympus 5 mm 30° and 45° rigid endoscopes and Stryker's autoclavable 5 mm HD scope. Their broad utility spans laparoscopic cholecystectomy, appendectomy, nephrectomy, hysterectomy, and endometriosis ablation. These scopes are highly compatible with current-generation 4K and fluorescence-guided systems, enhancing procedural accuracy and intraoperative decision-making.

The 2-3.9 mm segment is anticipated to grow at the fastest CAGR over the forecast period. Growth in this segment is fueled by the shift to outpatient and minimally invasive diagnostics. In gynecology, there is rising demand for small-diameter scopes compatible with portable towers, making them ideal for mobile or remote clinics. The affordability of these scopes, along with strong procedure compatibility and moderate reusability, ensures consistent demand. Unit volume growth is vigorous in emerging markets where cost-sensitive clinics prefer smaller screens for adult and pediatric diagnostic applications.

Product Length Insights

By product length, the standard/long length scopes (30-35 cm) segment dominated the market with the largest revenue share of over 36.3% in 2025 and is anticipated to grow at the fastest CAGR over the forecast period. Standard-length rigid scopes (30-35 cm) are the most commonly used tools in laparoscopic surgery, offering the ideal balance of reach, ergonomics, and clear visualization across procedures such as general, bariatric, gynecologic, and colorectal operations. Leading manufacturers like Olympus Corporation, KARL STORZ, and Stryker Corporation provide durable, autoclavable scopes that are widely adopted in hospitals and training centers. Their versatility and reliability make them a standard component of most minimally invasive surgery systems.

The extra-long scopes (> 35 cm) segment is anticipated to grow at a significant CAGR over the forecast period. Extra-long rigid scopes (>35 cm) are used in deep-cavity surgeries, bariatric and thoracic surgeries, robotic-assisted surgeries, and spinal endoscopies. Due to their extended reach, these scopes require enhanced handling and sterility solutions. They often employ sterile draping or sheathing systems to maintain asepsis while preventing cross-contamination across longer shaft lengths. Notable examples include robotically compatible 38-45 cm scopes, bariatric laparoscopes, and spinal endoscopes used in minimally invasive discectomies. Companies such as Intuitive Surgical, KARL STORZ, and Stryker offer scopes tailored for longer procedures, often integrating camera heads, fluorescence guidance, and articulated sheathing systems.

Surgical Center Size Insights

By surgical center size, the large (300+ beds) segment dominated the market with the largest revenue share of over 41.0% in 2025. Multispecialty hospitals, academic medical centers, and tertiary care institutions comprise the large surgical centers. With departments for surgery, training, oncology, and high-acuity care, these facilities require a spectrum of rigid scopes across all specialties general, colorectal, gynecology, urology, thoracic, ENT, bariatric, and more. These hospitals require scopes of all diameters and lengths, including robotic-compatible extra-long scopes, angled optics for complex dissections, and chip-on-tip systems for integrated imaging. Vendors such as Olympus, KARL STORZ, and Stryker maintain long-term equipment partnerships with these institutions, often bundling scopes with visualization towers and service contracts.

The medium (100-299 beds) segment is anticipated to grow at the fastest CAGR over the forecast period. Medium-sized surgical centers include regional hospitals, urban community hospitals, and private surgical institutes. Although these centers offer surgeries across specialties, they operate within mid-range budgets and limited OR capacity. Their scope of procurement is guided by versatility, standardization, and OR efficiency. They generally require 4-5.9 mm autoclavable scopes in standard lengths (30-35 cm), with angled optics (30°, 45°) being the preferred choice across most MIS procedures. Scope selection is often tied to manufacturer support. Many centers enter vendor agreements that bundle endoscopes with light sources, monitors, and processors under long-term maintenance contracts.

Surgical Center Location Insights

By surgical center location, the metropolitan segment dominated the market with the largest revenue share of over 48.1% in 2025 and is anticipated to grow at the fastest CAGR over the forecast period. Metropolitan surgical centers in large urban cities constitute the largest and most technologically advanced segment of the rigid endoscopes industry. These centers include public and private tertiary care hospitals, academic medical centers, and multi-specialty private institutions. Due to high patient volumes, procedure diversity, and funding access, they drive the demand for rigid endoscopes. Metropolitan centers have the infrastructure to support a full range of rigid scopes varying in angle, diameter, and length across specialties such as general surgery, gynecology, urology, thoracic, and bariatrics. These hospitals are early adopters of 4K/3D visualization, robotic-integrated rigid scopes, and chip-on-tip imaging systems. Countries with large urban hospital networks, such as the U.S., Germany, and the UK, dominate this segment’s growth.

