- Home

- »

- Next Generation Technologies

- »

-

Smart Stadium Market Size And Share Report, 2026-2033GVR Report cover

![Smart Stadium Market (2026 - 2033)Report]()

Smart Stadium Market (2026 - 2033)

Size, Share & Trends Analysis Report By Offering (Infrastructure, Hardware, Software, Services), By Installation (Retrofit, New Installation), By Deployment (On Premise, Cloud), By Region (North America, Europe, MEA), And Segment Forecasts

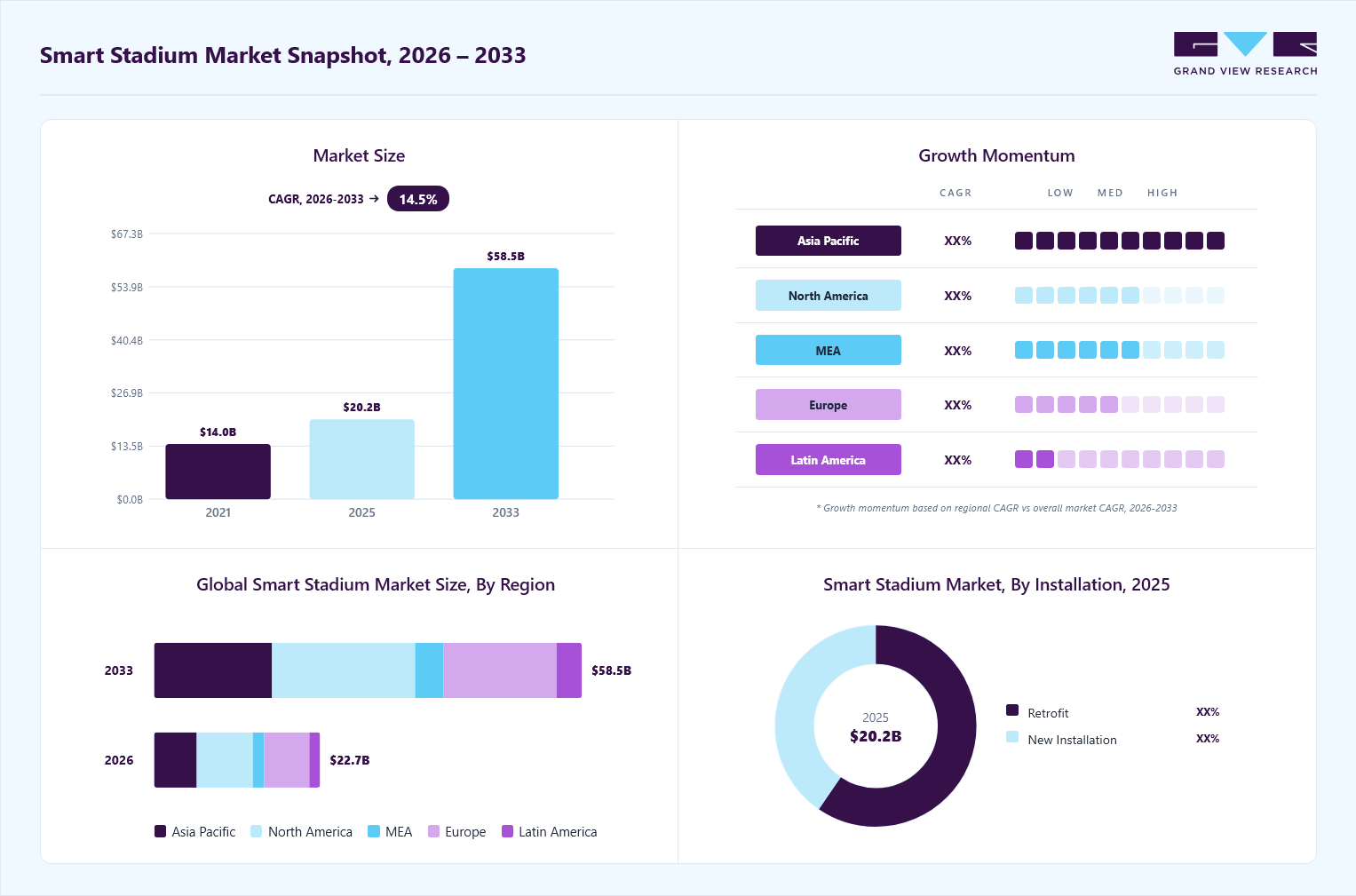

Market Size, 2025

$20.2BMarket Estimate, 2026

$22.7BMarket Forecast, 2033

$58.5BCAGR, 2026–2033

14.5%Smart Stadium Market Summary

The global smart stadium market size was valued at USD 20.2 billion in 2025 and is projected to grow from USD 22.7 billion in 2026 to USD 58.5 billion by 2033, growing at a CAGR of 14.5% from 2026 to 2033. The market in North America dominated with a revenue share of 33.9% in 2025. The market is driven by the rising demand for immersive fan experiences enabled by 5G connectivity, IoT-enabled infrastructure, and AR/VR technologies.

Key Market Trends & Insights

- By offering: The infrastructure segment led the market with the largest revenue share of 39.8% in 2025.

- By installation: The retrofit segment led the market with the largest revenue share of 59.5% in 2025.

Regional Highlights

- Largest regional market: North America (33.9% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 20.2 Billion

- Estimated market size in 2026: USD 22.7 Billion

- Projected market size by 2033: USD 58.5 Billion

- CAGR (2026-2033): 14.5%

Advancements in AI-driven analytics and automation optimize operations, from crowd management to energy efficiency, while sustainability mandates and safety innovations like biometric systems further accelerate market adoption. In addition, revenue opportunities from dynamic pricing, targeted advertising, and partnerships with tech giants is expected to drive investments in next-generation smart stadium industry solutions worldwide.Smart stadiums are increasingly leveraging technologies such as IoT-enabled devices, AI-based systems, and cloud computing to automate operations, crowd management, and fan experience personalization. The convergence of smart ticketing systems, digital signage, real-time analytics, and interactive apps is enhancing the fan experience with personalized services such as customized recommendations, instant seat upgrades, and on-demand services. These factors are expected to drive the smart stadium industry expansion.

