- Home

- »

- Plastics, Polymers & Resins

- »

-

Self-Adhesive Labels Market Size, Share Report, 2024-2030GVR Report cover

![Self-Adhesive Labels Market (2024 - 2030)Report]()

Self-Adhesive Labels Market (2024 - 2030)

Size, Share & Trends Analysis Report By Composition (Facestock, Adhesives), By Type (Release Liner, Linerless) By Technology (Flexography, Digital Printing), By Nature, By Application, By Region, And Segment Forecasts

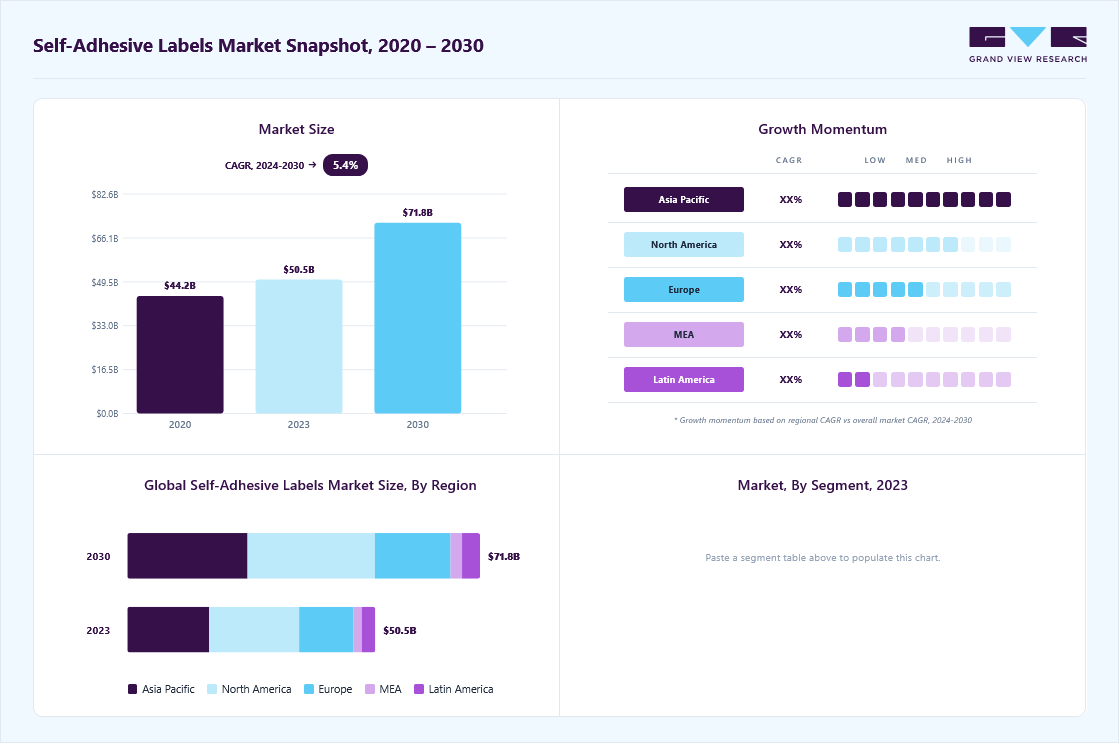

Market Size, 2023

$50.5BMarket Estimate, 2026

$57.1BMarket Forecast, 2030

$71.8BCAGR, 2024–2030

5.4%Self-Adhesive Labels Market Summary

The global Self-Adhesive labels market size was valued at USD 50.5 billion in 2023 and is projected to grow from USD 57.1 billion in 2026 to USD 71.8 billion by 2030, at a CAGR of 5.4% from 2024 to 2030. The market in North America dominated with a revenue share of 36.4% in 2023. The market is experiencing robust growth driven by the increasing demand for packaged goods, particularly in the food and beverage, personal care, and pharmaceuticals industries.

Key Market Trends & Insights

- By composition, adhesives segment held the largest market share of 85% in 2023.

- By type, release liners segment dominated the self-adhesive labels market and accounted for largest revenue share of over 74% in 2023.

- By nature, permanent labels segment held the largest market share in 2023.