The suburban segment is anticipated to grow at a significant CAGR over the forecast period. Suburban surgical centers are located in smaller urban clusters or the periphery of major cities. They consist mainly of mid-sized community hospitals, specialty clinics, and ambulatory surgical centers (ASCs) that provide essential surgical care at a lower cost structure than metro facilities. Rigid endoscopes in suburban centers cover routine laparoscopic, gynecologic, and urology procedures. These centers prefer standard-diameter (4-5.9 mm), autoclavable scopes with 30°/45° viewing angles and moderate shaft lengths. Furthermore, the rising patient preference for localized, convenient care is a key market driver for the segment's growth. As populations in suburban regions grow particularly among middle-aged and elderly groups requiring routine surgeries, demand increases for facilities that offer high-quality procedures without traveling to congested city hospitals.

End-use Insights

By end-use, the hospitals segment dominated the market with a revenue share of over 67.4% in 2025. Hospitals dominate the rigid endoscope end-use segment, accounting for the largest revenue share. This setting includes public, private, multi-specialty, and tertiary care hospitals, which handle a broad spectrum of surgeries across general, gynecologic, urologic, bariatric, orthopedic, and thoracic specialties. Rigid endoscopes are essential for emergency and elective procedures, and their presence is standard in most OR suites. Hospitals typically maintain large fleets of autoclavable rigid endoscopes in multiple diameters and lengths, allowing for efficient turnover, multi-procedure compatibility, and adherence to sterilization protocols. Major OEMs such as Olympus, KARL STORZ, Stryker, and Richard Wolf often supply hospital chains under capital bundles or service contracts, which include replacement cycles, scope tracking systems, and integrated video towers.

Theoutpatient facilities segment is expected to grow at the fastest CAGR during the forecast period. The outpatient segment comprises ambulatory surgical centers (ASCs) and specialty surgical centers, is growing rapidly as global healthcare systems shift toward cost-effective, short-stay interventions. These centers focus on high-volume, low-acuity MIS procedures such as laparoscopic cholecystectomy, hernia repair, diagnostic hysteroscopy, and urology interventions. Outpatient facilities play a vital role in the rigid endoscope market by providing convenient & efficient diagnostic and therapeutic procedures. The increasing popularity of endoscopes in outpatient settings is attributed to their numerous advantages. One significant advantage of endoscopes in outpatient facilities is their cost-effectiveness. Such factors boost the segment growth.

Regional Insights

North America rigid endoscopes industry dominated the market with a revenue share of 40.6% in 2025. Established regional R&D competencies, a high utilization rate of minimally invasive surgeries, and an efficient healthcare infrastructure all contribute to this dominance. In addition, the growing awareness of laparoscopic procedures among patients and healthcare providers is leading to the establishment of market leadership. In April 2023, Xenocor, a Utah-based medical device company, raised USD 10 million to launch its Saberscope, a single-use, HD, fog-free, articulating laparoscope cleared by the FDA.

U.S. Rigid Endoscopes Market Trends

The U.S. rigid endoscopes market held the largest revenue share in North America region in 2025. The growing preference for minimally invasive procedures across various medical specialties in the U.S., including gastroenterology, urology, and gynecology, is driving the demand for rigid endoscopes. Furthermore, the rising prevalence of cancer, the growing geriatric population, which is susceptible to chronic illnesses requiring endoscopic procedures, and the increasing importance of timely disease diagnosis & early interventions are driving the demand for endoscopes. According to the American Cancer Society, approximately 26,890 new cases of stomach cancer and around 10,880 stomach cancer-related deaths are expected to be reported in 2024.

Europe Rigid Endoscopes Market Trends

The rigid endoscopes market in Europe is expected to grow significantly over the forecast period. Ongoing technological advancements in endoscopy and rise in demand for minimally invasive procedures are among the factors driving the Europe market. Favorable macro environment factors are driving key players to revise their market entry strategies through mergers & acquisitions and technological collaborations to expand their footprint.

UK rigid endoscopes market is expected to grow significantly during the forecast period. The growing awareness of and preference among physicians and patients for improving post-procedure outcomes and growing investment by public or private market players and hospitals are driving the demand for rigid endoscopes. For instance, in May 2025, the Queen's Medical Centre (QMC) is expected to receive a refurbished and expanded unit to boost clinical capacity. This development comes after a significant investment of 16.31 million from Nottingham University Hospitals (NUH) NHS Trust, the organization that operates the hospital in collaboration with NHS England.

The rigid endoscopes market in Germany is expected to witness growth over the forecast period. The adoption of rigid endoscopes in Germany is expected to be driven by the increasing prevalence of chronic diseases. For instance, according to an article published by NCBI in February 2024, 46% of the adult population reported at least one chronic health condition in Germany. Furthermore, the presence of a greater number of endoscopic device manufacturers in Germany, coupled with a surge in the development of rigid endoscopes, is fueling market growth in the region.

