- Home

- »

- Clinical Diagnostics

- »

-

Allergy Diagnostics Market Size, Share, Industry Report 2033GVR Report cover

![Allergy Diagnostics Market Size, Share & Trends Report]()

Allergy Diagnostics Market (2026 - 2033) Size, Share & Trends Analysis Report By Products & Services (Instruments, Consumables, Services), By Allergen (Food, Inhaled, Drug), By Test Type (In Vivo Test, In Vitro Test), By End-use, By Region, And Segment Forecasts

Market Size, 2025

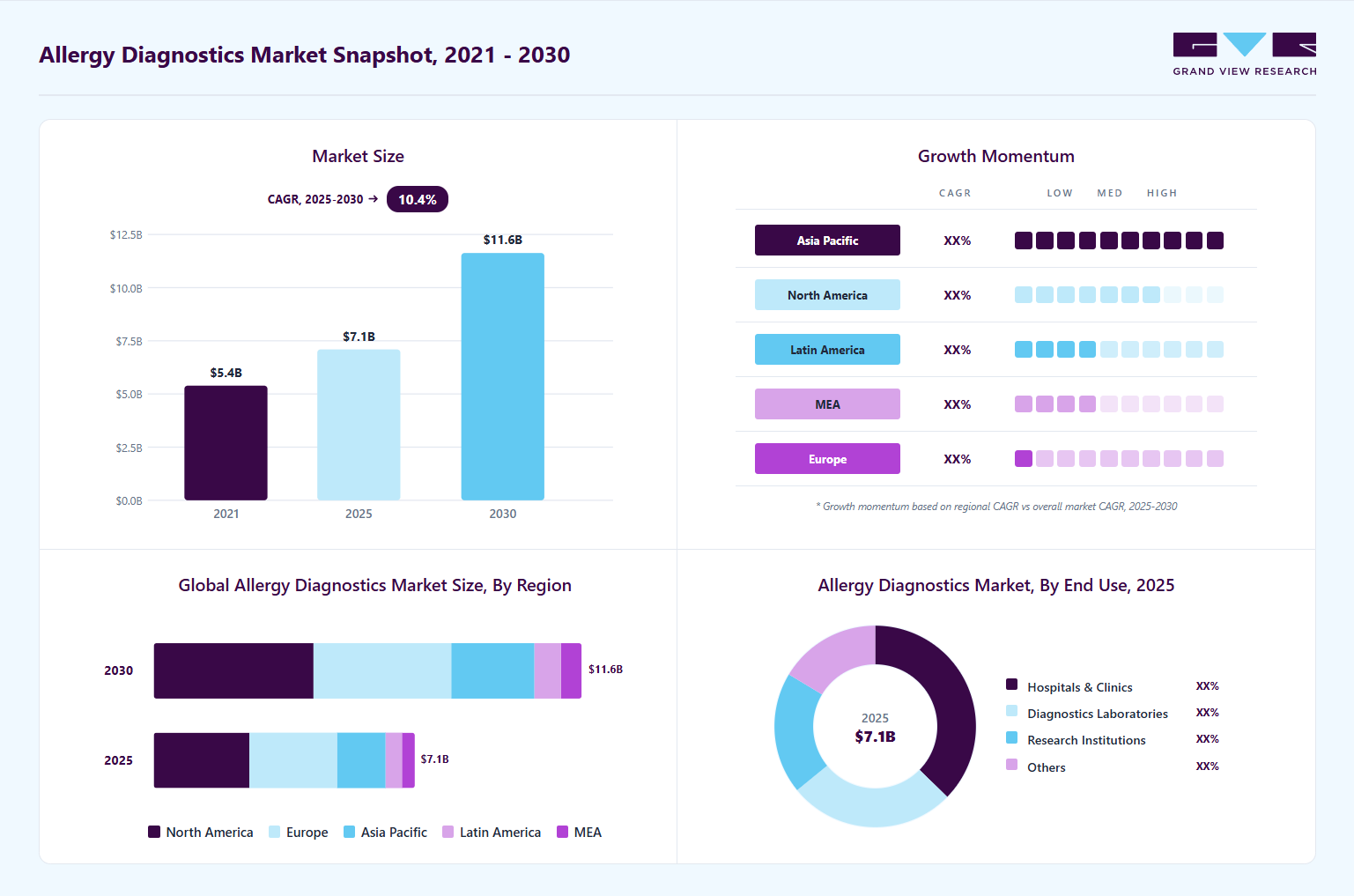

$7.1BMarket Estimate, 2026

$7.7BMarket Forecast, 2033

$16.4BCAGR, 2026–2033

11.3%Allergy Diagnostics Market Summary

The global allergy diagnostics market size was valued at USD 7.09 billion in 2025 and is projected to reach USD 16.37 billion by 2033, growing at a CAGR of 11.29% from 2026 to 2033. The growth is driven by the rising incidence of conditions such as allergic rhinitis, asthma, atopic dermatitis, and food allergies, which are becoming more common due to environmental pollution, urbanization, and lifestyle changes.

Key Market Trends & Insights

- North America allergy diagnostics market held the largest share of 36.62% of the global market in 2025.

- The allergy diagnostics industry in the U.S. is expected to grow significantly over the forecast period.

- By products and services, the consumables segment held the highest market share of 63.21% in 2025.

- By allergen, the inhaled segment held the highest market share in 2025.

- By test type, the in-vitro segment held the highest market share in 2025.

- By end use, hospitals & clinics held the highest market share in 2025.

Market Size & Forecast

- 2025 Market Size: USD 7.09 Billion

- 2033 Projected Market Size: USD 16.37 Billion

- CAGR (2026-2033): 11.29%

- North America: Largest market in 2025

- Asia Pacific: Fastest growing market

For instance, allergic rhinitis affects about 400 million individuals worldwide annually, impacting around 25% of children and 40% of adults. Furthermore, unhealthy habits, such as smoking, and urbanization, are some of the key factors contributing to the increasing incidence of allergic conditions.")

Market Dynamics

The increasing incidence of allergies is one of the key factors contributing to the market growth. Rising exposure to outdoor and indoor air pollutants and occupational exposure are among the high-risk factors causing chronic respiratory diseases. The prevalence of allergies is much higher in the urban population compared to rural areas due to rising exposure to environmental pollutants from industrial activities and urbanization.

