- Home

- »

- Plastics, Polymers & Resins

- »

-

Beer Packaging Market Size And Share Report, 2026-2033GVR Report cover

![Beer Packaging Market (2026 - 2033)Report]()

Beer Packaging Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material (Glass, Plastic, Metal), By Product (Bottles, Cans, Kegs), By End Use (Breweries, Restaurants & Bars, Liquor Stores), By Region, And Segment Forecasts

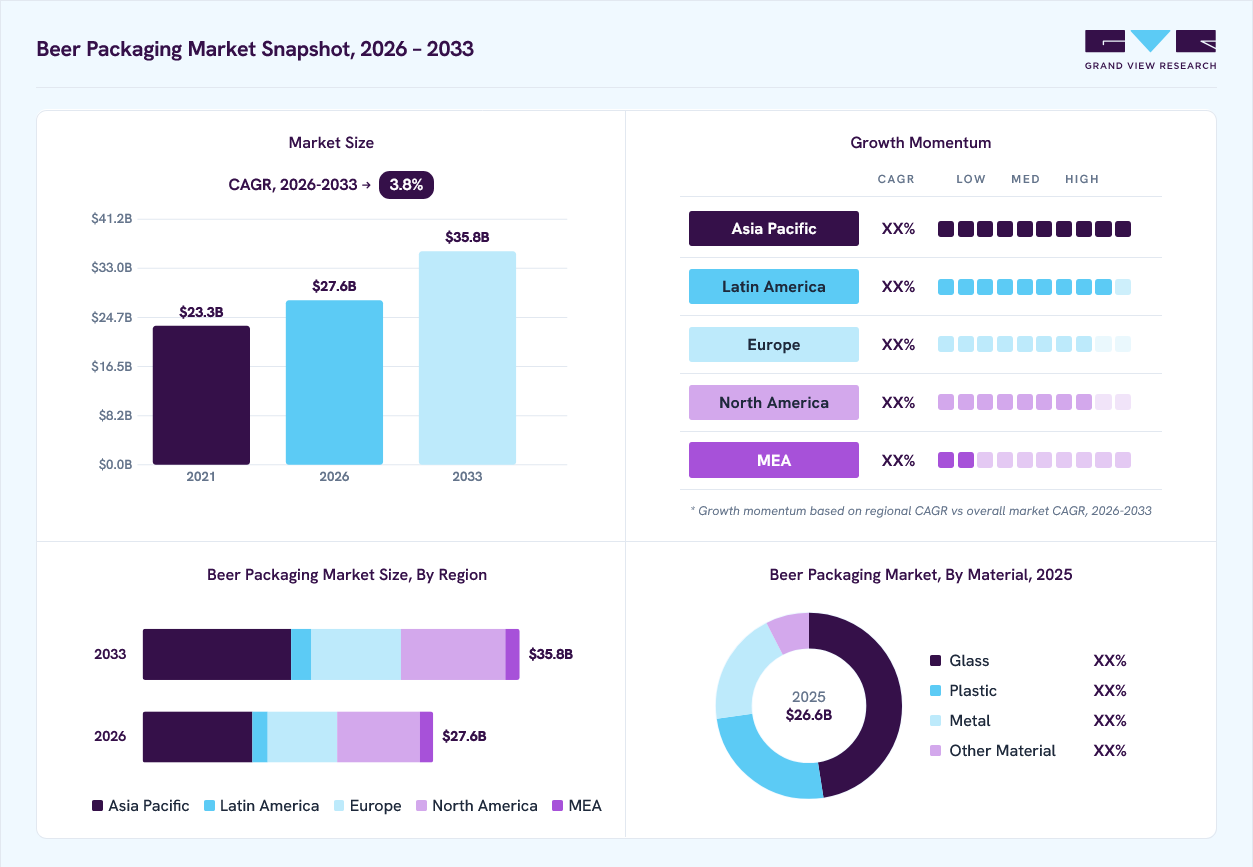

Market Size, 2025

$26.6BMarket Estimate, 2026

$27.6BMarket Forecast, 2033

$35.8BCAGR, 2026–2033

3.8%Beer Packaging Market Summary

The global beer packaging market size was valued at USD 26.6 billion in 2025 and is projected to grow from USD 27.6 billion in 2026 to USD 35.8 billion by 2033, at a CAGR of 3.8% from 2026 to 2033. Asia Pacific dominated the beer packaging market with the largest revenue share of 37.5% in 2025. Rising global beer consumption, especially craft and premium varieties, is driving demand for innovative and sustainable packaging.

