- Home

- »

- Renewable Energy

- »

-

Wind Power Market Size, Growth Report, 2026-2033GVR Report cover

![Wind Power Market (2026 - 2033)Report]()

Wind Power Market (2026 - 2033)

Size, Share & Trends Analysis Report By Location (Onshore, Offshore), By Application (Utility, Non-utility), By Region (North America, Europe, Asia Pacific, Middle East & Africa), And Segment Forecasts

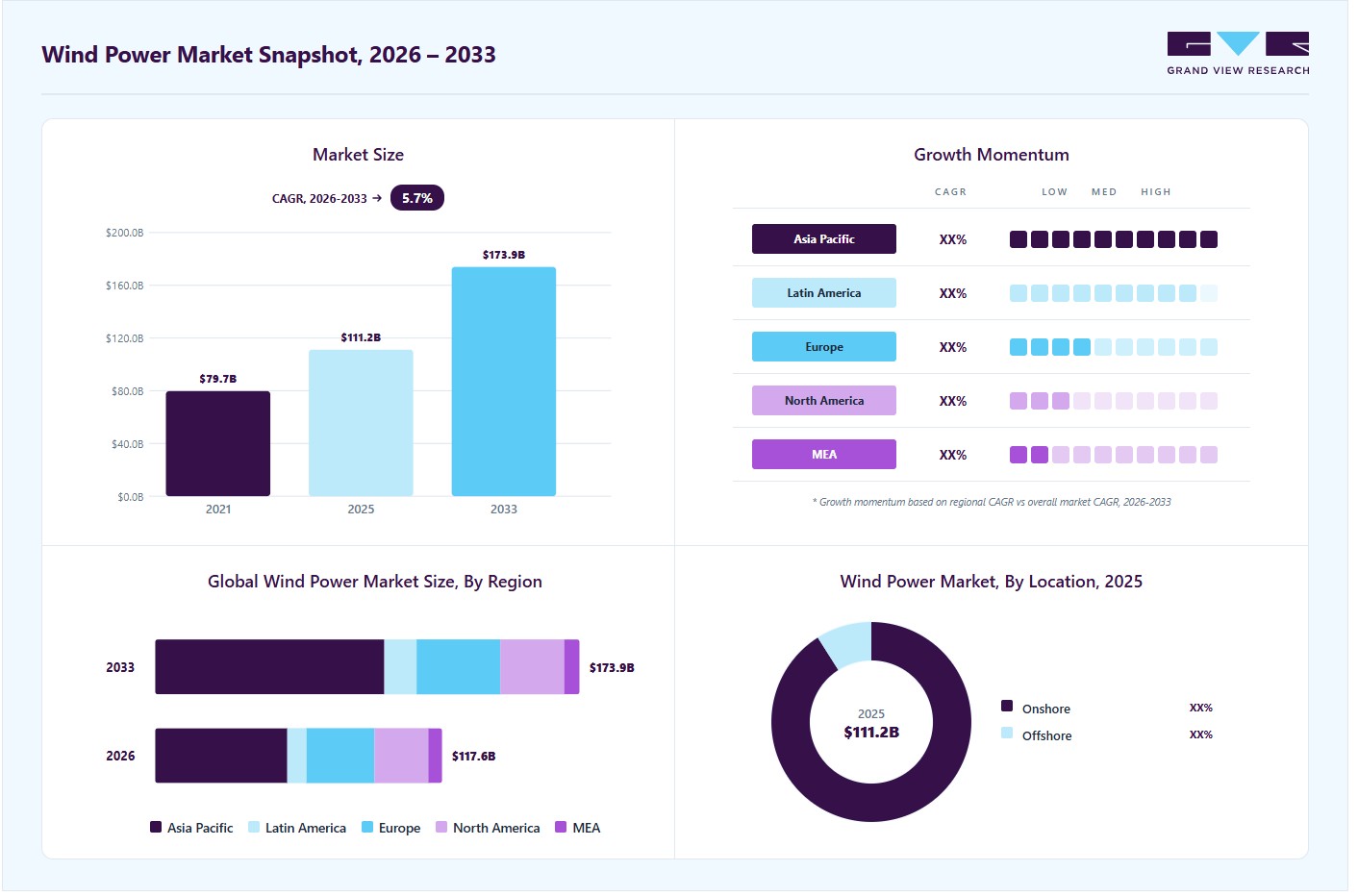

Market Size, 2025

$111.2BMarket Estimate, 2026

$117.6BMarket Forecast, 2033

$173.9BCAGR, 2026–2033

5.7%Wind Power Market Summary

The global wind power market size was valued at USD 111.2 billion in 2025 and is projected to grow from USD 117.6 billion in 2026 to USD 173.9 billion by 2033, at a CAGR of 5.7% from 2026 to 2033. Asia Pacific dominated the global market, accounting for the largest revenue share of 44.9% in 2025. The industry is expanding due to the global push for decarbonization, as countries aim to reduce greenhouse gas emissions and transition to cleaner energy sources.

