- Home

- »

- Biotechnology

- »

-

Cell Counting Market Size & Share Report, 2026-2033GVR Report cover

![Cell Counting Market Size, Share & Trends Report]()

Cell Counting Market (2026 - 2033) Size, Share & Trends Analysis Report By Product (Instruments, Consumables & Accessories), By Application (CBC, Stem Cell Research), By End-use, By Region, And Segment Forecasts

Market Size, 2025

$10.2BMarket Estimate, 2026

$11.0BMarket Forecast, 2033

$20.5BCAGR, 2026–2033

9.3%Cell Counting Market Summary

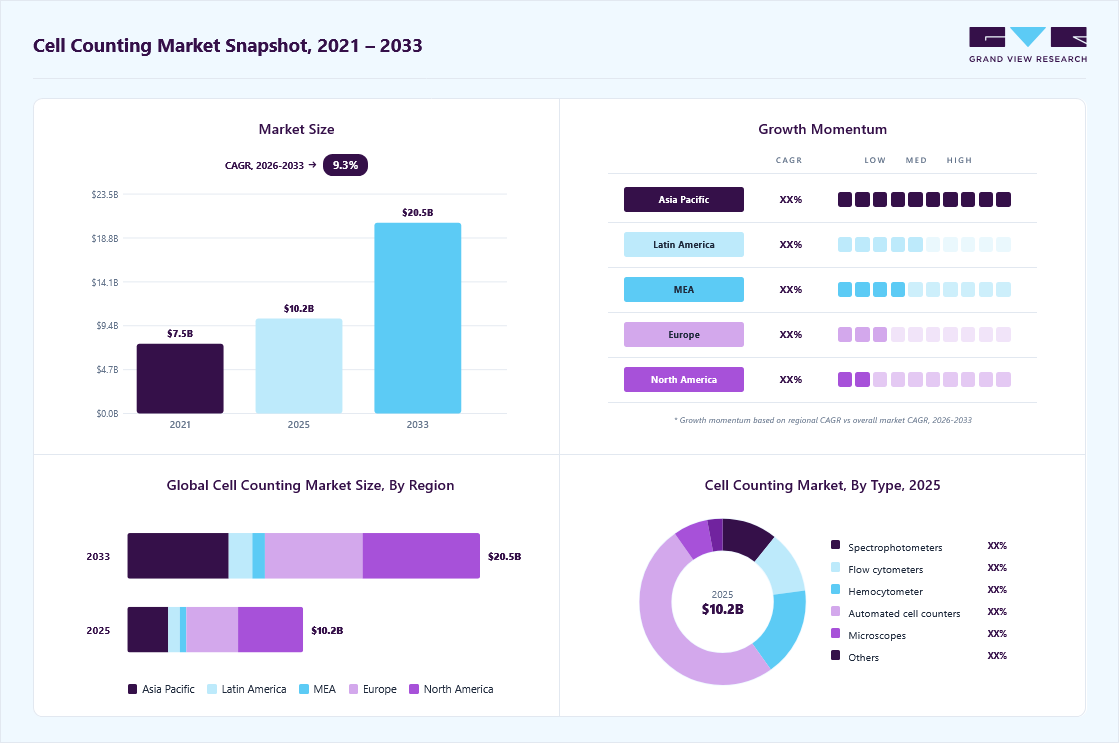

The global cell counting market size was valued at USD 10.2 billion in 2025 and is projected to grow from USD 11.0 billion in 2026 to USD 20.5 billion by 2033, at a CAGR of 9.3% from 2026 to 2033. North America held the largest share of 37.0% of the global market in 2025. As healthcare increasingly pivots towards tailored treatments, precision cell counting methodologies are becoming critical for evaluating cell viability and proliferation rates. In addition, advancements in automated, AI-enabled, and fluorescence-based cell counting systems are improving workflow efficiency and accelerating adoption across research and clinical laboratories.

Key Market Trends & Insights

- By products: Consumables & accessories segment held the largest share of 54.2% in 2025.

- By application: Complete blood count (CBC) segment held the largest share of 59.0% in 2025.

- By end use: Research & academic institutes segment led the market in 2025.

Regional Highlights

- Largest regional market: North America (37.0% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. cell counting market is expected to grow significantly from 2026 to 2033.