Key Market Trends & Insights

- By material: Glass segment held the largest market share of 47.4% in 2025.

- By product: Bottles segment held the largest market share of 51.8% in 2025.

- By end use: Breweries segment held the largest market share of 39.8% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (37.5% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 26.6 Billion

- Estimated market size in 2026: USD 27.6 Billion

- Projected market size by 2033: USD 35.8 Billion

- CAGR (2026-2033): 3.8%

Additionally, increasing focus on product shelf life and branding is boosting the adoption of advanced packaging solutions. The beer packaging industry’s growth is primarily driven by rising global beer consumption, particularly in emerging economies. As countries such as China, India, Brazil, and Vietnam experience rising disposable incomes, urbanization, and shifting consumer preferences toward Western lifestyles, beer consumption has increased significantly. This uptick drives demand for innovative, functional, and region-specific packaging solutions such as cans, glass bottles, PET bottles, and kegs. For example, in India, the growing preference for craft and premium beers is pushing packaging companies to offer sleek, attractive, and differentiated packaging formats to support brand visibility and appeal.")

The surge in demand for sustainable and eco-friendly packaging solutions is also contributing to the growth of the beer packaging market. Consumers, particularly Millennials and Gen Z, are increasingly favoring brands that adopt green practices. As a result, breweries and packaging manufacturers are shifting toward recyclable materials, lightweight designs, and reduced plastic usage. For instance, companies such as Carlsberg have developed fiber-based "Green Fibre Bottle" prototypes, while others are exploring biodegradable labels and eco-friendly inks. This sustainability push is not only a response to environmental concerns but also helps brands comply with tightening regulations on packaging waste in regions such as the EU and North America.

The rise of e-commerce and direct-to-consumer alcohol delivery services has also become a crucial growth factor. These platforms require durable, tamper-evident, and visually appealing packaging that can withstand shipping while enhancing brand experience. As online sales of alcoholic beverages expand, especially post-COVID-19, there’s increasing pressure on packaging manufacturers to innovate with formats that are both transport-friendly and shelf-ready.

Market Dynamics

The beer packaging market is witnessing steady growth, supported by rising beer consumption, the expansion of craft breweries, and increasing demand for premium and sustainable packaging solutions. Manufacturers are adopting lightweight, recyclable, and innovative packaging formats to enhance product protection, shelf appeal, and regulatory compliance. Growing preference for canned beer, along with advancements in labeling and packaging customization, is further driving market development. However, volatility in raw material costs and evolving sustainability regulations remain key challenges for industry participants.

Sustainability has emerged as a key driver of the beer packaging market as breweries, consumers, and regulators increasingly prioritize environmentally responsible packaging materials. Growing concerns regarding packaging waste and carbon emissions have encouraged manufacturers to adopt recyclable and lightweight materials such as aluminum cans, glass bottles with higher recycled content, and paper-based secondary packaging. These solutions help breweries meet sustainability targets while reducing transportation costs and environmental impact.

Changing consumer preferences are further prompting beer brands to invest in eco-friendly packaging that aligns with purchasing decisions. Many breweries are introducing recyclable, reusable, and resource-efficient packaging formats to strengthen brand image and comply with evolving environmental regulations. The increasing emphasis on circular economy practices and sustainable packaging innovation is expected to continue driving demand and supporting long-term growth in the beer packaging market.

A significant restraint in the beer packaging market is the volatility in the prices of key raw materials such as aluminum, glass, paperboard, and plastic. Fluctuations in material and energy costs can increase packaging production expenses, placing pressure on brewery profit margins and limiting pricing flexibility. Supply chain disruptions, inflationary pressures, and geopolitical uncertainties further contribute to cost instability, making it challenging for packaging manufacturers and beer producers to maintain consistent operational efficiency and profitability.