Asia Pacific Rigid Endoscopes Market Trends

The Asia Pacific rigid endoscopes industry is expected to register the fastest CAGR over the forecast period. The region's growth is fueled by rising surgical volumes, awareness of minimally invasive procedures, and increasing healthcare costs. Government initiatives and the rapid expansion of hospitals in China, South Korea, and India further accelerate demand. In April 2025, to improve minimally invasive surgical capabilities in the area, the Administrator General of Tamil Nadu donated an advanced laparoscopy system with a high-definition camera to Kanniyakumari Government Medical College and Hospital.

China rigid endoscopes market is anticipated to register considerable growth during the forecast period. Growth is driven by expanding hospital infrastructure, increasing medical tourism, rising adoption of laparoscopic surgeries across tertiary and secondary care facilities and technological advanced product launch. In October 2023, Olympus Corporation launched its next-generation EVIS X1 endoscopy system in China, marking the availability of the system in all the major markets of Olympus. The Olympus EVIS X1 endoscopy system represents a significant advancement in medical technology for GI practitioners.

The rigid endoscopes market in Japan is expected to witness rapid growth, driven by aging population, strict procedural guidelines, and the use of the latest laparoscopic technology in medical facilities. in June 2024, an 8K Super Hi-Vision medical camera system (the MKC-820NP) was used in clinical trials in Japan to transmit laparoscopic surgical images in real time for telementoring, representing ongoing innovation in ultra-high-definition visualization for surgical guidance.

Latin America Rigid Endoscopes Market Trends

The Latin America rigid endoscopes market is anticipated to witness considerable growth over the forecast period. Growth is fueled by rising investments in healthcare infrastructure, increasing minimally invasive surgical procedures, and expanding awareness of laparoscopic benefits. In January 2025, MicroPort MedBot’s Toumai laparoscopic surgical robot received market approval from Brazil’s ANVISA, marking a milestone in robotic-assisted laparoscopic surgery in Latin America.

Brazil rigid endoscopes market is anticipated to register considerable growth during the forecast period. Rising procedural volumes, government support for modernizing healthcare facilities, and adopting advanced imaging technologies drive market expansion. In October 2024, Purple Surgical officially launched in Brazil at the 72nd Congress of Coloproctology, introducing its rigid endoscopes and other advanced laparoscopic instruments, surgical staplers, and trocars to the local market.

Middle East and Africa Rigid Endoscopes Market Trends

The Middle East and Africa rigid endoscopes market is anticipated to witness considerable growth over the forecast period, driven by large-scale healthcare infrastructure expansion, rising adoption of minimally invasive surgery, and increasing integration of robotic-assisted laparoscopic platforms across advanced hospitals in the Gulf and key African urban centers. Government healthcare transformation programs, along with rapid private hospital network development, are accelerating procurement of advanced rigid laparoscopes for general surgery, gynecology, urology, and bariatric procedures.

Saudi Arabia rigid endoscopes market is anticipated to register considerable growth during the forecast period. Government programs to enhance surgical results, expanding healthcare infrastructure, and a growing emphasis on minimally invasive procedures in public and private hospitals are some of the driving factors of this industry. In November 2024, Fujifilm Middle East expanded in Saudi Arabia through MoUs with healthcare providers, endoscopy training programs, and AI-driven screening centers aligned with Vision 2030.

Key Rigid Endoscopes Company Insights

Key participants in the rigid endoscopes industry are focusing on devising innovative business growth strategies, such as expanding their product portfolios, partnerships and collaborations, mergers and acquisitions, and expanding their business footprints.

Key Rigid Endoscopes Companies:

The following key companies have been profiled for this study on the rigid endoscopes market.

- Olympus Corporation

- Arthrex, Inc.

- Karl Storz GmbH & Co. KG

- Stryker Corporation

- Smith+Nephew

- Richard Wolf GmbH

- Medtronic Plc

- B. Braun Melsungen AG

- CONMED Corporation

Recent Developments

-

In December 2025, Olympus Corporation officially announced the launch of its latest generation rigid cystoscopes through its formal press release channels, confirming the product introduction as a verified corporate development. The announcement, published on the company’s official Europe newsroom platform, outlines enhancements in optical clarity, durability, and ergonomic design intended to support improved visualization during urological procedures.

-

In November 2024, Medtronic strengthened its surgical and endoscopy portfolio by acquiring Fortimedix Surgical, a developer of articulating instruments used in minimally invasive and endoscopic procedures.

