- Home

- »

- Next Generation Technologies

- »

-

AI Detector Market Size, Share & Trends Report, 2026-2033GVR Report cover

![AI Detector Market (2026 - 2033)Report]()

AI Detector Market (2026 - 2033)

Size, Share & Trends Analysis Report By Solution (Platform API/SDKs), By Application (Academic Integrity, Content Verification, Deepfake and Synthetic Media Detection), By Detection Modality, By End Use, By Region, And Segment Forecasts

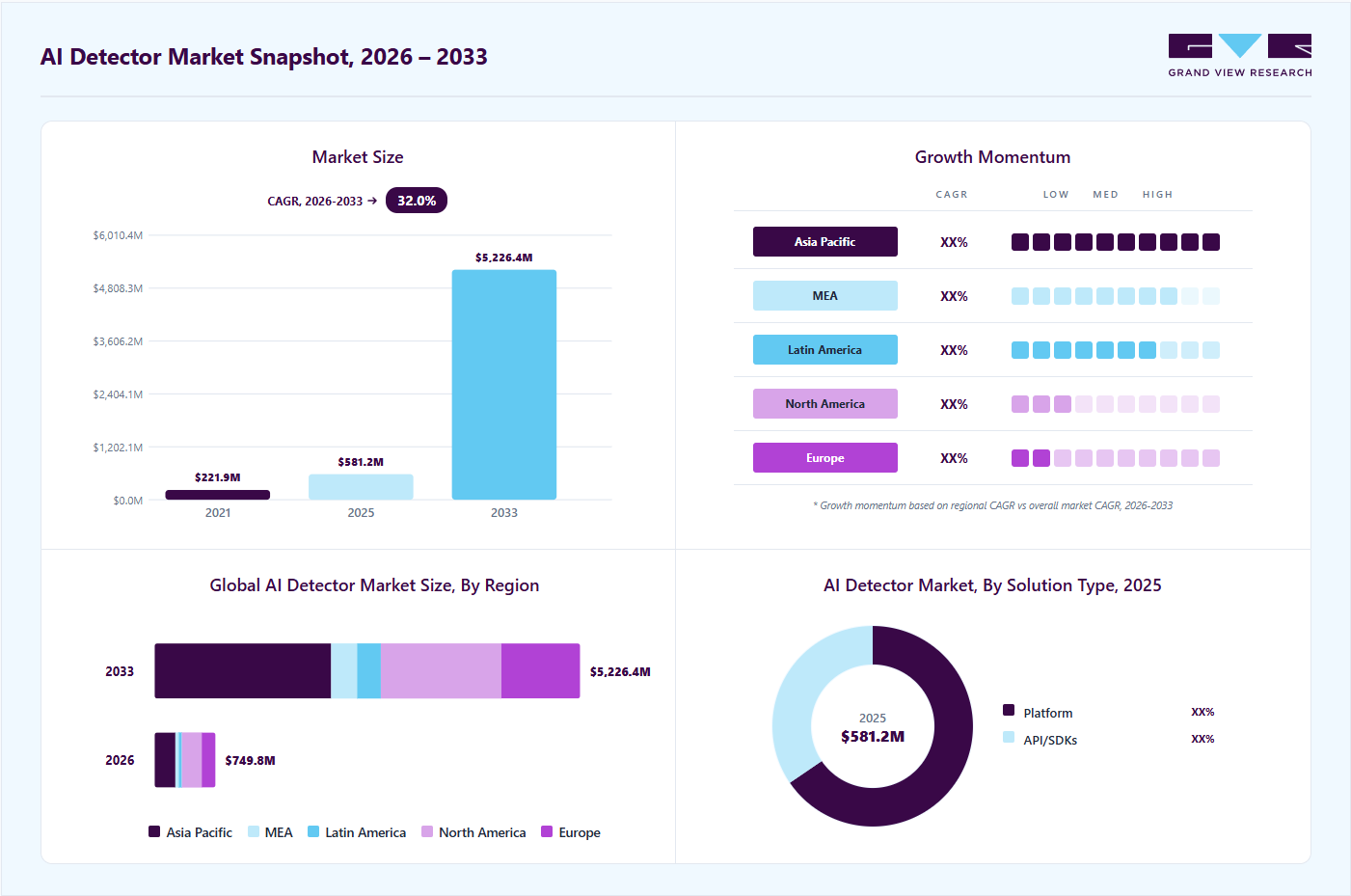

Market Size, 2025

$581.3MMarket Estimate, 2026

$749.8MMarket Forecast, 2033

$5,226.4MCAGR, 2026–2033

32.0%AI Detector Market Summary

The global AI detector market size was valued at USD 581.3 million in 2025 and is projected to grow from USD 749.8 million in 2026 to USD 5,226.4 million by 2033, at a CAGR of 32.0% from 2026 to 2033. North America dominated the global market with the largest revenue share of 33.2% in 2025. The market is driven by the rapid proliferation of generative AI content across education, media, and enterprises, increasing demand for tools that can verify content authenticity, identify AI-generated text and media, and support compliance with emerging digital transparency standards.

Key Market Trends & Insights

- By solution type: Platform segment dominated the market, with a revenue share of 65.5% in 2025.

- By application: Academic integrity segment held the largest market share of 24.9% in 2025.

- By detection modality: AI generated text segment hold the largest revenue share in 2025.

- By end use: Education segment hold the largest revenue share of 31.3% in 2025.

Regional Highlights

- Largest regional market: North America (33.2% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 581.3 Million

- Estimated market size in 2026: USD 749.8 Million

- Projected market size by 2033: USD 5,226.4 Million

- CAGR (2026-2033): 32.0%

The market is witnessing significant evolution as stakeholders focus on transparency, accountability, and compliance with ethical AI standards. Increasing regulatory inspection around content authenticity is compelling institutions and businesses to implement AI verification systems at scale. The market is also benefiting from partnerships between AI detection providers and major learning management and publishing platforms. As generative AI capabilities advance, the need for strong, explainable, and adaptive AI detection frameworks will remain critical to sustaining digital integrity.The market demand