Key Market Trends & Insights

- By location: Onshore segment accounted for the largest revenue share of 91.0% in 2025.

- By application: Utility segment held the largest revenue share of 94.5% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (44.9% revenue share, 2025)

- By country: The China wind power industry is a major contributor to the global market.

Market Size & Forecast

- Market size in 2025: USD 111.2 Billion

- Estimated market size in 2026: USD 111.6 Billion

- Projected market size by 2033: USD 173.9 Billion

- CAGR (2026-2033): 5.7%

Supportive policies, falling technology costs, and rising electricity demand are also accelerating the adoption of wind energy. The industry is experiencing strong growth as countries and corporations accelerate decarbonization efforts and shift toward cleaner energy sources. Governments are introducing supportive policies such as subsidies, tax incentives, and renewable energy targets, making wind projects more financially viable. The cost of wind energy has declined significantly due to improvements in turbine design, larger rotor sizes, and more efficient installation techniques, making it increasingly competitive with conventional power generation.

")

The rising global demand for electricity, particularly in emerging economies, where expanding infrastructure requires reliable and scalable energy solutions, is also driving this market's growth. Wind power is also benefiting from increased private sector participation, with companies investing heavily in renewable energy to meet sustainability commitments and reduce long-term energy costs. Advancements in grid integration, energy storage, and offshore wind development are opening new opportunities, enabling wider adoption and supporting a consistent power supply.

Drivers, Opportunities & Restraints

The primary driver of the industry is the increasing global focus on decarbonization to reduce greenhouse gas emissions. Governments across regions are setting strict climate targets and promoting renewable energy adoption to shift away from fossil fuels. This is leading to higher investments in wind energy projects supported by favorable policies and financial incentives. Businesses are also aligning with decarbonization goals by adopting clean energy sources to lower their carbon footprint. Therefore, wind power is gaining strong momentum as a reliable and scalable solution for achieving long-term sustainability targets.

Offshore wind development presents a strong growth opportunity as investments increase in floating wind turbines that can operate in deeper waters where wind speeds are higher and more consistent. This allows developers to access new locations beyond shallow coastal areas, significantly expanding the potential for power generation. Advancements in floating platform technology and installation methods are making these projects more feasible and cost-effective over time. Governments are supporting offshore wind through dedicated policies, leasing programs, and funding initiatives to accelerate deployment.

However, economic pressures are creating challenges for the market. Inflation has significantly increased the cost of wind turbines and related components, making project development more expensive for companies. High interest rates are raising the cost of capital, which is affecting financing for new wind projects. These conditions are leading to delays in project execution and, in some cases, cancellations of planned installations. Thus, the developers are becoming more cautious with investment decisions and focusing on cost optimization and risk management.

Infrastructure and logistics limitations are restraining the growth of the industry. In many regions, insufficient grid infrastructure and a lack of adequate transmission capacity are creating hurdles in efficiently integrating wind energy into the power system. Offshore wind projects also face significant logistical complexities due to the need for specialized vessels, ports, and heavy lifting equipment. These bottlenecks increase project timelines and costs, thereby slowing down large-scale wind power deployment.

Application Insights

The utility segment held the largest share of 94.5% in 2025, driven by large-scale wind farm installations for grid-based electricity generation. Long-term power purchase agreements ensure stable and predictable revenue streams. Strong government policies and renewable energy targets are increasing investments in utility-scale projects. Utilities have the financial capacity to develop and operate large wind power infrastructure. Grid integration capabilities and established transmission networks further support large-scale deployment. This makes utility-scale projects more reliable and commercially viable.

The non-utility segment is projected to register the fastest CAGR of 15.3% over the forecast period due to the rising adoption of distributed wind systems by commercial, industrial, and residential users. Businesses are increasingly investing in wind energy to reduce electricity costs and meet sustainability targets. Supportive policies such as net metering and incentives are encouraging small-scale installations. Technological advancements are also making smaller wind systems more efficient and easier to deploy.