Market Size & Forecast

- Market size in 2025: USD 10.2 Billion

- Estimated market size in 2026: USD 11.0 Billion

- Projected market size by 2033: USD 20.5 Billion

- CAGR (2026-2033): 9.3%

")

Types of Automated Cell Counters

Parameter

Image-Based Cell Counters

Flow Cytometers

Coulter Counters

Technology Used

Bright-field or fluorescent microscopy with digital imaging (CMOS/CCD cameras)

Laser/light-based flow analysis with fluorescence detection

Electrical impedance technology

Working Principle

Captures cell images and analyzes them using image analysis software

Cells pass individually through a focused light source and scattered/fluorescent signals are measured

Cells passing through a small aperture cause changes in electrical impedance proportional to particle size

Key Features

Total cell count, viable/dead cell analysis, morphology-based analysis, automated image processing

Multi-parameter cell analysis, volumetric counting, fluorescence-based detection, cell characterization

Measures cell number and size, rapid particle counting

Advantages

High accuracy and reproducibility, reduced user variability, fast results, viability analysis possible

Highly sensitive, analyzes multiple cell parameters simultaneously, suitable for complex samples

Fast counting process, reliable size measurement, suitable for high-throughput analysis

Limitations

Requires consumables such as slides/cartridges; instrument cost can be high

Complex operation, expensive instruments, requires trained personnel

Cannot determine cell viability, limited cellular characterization

Common Applications

Cell viability analysis, stem cell research, cell culture monitoring, biopharmaceutical research

Immunology, oncology, hematology, biomarker analysis, and research laboratories

Blood cell counting, routine laboratory analysis, particle sizing applications

Source: Bio-Rad Laboratories, Inc., Secondary Research, Grand View Research

Market Dynamics

The rising adoption of automated cell counting technologies is significantly driving the cell counting market, as laboratories increasingly replace manual hemocytometer-based methods with faster and more accurate automated systems. Automated cell counters improve reproducibility, reduce human error, and enhance workflow efficiency, making them widely used in biotechnology, pharmaceutical research, clinical diagnostics, and cell therapy applications.

Growing demand for high-throughput analysis and precise cell viability assessment is further accelerating market growth. For instance, in July 2025, DeNovix launched new AI-enabled applications for its CellDrop FLxi Automated Cell Counter to support stem cell and viability analysis workflows.

High cost of advanced cell counting systems is a key restraint for the Cell Counting Market. Automated and AI-enabled platforms require significant upfront capital investment, making them less accessible for small and mid-sized laboratories. In addition to equipment costs, regular maintenance, calibration, and software upgrades further increase total ownership expenses. Consumables such as specialized slides, reagents, and cartridges also add recurring operational costs. These financial barriers limit global adoption, particularly in cost-sensitive and emerging market settings. As a result, many laboratories continue to rely on traditional manual cell counting methods despite their lower efficiency.

The expansion of regenerative medicine and stem cell research is creating significant growth opportunities for the cell counting market, as accurate cell counting and viability analysis are essential for stem cell manufacturing, tissue engineering, and cell therapy development. Automated cell counters are increasingly adopted to support quality control, scalability, and workflow efficiency in regenerative medicine applications. A research study published in Springer Nature in May 2025 demonstrated scalable stem cell-derived manufacturing using advanced automated bioreactor systems, highlighting the growing need for precise, high-throughput cell analysis technologies in stem cell research and production workflows.

A key challenge in the cell counting Market is the lack of standardization across instruments, protocols, and sample preparation methods, which can lead to variability in results. Different technologies, such as image-based counters, flow cytometers, and Coulter counters often produce inconsistent outputs depending on assay conditions. This variability reduces data comparability across laboratories and limits confidence in automated systems. In addition, differences in staining techniques and user handling further impact accuracy and reproducibility. As a result, achieving uniform performance standards remains a critical challenge for market growth and adoption.

Market Concentration & Characteristics

The cell counting industry is rapidly evolving with automation, AI-based imaging, and integrated analytical platforms enhancing accuracy and workflow efficiency. Advanced technologies such as spectral flow cytometry and image-based cell counters are replacing manual methods with faster, more reliable analysis. For instance, in May 2025, BD (Becton, Dickinson and Company) launched the FACSDiscover A8 Cell Analyzer, integrating real-time spectral imaging and AI-assisted single-cell analysis for high-resolution applications. AI-driven algorithms are further improving cell recognition and classification accuracy while reducing human error. These innovations are enabling more standardized, scalable, and high-throughput workflows across research and clinical laboratories.

The cell counting industry is witnessing moderate M&A activity, driven by the need to enhance automation, AI-based imaging, and advanced analytical capabilities. Companies are acquiring or partnering with niche players to strengthen their cell analysis, flow cytometry, and high-throughput screening portfolios. These strategic deals are supporting the integration of advanced technologies into cell counting workflows. Overall, M&A activity is enhancing innovation, portfolio expansion, and global competitiveness in the market.