According to data published by the Centers for Disease Control and Prevention in January 2026, approximately 3 in 10 adults and children in the United States reported having seasonal allergies, eczema, or food allergies in 2024. The report further indicated that 25.2% of U.S. adults experienced seasonal allergies, while nearly 7% of adults and 5% of children were affected by food allergies. The increasing prevalence of allergic conditions across both pediatric and adult populations is contributing to higher demand for advanced allergy diagnostics, including specific IgE testing, multiplex allergen assays, and molecular allergy profiling technologies across North America.

Technological innovations are significantly enhancing the allergy diagnostics landscape. Advancements such as component-resolved diagnostics (CRD), multiplex assays, and the integration of artificial intelligence (AI) are enabling more precise allergen identification and personalized treatment plans. The IVD tests offer increased accuracy, reduced invasiveness, and improved patient comfort, making them a preferred choice over traditional skin prick tests. Additionally, the development of at-home and point-of-care testing kits is expanding access to allergy diagnostics, particularly in remote and underserved areas.

The market's expansion is also supported by increased healthcare spending and strategic initiatives by key players. Global healthcare spending is projected to reach USD 10.2 trillion by 2025, with a significant portion allocated to treating chronic diseases like allergies. Companies are investing in research and development to create innovative diagnostic products, such as AI-powered testing solutions, to address unmet medical needs.

Limited accessibility to advanced technologies remains a significant restraint, particularly across low- and middle-income countries and rural healthcare settings where access to specialized diagnostic infrastructure is limited. Advanced allergy diagnostic platforms such as component-resolved diagnostics (CRD), multiplex immunoassays, molecular allergen profiling, and automated immunoassay systems require high capital investment, sophisticated laboratory infrastructure, and trained healthcare professionals for accurate interpretation and operation. Smaller hospitals, community clinics, and decentralized laboratories often lack the financial and technical capabilities required to adopt these technologies, resulting in continued dependence on conventional skin prick testing and basic IgE assays with lower diagnostic precision.

