- Home

- »

- Pharmaceuticals

- »

-

Benign Positional Vertigo Market Size Report, 2025-2033GVR Report cover

![Benign Positional Vertigo Market (2025 - 2033)Report]()

Benign Positional Vertigo Market (2025 - 2033)

Size, Share & Trends Analysis Report By Therapeutics (Vestibular Function Restoratives, Antivertigo H1 Antihistamines), By Type (Branded, Generic), By Distribution Channel, By Region, And Segment Forecasts

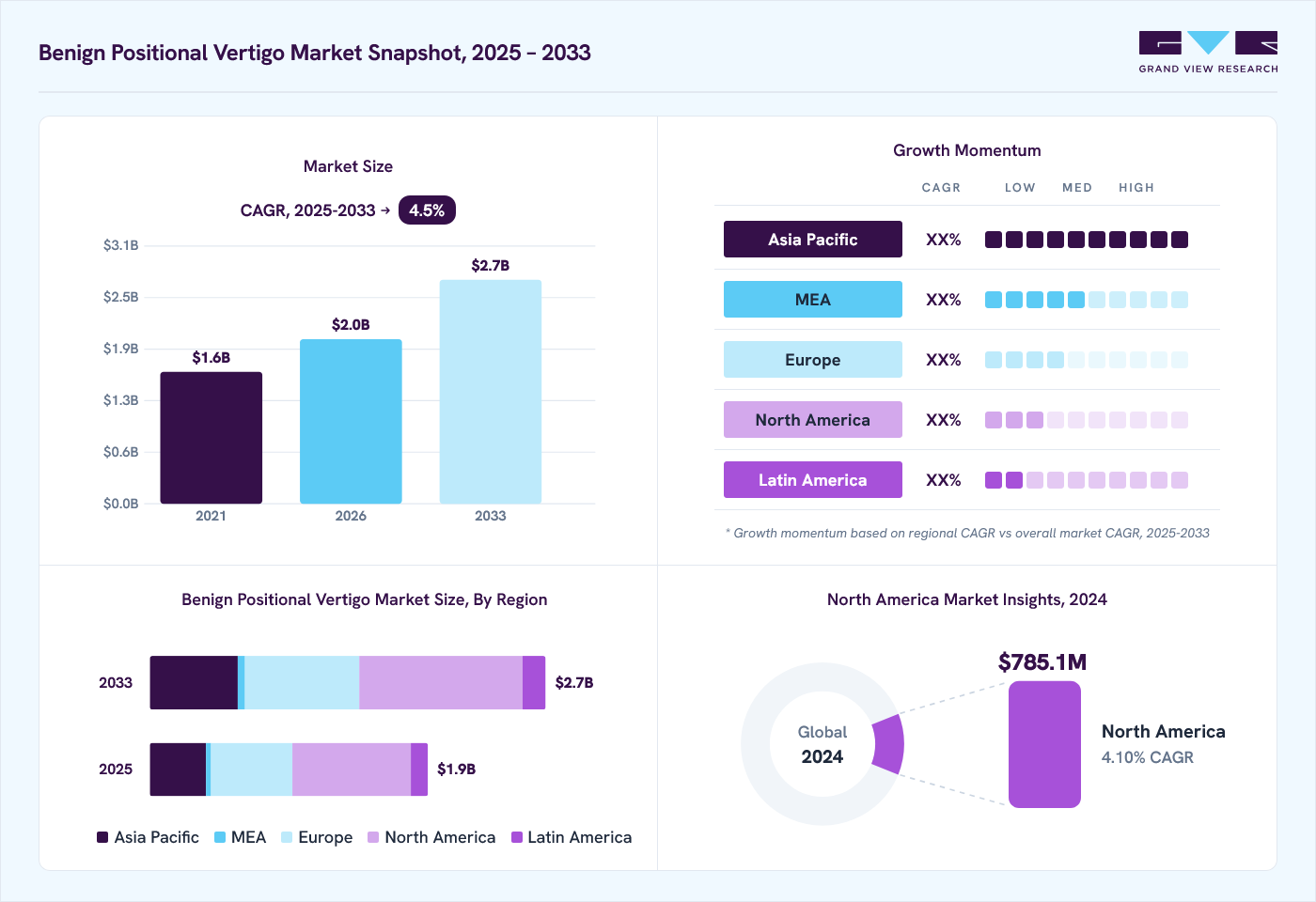

Market Size, 2024

$1.8BMarket Estimate, 2026

$2.0BMarket Forecast, 2033

$2.7BCAGR, 2025–2033

4.5%Benign Positional Vertigo Market Summary

The global benign positional vertigo market size was valued at USD 1.8 billion in 2024 and is projected to grow from USD 2.0 billion in 2026 to USD 2.7 billion by 2033, at a CAGR of 4.5% from 2025 to 2033. North America dominated the market, accounting for a revenue share of 42.7% in 2024. The benign positional vertigo industry is driven by the growing prevalence of vestibular disorders, increased awareness of balance-related conditions, and advancements in diagnostic tools such as videonystagmography (VNG) and magnetic resonance imaging (MRI).