for solutions is increasing as organizations across sectors strive to maintain authenticity and credibility in digital content. With the propagation of generative AI tools, businesses, educators, and publishers are adopting detection technologies to identify and mitigate AI-generated misinformation as these systems are being deployed to uphold transparency, prevent plagiarism, and ensure accountability in AI-assisted workflows. As awareness of ethical AI practices rises globally, the adoption of AI detection solutions continues to accelerate across multiple domains.

")

The integration of advanced machine learning and linguistic models is transforming the AI detector industry, enabling more accurate identification of AI-generated content. Modern detection tools now use contextual analysis, natural language processing, and neural network-based algorithms to distinguish between human-written and synthetic text with higher precision. These advancements are enhancing user trust and improving workflow efficiency in education, journalism, and enterprise communication. The continuous innovation in AI model interpretability and explainability is expected to further strengthen market adoption.

Market Dynamics

The AI detector market is rising due to the rapid adoption of generative AI tools across education, enterprises, media, and digital platforms increases the need to verify content authenticity and identify AI-generated text, images, videos, and deepfakes. Organizations are deploying AI detection solutions to tackle misinformation, protect intellectual property, maintain academic integrity, and comply with emerging AI transparency regulations. The growing volume of synthetic content and rising concerns over fraud, reputational risks, and content credibility are driving demand for advanced detection technologies.

The widespread availability of generative AI tools has significantly increased the creation of realistic synthetic content, including text, images, audio, and videos that are often difficult to distinguish from authentic material. As AI-generated misinformation and deepfakes become more sophisticated, organizations, governments, media platforms, and educational institutions are facing growing challenges in maintaining content credibility and public trust. The potential misuse of synthetic media for fraud, impersonation, political manipulation, and reputational damage has elevated the need for reliable verification mechanisms.