Market Size & Forecast

- 2023 Market Size: USD 50.5 Billion

- 2030 Projected Market Size: USD 71.8 Billion

- CAGR (2024-2030): 5.4%

- North America: Largest market in 2023

As consumers seek convenience and product information, the need for high-quality, informative, and aesthetically pleasing labels is rising. Another critical driver is the advancement in labeling technologies. Innovations such as smart labels, which incorporate QR codes and RFID tags for better tracking and consumer engagement, are gaining traction. For example, Avery Dennison launched its new range of sustainable self-adhesive labels that reduce environmental impact, highlighting the trend towards eco-friendly products. Additionally, regulatory requirements for product information, safety, and traceability are pushing manufacturers to adopt advanced labeling solutions. In emerging markets, urbanization and increased consumer spending are leading to higher demand for labeled products.")

Opportunities in the market are also emerging from the shift towards sustainable materials. With increasing environmental concerns, there is a growing preference for labels made from recyclable and biodegradable materials. Companies like UPM Raflatac are investing in developing sustainable facestock and adhesives, opening new avenues for growth. The rise of e-commerce also presents significant opportunities, as online retailers require efficient labeling solutions for logistics and branding purposes.

Market Dynamics

The global self-adhesive labels industry is experiencing significant growth due to the increasing demand for sustainable, visually appealing, and operationally efficient packaging solutions across industries such as food & beverages, pharmaceuticals, personal care, logistics, and retail. Brand owners are increasingly adopting self-adhesive labels because they offer superior print quality, strong durability, moisture resistance, and enhanced shelf appeal compared to traditional glue-applied labels. These labels support advanced printing technologies, including digital and variable data printing, enabling manufacturers to incorporate QR codes, RFID tags, barcodes, product traceability features, and personalized branding elements. As packaging becomes a critical tool for product differentiation and consumer engagement, self-adhesive labels are gaining widespread acceptance for their flexibility across various substrates including glass, plastic, metal, and corrugated packaging.

In addition, growing environmental awareness and tightening packaging sustainability regulations are accelerating innovation in eco-friendly self-adhesive label materials. Manufacturers are increasingly developing recyclable, linerless, biodegradable, and water-based adhesive labels to align with circular economy goals and corporate sustainability commitments. The rapid expansion of e-commerce and organized retail has further amplified demand for durable and efficient labeling solutions that can withstand transportation, warehousing, and varying environmental conditions while ensuring accurate inventory tracking and regulatory compliance. Furthermore, sectors such as pharmaceuticals and food packaging increasingly rely on self-adhesive labels for tamper evidence, authentication, ingredient disclosure, and traceability, making them indispensable in modern packaging ecosystems.

One of the major restraints affecting the global self-adhesive labels industry is the fluctuation in prices of raw materials such as paper, plastic films, adhesives, and release liners. These materials are heavily influenced by crude oil prices, supply chain disruptions, geopolitical uncertainties, and changing environmental regulations. Sudden increases in material costs directly impact manufacturing expenses and profit margins for label producers, particularly small and medium-sized companies with limited pricing flexibility. In addition, the growing shift away from conventional plastic-based materials toward sustainable alternatives often involves higher production costs and investment requirements, creating pricing pressure across the value chain and limiting adoption in price-sensitive markets.

A major challenge in the self-adhesive labels industry is the difficulty associated with recycling and waste management of label components, particularly release liners and adhesive residues. Traditional self-adhesive labels often use silicone-coated liners and synthetic adhesives that complicate recycling processes by contaminating packaging waste streams or reducing the recyclability of containers. As governments and consumers increasingly demand environmentally responsible packaging, manufacturers face pressure to redesign labels that maintain strong adhesion and performance while also being compatible with recycling systems. Achieving the right balance between functionality, regulatory compliance, sustainability, and cost-effectiveness remains a critical challenge for industry participants, especially as global brands pursue ambitious zero-waste and circular packaging targets.

Composition Insights

Adhesives held the largest market share of 85% in 2023. Hot melt adhesives are preferred for their strong bonding capabilities and quick setting times, making them suitable for high-speed production lines. Acrylic adhesives are witnessing the fastest-growing CAGR due to their versatility and superior performance in various environmental conditions, including resistance to UV light and chemicals.

Among Facestock Paper-based is the fastest growing due to its cost-effectiveness and versatility. It is widely used in various industries, including food and beverages and retail. Plastic facestock is also driven by its durability and aesthetic appeal. It is particularly popular in personal care and household products.