Regulations significantly influence the cell counting market by shaping product standards, validation processes, and clinical adoption. Compliance with GMP, ISO standards, and regulatory guidelines ensures accuracy, reproducibility, and data integrity in cell analysis workflows. Regulatory requirements also govern instrument calibration, quality control, and reliability of automated and AI-based systems. While these frameworks increase development costs and approval timelines, they enhance standardization and user confidence. Overall, regulations support global acceptance and drive quality-focused innovation in cell counting technologies.

Product expansion in the cell counting industry is driven by rising demand for automated, high-throughput, and application-specific solutions in research and diagnostics. Companies are expanding portfolios with AI-enabled cell counters, imaging cytometers, and integrated platforms to improve speed and accuracy. For instance, in May 2026, Thermo Fisher Scientific introduced the Countess Automated Cell Counter, an optics- and image analysis-based system for accurate cell counting and viability assessment using trypan blue staining. Overall, product expansion is enhancing efficiency, scalability, and analytical precision in cell counting solutions.

Regional expansion in the cell counting industry is driven by the rising adoption of cell-based research and clinical diagnostics across emerging and developed regions. Companies are strengthening their presence in Asia-Pacific, Latin America, and the Middle East & Africa through partnerships, distribution networks, and localized operations. Growth is supported by improving laboratory infrastructure and increasing life sciences research investments. Demand for cost-effective, automated cell-counting solutions is further accelerating market penetration. Overall, regional expansion is enhancing the accessibility, adoption, and global market reach of advanced cell counting technologies.

Case Study

AI-Powered Cell Counting & Classification Solution

Overview

Folio3 AI partnered with a U.S.-based biotechnology company to develop a customized AI-powered cell counting and classification tool. The solution leverages advanced image analysis and machine learning algorithms to automate cell identification, counting, and classification with high precision, improving laboratory efficiency and diagnostic accuracy.

Client Profile

The client is a global biotechnology and healthcare company focused on advancing cell research, disease identification, prevention, and therapeutic development through innovative technologies and scientific research.

Business Challenge

The biotechnology company required an automated solution capable of:

-

Counting and classifying cells based on varying cellular characteristics

-

Analyzing extremely small and difficult-to-interpret microscopic cell images

-

Reducing dependence on manual cell counting processes

-

Improving workflow efficiency and analytical consistency

-

Building a scalable machine learning pipeline for high-volume image analysis

Manual cell analysis was time-consuming, prone to variability, and inefficient for large-scale laboratory operations.

Solution Implemented

Folio3 AI developed an AI-driven automated cell counting and classification platform using advanced image recognition and machine learning technologies.

Key Solution Features

-

Automated Cell Identification: AI algorithms identify and classify cells based on morphology, staining patterns, and other cellular characteristics.

-

High Precision & Consistency: Automated analysis minimizes human error and improves reproducibility of results.

-

Advanced Image Analysis: Machine learning models process microscopic images that are difficult to analyze manually.

-

Workflow Integration: The platform integrates seamlessly with laboratory systems and diagnostic workflows.

-

Scalable Architecture: Designed to handle large datasets and high-throughput laboratory environments.

-

User-Friendly Interface: Accessible platform enabling easy adoption by healthcare and laboratory professionals.

Result

The AI-powered platform improved the efficiency and accuracy of cell counting and classification workflows while reducing reliance on manual analysis. The solution enabled streamlined laboratory operations, enhanced diagnostic capabilities, and scalable image analysis for high-throughput environments. Additionally, the user-friendly interface improved accessibility for healthcare professionals with varying levels of technical expertise.

Product Insights

The consumables & accessories segment dominated the market, accounting for 54.2% in 2025. Consumables and accessories, such as reagents, kits, and sample preparation tools, are crucial for precise cell counting. Their ongoing use in laboratories, especially in personalized medicine and biopharmaceutical research, drives consistent demand due to their role in quality control and standardizing procedures within the cell counting ecosystem.

The instruments segment is expected to grow rapidly over the forecast period. The rising incidence of chronic diseases, including cancer and diabetes, requires monitoring cell counts precisely for effective diagnosis and treatment. Automated cell counters, enhanced with high-throughput capabilities and cloud integration, are vital in research and clinical settings, underpinning the demand for advanced instruments in modern healthcare.

Application Insights

The complete blood count (CBC) segment held the largest share, 59.0%, in 2025, driven by its critical role in diagnosing and monitoring health conditions. As blood disorders such as anemia and leukemia increase, the routine use of CBC testing for management, check-ups, and preoperative assessments is driving demand for reliable cell-counting technologies in clinical settings.