AI detectors are increasingly being integrated into digital publishing platforms, social media networks, enterprise security systems, and academic environments to support authenticity verification and risk mitigation. This growing emphasis on safeguarding information integrity and reducing the impact of deceptive digital content continues to drive expansion of the AI detector market globally.

AI detector solutions often require access to large volumes of user-generated content, raising concerns about data privacy, consent management, and the handling of sensitive information. Educational institutions, enterprises, and government organizations are increasingly scrutinizing how detection platforms collect, store, and process content, particularly in regions governed by stringent data protection regulations. Compliance requirements can increase implementation complexity and operational costs for solution providers.

At the same time, ethical concerns surrounding content surveillance and automated decision-making create additional barriers to adoption. Incorrect classification of human-created content as AI-generated can lead to disputes, reputational damage, and questions regarding fairness and transparency. As organizations seek greater accountability in AI governance, vendors face growing pressure to establish explainable detection methodologies, strong data management practices, and clear compliance frameworks before large-scale deployment.

The widespread adoption of generative AI tools by students and researchers is creating a growing need for reliable content verification solutions across schools, colleges, and universities. Educational institutions are increasingly seeking AI detectors to help identify AI-generated assignments, essays, research papers, and examination responses while preserving academic integrity. As digital learning environments continue to expand, institutions require scalable verification tools that can be integrated directly into learning management systems and assessment platforms.

At the same time, educators are shifting toward balanced AI governance frameworks that highlight transparency and responsible AI usage rather than outright restrictions. This trend is creating opportunities for AI detector providers to offer advanced verification, authorship analysis, and content authenticity capabilities focused to academic workflows. Growing investments in digital education infrastructure and the establishment of institutional AI policies are expected to support sustained demand for AI content verification technologies across the education sector.

Market Concentration & Characteristics

Regulations have a moderately high impact on the AI detection market as governments and regulatory bodies introduce frameworks promoting AI transparency, accountability, and responsible AI usage. Emerging requirements for content disclosure, deepfake identification, and AI-generated media labeling are increasing demand for detection and verification technologies. Organizations are adopting AI detection solutions to support compliance efforts and reduce legal, reputational, and operational risks associated with synthetic content. The regulatory landscape is expected to become a significant driver of long-term market adoption across multiple industries.

The AI detection market has a moderately diversified end-user base, with demand emerging from education, media, publishing, cybersecurity, government, legal services, and enterprise sectors. No single end-user group dominates the market entirely, which helps distribute revenue opportunities across multiple industries. Educational institutions currently represent a significant adoption segment, while enterprise and government demand is expanding rapidly due to compliance and security requirements. This broadening customer base reduces dependence on any one sector and supports sustainable market growth over the forecast period.

Analyst Perspective

The AI detector market occupies a distinct position within the broader AI ecosystem because its growth is directly tied to the accelerating volume of AI-generated content rather than the adoption of AI models themselves. The defining competitive advantage, however, is unlikely to come from standalone detection accuracy, which continually degrades as generative models improve, but rather from the ability to integrate verification, provenance tracking, risk scoring, and governance workflows into a unified trust layer. Vendors that establish themselves as the system of record for digital authenticity across text, image, audio, and video ecosystems are positioned to capture the most durable value as AI-generated content becomes a permanent feature of the digital economy.

Solution Insights

Based on solution type, the platform segment led the market with the largest revenue share of 65.5% in 2025 and is expected to grow at the fastest CAGR over the forecast period, fueled by the growing need for integrated and scalable detection solutions. Enterprises are increasingly adopting platform-based systems that allow centralized management and consistent performance across text, image, audio, and code detection. The rise in generative AI adoption across industries is encouraging organizations to embed detection capabilities within their core digital operations. Platforms provide advantages such as automation, real-time analysis, and smooth integration with existing workflows, making them highly attractive for enterprise and institutional users.