The growing adoption of precision allergy diagnostics presents a strong opportunity for the industry. Healthcare providers are increasingly shifting toward component-resolved diagnostics (CRD), multiplex allergen testing, and molecular allergy profiling technologies that provide highly accurate identification of specific allergen sensitivities and cross-reactive allergens. These advanced diagnostic approaches improve clinical decision-making, support personalized immunotherapy selection, and reduce the risk of misdiagnosis associated with conventional testing methods. Rising prevalence of food allergies, asthma, and allergic rhinitis, combined with increasing awareness regarding early allergy detection and personalized treatment strategies, is expected to accelerate demand for technologically advanced allergy diagnostic solutions across hospitals, laboratories, and specialty clinics globally.

Market Concentration & Characteristics

The industry demonstrates a high degree of innovation, driven by the rapid development of molecular diagnostics, multiplex assays, and the integration of digital health technologies such as artificial intelligence (AI). For example, in February 2025, Swiss biotech startup ATANIS Biotech secured a USD 2 million grant from FARE (Food Allergy Research & Education) after winning Phase 2 of its Innovation Award Diagnostic Challenge. The funding will support the commercialization of ATANIS's FAST-PASE allergy test, an innovative ex vivo mast cell activation assay designed to safely and accurately diagnose food allergies without the risks associated with traditional oral food challenges. Clinical studies have demonstrated over 95% accuracy for peanut allergy detection. ATANIS is collaborating with leading institutions, including Mount Sinai and SickKids Toronto, to advance the test's development across multiple allergy indications.

The industry experiences a high level of mergers and acquisitions (M&A), as major players seek to broaden their technological capabilities, enhance their product portfolios, and enter new regional markets. Several market players are acquiring smaller players to strengthen their market position. This strategy enables companies to increase their capabilities, expand their product portfolios, and improve their competencies. Key players engaged in this growth strategy. For instance, in 2023, Thermo Fisher Scientific acquired The Binding Site Group, a leader in specialty diagnostics, including allergy testing, to enhance its immunodiagnostics segment and strengthen its global footprint. These activities highlight how M&A is a core strategy for companies to diversify offerings, integrate innovative platforms, and capture greater market share in the evolving allergy diagnostics landscape.

Regulatory frameworks play a pivotal role in shaping the industry by ensuring patient safety, efficacy, and accuracy of diagnostic products. The U.S. FDA, European CE marking, and local regulatory bodies have set stringent standards for allergy testing kits, particularly molecular and at-home diagnostics. In 2025, the European Union updated its In Vitro Diagnostic Regulation (IVDR), intensifying compliance requirements for allergy diagnostic products, thereby pushing companies to invest in rigorous clinical validation and post-market surveillance. These regulatory pressures are driving innovation while simultaneously raising entry barriers for new players, ensuring that only high-quality, reliable diagnostic tools enter the market.

Product expansion is at a high level in the industry, with companies diversifying their offerings to cover a broader range of allergens, including food, inhalants, and drug allergies. For instance, in October 2024, ALK, a Denmark-based pharmaceutical company specializing in allergy prevention and treatment, received U.S. FDA approval for its AccuTest line of allergy skin testing devices and allergen trays. The AccuTest-1 is a single-prick device, while the AccuTest-8 and AccuTest-10 are multi-head applicators with eight and ten heads, respectively. These devices feature smaller tine lengths and diameters to enhance precision and minimize patient discomfort. Additionally, the AccuTest 48-well and 60-well allergen trays are designed with air-tight locking mechanisms and non-slip rubber bottoms to prevent contamination and ensure stability during testing procedures. This aggressive product expansion strategy is helping companies cater to the growing demand for personalized and precise allergy management.

The industry is witnessing a medium to high level of regional expansion as companies aim to tap into growth opportunities in emerging markets while solidifying their presence in established regions. Asia-Pacific, Latin America, and the Middle East are becoming key targets. In 2023, Thermo Fisher Scientific expanded its allergy testing portfolio in China and India, recognizing the large, underserved population suffering from allergic diseases. Similarly, EUROIMMUN (a PerkinElmer company) launched new regional collaborations in Brazil and the Gulf Cooperation Council (GCC) countries, aiming to penetrate emerging markets with high growth potential. This strategic regional expansion is enabling companies to capitalize on the growing demand for allergy diagnostics in developing economies, while consolidating their position in established markets.