The expanding craft beer and premium beer segments present a significant opportunity for the beer packaging market. Craft breweries and premium beer brands increasingly seek distinctive, high-quality packaging solutions that enhance brand identity and consumer appeal. This trend is driving demand for customized cans, premium glass bottles, innovative labeling, and limited-edition packaging designs. As consumers continue to favor unique and premium drinking experiences, packaging manufacturers have opportunities to develop value-added, visually attractive, and sustainable packaging solutions that support product differentiation and brand recognition.

Market Concentration & Characteristics

The beer packaging industry operates under stringent regulations related to safety, labeling, recycling, and materials usage. Governments across regions enforce laws that govern permissible packaging materials, recycling mandates, and health-related labeling (alcohol content warnings). These regulations vary significantly by geography, requiring packaging companies to customize solutions for compliance in each market. For instance, returnable glass bottles are commonly used in Germany due to deposit laws, while in the U.S., aluminum cans dominate due to cost efficiency and ease of recycling.

Sustainability is central to the beer packaging market, with rising demand for lightweight, recyclable, and biodegradable packaging solutions. Environmental concerns and consumer awareness are pushing brands to minimize plastic usage and carbon footprint through sustainable designs and materials. Companies are adopting eco-friendly alternatives such as molded fiber packaging, paper-based multipacks, and refillable containers.

For instance, in June 2022, Carlsberg Group launched its largest-ever trial of a new Fibre Bottle, a bio-based and fully recyclable beer bottle, placing 8,000 units in the hands of consumers across eight Western European markets, including Denmark, Sweden, Norway, Finland, the UK, Poland, Germany, and France. The bottle features a sustainably sourced wood fibre outer shell with insulating properties that can keep beer colder longer, and a plant-based polyethylene furanoate (PEF) polymer lining developed by Carlsberg’s partner Avantium. This pilot aims to gather consumer feedback to refine the bottle design and accelerate Carlsberg’s ambition to commercialize this innovative packaging, which could reduce carbon emissions by up to 80% compared to traditional single-use glass bottles.

Analyst Perspective

The beer packaging market is poised for steady growth, driven by rising global beer consumption, expanding craft brewery operations, and increasing demand for packaging solutions that preserve product freshness, flavor, and carbonation. Manufacturers are increasingly adopting lightweight, durable, and recyclable materials such as aluminum and glass to enhance product protection while meeting sustainability objectives. The market is also witnessing growing demand for premium and customized packaging formats that strengthen brand differentiation and consumer engagement in a competitive beverage landscape. Going forward, companies that can combine sustainable material innovations, cost-efficient packaging technologies, and visually appealing designs will be well positioned to capitalize on opportunities across both mature beer markets and rapidly growing emerging economies.

Material Insights

Based on material, the glass segment led the market with the largest revenue share of 47.4% in 2025. Glass remains a traditional and premium packaging material in the beer industry, particularly for bottled beers. It is inert, non-permeable, and preserves the flavor and carbonation of beer effectively. Craft brewers and premium brands widely use glass packaging to reflect authenticity and quality. The growing demand for premium, craft, and specialty beers is a major driver for glass packaging. Additionally, glass is 100% recyclable without loss of quality, aligning with sustainability trends and influencing eco-conscious consumer preferences and regulatory support.

The metal segment is expected to grow at the fastest CAGR of 4.5% during the forecast period. Metal, particularly aluminum cans, is a dominant packaging format in the beer industry. Cans are lightweight, easily stackable, and protect beer from light and oxygen exposure. They are widely used across both mainstream and craft beer brands due to their portability and fast chilling properties. The growth of canned beer, especially among younger consumers and for outdoor events, is a key driver. Sustainability is also pushing this segment forward, as aluminum is highly recyclable and has a lower carbon footprint over its lifecycle.