Key Market Trends & Insights

- By therapeutics, the vestibular function restoratives segment led the market with the largest revenue share of 42.1% in 2024.

- Based on type, the branded segment accounted for the largest market revenue share in 2024.

- By distribution channel, the hospital pharmacies segment accounted for the largest market revenue share in 2024.

Market Size & Forecast

- 2024 Market Size: USD 1.8 Billion

- 2033 Projected Market Size: USD 2.7 Billion

- CAGR (2025-2033): 4.5%

- Asia Pacific: Fastest growing market

Rising geriatric population prone to inner ear dysfunctions further supports market growth. Expanding use of vestibular rehabilitation therapy and pharmacological treatments, including antihistamines and vestibular suppressants, is contributing to demand. In addition, increasing research on vestibular dysfunction mechanisms is expected to enhance treatment accessibility and adoption.")

The rise in vestibular disorders and the growing elderly population drive demand for effective treatment options for benign positional vertigo across a wide patient base. Advances in diagnostic tools, non-invasive therapies, and guided repositioning devices have improved accuracy, patient comfort, and clinical outcomes. Vestibular impairments occur frequently with age, creating a substantial population at risk. According to an article published in the International Journal of Otorhinolaryngology and Head and Neck Surgery in July 2023, the overall prevalence of age-related vestibular loss was reported to be 35.4% among individuals aged over 40 years, highlighting the substantial patient pool requiring targeted interventions.

Market Concentration & Characteristics

High clinical validation costs, complex diagnostic protocols, and limited patient awareness pose notable entry barriers. Existing brand presence in vestibular diagnostics and therapies constrains new entrants. In addition, the niche patient pool and dependency on specialist consultations limit large-scale commercialization, maintaining moderate market concentration.

Regulatory frameworks emphasize patient safety, device calibration, and drug efficacy for vertigo-related treatments. Medical devices and pharmacological products require compliance with safety testing, manufacturing quality, and post-market reporting. Delays in regulatory approvals influence market entry timelines and product availability.

The level of mergers and acquisitions (M&A) in the benign positional vertigo industry remains low to moderate due to the niche nature of the disorder and limited commercialization scope. Most M&A activities occur indirectly through broader portfolios in neurology and vestibular disorder treatment segments rather than BPV-specific deals. Larger pharmaceutical and medical device companies acquire smaller firms with innovative vestibular diagnostic tools, rehabilitation systems, or balance assessment technologies to expand their neuro-otology offerings. Strategic collaborations are more common than large-scale acquisitions, focusing on technology integration, digital rehabilitation platforms, and regional distribution expansion.

Physical maneuvers such as the Epley and Semont techniques, along with vestibular rehabilitation exercises, serve as primary substitutes for pharmacological treatments. Alternative therapies, including physiotherapy and balance training, influence drug demand and pricing dynamics in the benign positional vertigo industry.

Market growth is supported by increasing diagnosis rates, rising awareness of vestibular disorders, and aging populations in developed regions. Emerging economies are witnessing gradual adoption through improved ENT and neurology infrastructure. Companies are focusing on regional collaborations, training programs, and distribution partnerships to enhance accessibility and strengthen geographic reach.

Therapeutics Insights

The vestibular function restoratives (VFR) segment led the market with the largest revenue share of 42.1% in 2024. This segment's dominance is driven by the increasing prevalence of vestibular disorders, aging populations, and rising awareness of non-pharmacological therapies. Vestibular Rehabilitation Therapy (VRT), which includes structured exercises, balance training, and vestibular adaptation maneuvers, is widely adopted in clinical and outpatient settings to improve stability.

The antivertigo H1 antihistamines segment is expected to grow at the fastest CAGR of 4.2% over the forecast period. These medications selectively block H1 histamine receptors in the central nervous system, alleviating vertigo, nausea, and imbalance symptoms. Segment growth is driven by the rising incidence of vertigo-related disorders, wider over-the-counter availability, and newer non-sedating formulations that improve patient compliance. The regulatory approval of generic formulations has increased accessibility and affordability for patients.

Type Insights

The branded segment accounted for the largest market revenue share in 2024, driven by the widespread adoption of established branded medicines in treatment protocols globally. Branded products benefit from strong clinical validation, higher physician trust, and established market recognition, making them the preferred choice in hospitals and specialty clinics.

The generic segment is projected to register at the fastest CAGR over the forecast period, fueled by growing demand for affordable and accessible alternatives. Generic medicines provide the same therapeutic efficacy as branded counterparts while reducing treatment costs, increasing patient reach, and adherence.