Stem cell research is projected to grow at the fastest CAGR over the forecast period, fueled by substantial investments in regenerative medicine. Increased funding from both the government and private sectors will enhance research on stem cell therapies for chronic diseases and injuries. Accurate cell counting is vital for assessing stem cell viability and proliferation, thereby advancing the development of treatments and clinical trials.

End Use Insights

Research & academic institutes led the market, accounting for 39.8% of revenue in 2025. These institutions are crucial to extensive research on chronic diseases, stem cells, and regenerative medicine, which necessitates precise cell-counting methodologies. The rise in publications and clinical trials in cancer research and immunology, coupled with government funding for innovative projects, further intensifies demand for reliable cell-counting technologies.

Pharmaceutical & biotechnology companies are expected to register the fastest CAGR over the forecast period. These companies depend on accurate cell counting for preclinical testing of new drug candidates and vaccines, which is critical for evaluating therapeutic efficacy and toxicity. The emergence of biologics and advanced therapies, such as CAR T-cell therapies, demands precise counting during production and quality control, enhancing throughput and reducing development costs.

Regional Insights

The North America cell counting market dominated the global market with a revenue share of 37.0% in 2025. The region features a robust healthcare infrastructure, substantial investments in research and development, and a high incidence of chronic diseases. Its focus on precision medicine and personalized treatments fuels demand for accurate cell counting technologies, while leading manufacturers and a shift toward automation strengthen the region’s market position.

U.S. Cell Counting Market Trends

The U.S. cell counting market is highly competitive and innovation-driven, supported by strong healthcare spending, a robust biopharmaceutical sector, and extensive research infrastructure. Rising demand for accurate cell analysis in diagnostics, drug discovery, and regenerative medicine is driving the adoption of advanced automated cell counting technologies. Increasing investments in precision medicine and biologics development are further supporting market growth.

Europe Cell Counting Market Trends

The Europe cell counting market held a substantial market share in 2025, driven by a growing patient population with chronic diseases and robust research and development efforts. Increased funding in the life sciences and biotechnology sectors supports innovations in cell-counting technologies, while the growing use of biologics further drives demand for precise cell-counting methodologies.

The UK cell counting market is driven by a strong focus on biomedical research, increasing adoption of advanced diagnostic technologies, and growing applications in oncology and regenerative medicine. Rising collaborations between research institutions and biotechnology companies are further supporting innovation and demand for automated cell counting solutions.

The cell counting market in Germany is expected to grow rapidly over the forecast period, driven by its strong healthcare system, significant investments in life sciences research, and the high prevalence of chronic diseases. The presence of leading biotechnology firms and research institutions focused on innovative therapies, along with government initiatives, further strengthens the market growth.

Asia Pacific Cell Counting Market Trends

The Asia Pacific cell counting market is expected to register the fastest CAGR of 12.4% over the forecast period. The increasing prevalence of chronic diseases and infectious conditions underscores the need for precise diagnostic tools, such as cell counters. Moreover, the growth of the biopharmaceutical sector and government initiatives to enhance healthcare access significantly drive market expansion.

The China cell counting market is growing rapidly due to increasing investments in biotechnology, expanding healthcare infrastructure, and rising demand for advanced diagnostics. The growing adoption of automated, high-throughput cell-counting systems, along with government support for precision medicine and life sciences research, is further driving market growth.

The Japan cell counting market is driven by advanced healthcare infrastructure and substantial investments in medical research and biotechnology. With a high prevalence of chronic diseases that require accurate cell-counting methodologies, Japan’s emphasis on innovative therapies and regenerative medicine further fuels demand for advanced cell-counting technologies.

Middle East & Africa Cell Counting Market Trends

The MEA cell counting market is witnessing gradual growth driven by improving healthcare infrastructure, increased focus on diagnostics, and rising investments in life sciences research. The growing demand for cost-effective, efficient cell analysis solutions is further driving market expansion across the region.

The Kuwait cell counting market is experiencing steady growth, driven by healthcare investments and increasing adoption of advanced diagnostic technologies. The growing focus on precision medicine and biomedical research is further driving demand for automated cell-counting systems.

Key Cell Counting Company Insights

The cell counting market is highly competitive, with key players such as Thermo Fisher Scientific Inc., Merck KGaA, Agilent Technologies, Inc., PerkinElmer, BD, Danaher Corporation, Bio-Rad Laboratories, Inc., GE HealthCare, and DeNovix focusing on automated and high-throughput cell counting technologies to strengthen their market presence. Continuous investments in R&D, product innovation, and strategic collaborations are supporting market growth across research, diagnostics, and biopharmaceutical applications.