Location Insights

The onshore segment accounted for the largest revenue share of 91.0% in 2025 due to its lower installation and maintenance costs compared to offshore projects. Onshore wind farms are easier to develop as they require less complex infrastructure and simpler logistics. They also benefit from faster project execution timelines and easier grid connectivity in many regions. The availability of suitable land areas and supportive government policies has encouraged widespread deployment. These factors collectively make onshore wind the most widely adopted and cost-effective option in the market.

The offshore segment is the fastest-growing segment, with a projected CAGR of 15.5% over the forecast period, driven by its ability to generate higher and more consistent energy output from stronger wind speeds at sea. Offshore projects can support larger turbines, which improves overall efficiency and power generation capacity. Increasing investments in floating wind technology are also enabling development in deeper waters, expanding project potential. Governments are actively supporting offshore wind through dedicated policies and long-term targets. These factors are driving rapid growth despite higher initial costs compared to onshore projects.

Regional Insights

Asia Pacific wind power market accounted for the largest revenue share of 44.9% in 2025, due to the presence of established wind energy markets and large-scale installations across key countries. The region benefits from strong government support, including favorable policies, subsidies, and long-term renewable energy targets. High electricity demand and continuous investments in onshore and offshore wind projects have further strengthened market growth. The presence of major manufacturing hubs and a well-developed supply chain supports cost-effective project development. These factors collectively contribute to the region’s leading position in the global market.

China Wind Power Market Trends

The wind power market in China is shaped by aggressive renewable energy targets under its “dual carbon” strategy, which aims to peak emissions by 2030 and achieve carbon neutrality by 2060. This is driving large-scale investments in both onshore and offshore wind projects across the country. Strong government support through policies, subsidies, and grid expansion is further accelerating capacity additions. China also benefits from a well-established domestic manufacturing base, which helps reduce costs and improve project execution.

Europe Wind Power Market Trends

The wind power market in Europe is driven by a strong focus on energy security and independence, as countries shift away from imported fossil fuels, particularly Russian gas. This transition is accelerating large-scale investments in renewable energy infrastructure, including both onshore and offshore wind projects. Governments are introducing supportive policies and fast-tracking project approvals to expand domestic energy generation. Regional cooperation and grid integration efforts are improving energy distribution across countries.

North America Wind Power Market Trends

The wind power market in North America is witnessing strong growth, supported by rapid technological advancements in turbine design and deployment. The shift toward larger turbines are improving capacity factors and increasing overall energy output. These advanced turbines enable more efficient utilization of wind resources, especially in high-potential regions. The development of floating wind technology is unlocking access to deep-water offshore sites that were previously not viable. These innovations are enhancing project feasibility and supporting the continued expansion of wind power across the region.

The wind power market in the U.S. is driven by strong federal and state policy support that encourages renewable energy development. The extension of Production Tax Credits (PTC) and Investment Tax Credits (ITC) is significantly influencing investment by improving project economics and attracting developers. State-level initiatives and Renewable Portfolio Standards (RPS) are ensuring consistent long-term demand for wind energy. These policies provide revenue visibility and reduce financial risks for project developers.

Latin America Wind Power Market Trends

The wind power market in Latin America is expected to grow at the second-fastest CAGR of 7.6%. The market in the region is being driven by competitive auction systems that enable cost-efficient project development. Governments are increasingly adopting transparent bidding frameworks, attracting both domestic and international investors. The rise of corporate power purchase agreements (PPAs) is encouraging private sector participation in renewable energy projects. The development of utility-scale and hybrid wind-solar projects is further supporting market expansion across the region. Favorable wind resources in key countries are also enhancing project viability and energy output.

Middle East & Africa Wind Power Market Trends

The wind power market in the Middle East and Africa (MEA) is being driven by the declining Levelized Cost of Energy (LCOE), which is making wind energy increasingly competitive with traditional fossil fuels. Lower generation costs are encouraging governments and developers to invest in wind projects as a cost-effective power solution. This shift is supporting the diversification of energy sources in economies that have traditionally relied on fossil fuels. Improving project economics is attracting international investments and financing.

