- Home

- »

- Next Generation Technologies

- »

-

System Integration Market Size, Growth Report, 2026-2033GVR Report cover

![System Integration Market (2026 - 2033)Report]()

System Integration Market (2026 - 2033)

Size, Share & Trends Analysis Report By Services (Infrastructure Integration, Application Integration, Consulting), By Enterprise Size, By End-use, By Region, And Segment Forecasts

Market Size, 2025

$421.4BMarket Estimate, 2026

$467.0BMarket Forecast, 2033

$1,228.6BCAGR, 2026–2033

14.8%System Integration Market Summary

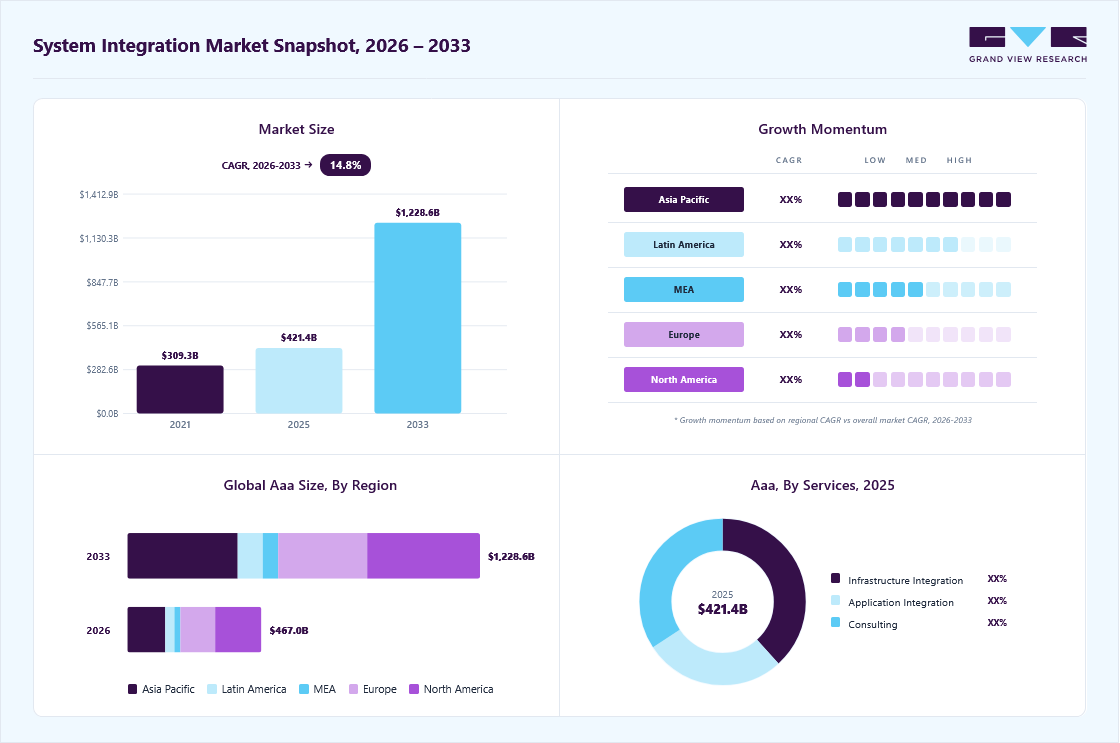

The global system integration market size was valued at USD 421.4 billion in 2025 and is projected to grow from USD 467.0 billion in 2026 to USD 1,228.6 billion by 2033, at a CAGR of 14.8% from 2026 to 2033. North America dominated the global market, accounting for the largest revenue share of 34.8% in 2025, As organizations across industries are modernizing legacy IT environments to enable automation, real-time analytics, omnichannel engagement, and operational agility.

Key Market Trends & Insights

- By services: Infrastructure integration segment held the largest revenue share of 38.2% in 2025.

- By enterprise size: Large enterprises segment accounted for the largest revenue share in 2025.

