- Home

- »

- Advanced Interior Materials

- »

-

Thermal Paper Market Size, Share & Growth Report, 2033GVR Report cover

![Thermal Paper Market (2026 - 2033)Report]()

Thermal Paper Market (2026 - 2033)

Size, Share & Trends Analysis Report By Width (57mm, 80mm), By Application (POS, Tags & Label, Lottery & Gaming, Ticketing, Medical), By Technology (Direct Transfer, Thermal Transfer), By Region, And Segment Forecasts

Market Size, 2025

$4.2BMarket Estimate, 2026

$4.4BMarket Forecast, 2033

$6.0BCAGR, 2026–2033

4.6%Thermal Paper Market Summary

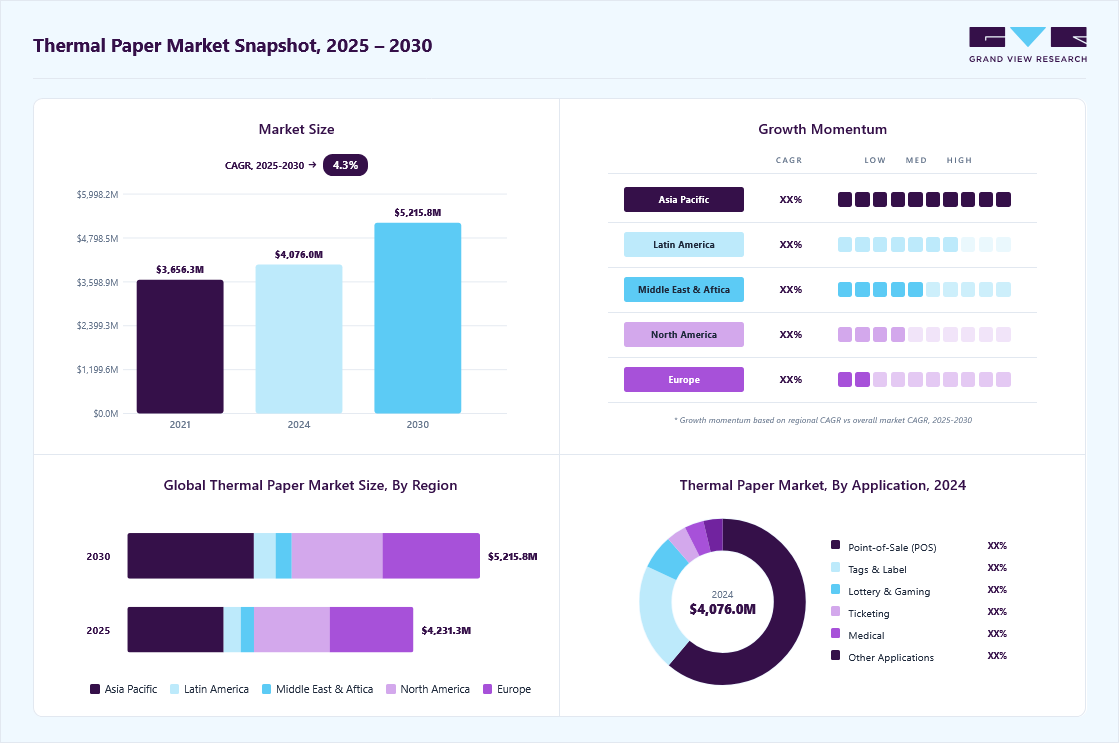

The global thermal paper market size was valued at USD 4.2 billion in 2025 and is projected to grow from USD 4.4 billion in 2026 to USD 6.0 billion by 2033, growing at a CAGR of 4.6% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 33.7% in 2025. The rapid expansion of the retail and e-commerce sectors is a significant driver of the market growth.

Key Market Trends & Insights

- By width: The 80mm segment held the largest market share of 45.7% in 2025.

- By technology: direct thermal segment held the largest market share of 60.7% in 2025.

- By application: point-of-sale (POS) segment held the largest market share of 61.0% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (33.7% revenue share, 2025)

- The thermal paper industry in China held the largest revenue share in 2025.

Market Size & Forecast

- Market size in 2025: USD 4.2 Billion

- Estimated market size in 2026: USD 4.4 Billion

- Projected market size by 2033: USD 6.0 Billion

- CAGR (2026-2033): 4.6%

Thermal paper is extensively used for point-of-sale (POS) receipts, labels, and tags in these industries. With the rise of online shopping, there is an increasing demand for shipping labels and tracking tags, which are primarily made from thermal paper. Retail outlets and logistics providers rely on thermal paper for its cost-effectiveness, reliability, and efficiency in providing quick printouts, further boosting market demand.")