")

Additionally, energy-efficient systems such as smart lighting and heating are becoming more common for stadium operators, while data analytics are being utilized to maximize energy usage. The 5G network is also having a transformative impact by allowing uninterrupted, high-speed communication within and between stadiums, improving both operational effectiveness and fan experience. These trends are driving the smart stadium industry's growth.

Furthermore, augmented reality (AR) and virtual reality (VR) are two of the most promising technological trends changing the fan experience. AR is enhancing the in-stadium experience by offering supplementary layers of information on mobile phones, including interactive maps, real-time statistics, and player data. VR, however, provides fans with the chance to watch games from unusual angles or even at home, placing fans in closer proximity to the action. These technologies are changing the way fans engage with their favorite teams and players, providing a richer, more dynamic experience, thereby driving the smart stadium industry expansion.

Moreover, regulatory pressures, technological innovation, and increasing consumer demand are all driving the fast development of smart stadiums. With the increasing emphasis on sustainability, cost savings, and operational efficiency, smart stadiums are poised to transform the sports and entertainment sector, which is expected to further boost the smart stadium market expansion in the coming years.

Market Dynamics

Smart stadium solutions are gaining strong traction as they offer enhanced fan engagement features such as mobile ticketing, real-time navigation, personalized content delivery, contactless payments, smart parking, and AI-driven crowd management. These platforms enable venue operators to deliver seamless and immersive spectator experiences while improving operational efficiency through connected infrastructure and data-driven decision-making. The growing demand for superior in-stadium experiences, coupled with increasing investments in 5G connectivity, IoT-enabled devices, and digital venue modernization initiatives, is expected to continue driving growth in the smart stadium market.