Products and Services Insights

Consumables held the largest share of 63.42% of the market in 2025. This segment comprises critical components such as allergen extracts, assay kits, and reagents that are indispensable for both in vitro and in vivo testing. The continuous, repeatable nature of allergy testing in clinical settings drives steady demand for consumables. Moreover, the expanding allergy testing menu and inclusion of new allergens further augment the demand for consumables.

Instruments are expected to grow at the substantial rate over the forecast period, supported by the adoption of automated diagnostic platforms that improve laboratory efficiency, throughput, and diagnostic accuracy. Automation is increasingly being integrated into allergy diagnostics to support high-volume testing and standardized results, which is especially crucial in large diagnostic networks. A key development in this space is the April 2025 launch of Beckman Coulter Life Sciences' Basophil Activation Test (BAT), which provides laboratories with a novel, highly sensitive method for identifying IgE-mediated allergic reactions using flow cytometry, further modernizing allergy diagnostics workflows.

Allergen Insights

Inhaled allergen type accounted for the largest revenue share of the market in 2025, driven by the high prevalence of conditions such as asthma, allergic rhinitis, and allergic conjunctivitis caused by allergens like pollen, dust mites, and mold spores. Urbanization, rising pollution levels, and climate change are intensifying the burden of inhaled allergens globally. On July 29, 2024, AliveDx received the IVDR CE mark for its microarray immunoassay, marking its inaugural entry into allergy diagnostics. This assay, designed to detect specific IgE antibodies targeting protein allergens in human serum, operates on AliveDx’s proprietary MosaiQ platform. The multiplex immunoassay microarray enables the simultaneous detection of over 30 allergens, encompassing both inhalant and food allergens, thereby streamlining laboratory workflows and reducing diagnostic time.

Food allergens are expected to grow at a substantial rate over the forecast period. Growing pediatric populations and increased food allergy prevalence in both developed and emerging countries are contributing to this trend. A significant regulatory milestone in this area includes Thermo Fisher Scientific's 2022 FDA approval for its ImmunoCAP tests for wheat and sesame allergens, providing clinicians with reliable tools to differentiate between true wheat allergy and cross-reactivity with grass pollen, thereby avoiding unnecessary dietary restrictions. Companies such as 3M offer Allergen Protein Rapid Test Kits: These lateral flow assays provide quick, qualitative detection of specific food allergens such as almond, peanut, pecan, walnut, and gluten. They are suitable for monitoring allergens in raw ingredients, finished products, and environmental samples, delivering results in approximately 10-12 minutes.

Test Type Insights

In Vitro Test dominated the market in 2025, propelled by its convenience, reproducibility, and safety, particularly in patients where skin tests may pose risks. The growing preference for blood-based assays such as specific IgE tests, component-resolved diagnostics (CRD), and basophil activation tests reflects the market’s move toward minimally invasive, standardized diagnostics.

The In Vivo Test segment is anticipated to grow at the fastest rate over the forecast period. This segment encompasses skin prick tests (SPT), intradermal tests, and patch tests, and is poised for accelerated adoption, especially in outpatient clinics where immediate reactions can be visually assessed. Technological refinements in test devices, combined with clinical protocols integrating both in vitro and in vivo tests, are enhancing diagnostic precision and patient experience. Growth is further attributed to increasing adoption of several in vivo tests having convenient, cost-effective, safe & reliable properties than that of others. Growing demand for rapid, simple, and efficient testing has fueled the growth of in vivo diagnostic tests. These tests look at the susceptibility and reactivity of dermal mast cells, which can indicate allergic sensitivity. To ensure reliability, these procedures include skin exams with standardized allergenic extracts.

End-use

Hospitals & clinics accounted for the largest revenue share of the market in 2025. These settings are central to allergy diagnosis, management, and treatment planning, offering both diagnostic services and immunotherapy interventions under one roof. The rising prevalence of allergic diseases, combined with the availability of advanced diagnostic modalities, supports the sustained growth of this segment.