Technological advancements in thermal printing are making thermal printers more efficient, durable, and capable of handling high-speed printing tasks. These improvements have encouraged businesses to adopt thermal printing over traditional printing methods, driving the demand for thermal paper. Innovations such as color thermal printing and enhanced image durability have expanded the applications of thermal paper beyond conventional uses, such as for event tickets, lottery tickets, and medical charts.

Thermal paper plays a vital role in the healthcare industry, particularly for printing medical reports, diagnostic images, and prescription labels. The increasing focus on digital healthcare solutions and patient record-keeping has not diminished the demand for physical prints in critical applications, where thermal paper offers high-resolution and durable printouts. In addition, the growing prevalence of chronic diseases necessitates diagnostic and monitoring equipment, which often uses thermal paper for data printing. Thermal paper is widely used for labeling in the food and beverage sector, particularly for perishable products that require accurate and clear labeling of expiry dates, batch numbers, and storage instructions. The rise in global food consumption and stringent labeling regulations have significantly contributed to the demand for thermal paper. Furthermore, the adoption of thermal paper in self-checkout systems in supermarkets and fast-food restaurants has gained traction.

Market Dynamics

The thermal paper market is experiencing steady growth due to increasing demand for point-of-sale (POS) receipts, labels, tickets, tags, lottery systems, logistics tracking, and healthcare documentation. Thermal paper offers advantages such as high-speed printing, low maintenance requirements, cost efficiency, and the elimination of ink or toner usage. The expansion of retail networks, growing e-commerce activities, rising adoption of automated transaction systems, and increasing demand for barcode labeling and packaging solutions are further supporting market growth. Additionally, technological advancements in BPA-free and environmentally friendly thermal paper formulations are contributing to wider industry adoption.

The increasing use of thermal paper in retail and point-of-sale (POS) systems is a major factor driving the thermal paper market. Rapid growth in organized retail, supermarkets, convenience stores, restaurants, and hospitality establishments has significantly increased the demand for printed receipts and transaction records. Thermal paper enables fast, reliable, and cost-effective printing without requiring ink cartridges or ribbons, making it highly suitable for high-volume transaction environments. The widespread deployment of electronic cash registers and POS terminals across both developed and emerging economies continues to support consumption of thermal paper products.

Furthermore, the expansion of e-commerce and omnichannel retailing is creating additional demand for thermal labels, shipping tags, and logistics documentation. Businesses are increasingly relying on barcode and tracking systems to improve inventory management and supply chain visibility. As retail transactions and logistics operations continue to grow globally, the demand for thermal paper across receipt printing and labeling applications is expected to remain strong, supporting long-term market expansion.

The thermal paper market faces challenges due to growing environmental and regulatory concerns surrounding the use of chemical developers such as Bisphenol A (BPA) and Bisphenol S (BPS) in thermal paper coatings. Several governments and regulatory bodies have implemented restrictions on BPA-containing thermal paper due to concerns regarding potential health and environmental impacts. Compliance with evolving regulations often requires manufacturers to invest in alternative coating technologies and reformulate products, increasing production costs.

The increasing focus on sustainability and regulatory compliance is creating significant growth opportunities for the thermal paper market. Manufacturers are investing in BPA-free, phenol-free, and recyclable thermal paper technologies to address environmental concerns while meeting evolving regulatory requirements. Growing demand from retailers, financial institutions, healthcare providers, and logistics companies for environmentally responsible printing materials is accelerating the adoption of sustainable thermal paper products.

In addition, advancements in coating technologies are improving print durability, image stability, recyclability, and overall product performance. Governments and businesses are increasingly promoting sustainable packaging and documentation practices as part of broader ESG and circular economy initiatives. As organizations seek safer and more environmentally friendly alternatives to conventional thermal paper, the adoption of next-generation eco-friendly thermal paper products is expected to create substantial growth opportunities across multiple end-use industries.