The modern venue operators are increasingly investing in connected technologies that enhance the overall spectator experience through personalized services, real-time information access, mobile applications, and interactive digital content. Smart stadium solutions enable visitors to access seamless ticketing, wayfinding assistance, in-seat ordering, and customized event experiences, helping operators strengthen audience satisfaction while increasing event participation and loyalty.

The widespread deployment of 5G networks, IoT sensors, artificial intelligence, and advanced analytics is further transforming venue operations by enabling real-time engagement and personalized interactions. Stadium administrators are leveraging these technologies to deliver targeted promotions, live event updates, and enhanced digital experiences throughout the venue. As consumer expectations continue to evolve toward convenience and connectivity, investments in intelligent venue infrastructure are becoming a strategic priority for sports and entertainment facilities worldwide.

Implementing advanced stadium technologies requires a significant upfront investment in networking infrastructure, connectivity systems, surveillance equipment, cloud platforms, and integrated management software. Many venue owners face financial constraints when evaluating large-scale modernization projects, particularly in regions where sports infrastructure budgets remain limited. These high deployment costs can delay technology adoption and restrict modernization initiatives among smaller facilities.

Beyond installation expenses, operators must allocate ongoing resources for software upgrades, cybersecurity measures, equipment maintenance, and training for the technical workforce. The complexity of integrating multiple digital systems into existing venue environments often creates additional operational challenges. Concerns about return on investment and long implementation timelines may discourage some stakeholders from pursuing comprehensive smart-venue transformation projects, thereby limiting broader market adoption.

The increasing availability of real-time operational and behavioral data is creating new revenue-generation avenues for venue operators. Smart stadium platforms enable organizations to collect valuable insights related to attendee preferences, purchasing habits, movement patterns, and engagement levels. These analytics support the development of targeted advertising campaigns, premium digital services, and personalized offerings that improve commercial performance during live events.

Advanced data intelligence capabilities allow operators to optimize sponsorship programs, dynamic pricing strategies, concession sales, and customer engagement initiatives. Businesses partnering with venues can utilize audience insights to deliver highly relevant promotions and experiences, improving marketing effectiveness. As digital ecosystems become more sophisticated, data-centric monetization strategies are expected to become an increasingly important competitive differentiator for venue operators seeking diversified revenue streams.

Market Concentration & Characteristics

The smart stadium market is moderately concentrated, with a mix of leading global technology providers, telecommunications companies, venue infrastructure specialists, and emerging sports technology firms. The market is expanding due to increasing investments in connected venue infrastructure, rising demand for enhanced spectator experiences, and growing adoption of digital technologies across sports and entertainment facilities. Strategic partnerships among stadium operators, software developers, and sports organizations are becoming increasingly common as stakeholders focus on improving operational efficiency and enhancing fan engagement capabilities. Continuous investments in artificial intelligence, IoT-enabled monitoring systems, cloud-based venue management platforms, advanced surveillance technologies, and real-time analytics solutions are emerging as key competitive strategies across the market.

The market is characterized by a very high level of innovation, driven by the integration of 5G connectivity, AI-powered crowd analytics, immersive fan engagement applications, and smart facility management technologies. The industry is witnessing moderate merger and acquisition activity as technology providers seek to expand their digital infrastructure capabilities and strengthen their venue management portfolios. Competition from conventional stadium management systems and standalone operational technologies remains moderate, though demand for integrated digital venue ecosystems continues to grow among entertainment venues. Growing investments in contactless services, smart security infrastructure, sustainability-focused building automation, augmented reality experiences, and data-driven venue monetization platforms are expected to further support development across the smart stadium market.