The growing demand for the API/SDKs segment in the market is driven by the growing need to integrate detection tools directly into existing enterprise systems and digital platforms. Organizations are increasingly favoring modular, developer-friendly solutions that allow seamless embedding of AI detection across content management, education, and communication applications. This shift reflects the rising demand for flexibility, faster deployment, and reduced integration complexity compared to standalone solutions. Vendors offering robust SDKs and scalable APIs are attracting enterprise clients seeking real-time detection and compliance assurance within their operational workflows.

Application Insights

The academic integrity segment holds the largest share in the market in 2025, fueled by the rising use of generative AI tools among students for assignments and assessments. Educational institutions are rapidly deploying advanced detection systems to uphold originality, ensure fair evaluation, and maintain the credibility of academic qualifications. The increasing adoption of online and hybrid learning environments has further accelerated the demand for scalable, cloud-based AI detection solutions. Integration with learning management systems is becoming a key priority, allowing educators to monitor and verify content authenticity in real time.

The deepfake and synthetic media detection segment is expected to grow at the fastest CAGR in the coming years, driven by the increasing sophistication and accessibility of AI-generated audio, video, and image content. Organizations across media, government, and enterprise sectors are investing in advanced detection technologies to combat misinformation, identity fraud, and reputational risks. The surge in digital manipulation has intensified the demand for real-time, multimodal detection systems capable of analyzing visual and auditory data with high accuracy. Regulatory initiatives requiring content verification and labeling of AI-generated media are further accelerating adoption.

Detection Modality Insights

The AI generated text segment holds the highest share in the market in 2025, driven by the widespread adoption of large language models and text-based generative tools across industries. Organizations are increasingly relying on AI detectors to identify machine-generated essays, reports, articles, and communications to maintain authenticity and prevent misuse. The rapid integration of generative text tools in education, publishing, and corporate environments has heightened the need for reliable verification systems. Advancements in linguistic analysis and natural language processing are further enhancing detection accuracy and scalability.

The demand for AI-generated image and video detection solutions is rising, driven by the rapid spread of deepfake technology and synthetic visual media across digital platforms. Organizations are investing in advanced detection systems to identify manipulated visuals and safeguard brand reputation, security, and public trust. The proliferation of generative AI tools capable of producing highly realistic content has created an urgent need for authenticity verification in news, social media, and enterprise communication. Detection platforms leveraging computer vision, metadata analysis, and AI watermarking are gaining traction for their ability to deliver real-time, high-accuracy results.

End Use Insights

Based on end-use, the education segment led the market with the largest revenue share of 31.3% in 2025, propelled by the growing adoption of generative AI tools in student assignments and remote learning environments. Schools and universities are increasingly integrating detection systems with learning-management platforms to uphold academic integrity and prevent plagiarism from AI-generated text and code. Institutions are implementing scalable, cloud-based solutions to monitor real-time submission authenticity and ensure fair assessment practices. With regulatory and accreditation bodies tightening standards, the education sector is under pressure to maintain trust in credentials and learning outcomes.

The growing demand for AI detector solutions among software and technology providers is driven by the need to embed content authenticity checks directly into digital products and enterprise platforms. As generative AI models become widely integrated across applications, technology vendors are prioritizing built-in detection capabilities to ensure transparency, compliance, and trust. Software developers are leveraging APIs and SDKs to incorporate real-time detection for text, image, audio, and code generation within their ecosystems. This integration enables seamless monitoring and reduces the risk of synthetic content misuse across user-generated platforms and enterprise tools.

Regional Insights

North America dominated the AI detector market with the largest revenue share of 33.2% in 2025, owing to the increasing deployment of AI detection systems across universities, enterprises, and digital content platforms to uphold authenticity and originality. Educational institutions are integrating AI detection tools to maintain academic integrity amid the surge in generative AI usage. Enterprises are also leveraging these solutions to ensure transparency in marketing and customer communications. Growing awareness of AI-driven misinformation and data ethics continues to strengthen market expansion.