The research institutions segment is expected to grow at the highest CAGR during the forecast period. Academic and research centers are increasingly conducting translational research in allergy diagnostics, focusing on novel biomarkers, molecular allergens, and personalized diagnostic approaches. Notable partnerships between diagnostic companies and research entities, such as Allergy Partners' 2022 collaboration with Aimmune Therapeutics to expand access to PALFORZIA through its network of clinics, are fostering innovation at the interface of diagnostics, therapeutics, and clinical research. This synergy is accelerating the development of next-generation allergy diagnostic tools and expanding the understanding of allergy pathophysiology.

Regional Insights

North America dominated the allergy diagnostics market and accounted for a 36.62% share in 2025, supported by the rising prevalence of food allergies, allergic rhinitis, asthma, and atopic dermatitis across the United States and Canada. The region benefits from high awareness regarding early allergy diagnosis, strong reimbursement coverage, and widespread adoption of advanced diagnostic technologies such as component-resolved diagnostics (CRD), multiplex allergen testing, and automated immunoassay systems across hospitals and specialty laboratories. For instance, in May 2023, Thermo Fisher Scientific expanded its ImmunoCAP allergy diagnostics portfolio in the United States by introducing advanced molecular allergen testing capabilities designed to improve identification of specific allergen sensitizations and support precision allergy management in clinical laboratories. Such developments strengthen the adoption of technologically advanced allergy testing solutions across North America.

U.S. Allergy Diagnostics Market Trends

The allergy diagnostics market in the U.S. is propelled by rising prevalence of allergies, advanced biotechnology infrastructure, strong government support, and significant private investments. Government-backed initiatives aimed at allergy awareness, along with a rise in self-reported allergic conditions, are further supporting the uptake of both in vitro and point-of-care allergy tests. In the United States, over 50 million people experience allergies annually, making it the sixth most common cause of chronic illness. This includes seasonal allergies (affecting 25.7% of adults and 18.9% of children), eczema (7.3% of adults), and food allergies (6.2% of adults and 5.8% of children), according to the CDC. Specifically, seasonal allergic rhinitis, also known as hay fever, affects 67 million adults and 14 million children annually. In May 2022, Thermo Fisher Scientific announced the U.S. availability of its Phadia 2500+ series of instruments, expanding its application to include autoimmune testing alongside allergy diagnostics. These high-capacity, automated systems are designed to enhance laboratory efficiency by enabling the simultaneous processing of EliA autoimmune and ImmunoCAP allergy tests on a single platform.

Europe Allergy Diagnostics Market Trends

The allergy diagnostics market in Europe is rapidly evolving, driven by the increasing clinical emphasis on accurate identification of environmental and food-related allergens. The region benefits from the support of harmonized regulatory policies that encourage the adoption of advanced diagnostic assays, while lifestyle shifts and pollution are contributing to the growing allergy burden. The European Academy of Allergy and Clinical Immunology (EAACI) estimates that over 150 million Europeans suffer from chronic allergic diseases, and by 2025, more than 50% of all Europeans will suffer from at least one type of allergy, with no age, social, or geographical distinction. Regulatory frameworks, such as IVDR, support the introduction of innovative diagnostic assays across the region. Key players, including Thermo Fisher Scientific, EUROIMMUN (PerkinElmer), and Stallergenes Greer, are actively expanding their offerings through partnerships, product launches, and digital integration, focusing on high-throughput and multiplex testing to meet the growing demand for precision diagnostics.

The UK allergy diagnostics market is experiencing significant growth, driven by a growing need for accurate allergy detection tools, particularly among pediatric populations affected by food and respiratory allergies. The NHS’s integration of allergy services in primary care and hospitals has further strengthened the demand for reliable and accessible testing platforms. Approximately 44% of the UK's adult population and up to 40% of children experience at least one allergy, driving demand for accurate testing solutions. The market is led by companies such as Omega Diagnostics and Lincoln Diagnostics, with a focus on improving point-of-care testing and home-based allergy testing services.