Type Insights

Release liners segment dominated the self-adhesive labels market and accounted for largest revenue share of over 74% in 2023. Release liners hold the highest market share due to their wide usage across multiple industries for their reliability and ease of use. They also have the fastest-growing CAGR as innovations in liner materials and recycling processes boost their appeal.

Linerless labels are gaining traction due to their eco-friendly nature, as they eliminate the waste associated with release liners. Their market share is growing as companies seek sustainable labeling solutions.

Printing Technology Insights

Flexography holds the highest market share due to its cost-effectiveness and versatility in printing on various substrates. It also has the fastest-growing CAGR, driven by advancements in flexographic printing technology that improve print quality and efficiency.

Digital printing is gaining popularity for its ability to produce high-quality, customized labels with shorter turnaround times. The segment is growing rapidly due to increasing demand for personalized packaging and short-run label production.

Nature Insights

Permanent labels segment held the largest market share in 2023, due to their strong adhesive properties, making them ideal for products requiring long-term durability. They also exhibit the fastest-growing CAGR as industries such as pharmaceuticals and logistics demand reliable, tamper-proof labeling solutions.

Removable labels are used for temporary applications, while repositionable labels cater to needs where the label position may need adjusting. Both segments are growing steadily as they find applications in retail and logistics.

Application Insights

The food and beverages segment held the largest market share of over 54% in 2023, due to the extensive use of labels for product information, branding, and regulatory compliance. The demand for labels in this sector is driven by the need for product differentiation and the growing trend of packaged and convenience foods.

")

The pharmaceuticals segment is the fastest-growing due to stringent regulatory requirements for labeling, including information on dosage, expiration dates, and safety instructions. The increasing demand for over-the-counter drugs and the growth of the pharmaceutical industry contribute to this segment's rapid expansion.

Other applications include automotive, logistics, and industrial products, where labels are used for tracking, inventory management, and compliance with industry standards. This segment is also witnessing growth due to the increasing need for efficient and reliable labeling solutions across various industries.

Regional Insights

North America holds the largest market share in the global market. The region's dominance can be attributed to the robust growth of industries such as food and beverages, pharmaceuticals, and retail. The increasing demand for packaged goods and stringent labeling regulations are driving market growth. Moreover, the presence of leading market players and the adoption of advanced labeling technologies contribute to the region's significant market share.

Asia Pacific Self-Adhesive Labels Market Trends

The Asia Pacific region is the fastest-growing market for self-adhesive labels. Rapid industrialization, urbanization, and increasing consumer spending are key factors fueling the market's expansion.

Self-adhesive labels market in China is growing on account of rising e-commerce sector which also boosts the demand for efficient labeling solutions. Additionally, the increasing adoption of packaged and convenience foods, along with rising awareness about product information and safety, contributes to the region's rapid growth.

Europe Self-Adhesive Labels Market Trends

Europe is a significant market for self-adhesive labels, driven by stringent environmental regulations and a strong focus on sustainability. The European Union's regulations on packaging waste and recycling are pushing manufacturers to adopt eco-friendly labeling solutions. Companies in the region are increasingly investing in sustainable materials and technologies to meet regulatory requirements and consumer preferences for environmentally responsible products. The market growth in Europe is also supported by advancements in labeling technologies and the presence of a well-established packaging industry.

Central & South America Self-adhesive Labels Market Trends

The market in Central and South America is experiencing steady growth, driven by the expanding food and beverage, retail, and pharmaceutical sectors. The region's market growth is supported by increasing consumer awareness about product information and safety. Additionally, the growing middle-class population and rising disposable incomes are driving the demand for packaged goods, further boosting the need for labeling solutions. Countries like Brazil and Argentina are key contributors to the market's growth in this region, with increasing investments in the packaging industry and the adoption of advanced labeling technologies.

Key Self-Adhesive Labels Company Insights

The market is highly fragmented with the presence of a significant number of companies. Self-adhesive labels industry has been witnessing a significant number of new product launches and expansions over the past few years. This can be attributed to the circular economy initiatives, innovation in materials and technologies, and consumer demand for sustainability.

-

In May 2024, Beontag launched self-adhesive labels in the Latin America wine market. These new self-adhesive labels comprise of 40% of grass fiber which is combined with FSC certified cellulose.