Analyst Perspective

The smart stadium market is positioned at the convergence of connected infrastructure expansion, increasing demand for immersive fan experiences, and the growing digital transformation of sports and entertainment venues through AI, IoT, cloud computing, and advanced analytics. The strongest long-term competitive moat, however, will belong to the provider that can seamlessly integrate venue operations, crowd intelligence, smart security, personalized fan engagement, digital ticketing, and data-driven monetization into a unified stadium ecosystem, transforming traditional venues into intelligent, always-connected environments that enhance operational efficiency, maximize revenue opportunities, and strengthen visitor engagement across global sports and entertainment facilities.

Offering Insights

Based on offering, the infrastructure segment led the market with the largest revenue share of 39.8% in 2025 and is expected to grow at a considerable CAGR over the forecast period, driven by the increasing demand for advanced technologies to enhance fan experiences and operational efficiency. Stadiums are integrating IoT sensors, AI analytics, and 5G connectivity to optimize crowd management, security, and energy usage. Additionally, the need for sustainable practices and improved facility management is propelling investments in smart infrastructure solutions. These advancements enable stadiums to provide personalized services, real-time data analytics, and efficient resource utilization, thereby driving segmental growth.

The software segment is expected to witness the highest CAGR of over 15% from 2025 to 2030, fueled by the growing reliance on digital solutions for managing various stadium functions. Software platforms enable seamless integration of services such as ticketing, crowd management, video surveillance, and data analytics, enhancing the overall fan experience. Additionally, the increasing adoption of cloud-based solutions offers scalability, flexibility, and cost-effectiveness, further driving the demand for software in smart stadiums.

Installation Insights

Based on installation, the retrofit segment led the market with the largest revenue share of 59.5% in 2025, driven by the growing need to modernize existing stadiums in a cost-effective manner without complete reconstruction. Many older venues are being upgraded with smart technologies-such as advanced security systems, improved connectivity, and energy-efficient solutions-to enhance fan experience and operational performance. This approach allows operators to extend the life of their infrastructure while meeting the rising expectations for digital engagement and sustainability, all while minimizing disruption and investment compared to building new facilities.

The new installation segment is expected to witness a significant CAGR from 2025 to 2030, largely driven by the growing demand to host mega-events such as the FIFA World Cup 2034 and the Asian Games, where high-tech incorporation is a competitive advantage for new stadiums. New stadiums, such as SoFi Stadium in the US and Lusail Stadium in Qatar, are at the forefront of providing cutting-edge amenities, such as embedded 5G Distributed Antenna Systems for frictionless connectivity, sustainability elements such as energy-efficient architecture, and advanced seating and fan engagement systems. Such advancements are accelerating growth in the new installation segment, as the demand for technologically advanced, eco-conscious, and immersive stadium experiences continues to rise globally.

Deployment Insights

The on-premise segment accounted for the largest market share in 2025, driven by the demand for richer fan experiences, including high-speed internet connectivity, real-time analytics, and effortless connectivity within stadiums. On-premise technologies like high-definition video screens, intelligent seating, and built-in Wi-Fi systems are becoming a part of state-of-the-art stadiums. These technologies not only enhance fan engagement but also optimize operations, increase revenue through targeted advertising, and improve security measures. The growing use of Internet of Things (IoT) devices, smart ticketing, and data-based solutions also fuels the growth of the segment further

The cloud segment is expected to witness a significant CAGR from 2026 to 2033, owing to its scalability, flexibility, and cost-effectiveness. Cloud-based solutions enable stadiums to handle large amounts of data, especially during major events, without the need for costly physical infrastructure. These platforms allow real-time data processing, which is essential for enhancing fan engagement, improving operations, and offering personalized experiences. Cloud services also enable seamless integration with emerging technologies such as AI, 5G, and AR/VR, further enhancing the stadium experience and boosting segmental growth.

Regional Insights

North America dominated the smart stadium market with the largest revenue share of 33.9% in 2025, primarily driven by increasing demand for enhanced fan engagement and digital experiences. Stadiums are integrating advanced technologies like IoT, 5G, and AI to improve operational efficiency and safety. There is a rising adoption of mobile ticketing, contactless payments, and smart seating solutions, offering convenience and reducing physical touchpoints. Real-time data analytics is being widely used to manage crowd control, security, and resource optimization.