The allergy diagnostics market in Germany is influenced by the high demand for precision testing in both private and public healthcare settings. The availability of comprehensive allergy panels and molecular-level diagnostic technologies is fostering the growth of personalized allergy management practices across the country. Companies such as Siemens Healthineers, HOB Biotech, and AESKU.GROUP are key contributor to the market, leveraging automation, molecular panels, and component-resolved diagnostics to expand their clinical utility and reach both private and public health settings.

Asia Pacific Allergy Diagnostics Market Trends

The allergy diagnostics market in Asia Pacific is anticipated to witness significant growth, driven by rising urbanization, lifestyle changes, and environmental pollution. Increased focus on preventive healthcare and growing awareness regarding food and respiratory allergies have created fertile ground for companies to introduce technologically advanced yet affordable diagnostic solutions. Expanding healthcare infrastructure, improving access to diagnostic services, and rising awareness regarding early allergy detection are accelerating adoption of allergy testing across hospitals, diagnostic laboratories, and specialty clinics. Governments and healthcare organizations across the region are also increasing focus on preventive healthcare and chronic respiratory disease management, supporting demand for advanced allergy diagnostics. For instance, in October 2025, Sysmex Corporation collaborated with regional healthcare institutions in Japan and Southeast Asia to expand the availability of automated allergy testing solutions and multiplex immunoassay technologies aimed at improving the detection of respiratory and food allergens in clinical laboratories. Such initiatives support wider accessibility of advanced allergy diagnostics across Asia Pacific and contribute to regional market growth.

China allergy diagnostics market held a substantial share in 2025. The market is advancing steadily due to a combination of rising allergy prevalence, especially among children, and government-led public health programs emphasizing early diagnosis. The market also benefits from domestic investments in local manufacturing and distribution networks to improve accessibility.

The allergy diagnostics market in Japan is growing steadily, reflecting a preference for high-precision diagnostic solutions, with an emphasis on in vitro testing. The country’s aging population, coupled with an increase in allergic conditions like asthma and atopic dermatitis, is propelling the demand for sophisticated allergy detection tools.

Latin America Allergy Diagnostics Market Trends

The allergy diagnostics market in Latin America is witnessing increasing attention due to collaborative efforts and government initiatives. Increasing environmental pollution and evolving dietary patterns have contributed to a rise in allergy incidence across the region.

The Brazil allergy diagnostics market is witnessing substantial growth, fueled by expanding healthcare services and improved patient awareness. The country is witnessing greater acceptance of laboratory-based allergy tests in both urban and semi-urban areas, supporting market expansion.

Middle East & Africa Allergy Diagnostics Market Trends

The allergy diagnostics market in the Middle East and Africa (MEA) is poised for growth due to the increasing prevalence of respiratory allergies, asthma, allergic rhinitis, and food allergies across urban populations. Rising healthcare investments, expanding private diagnostic laboratory networks, and improving awareness regarding early allergy identification are supporting market development across countries such as the UAE, Saudi Arabia, and South Africa. The growing demand for specialized allergy services is encouraging both local and international players to invest in improving testing infrastructure and expanding access to advanced immunoassay and molecular allergy diagnostic technologies. In addition, increasing air pollution, desert dust exposure, and climate-related allergen sensitivity across several Middle Eastern countries are contributing to higher demand for respiratory allergy testing. Expansion of multispecialty hospitals and diagnostic centers equipped with automated laboratory systems is further expected to support the adoption of allergy diagnostics across the MEA region.

The Saudi Arabia allergy diagnostics market is experiencing robust growth, marked by increasing public and private sector investments in healthcare infrastructure. The growing burden of food and respiratory allergies, particularly among younger populations, has intensified the demand for accessible and accurate allergy diagnostics.

Key Allergy Diagnostics Company Insights

The allergy diagnostics market is driven by a cohort of specialized diagnostics and biotechnology companies that are advancing the field through continuous innovation, technological advancements, strategic partnerships, and portfolio expansion across in vitro and in vivo allergy testing.