Analyst Perspective

The thermal paper market is gradually transitioning from conventional receipt printing toward higher-value, application-specific solutions, with stronger growth opportunities in BPA-free and phenol-free papers, durable logistics labels, healthcare documentation media, and specialty thermal products. The key differentiator for companies will not be production capacity alone, but their ability to develop compliant coating technologies, ensure print durability, maintain consistent product performance, and address evolving environmental regulations. Players with advanced coating expertise, integrated manufacturing capabilities, strong relationships with retail and logistics customers, and sustainable product portfolios are likely to capture premium margins, while smaller and less diversified suppliers may remain vulnerable to regulatory pressures, raw material price volatility, and the increasing adoption of digital alternatives.

Width Insights

Based on width, the 80mm segment led the market with the largest revenue share of 45.7% in 2025 and is expected to grow at a CAGR of 3.9% over the forecast period. The 80mm segment is the most widely used thermal paper width in retail and hospitality industries due to its compatibility with standard point-of-sale (POS) systems. Retailers and restaurants prefer 80mm thermal paper rolls for their ability to produce detailed receipts, including logos, promotional messages, and transaction information, enhancing the customer experience. The increasing penetration of advanced POS systems in these industries continues to drive the demand for 80mm thermal paper.

The 57mm segment is expected to grow at the fastest CAGR of 5.1% over the forecast period. The 57mm thermal paper segment is driven by the increasing popularity of mobile and compact printers used in applications such as on-the-go billing, ticketing, and delivery receipt generation. These portable printers are widely used by delivery personnel, parking attendants, and small vendors due to their convenience and compatibility with 57mm thermal rolls. The growth of e-commerce and last-mile delivery services has further fueled the demand for this segment.

Application Insights

Based on application, the point-of-sale (POS) segment led the market with the largest revenue share of 61.0% in 2025 and is expected to grow at a CAGR of 4.5% over the forecast period. The modernization of POS systems with advanced features, such as touchscreens and wireless connectivity, has broadened their application across various industries. These systems rely on thermal paper for quick and efficient printing, minimizing delays in customer service. The increasing availability of compact and portable POS terminals in retail outlets and small businesses has further accelerated thermal paper adoption.

The tags & label segment is anticipated to grow at the fastest CAGR of 5.9% over the forecast period. Retail businesses are major consumers of thermal paper tags and labels, which are essential for pricing, barcode printing, and product information. The growth of organized retail formats, supermarkets, and hypermarkets has amplified the need for cost-effective and high-quality labeling solutions. Thermal paper labels provide quick printing capabilities, making them ideal for real-time price changes and inventory updates, which are critical in the dynamic retail environment.

Technology Insights

Based on technology, the direct thermal segment led the market with the largest revenue share of 60.7% in 2025 and is expected to grow at a CAGR of 4.1% over the forecast period. Direct thermal technology is widely utilized in logistics and supply chain management for printing shipping labels, warehouse tags, and inventory labels. Its ability to provide clear, durable prints suitable for short-term use aligns perfectly with the fast-paced nature of the logistics industry. As global trade expands and businesses increasingly adopt advanced supply chain solutions, the demand for direct thermal printing continues to grow.

The thermal transfer segment is expected to grow at the fastest CAGR of 4.4% over the forecast period. The thermal transfer segment benefits from regulatory requirements mandating clear and durable labeling in industries such as food and beverage, pharmaceuticals, and chemicals. For instance, in the pharmaceutical sector, thermal transfer labels are widely used to meet stringent regulatory standards for traceability and compliance. The ability of thermal transfer labels to maintain print integrity over extended periods makes them indispensable in such regulated environments.

Regional Insights

The North America thermal paper market growth is driven by the stringent regulations and labeling standards for thermal paper, particularly in the food and pharmaceutical sectors. The Food and Drug Administration (FDA) and other regulatory bodies require clear and accurate labeling, including the use of batch numbers, expiration dates, and safety instructions. As a result, thermal paper is a preferred option for compliance due to its ability to print durable, high-quality labels that meet regulatory standards. The continuous evolution of regulatory requirements, especially in food safety and pharmaceuticals, ensures sustained demand for thermal paper products.

U.S. Thermal Paper Market Trends

The thermal paper market in the U.S. is driven by the increasing adoption of self-checkout kiosks in retail stores, supermarkets, and fast-food chains, which contribute significantly to the demand for thermal paper. These self-service systems rely on thermal printers to produce receipts and labels quickly. As retailers focus on enhancing customer experience and reducing labor costs, the use of thermal paper for such systems is expected to continue rising, driving further growth in the market.