Product Insights

Based on product, the bottles segment led the market with the largest revenue share of 51.8% in 2025. Bottles, particularly glass bottles, have been a traditional packaging format for beer for decades. They are often associated with premium and craft beer due to their aesthetic appeal and ability to preserve taste by offering good barrier properties against oxygen. Bottled beers are typically favored in on-premise consumption settings such as restaurants and bars due to their upscale image and recyclable nature. The demand for bottled beer is driven by premiumization trends in the beer market, increasing demand for craft and artisanal beer, and consumer perception of glass as a more sustainable and quality-preserving material.

The cans segment is expected to grow at the fastest CAGR of 4.5% during the forecast period. Aluminum cans have grown rapidly in popularity due to their lightweight nature, high recyclability, and lower shipping costs. Cans are especially prevalent in retail and off-premise consumption settings. They offer excellent protection against light and oxygen, preserving beer freshness and allowing for easy branding with 360-degree printing. Cans are driven by their convenience, portability, and eco-friendliness due to their high recyclability. The growing popularity of ready-to-drink formats and expanding e-commerce channels also favors canned beer.

End Use Insights

Based on end use, the breweries segment led the market with the largest revenue share of 39.8% in 2025. Breweries are the primary consumers of beer packaging as they handle the production and bottling or canning of beer. Packaging for this segment ranges from glass bottles and aluminum cans to kegs and multipacks. The branding and labeling requirements are also a significant concern for breweries, as they directly influence consumer perception and shelf visibility. Increasing craft beer consumption, the rise of microbreweries, and innovation in sustainable packaging drive packaging demand in this segment.

The restaurants & bars segment is projected to grow at the fastest CAGR of 4.5% during the forecast period. Restaurants and bars utilize beer packaging primarily in the form of bottles, cans, and kegs for direct consumption. The aesthetic and functional aspects of the packaging are critical, especially for premium or specialty brews served in upscale venues. Growth in social dining culture, urban nightlife trends, and the popularity of beer pairings with gourmet food fuel demand.

Region Insights

Asia Pacific dominated the beer packaging market with the largest revenue share of 37.5% in 2025. The Asia Pacific region dominates the global market due to its massive population base and rapidly expanding middle class with increasing disposable income. Countries such as China, India, and Southeast Asian nations are experiencing significant urbanization and westernization of drinking habits, driving unprecedented demand for packaged beer. Additionally, the rise of craft beer culture and premium beer segments in major cities across the region has created demand for innovative packaging solutions that emphasize brand differentiation and sustainability.

China Beer Packaging Market Trends

The beer packaging market in China held the largest share in the Asia Pacific region in 2025. China stands as the world's largest beer market by volume, making it the primary driver of beer packaging demand globally. The country's massive urbanization process has transformed drinking patterns, with urban consumers increasingly preferring packaged beer over traditional bulk or draft options. Major international brewing companies such as AB InBev, Heineken, and Carlsberg have established significant manufacturing and packaging operations in China to serve both domestic demand and regional export markets. The rise of domestic premium brands such as Tsingtao Brewery Co.,Ltd. and Snow Beer has also driven innovation in packaging design and materials, with companies investing heavily in distinctive bottle shapes, premium labeling, and sustainable packaging solutions to appeal to increasingly sophisticated Chinese consumers.

North America Beer Packaging Market Trends

North America represents a mature but evolving beer packaging industry characterized by premiumization trends and strong consumer preferences for sustainable packaging solutions. The region's well-established craft beer industry, with thousands of microbreweries and craft producers, drives demand for diverse packaging formats and customized solutions that help smaller brands compete with established players. The regulatory environment in North America strongly supports sustainable packaging initiatives, with various states and provinces implementing bottle deposit programs and recycling mandates that influence packaging material selection. The region's sophisticated cold chain distribution networks and modern retail infrastructure support premium packaging formats. At the same time, the growing popularity of hard seltzers and flavored alcoholic beverages has created new packaging requirements that emphasize freshness and brand differentiation.

The beer packaging industry in the U.S. is primarily driven by its intense competition between major national brands and a thriving craft beer sector that demands diverse packaging solutions. The craft beer revolution has fundamentally transformed packaging requirements, with over 9,000 craft breweries requiring smaller batch packaging capabilities, unique bottle shapes, and customized labeling solutions that help differentiate their products in crowded retail environments.