U.S. AI Detector Market Trends

The AI detector market in the U.S. held the largest share in the North America region in 2025, driven by the rising need for reliable AI content verification tools in education, journalism, and corporate governance. Institutions and enterprises are investing in advanced AI detectors to identify machine-generated or manipulated text with higher precision. Major technology providers are also integrating explainable AI features to improve detection accuracy and build user trust. Additionally, strong government support for AI transparency initiatives has reinforced the U.S. position as a global leader in this market.

Europe AI Detector Market Trends

The AI detector market in Europe is primarily driven by stringent regulatory mandates promoting responsible AI use and content accountability. The implementation of the EU AI Act has compelled organizations to adopt transparent AI detection mechanisms. Educational bodies and publishers are increasingly turning to AI detectors to comply with emerging digital content standards. This regulatory push, coupled with growing public concern over AI manipulation, is accelerating adoption across the region.

Asia Pacific AI Detector Market Trends

The AI detector market in the Asia Pacific is expected to grow at the fastest CAGR from 2026 to 2033. The demand is being fueled by the expanding digital education sector and the proliferation of generative AI tools across creative and academic domains. Governments in countries like China, Japan, and India are promoting AI ethics and data reliability frameworks that support the adoption of detection solutions. Furthermore, increasing awareness among students and professionals about the responsible use of AI-generated content is fostering significant market growth in the region.

Key AI Detector Company Insights

Some of the key companies in the market include Turnitin, GPTZero, Originality.AI, Copyleaks, and Hive Moderation.

-

Turnitin is one of the prominent players in academic integrity and AI-generated text detection solutions. The company’s AI writing detection technology is built to identify content produced or assisted by large language models such as ChatGPT. Turnitin’s solutions are deeply integrated into educational systems, helping instructors verify originality in student submissions. By combining decades of plagiarism detection experience with advanced AI analytics, Turnitin remains a cornerstone in educational content authenticity verification.

-

GPTZero is a pioneering platform specifically designed to detect AI-generated writing in real time. Developed originally for educators and publishers, it has become one of the most recognized AI text detection tools globally. GPTZero’s algorithms focus on perplexity and burstiness analysis, which measure predictability in language to determine whether content is machine-generated. The company continues to enhance detection precision by training its models on diverse datasets of human and AI-generated text.

Key AI Detector Companies:

The following key companies have been profiled for this study on the AI detector market.

- AI Detector Pro (AIDP)

- Copyleaks

- Crossplag

- GPTZero

- Hive Moderation

- Neuralwriter

- Originality.AI

- Reality Defender

- Sensity

- Sightengine

- Truepic

- Turnitin

- Writer.com

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Copyleaks GPTZero, Hive Moderation, Originality.AI, Reality Defender)

- Focus on enterprise contracts, institutional deployments, and API-based integrations across education, media, and corporate environments.

- Expand capabilities through multimodal detection, governance tools, compliance features, and ecosystem partnerships.

- Established customer bases, proprietary datasets, and extensive model training improve detection accuracy and scalability.

- Strong brand recognition and integration within existing enterprise and academic workflows support customer retention.

- Higher dependence on detection accuracy creates challenges as generative AI models evolve rapidly.

- Enterprise-focused business models often involve longer sales cycles and increasing customer expectations for reliability.

Emerging Players (AI Detector Pro (AIDP), Crossplag, Neuralwriter, Sensity)

- Target niche use cases such as plagiarism detection, deepfake identification, or content verification for specific customer groups.

- Emphasize rapid product development, flexible pricing models, and digital-first customer acquisition strategies.

- Greater agility in adopting new detection methodologies and responding to emerging AI-generated content trends.

- Ability to address specialized market requirements with focused product offerings and customized solutions.

- Limited brand visibility and smaller customer networks compared with established market participants.

- Resource constraints may affect research investments, dataset expansion, and large-scale enterprise penetration.