Central & South America Thermal Paper Market Trends

The thermal paper market in CSA is anticipated to grow due to the adoption of advanced thermal printing technology that is creating new opportunities in the market. Enhanced printer reliability, lower maintenance costs, and the ability to handle high-volume printing have made thermal printing an attractive option for businesses. Innovations such as color thermal printing and heat-sensitive paper with longer shelf life are increasing thermal paper's appeal across various applications, including event tickets, parking tickets, and medical reports.

Asia Pacific Thermal Paper Market Trends

Asia Pacific dominated the thermal paper market with the largest revenue share of 33.7% in 2025. The Asia-Pacific region has witnessed a remarkable expansion in the retail and e-commerce sectors, driven by rising disposable incomes, urbanization, and a growing middle-class population. Countries like China, India, and Southeast Asian nations are leading this growth, with thermal paper being widely used for point-of-sale (POS) systems, receipts, and shipping labels. The rapid adoption of online shopping platforms and increased reliance on logistics and supply chain operations further amplify the demand for thermal paper in this region.

The thermal paper market in China is driven by the rapidly expanding food delivery and logistics industries, which contribute significantly to the demand for thermal paper. These sectors rely on thermal paper for labeling, packaging information, and real-time printing of receipts and invoices. The growth of online-to-offline (O2O) services in urban areas has also added to the consumption of thermal paper in labeling solutions for streamlined operations.

Europe Thermal Paper Market Trends

Europe thermal paper market is witnessing significant advancements in retail technology, particularly in point-of-sale (POS) systems. Retailers across Europe are increasingly adopting thermal printers for receipt generation, inventory management, and ticketing, owing to their speed, cost-efficiency, and reliability. As more retailers upgrade their systems and deploy self-checkout kiosks, the demand for thermal paper continues to rise. The widespread use of mobile POS systems and the shift toward cashless transactions also favor the adoption of thermal printing technologies in European markets.

Key Thermal Paper Company Insights

Some of the key players operating in the market include Oji Holdings Corporation, Appvion Inc. Others

-

Oji Holdings offers a wide range of high-quality thermal papers used in point-of-sale receipts, labels, and tickets. Their product offerings include eco-friendly, BPA-free thermal paper options that meet global sustainability standards, as well as advanced thermal papers for specialized applications like medical records, barcode labels, and lottery tickets.

-

Appvion's product offerings include high-quality thermal papers used for point-of-sale receipts, labels, tickets, and other applications. They offer a range of thermal paper products, such as coated and uncoated rolls, custom-printed thermal papers, and eco-friendly BPA-free thermal papers. The company emphasizes sustainable production practices and consistently adapts its product portfolio to meet the evolving demands of global markets, with an increasing focus on providing durable, high-performance, and environmentally responsible solutions.

Key Thermal Paper Companies:

The following key companies have been profiled for this study on the thermal paper market.

-

Oji Holdings Corporation

-

Appvion Inc

-

Koehler Group

-

Mitsubishi Paper Mills Limited

-

Hansol Paper Co. Ltd.

-

Gold Huasheng Paper Co. Ltd.

-

Henan Province JiangHe Paper Co. Ltd.

-

Thermal Solutions International Inc.

-

Iconex LLC

-

Twin Rivers Paper Company

-

Rotolificio Bergamasco Srl

-

Jujo Thermal Limited

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Established Players: Oji Holdings Corporation, Appvion Inc., Koehler Group, Mitsubishi Paper Mills Limited, Hansol Paper Co. Ltd.

- Focus on BPA-free and phenol-free thermal paper development.

- Expand global distribution and long-term supply agreements with retailers and logistics providers.

- Invest in capacity expansion and vertical integration across paper production and coating operations.

- Strong manufacturing scale and global customer base.

- Established brand recognition and regulatory compliance capabilities.

- Broad product portfolios serving POS, labels, ticketing, and healthcare applications.

- Higher operational and compliance costs.

- Exposure to declining receipt demand in digitized markets.

- Slower adaptation to niche and customized market requirements.

Emerging Players: Gold Huasheng Paper Co. Ltd., Henan Province JiangHe Paper Co. Ltd., Thermal Solutions International Inc.

- Focus on regional expansion and cost-competitive production.

- Target niche applications such as specialty labels and customized thermal rolls.

- Develop partnerships with local distributors and converters.

- Lower manufacturing costs and operational flexibility.

- Ability to rapidly respond to regional demand trends.

- Strong growth potential in emerging markets.

- Limited global brand recognition.