Europe Beer Packaging Market Trends

Europe’s beer packaging industry is shaped by stringent environmental regulations, a strong craft beer culture, and a preference for traditional glass bottles. Germany, the largest beer market in Europe, maintains a strong attachment to glass bottles due to cultural heritage and recycling infrastructure. However, cans are gaining traction among younger consumers and at festivals such as Oktoberfest, where convenience is key. The EU’s Single-Use Plastics Directive is pushing breweries to adopt more sustainable options, such as reusable bottles and biodegradable six-pack rings.

Countries such as the UK and Belgium are seeing a rise in canned craft beers, with brands such as BrewDog leading the shift toward eco-friendly aluminum packaging. Meanwhile, Eastern European markets, such as Poland and the Czech Republic, continue to favor glass bottles but are gradually embracing cans for export-oriented brands. The growing trend of home beer delivery services during the COVID-19 pandemic also accelerated demand for durable and lightweight packaging formats across the region.

Key Beer Packaging Company Insights

The beer packaging industry is characterized by intense competition among global and regional players. Key competitors include major packaging companies such as Ball Corporation, Crown Holdings, Amcor plc, Westrock Company, and Ardagh Group, alongside smaller niche firms catering to localized and artisanal brands. The market sees constant innovation in packaging formats, such as cans, bottles, and kegs, as well as in sustainable materials and digital labeling technologies. Companies compete on cost efficiency, product differentiation, environmental compliance, and partnerships with breweries, creating a dynamic and fragmented competitive landscape.

-

In March 2025, CANPACK partnered with United Breweries Limited (UBL), part of the Heineken Group, to launch Kingfisher Lemon Masala and Mango Berry Twist, flavored beers inspired by Indian street food. Aimed at Gen Z, CANPACK provided 330ml recyclable aluminum cans with vibrant, culturally inspired designs that align with the values of sustainability, innovation, and individuality. The collaboration highlights CANPACK’s advanced printing and manufacturing capabilities, enhancing shelf appeal and supporting UBL’s push for adventurous, modern flavor experiences.

-

In January 2025, Ardagh Glass Packaging enhanced its 12-oz Heritage glass beer bottle collection with two new additions: an amber glass bottle featuring a twist-off closure and a flint (clear) glass bottle with a pry-off closure. These new bottles offer craft brewers greater branding flexibility with a wider label area and a shorter, lighter design compared to traditional long-neck bottles, improving transport efficiency.

Key Beer Packaging Companies:

The following key companies have been profiled for this study on the beer packaging market.

-

Ardagh Group

-

Amcor plc

-

ALPLA

-

Berry Global Inc.

-

Smurfit Westrock

-

TricorBraun

-

Crown Holdings, Inc.

-

CANPACK

-

WestRock Company

-

AGI glaspac

-

Gamer Packaging

-

P. Wilkinson Containers Ltd.

-

INOXCVA

-

THIELMANN

-

Ball Corporation

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (Ardagh Group, Amcor plc, ALPLA, Berry Global Inc., Smurfit Westrock, TricorBraun, Crown Holdings, CANPACK, WestRock Company, Ball Corporation)

- Focus on large-scale production and global supply chain optimization to serve multinational breweries efficiently.

- Invest heavily in sustainable packaging innovations, lightweight materials, and advanced manufacturing technologies.

- Extensive global manufacturing footprint and strong relationships with leading beer producers.

- Diversified packaging portfolio across glass, metal, paperboard, and plastic formats supported by strong financial resources.

- High operational and capital expenditure costs associated with large-scale manufacturing facilities.

- Lower flexibility and slower response times due to complex organizational structures and global operations.

Emerging Players (AGI glaspac, Gamer Packaging, P. Wilkinson Containers Ltd., INOXCVA, THIELMANN)

- Concentrate on niche packaging segments and customized solutions for regional and craft breweries.

- Pursue targeted regional expansion and customer-focused service strategies to strengthen market presence.

- Greater operational agility and faster decision-making compared to larger competitors.