U.S. Smart Stadium Market Trends

The smart stadium market in the U.S. held the largest share in the North America region in 2025, driven by the integration of IoT, AI, and 5G networks. Stadiums are increasingly using facial recognition for security and contactless entry systems to enhance fan experience. Data analytics is being leveraged to optimize crowd management and personalize fan engagement. The rise of mobile apps for ticketing, concessions, and in-seat delivery is transforming the spectator experience.

Europe Smart Stadium Market Trends

Europe smart stadium market is expected to grow at a CAGR of over 13% from 2025 to 2030. This growth is driven by the region’s strong sports culture and technological innovation. Stadiums are increasingly adopting integrated systems for crowd management, digital signage, and interactive fan experiences. Advanced connectivity solutions, including 5G and Wi-Fi 6, are ensuring seamless digital interactions. AI-driven analytics help optimize event operations and improve security protocols.

The UK smart stadium market is expected to grow at a significant rate in the coming years. The UK is at the forefront of smart stadium innovation, with Premier League clubs investing heavily in technology. AI-powered crowd analytics are being used to enhance safety and optimize stadium operations. Mobile apps with wayfinding features and real-time updates are improving fan experience. The adoption of renewable energy sources, such as solar panels, is making stadiums more sustainable.

Germany smart stadium market is fueled by the region’s strong focus on integrating smart technologies to improve operational efficiency and fan satisfaction. Bundesliga stadiums are adopting IoT sensors to monitor crowd density and ensure safety. High-speed internet connectivity is being prioritized to support live streaming and interactive fan experiences. Smart parking systems are reducing congestion and improving access to stadiums.

Asia Pacific Smart Stadium Market Trends

Asia Pacific smart stadium market is expected to grow at the highest CAGR of over 15% from 2025 to 2030, driven by the increasing investments in digital infrastructure. Countries are adopting advanced technologies like facial recognition, cashless payments, and interactive displays. High-speed 5G networks and IoT devices are enhancing operational efficiency and fan engagement, and real-time analytics are optimizing crowd flow and event management.

Japan smart stadium market is gaining traction, fueled by its technological expertise to develop state-of-the-art smart stadiums. Robotics and automation are being used for cleaning, maintenance, and customer service. Stadiums are adopting cashless payment systems and digital ticketing to streamline operations. Japan is also prioritizing sustainability, with smart energy systems and eco-friendly materials. The upcoming Olympics and other international events are accelerating the adoption of smart technologies.

China smart stadium market is rapidly expanding, driven by government initiatives and tech advancements. AI-powered facial recognition systems are widely used for security and access control. Stadiums are integrating 5G networks to enable ultra-fast data transmission and enhance live streaming. Mobile apps with AR features provide interactive experiences for fans.

Key Smart Stadium Company Insights

Some key players operating in the market include Cisco Systems, Inc. and IBM Corporation, among others

-

Cisco Systems, Inc. is a prominent player in designing, manufacturing, and selling Internet Protocol-based networking products and services, with a presence across the globe. The company operates through diverse segments, including networking, security, collaboration, and observability, catering to businesses of all sizes, public institutions, governments, and service providers. Cisco’s product portfolio features advanced switching solutions for campus and data center environments, enterprise routing for secure network connectivity, wireless products for seamless mobility, and robust security solutions like network security and threat intelligence.

-

International Business Machines Corporation (IBM) is a prominent player in hybrid cloud, artificial intelligence (AI), and consulting services. The company operates through key business segments, including Software, Consulting, Infrastructure, and Financing. In the smart stadium market, IBM harnesses its advanced capabilities in cloud computing, AI, and the Internet of Things (IoT). The company’s products, such as IBM Watsonx, IBM Storage, and IBM Maximo, the company provide real-time data analytics, effective crowd management, and seamless connectivity, transforming traditional venues into sophisticated digital ecosystems.