Recent Developments

-

In October 2025, BrowserStack launched its Accessibility Issue Detection AI Agent, designed to bring human-like intelligence to accessibility testing. It uses context-aware analysis of web and mobile interfaces to detect issues such as missing alt text, poor color contrast, and broken keyboard navigation. By integrating seamlessly into the development lifecycle, it allows teams to identify and address accessibility problems earlier in the process.

-

In August 2025, Turnitin expanded its AI writing detection capabilities by launching an advanced feature to identify content altered by AI bypasser or “humanizer” tools, which enables educators to detect not only AI-generated text but also material intentionally modified to evade detection systems. Integrated seamlessly into Turnitin Originality, the tool eliminates the need for external add-ons while ensuring comprehensive academic integrity checks.

-

In August 2025, Grammarly launched a suite of specialized AI agents integrated into its new AI-native “Docs” platform to enhance user productivity. The agents, including Citation Finder, AI Grader, Reader Reactions, and Expert Review, are designed to assist users with evidence sourcing, content evaluation, audience analysis, and expert-level feedback. This innovation eliminates the need for complex prompting by offering context-aware and task-specific support across academic and professional use cases.

-

In July 2025, Copyleaks introduced AI Logic, a transparency-focused AI detection feature. The solution employs AI Phrases and AI Source Match technologies to identify and explain AI-generated content within student submissions. This launch reinforces Copyleaks’ commitment to academic integrity by transforming AI detection into a learning-driven and collaborative process.

AI Detector Market Report Scope

Report Attribute

Details

Market size in 2025

USD 581.3 million

Estimated market size in 2026

USD 749.8 million

Projected market size by 2033

USD 5,226.4 million

Growth rate

CAGR of 32.0% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Solution, application, detection modality, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; South Africa; UAE

Key companies profiled

AI Detector Pro (AIDP); Copyleaks; Crossplag; GPTZero; Hive Moderation; Neuralwriter; Originality.AI; Reality Defender; Sensity; Sightengine; Truepic; Turnitin; Writer.com

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global AI Detector Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends and opportunities in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global AI detector market based on solution, application, detection modality, end use, and region:

-

Solution Outlook (Revenue, USD Million, 2021 - 2033)

-

Platform

-

API/SDKs

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Academic Integrity

-

Content Verification

-

Plagiarism Detection

-

Deepfake and Synthetic Media Detection

-

Code Authenticity Checking

-

Misinformation and Disinformation Detection

-

Others

-

-

Detection Modality Outlook (Revenue, USD Million, 2021 - 2033)

-

AI Generated Text

-

AI Generated Image & Video

-

AI Generated Audio & Voice

-

AI Generated Code

-

Multimodal

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Education

-

Media & Entertainment

-

Government & Defense

-

BFSI

-

Software & Technology Providers

-

Healthcare & Life Sciences

-

Legal

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Research Methodology

Segment Definition

Segment - Solution Type

Revenue capture definition

Platform

Platform solutions generate revenue by providing a centralized environment for AI-generated content detection across multiple content formats and user groups. Revenue capture is driven by subscription-based licensing, enterprise deployments, user-based pricing models, and premium analytics features.

API/SDKs

API and SDK solutions capture revenue by embedding AI detection capabilities directly into existing applications, workflows, and digital platforms. Monetization is commonly based on API call volumes, usage tiers, transaction-based pricing, and custom integration agreements that support scalable deployment across diverse end-use environments.

Segment - Application

Revenue capture definition

Academic Integrity

This segment captures revenue generated by educational institutions, certification bodies, and online learning platforms to evaluate the originality of student submissions and assessments. Revenue is derived from software subscriptions, institutional licenses, and integrated monitoring tools that support academic standards and assessment transparency.

Content Verification

Revenue in this segment originates from organizations that deploy AI detectors to validate the authenticity of digital content before publication or distribution. Demand comes from publishers, enterprises, and content platforms seeking to distinguish human-created material from AI-generated outputs across documents, articles, and multimedia assets.