- Strong specialization in specific packaging formats, enabling tailored solutions and closer customer relationships.

- Limited production capacity and financial resources compared to established market leaders.

- Restricted geographic presence and narrower product portfolios, reducing competitiveness in large-scale contracts.

Beer Packaging Market Report Scope

Report Attribute

Details

Market size in 2025

USD 26.6 billion

Estimated market size in 2026

USD 27.6 billion

Projected market size by 2033

USD 35.8 billion

Growth rate

CAGR of 3.8% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Material, product, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; China; Japan; India; South Korea; Australia; Brazil; Argentina; Saudi Arabia; South Africa; UAE

Key companies profiled

Ardagh Group; Amcor plc; ALPLA; Berry Global Inc.; Smurfit Westrock; TricorBraun; Crown Holdings, Inc.; CANPACK; WestRock Company; AGI glaspac; Gamer Packaging; P. Wilkinson Containers Ltd.; INOXCVA; THIELMANN; Ball Corporation

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Beer Packaging Market Report Segmentation

This report forecasts revenue growth at a global level and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global beer packaging market report based on material, product, end use, and region:

-

Material Outlook (Revenue, USD Million 2021 - 2033)

-

Glass

-

Plastic

-

Metal

-

Others

-

-

Product Outlook (Revenue, USD Million 2021 - 2033)

-

Bottles

-

Cans

-

Kegs

-

Others

-

-

End Use Outlook (Revenue, USD Million 2021 - 2033)

-

Breweries

-

Restaurants & Bars

-

Convenient Stores

-

Liquor Stores

-

Others

-

-

Region Outlook (Revenue, USD Million 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

India

-

Japan

-

Australia

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

-

Research Methodology

The beer packaging market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each beer packaging segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Material

Revenue capture definition

Glass

Revenue generated from the sale of glass beer packaging solutions designed to preserve product quality, carbonation, and flavor while offering premium brand presentation. This segment includes glass bottles and specialty glass containers used across commercial and craft beer applications.

Plastic

Revenue generated from the sale of plastic beer packaging products that provide lightweight, cost-effective, and shatter-resistant storage and transportation solutions. This segment includes PET bottles and other plastic packaging formats used in selected beer distribution channels.

Metal

Revenue generated from the sale of metal beer packaging solutions that offer durability, recyclability, and protection against light and oxygen exposure. This segment primarily includes aluminum and steel cans, kegs, and related packaging products used by breweries and beverage distributors.

Other Materials

Revenue generated from the sale of beer packaging products manufactured from alternative materials such as paperboard, composite materials, and bio-based materials. This segment includes secondary and specialty packaging solutions designed for transportation, branding, and sustainability initiatives.

Segment - Product

Revenue capture definition

Bottles

Revenue generated from the sale of beer bottles designed for product storage, protection, and retail distribution. This segment includes glass, plastic, and specialty bottles used across mass-market, premium, and craft beer categories.

Cans

Revenue generated from the sale of beer cans that provide lightweight, durable, and highly recyclable packaging solutions. This segment includes aluminum and steel cans used for retail, convenience, and on-the-go consumption applications.

Kegs

Revenue generated from the sale of kegs used for bulk beer storage, transportation, and dispensing. This segment includes stainless steel, aluminum, and reusable keg systems supplied to breweries, restaurants, bars, and event venues.

Others

Revenue generated from the sale of alternative beer packaging formats such as growlers, crowlers, bag-in-box systems, and specialty containers used for niche distribution and consumption requirements.

Segment - End Use

Revenue capture definition

Breweries

Revenue generated from the supply of beer packaging solutions to breweries for product filling, storage, branding, and distribution. This segment includes packaging products purchased by large-scale, regional, and craft beer producers.

Restaurants & Bars

Revenue generated from the sale of beer packaging products used by restaurants, bars, pubs, and hospitality establishments for beer storage, dispensing, and serving applications.

Convenience Stores

Revenue generated from the sale of packaged beer products distributed through convenience store channels. This segment includes packaging formats optimized for retail display, portability, and consumer convenience.