- By end-use: IT & telecom sector segment is expected to grow at the fastest CAGR from 2026 to 2033.

Regional Highlights

- Largest regional market: North America (34.8% revenue share, 2025)

- By country: The France system integration industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 421.4 Billion

- Estimated market size in 2026: USD 467.0 Billion

- Projected market size by 2033: USD 1,228.6 Billion

- CAGR (2026-2033): 14.8%

System integrators play a central role in orchestrating end-to-end transformation programs-integrating ERP, CRM, SCM, HRMS, and industry-specific platforms with cloud, AI, and IoT ecosystems. Large-scale transformation projects typically require multi-vendor interoperability, middleware deployment, API orchestration, and custom application integration, which directly fuels system integrators' demand.

Enterprises are increasingly adopting hybrid and multi-cloud strategies to balance scalability, compliance, and cost efficiency. Integrating on-premise infrastructure with public and private cloud environments requires architectural redesign, workload migration, containerization, and secure connectivity frameworks. System integrators provide cloud readiness assessments, migration roadmaps, orchestration tools, and post-migration optimization, making cloud transformation a major revenue driver for the market. Fortinet’s 2026 Cloud Security Report indicates that hybrid and multi-cloud strategies have become the norm, with 88% of organizations reporting operations across multiple cloud environments. The study further reveals that 81% of enterprises depend on at least two cloud providers to support mission-critical workloads, underscoring the growing complexity of cloud infrastructures and the increasing need for integrated, cross-platform security frameworks.

")

The deployment of AI/ML models, data lakes, advanced analytics platforms, and robotic process automation (RPA) is driving integration complexity. Enterprises need structured data pipelines, interoperable APIs, edge-to-core data flows, and governance frameworks. System integrators enable AI model deployment within enterprise workflows, integrate analytics engines with operational systems, and ensure data harmonization across silos, accelerating market growth.

Services Insights

The infrastructure integration segment dominated the market and accounted for the revenue share of 38.2% in 2025, driven by the modernization of legacy IT environments and the growing need to unify compute, storage, networking, and security architectures across hybrid and multi-cloud ecosystems. Enterprises are consolidating fragmented data centers, deploying hyperconverged infrastructure (HCI), edge computing nodes, and software-defined networks (SDN) to support AI workloads, real-time analytics, and latency-sensitive applications.

The consulting segment is anticipated to grow at the highest CAGR during the forecast period, driven by the increasing strategic complexity of enterprise digital transformation initiatives. Organizations are no longer seeking only technical deployment support; they require upstream advisory services for IT roadmap development, cloud strategy formulation, AI adoption frameworks, cybersecurity architecture design, data governance models, and enterprise architecture rationalization. As businesses migrate toward hybrid multi-cloud environments, modernize legacy systems, and adopt emerging technologies such as generative AI and automation, the need for feasibility assessments, ROI modeling, vendor selection advisory, compliance alignment, and change management planning has intensified.

Enterprise Size Insights

The large enterprises segment dominated the market and accounted for the largest revenue share in 2025, driven by the scale, complexity, and mission-critical nature of their IT environments. Large organizations typically operate multi-country, multi-business-unit infrastructures that include legacy core systems, hybrid and multi-cloud deployments, advanced cybersecurity frameworks, and industry-specific platforms. Their ongoing digital transformation initiatives, such as ERP modernization, AI-driven analytics integration, enterprise-wide automation, and zero-trust security implementation, require sophisticated architectural redesign and cross-platform interoperability.

The small & medium enterprises segment is expected to grow at a significant CAGR during the forecast period due to accelerated digital adoption supported by cost-effective cloud platforms, low-code ecosystems, and managed services models. SMEs are increasingly implementing integrated ERP, CRM, HRMS, cybersecurity, and e-commerce platforms to enhance operational efficiency, improve customer experience, and remain competitive against larger enterprises.