GP Smart Stadium and Barco NV are some emerging market participants in the smart stadium market.

-

GP Smart Stadium is an independent company specializing in consultancy services and advanced embedded solutions for stadiums, arenas, and entertainment venues. The company offers a multidisciplinary approach that integrates strategic, marketing, and organizational elements, facilitating turnkey solutions that are durable and valuable for all parties involved. Their extensive network includes collaborations with high-tech companies, construction firms, security providers, and energy and climate control producers, ensuring comprehensive solutions for sports and cultural venues worldwide.

-

Barco NV is a Belgian technology company specializing in digital projection and imaging technology, focusing on entertainment, enterprise, and healthcare markets. Their product portfolio includes DLP projectors, LED displays, and connectivity platforms. In the smart stadium market, Barco leverages its expertise in visualization solutions to enhance fan engagement and operational efficiency. Their high-resolution projectors and LED displays are designed for large venues, providing immersive visual experiences for spectators.

Key Smart Stadium Companies

The following key companies have been profiled for this study on the smart stadium market.

-

Cisco Systems, Inc.

-

Fujitsu

-

GP Smart Stadium

-

Huawei Technologies Co., Ltd.

-

IBM Corporation

-

Intel Corporation

-

Mapsted Corp.

-

NEC Corporation

-

Johnson Controls

-

NXP Semiconductors

-

Schneider Electric

-

Telefonaktiebolaget LM Ericsson

-

CommScope Holding Company, Inc.

-

Corning Incorporated

-

Hewlett Packard Enterprise Company

-

Belden Inc.

-

Extreme Networks, Inc.

-

Barco NV

-

Daktronics, Inc.

-

KORE Wireless Group

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Cisco Systems, Inc., Huawei Technologies Co., Ltd., IBM Corporation)

- Focus on expanding integrated smart stadium ecosystems through connectivity, security, and analytics partnerships.

- Invest heavily in digital infrastructure and AI platforms for intelligent venue operations.

- Strong global presence, established venue relationships, and extensive smart infrastructure expertise.

- Ability to deliver secure, end-to-end solutions across complex stadium environments.

- Dependence on legacy venue contracts can slow the deployment of emerging technologies.

- Large organizational structures may reduce agility against specialized stadium technology providers.

Emerging Players (GP Smart Stadium, Barco NV)

- Focus on developing innovative fan engagement platforms through strategic technology collaborations.

- Invest in AI, IoT, and cloud solutions to optimize smart venues.

- Strong innovation capabilities enable rapid deployment of next-generation stadium technologies.

- Ability to provide flexible, specialized solutions tailored to modern venue requirements.

- Limited financial resources may constrain the deployment of large-scale stadiums.

- A smaller customer base can restrict market visibility and competitive positioning.

Recent Developments

-

In February 2025, Barco's ClickShare partnered with Neat to enhance meeting room collaboration. Neat Bar 2 and Neat Bar Pro received ClickShare certification, enabling effortless wireless conferencing. This collaboration ensures seamless end-to-end experiences for ClickShare and Neat customers, reinforcing Barco's focus on improving professional environments.

-

In January 2025, Hewlett Packard Enterprise (HPE) faced an antitrust lawsuit from the U.S. Department of Justice over its proposed USD14 billion acquisition of Juniper Networks. The Justice Department argued that the merger would reduce competition and innovation by creating a combined entity controlling 70% of the wireless networking market. HPE and Juniper planned to defend the deal in court, claiming it would benefit customers and strengthen competition against global rivals.

-

In December 2024, Daktronics announced a new LED display installation at Grayson Stadium, home of the Savannah Bananas, set to debut in 2025. The display, over 26 feet high and 47 feet wide, offers variable content zoning for live video, replays, game info, and sponsorship messages. This upgrade aims to enhance the fan experience with dynamic and engaging visual content.