Liquor Stores

Revenue generated from the sale of packaged beer products distributed through liquor and specialty beverage retail outlets. This segment includes packaging solutions designed to support product visibility, shelf appeal, and premium positioning.

Others

Revenue generated from the sale of beer packaging products supplied to supermarkets, hypermarkets, online retailers, entertainment venues, and other distribution channels not covered under the above categories.

Estimation Model

Layer Name

Key Question

Description

Beer Consumption Base Layer

What forms the demand base?

Identify global beer consumption volumes across key markets and consumption channels, including lager, ale, stout, craft beer, premium beer, and non-alcoholic beer segments. This layer establishes the total beer production and consumption base that drives demand for packaging solutions across the value chain.

Packaging Format Penetration Layer

Where is packaging utilized?

Estimate the distribution of beer volumes packaged in bottles, cans, kegs, and other formats across regions and sales channels. Assess packaging preferences based on consumer behavior, brewery size, product positioning, sustainability trends, and distribution requirements in both developed and emerging markets.

Packaging Demand Intensity Layer

How much packaging volume is required?

Analyze packaging unit consumption relative to beer production and sales volumes, considering refill rates, single-use versus reusable packaging, packaging material mix, transportation requirements, and retail distribution patterns. Packaging intensity is influenced by product type, channel strategy, and regional consumption habits.

Revenue Layer

How is market revenue generated?

Market revenue is quantified through the sale of beer packaging products, including bottles, cans, kegs, closures, labels, cartons, and related packaging components. Revenue is generated from demand across breweries, restaurants & bars, convenience stores, liquor stores, and other distribution channels, supported by packaging innovation, branding requirements, and sustainability-driven upgrades.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional Segmentation Analysis

Detailed assessment of the beer packaging market across North America, Europe, Asia Pacific, Central & South America, and Middle East & Africa, covering market size, growth trends, packaging demand, consumption patterns, regulatory developments, and investment activities.

Enables identification of high-growth regional markets, supports geographic expansion strategies, and highlights region-specific demand trends.

Cross-Segmentation Analysis

Comprehensive analysis of market intersections across Material (Glass, Plastic, Metal, Other Material), Product (Bottles, Cans, Kegs, Others), End Use (Breweries, Restaurants & Bars, Convenience Stores, Liquor Stores, Others), and regional markets to identify key revenue-generating segments.

Helps uncover high-growth segment combinations, evaluate market demand across end-use channels, and identify untapped business opportunities.

Opportunity Assessment

Identification and prioritization of growth opportunities across sustainable packaging materials, lightweight packaging solutions, premium packaging formats, recyclable metal and glass packaging, and expanding distribution channels such as convenience stores and liquor stores.

Supports strategic investment planning, product innovation initiatives, and market expansion efforts by highlighting the most attractive growth areas.

Frequently Asked Questions About This Report

The bottles segment led the beer packaging market with a 51.8% revenue share in 2025.

The global beer packaging market size was valued at USD 26.6 billion in 2025 and is estimated at USD 27.6 billion for 2026.

The global beer packaging market is expected to grow at a compound annual growth rate of 3.8% from 2026 to 2033 to reach around USD 35.8 billion by 2033.

Asia Pacific dominated the beer packaging market with a 37.5% revenue share in 2025.

Asia Pacific is the fastest-growing region in the beer packaging market with a CAGR of 4.4% over the forecast period.

The glass segment led the beer packaging market with a 47.4% revenue share in 2025.

The breweries segment led the beer packaging market with a 39.8% revenue share in 2025.

Key players in the beer packaging market include Ardagh Group; Amcor plc; ALPLA; Berry Global Inc.; Smurfit Westrock; TricorBraun; Crown Holdings, Inc.; CANPACK; WestRock Company; AGI glaspac; Gamer Packaging; P. Wilkinson Containers Ltd.; INOXCVA; THIELMANN; Ball Corporation.

Key factors driving the beer packaging market include rising beer consumption, growth of craft breweries, increasing demand for sustainable and recyclable packaging, growing preference for cans, and the need for enhanced product protection, convenience, and brand differentiation.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.