These companies are at the forefront of developing advanced allergy diagnostic solutions such as immunoassays, molecular allergy diagnostics, skin prick testing devices, and point-of-care testing platforms, addressing both respiratory and food allergies. For instance, in April 2025, Beckman Coulter Life Sciences announced the launch of its next-generation Basophil Activation Test (BAT), designed to enhance food allergy research by providing a safer and more efficient alternative to traditional testing methods. Similarly, HYCOR Biomedical continues to innovate with its NOVEOS System, focusing on automation and improved sensitivity in allergy testing. These ongoing innovations, coupled with strategic collaborations and regulatory approvals, are expected to drive significant advancements in the market, enabling earlier detection, better differentiation of allergens, and improved patient outcomes.

Key Allergy Diagnostics Companies:

The following key companies have been profiled for this study on the allergy diagnostics market.

- Thermo Fisher Scientific, Inc.

- HYCOR Biomedical

- EUROIMMUN Medizinische Labordiagnostika AG (PerkinElmer, Inc.)

- Omega Diagnostics Group PLC

- Lincoln Diagnostics, Inc.

- AESKU.GROUP GmbH

- Minaris Medical America, Inc.

- HOB Biotech Group Corp., Ltd.

- DASIT Group SPA

- R-Biopharm AG

- bioMérieux

- Siemens Healthcare GmbH

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Thermo Fisher Scientific; EURIMMUN Medizinische Labordiagnostika AG; bioMérieux; Siemens Healthineers; R-Biopharm AG; DASIT Group SPA

- Expansion of multiplex and component-resolved allergy diagnostics to improve allergen identification and diagnostic precision.

- Investment in automated immunoassay platforms and digital laboratory workflows to enhance testing efficiency.

- Strategic partnerships and regional expansion initiatives to strengthen accessibility across emerging healthcare markets.

- Strong global distribution networks and extensive installed base across hospitals and diagnostic laboratories.

- Broad allergy testing portfolios supported by regulatory approvals and advanced automation capabilities.

- High investment capacity for molecular diagnostics, R&D expansion, and strategic acquisitions.

- High pricing of advanced allergy diagnostic systems limits adoption in cost-sensitive healthcare markets.

- Complex regulatory compliance and large operational structures can slow product commercialization timelines.

- Dependence on centralized laboratory infrastructure reduces accessibility in decentralized healthcare settings.

Emerging Players: HYCOR Biomedical; Omega Diagnostics Group PLC

- Focus on cost-effective and flexible allergy testing platforms targeting regional laboratories and specialty clinics.

- Expansion through partnerships, localized distribution networks, and niche allergen testing portfolio development.

- Investment in decentralized and point-of-care allergy diagnostics to improve accessibility in underserved markets.

- Flexible and customizable allergen testing solutions targeting niche and regional diagnostic requirements.

- Faster adoption of innovative multiplex and point-of-care allergy diagnostic technologies.

- Cost-effective platforms improving accessibility across smaller laboratories and emerging healthcare markets.

- Limited global distribution networks and lower brand recognition compared to multinational competitors.

- Restricted financial resources for large-scale R&D, regulatory approvals, and commercialization activities.

- Smaller product portfolios and limited installed base reduce long-term recurring revenue generation.

Recent Developments

-

In April 2025, Beckman Coulter Life Sciences announced the launch of its next-generation Basophil Activation Test (BAT), a significant advancement in allergy research. This new assay offers a safer and more efficient alternative to traditional oral food challenges (OFCs), which often carry risks of severe allergic reactions.

-

In February 2025, Swiss biotech startup ATANIS Biotech secured a USD 2 million grant from FARE (Food Allergy Research & Education) after winning Phase 2 of its Innovation Award Diagnostic Challenge. The funding will support the commercialization of ATANIS's FAST-PASE allergy test, an innovative ex vivo mast cell activation assay designed to safely and accurately diagnose food allergies without the risks associated with traditional oral food challenges.

-

In October 2025, ALK, a Denmark-based pharmaceutical company specializing in allergy prevention and treatment, received U.S. FDA approval for its AccuTest line of allergy skin testing devices and allergen trays. The AccuTest-1 is a single-prick device, while the AccuTest-8 and AccuTest-10 are multi-head applicators with eight and ten heads, respectively.