-

In March 2024, NTT Corporation and Olympus Corporation launched a cloud-based endoscopy system demonstration that enables real-time image processing and analysis during procedures. The platform enhances diagnostic precision, improves workflow efficiency, and supports better clinical decision-making, representing a major advancement in digital endoscopic imaging.

-

In September 2024, Stryker launched its 1788 Advanced Imaging Platform in India. This versatile surgical visualization system, developed for various medical specialties, offers surgeons advanced imaging features that contribute to better patient outcomes.

-

In August 2023, Huaxin Medical and Yisi Medical formed a strategic alliance to accelerate the development and global commercialization of innovative rigid endoscopes. The partnership combines Huaxin’s R&D and manufacturing strengths with Yisi’s brand, clinical expertise, and international marketing channels.

Rigid Endoscopes Market Report Scope

Report Attribute

Details

Market size in 2025

USD 7.7 billion

Estimated market size in 2026

USD 8.1 billion

Projected market size by 2033

USD 11.1 billion

Growth rate

CAGR of 4.7% from 2026 to 2033

Actual data

2021 - 2025

Forecast data

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, angle of view, product dimension, product length, surgical center size, surgical center location, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; Spain; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Olympus Corporation; Arthrex, Inc.; Karl Storz GmbH & Co. KG; Stryker Corporation; Smith+Nephew; Richard Wolf GmbH; Medtronic Plc; B. Braun Melsungen AG; CONMED Corporation

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Rigid Endoscopes Market Report Segmentation

This report forecasts revenue growth and provides global, regional, and country levels analysis of the latest trends in each of the sub-segments from 2021 to 2033. For this report, Grand View Research has segmented the global rigid endoscopes market report based on product, angle of view, product dimension, product length, surgical center size, surgical center location, end-use, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033) (Procedure Volume, In Thousands, 2021 - 2033) (Unit Volume, In Thousand Units, 2021 - 2033)

-

Rigid Laparoscopes

-

Gynecology Endoscopes

-

Gastrointestinal Endoscopes

-

Colonoscope

-

Gastroscope (Upper GI Endoscope)

-

Duodenoscope

-

Enteroscope

-

Sigmoidoscope

-

-

Bronchoscopes

-

Ureteroscopes

-

Laryngoscopes

-

Otoscopes

-

Cystoscopes

-

Nasopharyngoscopes

-

Arthroscopes

-

Rhinoscopes

-

Neuroendoscopes

-

Hysteroscopes

-

-

Angle of View Outlook (Revenue, USD Million, 2021 - 2033)

-

0°

-

30°

-

45°

-

Others (70°, 90°, 120°+)

-

-

Product Dimension Outlook (Revenue, USD Million, 2021 - 2033)

-

<2 mm

-

2-3.9 mm

-

4-5.9 mm

-

≥6 mm

-

-

Product Length Outlook (Revenue, USD Million, 2021 - 2033)

-

Short Length Scopes (< 20 cm)

-

Medium Length Scopes (20-30 cm) [Autoclavable]

-

Standard/Long Length Scopes (30-35 cm)

-

Extra-Long Scopes (> 35 cm) [Draped (Sterile Sheathed)]

-

-

Surgical Center Size Outlook (Revenue, USD Million, 2021 - 2033)

-

Small (1-99 beds)

-

Medium (100-299 beds)

-

Large (300+ beds)

-

-

Surgical Center Location Outlook (Revenue, USD Million, 2021 - 2033)

-

Metropolitan

-

Suburban

-

Rural

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals

-

Outpatient Facilities

-

Ambulatory Surgical Centers

-

Specialty Surgical Centers

-

-

Academic Hospitals

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033) (Procedure Volume, In Thousands, 2021 - 2033) (Unit Volume, In Thousand Units, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

30° held the largest revenue share 38.9% in 2025.

Hospitals held the largest share (over 67.4%) in 2025 and theoutpatient facilities is the fastest-growing market.

North America dominated with a 40.6% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

The global rigid endoscopes market size was valued at USD 7.7 billion in 2025 and is expected to reach USD 8.1 billion by 2026.

Some of the key players operating in the market are Olympus Corporation; Arthrex, Inc.; Karl Storz GmbH & Co. KG; Stryker Corporation; Smith+Nephew; Richard Wolf GmbH; Medtronic Plc; B. Braun Melsungen AG; CONMED Corporation

The increasing prevalence of cancer and cancer-related mortality globally is one of the factors expected to drive the market

The global rigid endoscopes market is projected to grow at a CAGR of 4.7% from 2026 to 2033 to reach USD 11.1 billion by 2033.

The rigid laparoscopes segment led with a 28.7% revenue share in 2025, while otoscopes is the fastest-growing segment.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.