Plagiarism Detection

This segment includes revenue generated from AI-powered plagiarism detection platforms that identify copied, paraphrased, or unoriginal content across academic, corporate, and publishing environments. Revenue streams are supported by subscription-based software, enterprise contracts, and integration with content management and learning systems.

Deepfake and Synthetic Media Detection

Revenue is captured from solutions designed to identify manipulated images, videos, and other synthetic media generated through artificial intelligence technologies. Adoption across media organizations, cybersecurity providers, and digital platforms contributes to spending on detection software and monitoring systems.

Code Authenticity Checking

This segment accounts for revenue from AI detection tools that assess the origin and authenticity of software code, including the identification of AI-generated programming content. Demand is generated by software development firms and enterprises focused on code quality, intellectual property protection, and compliance requirements.

Misinformation and Disinformation Detection

Revenue in this segment is derived from AI-powered solutions that analyze and flag false, misleading, or manipulated information distributed through digital channels. Media organizations, social platforms, governments, and enterprises invest in these tools to support content moderation, fact-checking operations, and information integrity initiatives.

Others

This segment encompasses revenue generated from specialized AI detection applications that do not fall within the primary categories, including document authentication, authorship verification, legal evidence validation, and industry-specific content analysis. Revenue is supported by niche deployments and customized solutions addressing unique organizational requirements.

Segment - Detection Modality

Revenue capture definition

AI Generated Text

Revenue for this segment is derived from platforms that identify and verify AI-generated written content across academic, enterprise, publishing, and regulatory environments. The segment includes subscriptions, API-based detection services, authorship verification tools, and content authenticity solutions used to assess text produced by large language models.

AI Generated Image & Video

This segment captures revenue generated from solutions that detect synthetic images, manipulated visuals, deepfakes, and AI-generated video content. Revenue contributions originate from media organizations, social platforms, and enterprises seeking visual content verification and digital trust capabilities.

AI Generated Audio & Voice

Revenue in this segment includes software and services designed to identify AI-generated speech, cloned voices, synthetic audio recordings, and manipulated voice content. Demand is supported by applications in fraud prevention, call center authentication, media verification, financial services, and public sector security operations.

AI Generated Code

This segment accounts for revenue generated through tools that analyze software code to determine whether it was created or significantly assisted by AI coding models. Revenue streams include code source solutions, software governance platforms, compliance monitoring tools, and enterprise development environment integrations.

Multimodal

Revenue is generated from platforms capable of simultaneously detecting AI-generated content across multiple formats, including text, images, audio, video, and code. Organizations adopt these solutions to establish unified content verification frameworks, simplify AI governance processes, and manage authenticity risks across diverse digital assets.

Segment - End Use

Revenue capture definition

Education

Revenue in the education segment is generated through AI detection platforms used by schools, universities, certification bodies, and online learning providers to assess content authenticity in assignments, examinations, and research submissions.

Media & Entertainment

Media organizations allocate budgets toward AI detection tools to verify the authenticity of images, videos, and audio content before publication and distribution. Revenue capture originates from content verification software, deepfake identification solutions, and digital trust platforms supporting editorial workflows.

Government & Defense

These organizations invest in AI detection technologies to identify manipulated content, misinformation campaigns, synthetic media, and fraudulent digital communications. Revenue is derived from software licensing, intelligence monitoring systems, and secure content authentication platforms.

BFSI

Banks, financial institutions, and insurance providers utilize AI detection solutions to identify synthetic documents, AI-generated fraud attempts, and to manipulate customer communications. Market revenue stems from enterprise contracts, fraud prevention platforms, compliance monitoring tools, and risk management applications.

Software & Detection Modality Providers

Software companies and technology vendors integrate AI detection into broader cybersecurity, governance, and trust frameworks. Revenue is captured through API-based services, white-label solutions, embedded detection engines, and software licensing agreements with enterprise customers.