Allergy Diagnostics Market Report Scope

Report Attribute

Details

Market size value in 2026

USD 7.74 billion

Revenue forecast in 2033

USD 16.37 billion

Growth rate

CAGR of 11.29% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Products and services, allergen, test type, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico ;UK; Germany; France; Spain; Italy; Sweden; Denmark; Sweden; Norway; Japan; China; India; South Korea; Australia; Thailand; Brazil ; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Thermo Fisher Scientific, Inc.; HYCOR Biomedical; EUROIMMUN Medizinische Labordiagnostika AG (PerkinElmer, Inc.); Omega Diagnostics Group PLC; Lincoln Diagnostics, Inc.; AESKU.GROUP GmbH; Minaris Medical America, Inc.; HOB Biotech Group Corp., Ltd.; DASIT Group SPA; R-Biopharm AG; bioMérieux; Siemens Healthcare GmbH.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Allergy Diagnostics Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global allergy diagnostics market report based on products and services, allergen, test type, end use, and region:

-

Products and Services Outlook (Revenue, USD Million, 2021 - 2033)

-

Instruments

-

Consumables

-

Services

-

-

Allergen Outlook (Revenue, USD Million, 2021 - 2033)

-

Food

-

Dairy Products

-

Poultry Product

-

Tree Nuts

-

Peanuts

-

Shellfish

-

Wheat

-

Soys

-

Other Food Allergens

-

-

Inhaled

-

Drug

-

Other Allergens

-

-

Test Type Outlook (Revenue, USD Million, 2021 - 2033)

-

In Vivo Test

-

Skin Prick Test

-

Intradermal Test

-

Patch Test

-

-

In vitro Test

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals & Clinics

-

Diagnostics Laboratories

-

Research Institutions

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Spain

-

Italy

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Supply Chain & Sourcing Analysis

Detailed analysis of raw material sourcing locations, supplier network, logistics flow, lead-time challenges, and regional supply risks. Includes assessment of supplier dependency and disruption impact across key markets.

Helps identify supply chain vulnerabilities, improve procurement planning, reduce sourcing risks, and strengthen operational stability.

Online Sales & D2C Channel Analysis

Evaluation of competitor D2C platforms, e-commerce presence, digital visibility, online sales trends, subscription models, and marketplace performance across regions.

Identifies digital growth opportunities, improves online sales strategy, and supports expansion across e-commerce and direct-to-consumer channels.

Customer Buying Behavior Analysis

Assessment of customer purchase journey across awareness, consideration, purchase, and loyalty stages. Includes analysis of buying factors, preferred channels, and consumer engagement trends.

Helps optimize marketing strategy, improve customer targeting, and increase conversion and retention rates.

Emerging Technology Adoption Analysis

Analysis of AI, automation, IoT, digital platforms, and advanced technologies adopted by competitors across manufacturing, diagnostics, logistics, and commercial operations.

Tracks competitive technology trends, identifies innovation gaps, and supports future investment and digital transformation planning.

Frequently Asked Questions About This Report

The market is driven by rising incidence of conditions such as allergic rhinitis, asthma, atopic dermatitis, and food allergies, which are becoming more common due to environmental pollution, urbanization, and lifestyle changes.

Some key players operating in the allergy diagnostics market include Thermo Fisher Scientific, Inc.; HYCOR Biomedical; EUROIMMUN Medizinische Labordiagnostika AG (PerkinElmer, Inc.); Omega Diagnostics Group PLC; Lincoln Diagnostics, Inc.; AESKU.GROUP GmbH; Minaris Medical America, Inc.; HOB Biotech Group Corp., Ltd.; DASIT Group SPA; R-Biopharm AG; bioMérieux; Siemens Healthcare GmbH.

The global allergy diagnostics market size was estimated at USD 7.09 billion in 2025 and is expected to reach USD 7.74 billion in 2026.

The global allergy diagnostics market is expected to grow at a compound annual growth rate of 11.29% from 2026 to 2033 to reach USD 16.37 billion by 2033.

North America dominated the allergy diagnostics market and accounted for a 36.62% share in 2025, The increasing prevalence of food allergies, coupled with high awareness among patients and clinicians, drives demand for innovative diagnostic solutions

About the Author(s)

Clinical Diagnostics Research Team

Healthcare · Clinical DiagnosticsThis report was authored by the clinical diagnostics research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clinical diagnostics segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.