Key Wind Power Company Insights

Some of the key participants in the global wind power market include ABB, EDF Power Solution, GE Vernova, Goldwind, Northland Power Inc., Siemens Gamesa Renewable Energy, Sinovel Wind Group Co., Suzlon Energy Limited, United Power, Vensys Energy AG and Vestas. These companies collectively account for a significant share of the global market and play a pivotal role in shaping industry trends and competitive dynamics. They are actively investing in capacity expansion, advanced turbine technologies, and the development of large-scale onshore and offshore wind projects to enhance energy generation efficiency and reliability while aligning with global decarbonization targets.

Their operations typically span the design, manufacturing, installation, and maintenance of wind turbines, along with project development and power generation, supported by integrated global supply chains and service networks. The companies are increasingly leveraging digital technologies such as automation, real-time monitoring, and predictive analytics to optimize turbine performance, improve asset reliability, and enhance overall operational efficiency. The integration of advanced engineering and data-driven systems is enabling better energy output optimization, cost efficiency, and compliance with evolving grid and environmental standards.

As global electricity demand rises alongside stringent emission reduction goals, companies in the market are prioritizing technological innovation, offshore project expansion, and grid integration capabilities. Strategic partnerships with governments, utilities, and technology providers are becoming more prevalent to accelerate renewable energy deployment. Evolving market dynamics, including the transition toward clean energy systems and advancements in energy storage and hybrid solutions, are reshaping the competitive landscape.

Key Wind Power Companies:

The following key companies have been profiled for this study on the wind power market.

- ABB

- EDF power solutions

- GE Vernova

- Goldwind

- Northland Power Inc.

- Siemens Gamesa Renewable Energy

- Sinovel Wind Group Co.

- Suzlon Energy Limited

- United Power

- Vensys Energy AG

- Vestas

Recent Developments

- In September 2025, Vestas took over operations of an onshore blade manufacturing facility in Goleniów, Poland, previously operated by LM Wind Power, a subsidiary of GE Vernova. This move is part of Vestas’ strategy to expand its European manufacturing footprint and strengthen supply chain resilience, while supporting the region’s growing demand for secure, cost-effective, and sustainable energy.

Wind Power Market Report Scope

Report Attribute

Details

Market Definition

The Global Wind Power market refers to the total revenue generated from the development, installation, and operation of wind energy systems, including turbines and associated infrastructure, used to convert wind energy into electricity across various end-use sectors.

Market size in 2025

USD 111.2 billion

Estimated Market size in 2026

USD 117.6 billion

Projected Market size by 2033

USD 173.9 billion

Growth rate

CAGR of 5.7% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Capacity in MW; revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Capacity & revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Location, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Russia; China; India; Australia; Japan; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

ABB; EDF power solutions; GE Vernova; Goldwind; Northland Power Inc.; Siemens Gamesa Renewable Energy; Sinovel Wind Group Co.; Suzlon Energy Limited; United Power; Vensys Energy AG; Vestas

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Wind Power Market Report Segmentation

This report forecasts capacity & revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global wind power market report on the basis of location, application, and region:

-

Location Outlook (Capacity in MW; Revenue in USD Million, 2021 - 2033)

-

Onshore

-

Offshore

-

-

Application Outlook (Capacity in MW; Revenue in USD Million, 2021 - 2033)

-

Utility

-

Non-Utility

-

-

Regional Outlook (Capacity in MW; Revenue in USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Russia

-

-

Asia Pacific

-

China

-

India

-

Australia

-

Japan

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

The global wind power market size was valued at USD 111.2 billion in 2025 and is estimated at USD 117.6 billion for 2026.

The global wind power market is expected to grow at a CAGR of 5.7% from 2026 to 2033, reaching USD 173.9 billion by 2033.

Asia Pacific dominated with a 44.9% revenue share in 2025.

Utility segment held the largest share (over 94.0%) in 2025, while non-utility is the fastest-growing application.

The onshore segment led with a 91.0% revenue share in 2025, while offshore is the fastest-growing location.

Key players include ABB; EDF power solutions; GE Vernova; Goldwind; Northland Power Inc.; Siemens Gamesa Renewable Energy; Sinovel Wind Group Co.; Suzlon Energy Limited; United Power; Vensys Energy AG; Vestas.

The key factors driving the growth of the global wind power market are increasing investments in renewable energy driven by decarbonization goals and supportive government policies. Advancements in turbine technology, improved efficiency, and declining installation and maintenance costs are further accelerating its adoption.

About the Author(s)

Renewable Energy Research Team

Energy & Power · Renewable EnergyThis report was authored by the renewable energy research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the renewable energy segment of the energy & power industry. All findings are based on proprietary energy & power databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.