Healthcare & Life Sciences

Healthcare providers and pharmaceutical companies deploy AI detection technologies to verify scientific content, medical documentation, and digitally generated research materials. Revenue is generated from compliance-focused verification solutions, research integrity platforms, and authentication tools supporting healthcare data governance.

Legal

Law firms, corporate legal departments, and compliance specialists adopt AI detection systems to validate legal documents, evidence records, contracts, and case-related content. Revenue capture comes from document verification platforms, forensic content analysis solutions, and legal risk assessment applications.

Others

The other category includes publishing, consulting, e-commerce, telecommunications, and non-profit organizations that use AI detection tools to maintain content credibility and reduce exposure to synthetic media risks. Revenue is generated through sector-specific deployments, enterprise subscriptions, and customized verification solutions addressing unique operational requirements.

Estimation Model

Layer Name

Key Questions

Description

Content Creation Layer

Who Generates Digital Content?

Identify organizations and individuals digital content - calculate the addressable base across diverse sectors, and digital platforms where AI-generated content is prevalent.

Who Deploys AI Detection Solutions?

How Many Vehicles Are Traded?

Apply AI detector adoption rates across industries and evaluate deployment within different industry workflows. Measure the proportion of organizations actively utilizing AI-generated content detection technologies.

Verification Layer

How Much Solutions Are Utilized?

Measure the frequency of AI content verification. Measure utilization levels based on recurring verification activities and risk management requirements.

Monetisation Layer

How Much Revenue Is Generated?

Apply the average spending per customer. Aggregate revenues across education, media, government, BFSI, legal, and enterprise deployments to estimate the total AI detector market size.

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Market Entry & Expansion Assessment

• Regional demand sizing and forecasting

• Customer segmentation and buying behavior analysis

• Competitive landscape benchmarking

• Regulatory and distribution channel assessment

Identified high-growth market opportunities

• Supported go-to-market strategy development

• Highlighted investment priorities and risks

• Enabled data-driven expansion planning

Technology & Innovation Assessment

• Emerging technology trend analysis

• Innovation pipeline

• Technology adoption readiness assessment

• Ecosystem and partnership mapping

• Identified future growth areas

• Supported roadmap planning innovation

• Evaluated commercialization potential

• Strengthened strategic partnership decisions

Product Positioning & Competitive Intelligence

• Product benchmarking and feature comparison

• Pricing and value proposition analysis

• Brand perception and customer preference study

• Competitor strategy evaluation

• Improved product differentiation strategy

• Supported pricing optimization

• Identified unmet customer needs

• Enhanced competitive positioning

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

Some key players operating in the AI Detector market include AI Detector Pro (AIDP); Copyleaks; Crossplag; GPTZero; Hive Moderation; Neuralwriter; Originality.AI; Reality Defender; Sensity; Sightengine; Truepic; Turnitin; Writer.com

Key factors driving market growth include the rising demand for AI-generated content verification, the increasing deployment of deepfake detection systems across enterprises, the growing regulatory focus on synthetic media transparency, and the expanding integration of AI detectors into cybersecurity and content moderation platforms.

The global AI detector market size was estimated at USD 581.3 million in 2025 and is expected to reach USD 749.8 million in 2026.

The global AI detector market is projected to grow at a compound annual growth rate (CAGR) of 32.0% from 2026 to 2033, reaching a value of USD 5,226.4 million by 2033.

North America dominated the AI detector market, with a share of over 33.2% in 2025, driven by the rapid adoption of content authenticity tools by enterprises, stringent regulatory scrutiny surrounding AI-generated media, and the accelerated integration of detection systems across cybersecurity and media verification workflows.

The Platform segment led with a 65.5% revenue share in 2025, while API/SDKs is the fastest growing segment.

Academic Integrity held the largest revenue share in 2025, while Deepfake and Synthetic Media Detection is the fastest growing segment.

The Education segment led with a 31.3% revenue share in 2025, while Software & Detection Modality Providers is the fastest growing segment.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.