Smart Stadium Market Report Scope

Report Attribute

Details

Market size in 2025

USD 20.2 billion

Estimated market size in 2026

USD 22.7 billion

Projected market size by 2033

USD 58.5 billion

Growth rate

CAGR of 14.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Offering, installation, deployment, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Germany; U.K.; France; Italy; Spain; China; Japan; India; South Korea; Australia; Brazil; Mexico; Saudi Arabia; South Africa; UAE

Key companies profiled

Cisco Systems, Inc.; Fujitsu; GP Smart Stadium; Huawei Technologies Co., Ltd.; IBM Corporation; Intel Corporation; Mapsted Corp.; NEC Corporation; Johnson Controls; NXP Semiconductors; Schneider Electric; Telefonaktiebolaget LM Ericsson; CommScope Holding Company, Inc.; Corning Incorporated; Hewlett Packard Enterprise Company; Belden Inc.; Extreme Networks, Inc.; Barco NV; Daktronics, Inc.; KORE Wireless Group

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Smart Stadium Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest technological trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global smart stadium market report based on offering, installation, and deployment:

-

Offering Outlook (Revenue, USD Million, 2021 - 2033)

-

Infrastructure

-

Distributed Antenna Systems (DAS)

-

Fiber Optics and Network Infrastructure

-

High-Density Wi-Fi and Connectivity

-

Surveillance & Security Systems

-

Access Control Systems

-

Emergency Response Systems

-

Power Management Systems

-

Others

-

-

Hardware

-

Digital Signage

-

Audio Systems

-

Smart Lighting

-

IoT Sensors

-

Others

-

-

Software

-

Stadium & Public Security

-

Building Automation

-

Event Management

-

Fan Engagement Platforms

-

Real-Time Analytics & Data Management Platforms

-

Others

-

-

Services

-

Professional Services

-

Design & Consulting

-

Integration & Installation

-

Others

-

-

Managed Services

-

-

-

Installation Outlook (Revenue, USD Million, 2021 - 2033)

-

New Installation

-

Retrofit

-

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

On-premise

-

Cloud

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Mexico

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

UAE

-

-

Research Methodology

Segment Definition

Segment - Offering

Revenue capture definition

Infrastructure

Revenue is generated through the deployment of foundational stadium technologies, including high-speed connectivity, 5G networks, data centers, and IoT infrastructure. These systems support seamless communication, operational efficiency, and digital service delivery across venues.

Hardware

Revenue is captured through sales of surveillance cameras, sensors, digital displays, access control devices, networking equipment, and smart kiosks. Hardware solutions enable real-time monitoring, security management, and enhanced spectator experiences.

Software

Revenue is generated through stadium management platforms, analytics solutions, digital ticketing systems, crowd management applications, and fan engagement software. These platforms help operators optimize venue performance and deliver personalized visitor experiences.

Services

Revenue is captured through consulting, system integration, maintenance, managed services, and technical support. Service providers assist venue operators in implementing, managing, and optimizing smart stadium technologies throughout their lifecycle.

Segment - Installation

Revenue capture definition

New Installation

Revenue is generated through smart technology deployments in newly constructed stadiums and entertainment venues. Investments include integrated connectivity, security systems, digital ticketing, IoT infrastructure, and fan engagement platforms designed to create fully connected venue ecosystems.

Retrofit

Revenue is captured through upgrading existing stadiums with modern digital infrastructure, including wireless networks, smart surveillance, digital signage, and venue management systems. These projects improve operational efficiency and spectator experiences without requiring complete facility reconstruction.

Segment - Deployment

Revenue capture definition

On-premise

Revenue is generated through locally hosted smart stadium platforms, security solutions, and operational management systems. This model provides venue operators with greater control over data, system customization, and critical infrastructure management.

Cloud

Revenue is captured through cloud-based stadium management, analytics, fan engagement, and ticketing platforms. Cloud deployment enables scalable operations, real-time insights, remote accessibility, and lower infrastructure costs for venue operators.