- Smaller production capacities and distribution networks.

- Greater dependence on regional demand fluctuations and raw material prices.

Thermal Paper Market Report Scope

Report Attribute

Details

Market size in 2025

USD 4.2 billion

Estimated market size in 2026

USD 4.4 billion

Projected market size by 2033

USD 6.0 billion

Growth rate

CAGR of 4.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Volume in kilotons and Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Width, technology, application, and region

Regional scope

North America; Europe; Asia Pacific; Central & South America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Russia; China; India; Japan; South Korea; Australia; New Zealand; Vietnam; Brazil; Argentina, Saudi Arabia; South Africa; UAE; Qatar

Key companies profiled

Oji Holdings Corporation; Appvion Inc; Koehler Group; Mitsubishi Paper Mills Limited; Hansol Paper Co. Ltd.; Gold Huasheng Paper Co. Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Thermal Paper Market Report Segmentation

This report forecasts revenue & volume growth at country levels and provides an analysis of the industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global thermal paper market based on width, technology, application, and region:

-

Width Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

57mm

-

80mm

-

Others

-

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

POS

-

Tags & Label

-

Lottery & Gaming

-

Ticketing

-

Medical

-

Others

-

-

Technology Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Direct Transfer

-

Thermal Transfer

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Itay

-

Spain

-

Russia

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

New Zealand

-

Vietnam

-

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

Qatar

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Width

Revenue capture definition

57mm

Revenue generated from the sale of 57mm-width thermal paper rolls used primarily in compact printing devices, including handheld POS terminals, credit/debit card machines, mobile payment systems, portable receipt printers, parking meters, and vending machines. This segment captures revenues from thermal paper supplied for applications requiring small-format receipts and transaction records in retail, transportation, hospitality, and self-service environments.

80mm

Revenue generated from the sale of 80mm-width thermal paper rolls used in standard POS systems, cash registers, ATMs, kiosks, lottery terminals, and ticketing machines. This segment captures revenues from thermal paper supplied for high-volume receipt printing, transaction documentation, and customer billing applications across retail stores, supermarkets, restaurants, banking institutions, entertainment venues, and transportation facilities.

Other Widths

Revenue generated from the sale of thermal paper rolls in widths other than 57mm and 80mm, including customized and application-specific formats. This segment captures revenues from thermal paper supplied for specialized uses such as medical chart recorders, diagnostic equipment, industrial labeling systems, logistics printing, transportation ticketing, gaming terminals, and other niche commercial and industrial applications requiring non-standard paper dimensions.

Segment - Technology

Revenue capture definition

Direct Transfer

Revenue generated from the sale of direct thermal paper that produces printed images through heat-sensitive coatings without requiring ink, toner, or ribbons. This segment captures revenues from thermal paper supplied for applications such as POS receipts, transportation tickets, lottery tickets, medical records, and short-term labeling, where cost efficiency, high-speed printing, and ease of operation are critical requirements.

Thermal Transfer

Revenue generated from the sale of thermal transfer printing materials that utilize heat in combination with a ribbon to transfer ink onto paper or label substrates. This segment captures revenues from thermal paper and related media used for applications requiring enhanced print durability, resistance to heat, moisture, chemicals, and long-term readability, including industrial labeling, asset tracking, logistics, warehousing, pharmaceutical labeling, and product identification.

Others

Revenue generated from the sale of thermal paper and specialty printing technologies not classified under direct transfer or thermal transfer categories. This segment captures revenues from customized thermal printing solutions, hybrid printing technologies, specialty coated papers, security printing applications, and niche industrial or commercial uses that require specific performance characteristics beyond conventional thermal printing methods.

Segment - Application

Revenue capture definition

POS

Revenue generated from the sale of thermal paper used for printing transaction receipts, invoices, payment confirmations, and purchase records through point-of-sale systems. This segment captures revenues from thermal paper supplied to retail stores, supermarkets, restaurants, hospitality establishments, fuel stations, banking terminals, and other commercial outlets requiring high-volume receipt printing.

Tags & Label

Revenue generated from the sale of thermal paper used in the production of barcode labels, shipping labels, inventory tags, price tags, and product identification labels. This segment captures revenues from thermal paper utilized across logistics, warehousing, e-commerce fulfillment, retail inventory management, food packaging, and industrial tracking applications.