-

In February 2024, Coveris acquired Czech Republic based self-adhesive label producer, S&K LABEL. Since Coveris is also engaged in manufacturing of self-adhesive labels, this strategic acquisition will provide Coveris to expand its geographical presence in Central & Eastern Europe.

-

In November 2023, UK based premium self-adhesive labels manufacturer, Royston Labels, was acquired by Autajon Group which is engaged in manufacturing of labels, set-up boxes, and folding cartons. This acquisition is a part of Autajon Group’s expansion plan to grow is presence in the UK market.

Key Self-Adhesive Labels Companies:

The following are the leading companies in the self-adhesive labels market. These companies collectively hold the largest market share and dictate industry trends.

- 3M

- Avery Dennison Corporation

- LINTEC Corporation

- Mondi

- UPM

- Optimum Group

- HERMA

- AKO GROUP

- Advance Marks & Labels Pvt Ltd.

- Consolidated Label Co

- Nova Label

- Elite Labels

- StickyLine

- Rebsons Labels

- S&K LABEL spol. s r.o.

- Multipack Labels

- Swati Polypack

- Valley Forge Tape & Label

- Coast Label Company

- Jiangmen Hengyuan Label Co.Ltd.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: 3M; Avery Dennison Corporation; LINTEC Corporation; Mondi; UPM; HERMA

- Invest heavily in sustainable label materials, linerless technologies, recyclable adhesives, and RFID-enabled smart labeling solutions.

- Expand global production facilities and strengthen partnerships with FMCG, pharmaceutical, logistics, and e-commerce companies.

- Focus on digital printing compatibility, high-performance industrial labels, and automation-friendly labeling systems.

- Strong global brand recognition and diversified customer base across packaging, healthcare, retail, logistics, and industrial sectors.

- Advanced technological capabilities in adhesive chemistry, sustainable materials, and smart labeling innovations.

- Large-scale manufacturing and supply chain networks support cost competitiveness and global market penetration.

- High operational and raw material costs due to dependence on specialty chemicals, paper pulp, and petrochemical-based films.

- Regulatory pressure related to recyclability, plastic waste reduction, and environmental compliance increases operational complexity.

- Large organizational structures may reduce agility in addressing niche regional demands and rapidly evolving customization trends

Emerging Players: Optimum Group; AKO GROUP; Advance Marks & Labels Pvt Ltd.; Consolidated Label Co; Nova Label; Elite Labels; StickyLine; Rebsons Labels; S&K LABEL spol. s r.o.; Multipack Labels; Swati Polypack; Valley Forge Tape & Label; Coast Label Company; Jiangmen Hengyuan Label Co. Ltd.

- Focus on customized and short-run label production for food, beverage, cosmetics, pharmaceuticals, and local manufacturing industries.

- Offer flexible printing solutions including digital labels, barcode labels, tamper-evident labels, and promotional packaging labels.

- Strengthen regional distribution networks and customer-centric services for faster turnaround and low-volume orders.

- Greater flexibility in customization, design modifications, and quick-response manufacturing for regional clients.

- Lower operational complexity allows faster adaptation to changing customer preferences and packaging trends.

- Strong presence in niche and regional markets with personalized customer service and competitive pricing strategies.

- Limited global presence and smaller production capacities compared to multinational labeling companies.

- Dependence on regional demand and limited economies of scale may impact profitability during raw material price fluctuations.

- Lower investment capabilities in advanced sustainable technologies, RFID integration, and large-scale automation systems.

Self-Adhesive Labels Market Report Scope

Report Attribute

Details

Market size in 2023

USD 50.5 billion

Estimated market size in 2026

USD 57.1 billion

Projected market size by 2030

USD 71.8 billion

Growth rate

CAGR of 5.4% from 2024 to 2030

Historical data

2018 - 2022

Forecast period

2024 - 2030

Quantitative units

Revenue in USD million/billion, Volume in Million Square Meter, and CAGR from 2024 to 2030

Report coverage

Volume Forecast, Revenue forecast, competitive landscape, growth factors and trends

Segments covered

Composition, type, technology, nature, application, region

Regional scope

North America; Europe; Asia Pacific; Central & South America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Germany; France; UK; Italy; Spain; China; India; Japan; South Korea; Australia; Brazil; Argentina; Saudi Arabia; South Africa; UAE

Key companies profiled

3M; Avery Dennison Corporation; LINTEC Corporation; Mondi; UPM; Optimum Group; HERMA; AKO GROUP; Advance Marks & Labels Pvt Ltd.; Consolidated Label Co; Nova Label; Elite Labels; StickyLine; Rebsons Labels; S&K LABEL spol. s r.o.; Multipack Labels; Swati Polypack; Valley Forge Tape & Label; Coast Label Company; Jiangmen Hengyuan Label Co.Ltd.