Estimation Model

Venue Infrastructure Layer

Digital Readiness Layer

Adoption Layer

Revenue Generation Layer

Which venues have the required technology foundation?

Which venues have the required technology foundation?

Which venues actively deploy smart stadium technologies?

How much revenue is generated from smart stadium deployments?

Identify the total addressable venue base by estimating the number of sports stadiums, arenas, entertainment venues, multi-purpose complexes, and large event facilities across target regions. This establishes the potential market for smart stadium technologies and digital venue modernization initiatives.

Filter the potential venue base based on the availability of connectivity infrastructure, including high-speed broadband, Wi-Fi networks, 5G coverage, IoT deployment capability, cloud integration readiness, and digital management systems. This determines the technologically addressable market for smart stadium implementation.

Apply adoption rates to digitally ready venues and segment facilities based on implementation of smart ticketing, connected security systems, crowd management platforms, digital signage, fan engagement applications, and intelligent building management solutions. This converts addressable venues into active smart stadium users.

Estimate revenue from software subscriptions, hardware installations, managed services, connectivity solutions, analytics platforms, security systems, digital advertising technologies, and fan engagement applications. Multiply deployed solutions by average spending per venue to derive total market revenue.

Customization Table

Client Request

Customization Delivered

Value Adds

Fan Engagement, Venue Experience & Digital Adoption Trends

Conducted a focused analysis of smart stadium adoption across sports venues and entertainment facilities, covering fan engagement applications, mobile ticketing, contactless payments, in-seat services, venue navigation, personalized content delivery, connected device usage, and digital experience enhancement trends.

Helps stakeholders identify high-value venue segments, evaluate evolving spectator expectations, and assess revenue opportunities across digital services, fan engagement platforms, and connected venue ecosystems.

Venue Operations, Security Strategy & Intelligent Infrastructure Trends

Evaluated market trends related to AI-powered surveillance, crowd management systems, smart access control, intelligent building management, predictive maintenance solutions, IoT-enabled monitoring, real-time analytics platforms, and integrated security technologies supporting modern venue operations.

Provides insights into emerging operational technologies, safety enhancement strategies, resource optimization initiatives, and commercially attractive infrastructure investments that support venue differentiation and long-term competitiveness.

Connected Stadium Infrastructure, Technology Ecosystem & Market Expansion Assessment

Assessed demand for advanced connectivity infrastructure, 5G networks, cloud-based stadium management platforms, digital signage systems, smart parking solutions, technology partnerships, and expansion opportunities across developed and emerging sports infrastructure markets.

Supports investment and expansion strategies by identifying underserved venue modernization opportunities, evaluating digital readiness levels, assessing technology deployment scalability, and strengthening long-term opportunities across the global smart stadium ecosystem.

Frequently Asked Questions About This Report

The global smart stadium market size was estimated at USD 20.2 billion in 2025 and is expected to reach USD 22.7 billion in 2026.

The global smart stadium market is expected to grow at a compound annual growth rate of 14.5% from 2026 to 2033 to reach USD 58.5 billion by 2033.

Some key players operating in the smart stadium market include Cisco Systems, Inc.; Fujitsu Ltd.; IBM Corporation; Intel Corporation; Huawei Technologies Co.; Johnson Controls; NXP Semiconductors; and Telefonaktiebolaget LM Ericsson.

Key factors that are driving the market growth include the growing sports league culture, stringent security norms, and rising significance of improving fan engagement during the sports events.

The Asia Pacific is the fastest-growing region over the forecast period.

The infrastructure segment led with a 39.8% revenue share in 2025, while the software is the fastest-growing segment.

The retrofit segment led with a 59.5 revenue share in 2025, and is the fastest-growing device.

The on-premise segment led with a 55.8% revenue share in 2025, while cloud is the fastest growing segment.

North America dominated the smart stadium market with a share of 33.9% in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.