End-use Insights

The BFSI segment dominated the market and accounted for the largest revenue share in 2025, driven by large-scale core banking modernization, digital payment ecosystem expansion, and stringent regulatory compliance requirements. Financial institutions are transitioning from legacy monolithic systems to API-driven, cloud-native, and microservices-based architectures to enable real-time transactions, open banking frameworks, and embedded finance models. The rapid adoption of AI-powered fraud detection, risk analytics, RegTech platforms, and omnichannel customer engagement systems further increases integration complexity across core banking, CRM, cybersecurity, and data platforms.

The IT & telecom segment is expected to grow at a significant CAGR over the forecast period due to accelerated 5G deployment, network virtualization (NFV/SDN), edge computing expansion, and large-scale cloud-native transformation initiatives. Telecom operators are modernizing legacy OSS/BSS platforms, integrating core networks with open RAN architectures, and deploying distributed edge data centers to support ultra-low-latency applications such as IoT, autonomous systems, and real-time streaming.

Regional Insights

North America system integration market dominated the global industry with the largest revenue share of 34.8% in 2025, driven by large-scale enterprise modernization programs focused on cloud-native architectures and API-led connectivity strategies. Enterprises are increasingly adopting micro services-based application ecosystems and advanced middleware platforms to enable interoperability across digital channels.

U.S. System Integration Market Trends

The system integration market in the U.S. is expected to grow significantly at a CAGR of 12.9% from 2026 to 2033, due to defense modernization, federal IT transformation mandates, and large-scale infrastructure digitization programs. Government agencies are investing in secure, mission-critical system integration projects involving classified cloud environments, zero-trust frameworks, and integrated command-and-control systems.

Europe System Integration Market Trends

The system integration market in Europe is anticipated to register considerable growth from 2026 to 2033 due to sustainability compliance and ESG-driven digital reporting requirements.

The UK system integration market is expected to grow rapidly in the coming years, owing to financial services digital innovation and open banking frameworks. Banks and fintech firms are integrating API ecosystems, payment gateways, fraud detection platforms, and real-time settlement systems to comply with regulatory frameworks such as PSD2.

The system integration market in Germany held a substantial market share in 2025 due to advanced manufacturing digitization and industrial automation expansion. German enterprises are integrating robotics platforms, machine vision systems, and advanced industrial control networks with enterprise planning systems to enhance operational efficiency.

Asia Pacific System Integration Market Trends

The system integration market in the Asia Pacific region held a significant share in the global market in 2025, due to the rapid urbanization and large-scale smart infrastructure development projects. Governments and private enterprises are deploying integrated surveillance systems, intelligent transportation networks, and connected utility grids.

Japan system integration market is expected to grow rapidly in the coming years. Demographic shifts and labor shortages are accelerating automation and robotics deployment across industries. Enterprises are integrating advanced robotics, AI-enabled workflow systems, and legacy enterprise software to maintain productivity with a shrinking workforce.

The system integration market in China held a substantial market share in 2025, due to large-scale digital industrialization under national strategic initiatives promoting domestic technology ecosystems. Enterprises are integrating indigenous cloud platforms, AI processors, and localized enterprise software into vertically integrated digital environments.

Key System Integration Company Insights

Key players operating in the system integration industry are Accenture, NEC Corporation, Atos SE, Capgemini, Cisco Systems, Inc., and Cognizant, among others. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In February 2026, Cognizant entered into a strategic alliance with Palantir Technologies to strengthen AI-led modernization initiatives across healthcare and enterprise environments. Under the agreement, Cognizant will utilize Palantir Foundry and the Palantir Artificial Intelligence Platform (AIP) to enhance AI capabilities within its TriZetto healthcare portfolio, while also collaborating on enterprise-wide AI transformation programs across multiple industries. The partnership aligns with Cognizant’s positioning as an AI solutions developer, focused on delivering scalable, enterprise-grade platforms that convert artificial intelligence investments into measurable business outcomes.