Distribution Channel Insights

The hospital pharmacies segment accounted for the largest market revenue share in 2024, driven by strong consumer trust in healthcare institutions and direct access to specialized vertigo treatments. Hospitals and affiliated pharmacies serve as primary points of care for patients diagnosed with benign positional vertigo, providing prescription medications, vestibular function restoratives, and therapeutic devices under professional guidance. Several healthcare providers have expanded specialized care units for balance disorders to strengthen clinical management and patient outcomes. In December 2024, Apollo Hospitals in India launched an integrated Neuro-ENT Vertigo & Balance Disorders Clinic, reinforcing its focus on comprehensive diagnostics and treatment services.

The online pharmacies segment is expected to register at the fastest CAGR over the forecast period, supported by the increased adoption of digital healthcare platforms and the convenience of home delivery. Consumers use online sources to compare treatment options, review device specifications, and access patient education materials from home.

Regional Insights

North America dominated the benign positional vertigo market with the largest revenue share of 42.7% in 2024. The region’s growth is driven by public awareness, well-established healthcare infrastructure, and significant investments in research and development. Strategic collaborations between pharmaceutical companies, biotechnology firms, and contract research organizations (CROs) have further accelerated innovation, introducing advanced therapeutics, gene-based interventions, and industrial applications across diverse benign positional vertigo segments.

U.S. Benign Positional Vertigo Market Trends

The benign positional vertigo market in the U.S. accounted for the largest market revenue share in North America in 2024. The rising prevalence of benign paroxysmal positional vertigo (BPPV) in the U.S. supports this growth, creating a growing need for effective diagnostic and therapeutic solutions. According to the article published on the National Library of Medicine in December 2022, in the U.S., an analysis of patients getting medical attention for BPPV recorded an incidence of 64 per 100,000 annually. This incidence escalated by 38% each decade of life, translating to around 200,000 new cases annually.

Europe Benign Positional Vertigo Market Trends

The benign positional vertigo market in Europe is expected to grow at a steady CAGR over the forecast period, driven by the growing elderly population, awareness of vestibular disorders, and improvements in diagnostic and treatment technologies. Moreover, improved access to specialized healthcare services and growing adoption of non-invasive therapeutic options are expected to support market expansion across the region further.

The UK benign positional vertigo market is expected to grow at a significant CAGR over the forecast period. This growth is supported by increasing awareness of vestibular disorders, advancements in diagnostic technologies, and a well-established healthcare system that facilitates patient access to specialized care.

The benign positional vertigo market in Germany represents a significant share of the European BPV market, driven by early diagnosis practices, availability of specialized vestibular centers, and strong focus on clinical research. Hospitals and outpatient neurology clinics employ video head impulse testing (vHIT) and caloric testing for accurate diagnosis. Increasing use of vestibular rehabilitation therapy and pharmacological interventions supports steady growth. Favorable reimbursement policies and growing awareness of vestibular health among the elderly further strengthen market development.

Asia-Pacific Benign Positional Vertigo Market Trends

The benign positional vertigo market in Asia-Pacific is expected to grow at a significant CAGR during the forecast period, driven by the increasing prevalence of balance disorders, expanding healthcare infrastructure, and rising awareness of vertigo management. Growing access to ENT specialists and urban diagnostic centers is enhancing diagnosis rates. Demand for vestibular rehabilitation, balance therapy, and motion-sensing diagnostic devices is increasing, particularly in countries such as China, Japan, and India.

The China benign positional vertigo market is expanding due to a large aging population and increased investment in neurology and ENT services. Urban hospitals and clinics are adopting vestibular function testing and balance training technologies. Government programs to improve access to neurological diagnostics and promote early screening for vestibular disorders support market growth. Local medical device manufacturing and partnerships with global players are improving affordability and availability.

The benign positional vertigo market in Japan shows steady growth supported by an aging population and high prevalence of dizziness-related consultations. Advanced hospitals and clinics are integrating motion analysis systems, vestibular rehabilitation, and pharmacological therapy. Government efforts to enhance access to rehabilitation and geriatric care are contributing to broader treatment adoption. Growing focus on preventive neurology and balance health supports market expansion.

Latin America Benign Positional Vertigo Market Trends

The benign positional vertigo market in Latin America is growing gradually, driven by increasing diagnoses of vestibular disorders and improving access to ENT care. Public and private hospitals are expanding vestibular rehabilitation services, while awareness campaigns are improving early diagnosis. Adoption of low-cost pharmacological options and manual repositioning therapies supports accessibility. Local production of balance diagnostic tools and affordable vestibular therapy devices aids market penetration.