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Self-Adhesive Labels Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global self-adhesive labels market report based on composition, type, technology, nature, application, and region:

-

Composition Outlook (Revenue, USD Million; Volume, Million Square Meter, 2018 - 2030)

-

Facestock

-

Paper

-

Plastic

-

-

Adhesive

-

Hot melt

-

Acrylic

-

-

-

Type Outlook (Revenue, USD Million; Volume, Million Square Meter, 2018 - 2030)

-

Release Liner

-

Linerless

-

-

Technology Outlook (Revenue, USD Million; Volume, Million Square Meter, 2018 - 2030)

-

Flexography

-

Digital Printing

-

Letterpress

-

Screen Printing

-

Gravure

-

Offset

-

-

Nature Outlook (Revenue, USD Million; Volume, Million Square Meter, 2018 - 2030)

-

Permanent

-

Removable

-

Repositionable

-

-

Application Outlook (Revenue, USD Million; Volume, Million Square Meter, 2018 - 2030)

-

Food & Beverages

-

Pharmaceuticals

-

Consumer Durables

-

Home & Personal Care

-

Other Applications

-

-

Regional Outlook (Revenue, USD Million; Volume, Million Square Meter, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation

Detailed analysis of the global self-adhesive labels market across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, including country-level packaging demand trends, retail and e-commerce expansion, pharmaceutical labeling requirements, food & beverage packaging growth, sustainability regulations, recycling infrastructure, raw material availability, and regional manufacturing outlook.

Identify high-growth regional markets and emerging label manufacturing hubs. Support region-specific expansion strategies and production planning. Enable understanding of regional sustainability trends, labeling regulations, consumer packaging preferences, and competitive intensity across end-use industries.

Cross-Segmentation

Detailed market segmentation analysis by material type, adhesive type, label type, printing technology, application, end-use industry, and distribution channel, including volume and value analysis across major regions and countries.

Enable identification of high-growth product categories and emerging labeling applications. Support targeted product innovation, investment prioritization, and market entry strategies. Help understand evolving demand patterns across food & beverage, pharmaceuticals, logistics, personal care, retail, and industrial packaging sectors.

Trade Assessment

Analysis of global trade flows, import-export trends, paper and film raw material supply dynamics, adhesive material trade patterns, tariff structures, trade regulations, and regional supply chain dependencies impacting the self-adhesive labels market.

Support supply chain risk assessment and sourcing strategy development. Identify major exporting and importing countries, trade bottlenecks, and regional supply opportunities. Enable informed procurement diversification, raw material planning, and international expansion strategies.

Frequently Asked Questions About This Report

The global Self-Adhesive labels market size was valued at USD 50.5 billion in 2023 and is estimated at USD 57.1 billion for 2026.

The global Self-Adhesive labels market is expected to grow at a CAGR of 5.4% from 2024 to 2030, reaching USD 71.8 billion by 2030.

North America dominated with a 36.4% revenue share in 2023.

The global market for self-adhesive labels is growing significantly due to the rising demand for packaged goods, especially in the food and beverage, personal care, and pharmaceutical sectors. As consumers look for convenience and product details, the requirement for top-notch, informative, and visually appealing labels is increasing.

Key players include 3M; Avery Dennison Corporation; LINTEC Corporation; Mondi; UPM; Optimum Group; HERMA; AKO GROUP; Advance Marks & Labels Pvt Ltd.; Consolidated Label Co; Nova Label; Elite Labels; StickyLine; Rebsons Labels; S&K LABEL spol. s r.o.; Multipack Labels; Swati Polypack; Valley Forge Tape & Label; Coast Label Company; Jiangmen Hengyuan Label Co.Ltd.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.