-

In November 2025, Accenture acquired RANGR Data, a Palantir partner, delivering client-focused, scalable transformation programs. The move enhances Accenture’s ability to support enterprise reinvention by adding specialized expertise in data-driven operations, including supply chain optimization, enterprise systems integration, and real-time analytics. RANGR’s team of forward-deployed engineers is expected to play a key role in accelerating the design and deployment of customized Palantir-based solutions, supporting Accenture’s efforts to expand its Palantir services and deliver more agile, insight-led outcomes for clients across industries.

-

In October 2025, Tata Consultancy Services (TCS) expanded its collaboration with Google Cloud by incorporating Gemini Enterprise capabilities to advance the development and orchestration of agentic AI solutions. The expanded partnership is designed to strengthen AI-powered workflows, enable multi-agent coordination, and accelerate enterprise innovation across sectors. Through this initiative, TCS aims to help organizations deploy scalable, secure, and operationally efficient AI-driven systems that enhance overall business performance.

Key System Integration Companies:

The following key companies have been profiled for this study on the system integration market.

- Accenture

- Atos SE

- Boomi

- Capgemini

- Cisco Systems, Inc.

- Cognizant

- Deloitte Touche Tohmatsu Limited

- HCL Technologies Limited

- IBM Corporation

- Infosys Limited

- Livares Technologies Pvt Ltd.

- Mavenir

- MDS SI

- NEC Corporation

- Oracle Corporation

- Tata Consultancy Services Limited

- Tech Mahindra Limited

- Wipro

System Integration Market Report Scope

Report Attribute

Details

Market size in 2025

USD 421.4 billion

Estimated Market size in 2026

USD 467.0 billion

Projected Market size by 2033

USD 1,228.6 billion

Growth rate

CAGR of 14.8% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report enterprise size

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Services, enterprise size, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Accenture; Atos SE; Boomi; Capgemini; Cisco Systems, Inc.; Cognizant; Deloitte Touche Tohmatsu Limited; HCL Technologies Limited; IBM Corporation; Infosys Limited; Livares Technologies Pvt Ltd.; Mavenir; MDS SI; NEC Corporation; Oracle Corporation; Tata Consultancy Services Limited; Tech Mahindra Limited; Wipro

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global System Integration Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global system integration market report based on services, enterprise size, end-use, and region:

-

Services Outlook (Revenue, USD Billion, 2021 - 2033)

-

Infrastructure Integration

-

Application Integration

-

Consulting

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

Small & Medium Enterprises

-

-

End-use Outlook (Revenue, USD Billion, 2021 - 2033)

-

IT & Telecom

-

Defense & Security

-

BFSI

-

Oil & Gas

-

Healthcare

-

Transportation

-

Retail

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

The global system integration market size was estimated at USD 421.4 billion in 2025 and is expected to reach USD 467.0 billion in 2026.

The infrastructure segment led with a 38.2% revenue share in 2025, while consulting is the fastest-growing segment.

The large enterprises segment held the highest market share in 2025, while small & medium enterprises is growing significantly.

The BFSI segment accounted for the largest share in 2025, while IT & telecom is growing significantly.

The global system integration market is expected to grow at a compound annual growth rate of 14.8% from 2026 to 2033 to reach USD 1,228.6 billion by 2033.

North America dominated the global market with the largest revenue share of 34.8% in 2025.

Some key players operating in the system integration market are Accenture, Atos SE, Boomi, Capgemini, Cisco Systems, Inc., Cognizant, Deloitte Touche Tohmatsu Limited, HCL Technologies Limited, IBM Corporation, Infosys Limited, Livares Technologies Pvt Ltd., Mavenir, MDS SI, NEC Corporation, Oracle Corporation, Tata Consultancy Services Limited, Tech Mahindra Limited, Wipro

Key factors contributing to the growth of this market include organizations across industries that are modernizing legacy IT environments to enable automation, real-time analytics, omnichannel engagement, and operational agility.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.