The Brazil benign positional vertigo market is growing rapidly, due to high patient awareness and growing access to diagnostic and rehabilitation services. Hospitals and clinics are increasingly offering vestibular testing, physiotherapy, and balance training. The growing burden of aging-related dizziness and ear disorders drives sustained demand. Expansion of private healthcare services and local device manufacturing enhances accessibility and affordability of treatment options.

Middle East & Africa Benign Positional Vertigo Market Trends

The benign positional vertigo market in MEA is showing steady development, supported by healthcare infrastructure growth and rising awareness of vestibular disorders. Hospitals and ENT centers are expanding diagnostic and rehabilitation services. Increasing focus on balance health among older adults and occupational groups is boosting early diagnosis rates. Regional collaborations and partnerships with diagnostic device manufacturers support technology transfer and accessibility improvements.

The South Africa benign positional vertigo market represents the leading BPV market in the MEA region. Growing recognition of dizziness and balance disorders has driven hospitals and clinics to expand ENT and physiotherapy services. Vestibular rehabilitation, pharmacological therapy, and positional maneuvers are widely adopted in urban centers. Private healthcare initiatives and government focus on neurological disorder management contribute to increased access and treatment adoption.

Key Benign Positional Vertigo Company Insights

The global benign positional vertigo industry, from a pharmaceutical perspective, remains moderately competitive with limited product differentiation. Key participants focus on developing and marketing vestibular suppressants, antihistamines, benzodiazepines, and antiemetics for symptom management. Companies are exploring drug repurposing and formulation enhancements to improve efficacy and reduce side effects.

The benign positional vertigo industry is driven by increasing diagnosis rates and growing demand for pharmacological interventions over surgical or purely rehabilitative options. Competition primarily centers on pricing, distribution reach, and clinical evidence supporting product safety and effectiveness rather than novel drug introductions.

Key Benign Positional Vertigo Companies:

The following are the leading companies in the global benign positional vertigo market. These companies collectively hold the largest market share and dictate industry trends.

- Viatris Inc.

- Pfizer Inc.

- Zydus Group

- Prestige Consumer Healthcare Inc.

- GSK plc

- Novartis AG

- Johnson & Johnson

- Teva Pharmaceutical Industries Ltd.

- Sun Pharmaceutical Industries Ltd.

Recent Developments

-

In September 2025, Dr. Reddy’s Laboratories acquired Johnson & Johnson’s STUGERON brand for USD 50.5 million, expanding its presence in the anti-vertigo segment across 18 markets, including India and Vietnam.

Benign Positional Vertigo Market Report Scope

Report Attribute

Details

Market size in 2024

USD 1.8 billion

Estimated Market size in 2026

USD 2.0 billion

Projected Market size by 2033

USD 2.7 billion

Growth rate

CAGR of 4.5% from 2025 to 2033

Base year for estimation

2024

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Therapeutics, type, distribution channel, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; India; China; Japan; Australia; South Korea; Thailand; Brazil; Argentina; Saudi Arabia; UAE; South Africa; Kuwait

Key companies profiled

Viatris Inc.; Pfizer Inc.; Zydus Group; Prestige Consumer Healthcare Inc.; GSK plc; Novartis AG; Johnson & Johnson; Teva Pharmaceutical Industries Ltd.; Sun Pharmaceutical Industries Ltd.

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Benign Positional Vertigo Market Report Segmentation

This report forecasts revenue growth and provides an analysis on the latest trends in each of the sub-segments from 2021 to 2033. For this report, Grand View Research has segmented the global benign positional vertigo market report based on the therapeutics, type, distribution channel, and region:

-

Therapeutics Outlook (Revenue, USD Million, 2021 - 2033)

-

Vestibular Function Restoratives

-

Antivertigo H1 Antihistamines

-

Benzodiazepines

-

Others

-

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Branded

-

Generic

-

-

Distribution Channel Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospital Pharmacies

-

Online Pharmacies

-

Other

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

MEA

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

Key players include Viatris Inc.; Pfizer Inc.; Zydus Group; Prestige Consumer Healthcare Inc.; GSK plc; Novartis AG; Johnson & Johnson; Teva Pharmaceutical Industries Ltd.; and Sun Pharmaceutical Industries Ltd.

The industry is driven by the growing prevalence of vestibular disorders, increased awareness of balance-related conditions, and advancements in diagnostic tools such as videonystagmography (VNG) and magnetic resonance imaging (MRI).

The global benign positional vertigo market size was valued at USD 1.8 billion in 2024 and is estimated at USD 2.0 billion for 2026.

The global benign positional vertigo market is expected to grow at a CAGR of 4.5% from 2025 to 2033, reaching USD 2.7 billion by 2033.

North America dominated with a revenue share of 42.7% in 2024.

About the Author(s)

Pharmaceuticals Research Team

Healthcare · PharmaceuticalsThis report was authored by the pharmaceuticals research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the pharmaceuticals segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.