Lottery & Gaming

Revenue generated from the sale of thermal paper used for lottery tickets, betting slips, gaming vouchers, transaction receipts, and promotional gaming materials. This segment captures revenues from thermal paper supplied to lottery operators, casinos, sports betting facilities, gaming centers, and amusement venues that require secure and rapid ticket printing solutions.

Ticketing

Revenue generated from the sale of thermal paper used for transportation tickets, event tickets, parking tickets, cinema tickets, boarding passes, and access passes. This segment captures revenues from thermal paper utilized by public transportation systems, airlines, entertainment venues, sports facilities, parking operators, and event management organizations for ticket issuance and validation purposes.

Medical

Revenue generated from the sale of thermal paper used for medical documentation, patient monitoring records, diagnostic reports, prescription labels, and healthcare receipts. This segment captures revenues from thermal paper supplied to hospitals, clinics, diagnostic laboratories, pharmacies, and healthcare facilities for printing critical medical information and operational records.

Others

Revenue generated from the sale of thermal paper used in applications not categorized under POS, tags & labels, lottery & gaming, ticketing, or medical segments. This segment captures revenues from thermal paper utilized in kiosks, ATMs, vending machines, self-service terminals, parking meters, weighing scales, government documentation, and various specialized industrial and commercial printing applications.

Estimation Model

Layer Name

Key Question

Description

Demand Generation Layer

Who creates thermal paper demand?

Assess transaction volumes across retail POS, logistics labels, ticketing, healthcare records, gaming slips, ATMs, and kiosks to establish the addressable printing universe.

Thermal Printing Adoption Layer

Which transactions use thermal paper?

Apply thermal printer penetration rates across industries to identify the share of transactions utilizing thermal paper-based printing systems.

Consumption Layer

How much thermal paper is consumed?

Convert thermal print volumes into paper demand using average receipt consumed, and roll replacement frequencies.

Revenue Layer

How much revenue is generated?

Multiply thermal paper consumption by average selling prices, adjusted for product grade, technology type, and regional pricing variations.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Logistics Labeling & E-commerce Growth Opportunity Assessment

Evaluated thermal paper consumption trends in shipping labels, warehouse management, inventory tracking, and parcel identification driven by e-commerce growth and supply chain digitalization.

Supports investment decisions by identifying high-growth application segments, emerging demand centers, and opportunities for specialty label and durable thermal media solutions.

Thermal Paper Supply Chain & Raw Material Risk Assessment

Analyzed coating chemical availability, paper substrate sourcing, regional manufacturing capacity, pricing trends, and supply chain vulnerabilities affecting thermal paper production.

Enables manufacturers and investors to strengthen procurement strategies, mitigate supply risks, and enhance operational resilience amid fluctuations in raw material prices.

Regional Demand & Regulatory Landscape Benchmarking

Conducted country-level analysis of thermal paper demand, environmental regulations, recycling initiatives, and industry adoption trends across major regions.

Supports market entry and expansion strategies by identifying favorable regulatory environments, high-growth regions, and emerging competitive opportunities.

Frequently Asked Questions About This Report

Some of the key players operating in the thermal paper market include Oji Holdings Corporation, Appvion Inc, Koehler Group, Mitsubishi Paper Mills Limited, Hansol Paper Co. Ltd., and Gold Huasheng Paper Co. Ltd.

The key factors that are driving the thermal paper market are increasing usage of POS terminals for monetary transactions due to the expansion of the e-commerce and packaging industries.

The global thermal paper market size was estimated at USD 4.2 billion in 2025 and is expected to reach USD 4.4 billion in 2026.

The global thermal paper market is expected to grow at a compound annual growth rate of 4.6% from 2026 to 2033 to reach USD 6.0 billion by 2033.

POS dominated the thermal paper market with a share of 61.0% in 2025 due to the expansion of retail chain stores in countries, resulting in increased monetary transactions.

The thermal transfer technology segment is expected to grow at a CAGR of 5.2% over the forecast period.

Asia Pacific held the largest revenue share of 33.7% in 2025, supported by expanding retail infrastructure, increasing deployment of POS terminals, high transaction volumes, and a strong manufacturing base across key economies including China, India, and Japan.

The 57 mm width segment is expected to witness the highest growth, at a CAGR of 5.1% during the forecast period, owing to the growing deployment of portable POS systems and mobile payment terminals across retail, transportation, and service industries.

The 80 mm width segment accounted for the largest revenue share of 45.7% in 2025, driven by its extensive adoption in POS systems across retail, hospitality, and banking applications.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.