Key Cell Counting Companies:

The following key companies have been profiled for this study on the cell counting market.

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Agilent Technologies, Inc.

- PerkinElmer

- BD

- Danaher Corporation

- Bio-Rad Laboratories, Inc.

- GE HealthCare

- DeNovix

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Thermo Fisher Scientific Inc.

- Mergers & acquisitions

- Drive growth through large-scale acquisitions and global expansion, strengthening presence across pharma, biotech, and diagnostics

- Invest heavily in automation, digital labs to support end-to-end workflows

- Strong global scale, financial strength, and diversified portfolios across multiple life science segments

- High customer lock-in through installed base and consumables-driven recurring revenue models

- Heavy reliance on acquisition-led growth, increasing integration and execution risks

Emerging Players: PerkinElmer

- Operating Strategies

Focus on specialized, high-value niche applications - Pursue portfolio simplification and selective expansion, avoiding large-scale diversification

- Strong technical specialization and precision in niche applications

- High agility and faster innovation cycles compared to large diversified players

- Limited scale, global reach, and financial resources

Recent Developments

-

In October 2024, BD launched its first robotics-compatible reagent kits, enhancing automation in single-cell research, streamlining workflows, and improving efficiency in genetic sequencing across oncology and immunology applications through a collaboration with Hamilton.

-

In August 2024, DeNovix launched the CellDrop FLi Automated Cell Counter, enhancing cell counting capabilities with improved hardware and new applications, leveraging advanced machine-learning algorithms for accurate assessments across various sample types.

-

In June 2024, Bio-Rad launched the ddSEQ Single-Cell 3’ RNA-Seq Kit and Omnition v1.1 analysis software, enhancing single-cell gene expression research with efficient, cost-effective tools and workflows for diverse applications.

Cell Counting Market Report Scope

Report Attribute

Details

Market size in 2025

USD 10.2 billion

Estimated Market size in 2026

USD 11.0 billion

Projected Market size by 2033

USD 20.5 billion

Growth rate

CAGR of 9.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; India; China; Japan; Australia; South Korea; Thailand; Brazil; Argentina; Saudi Arabia; UAE; South Africa; Kuwait

Key companies profiled

Thermo Fisher Scientific Inc.; Merck KGaA; Agilent Technologies, Inc.; PerkinElmer; BD; Danaher Corporation; Bio-Rad Laboratories, Inc.; GE HealthCare; DeNovix

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cell Counting Market Report Segmentation

This report forecasts revenue growth and provides an analysis on the latest trends in each of the sub-segments from 2021 to 2033. For the purpose of this report, Grand View Research has segmented the global cell counting market report on the basis of product, application, end use, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Instruments

-

Spectrophotometers

-

Flow Cytometers

-

Hemocytometer

-

Automated Cell Counters

-

Microscopes

-

Others

-

-

Consumables & Accessories

-

Reagents

-

Microplates

-

Others

-

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Complete Blood Count

-

Automated Cell Counters

-

Manual Cell Counters

-

-

Stem Cell Research

-

Cell Based Therapeutics

-

Bioprocessing

-

Toxicology

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals & Diagnostic Laboratories

-

Research & Academic Institutes

-

Pharmaceutical & Biotechnology Companies

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Regional & Country-Level Cell Counting Analysis

Detailed segmentation of the cell counting market across key geographies (North America, Europe, Asia Pacific, Latin America, MEA) with country-level breakdown including market size, growth trends, adoption patterns, regulatory environment, and healthcare infrastructure maturity.

Helps identify high-growth regions, evaluate funding intensity in life sciences, compare adoption of automated vs manual cell counting technologies, and prioritize expansion markets based on research intensity and healthcare investments.

Cross-Segmentation Analysis (Product × Application × End-Use)

Integrated analysis combining product types (instruments, consumables & accessories), applications (stem cell research, CBC, bioprocessing, drug discovery), and end users (pharma & biotech companies, research institutes, hospitals & diagnostic labs).

Reveals high-value demand clusters such as consumables-driven revenue streams in research institutes, identifies application-specific growth pockets like stem cell research, and supports targeted product positioning strategies for automation and high-throughput workflows.

Competitive Benchmarking & Technology Positioning

Benchmarking of key players (e.g., Thermo Fisher Scientific, Bio-Rad, Danaher, Merck) based on product portfolio, automation capabilities, flow cytometry integration, pricing strategies, innovation focus, and geographic presence.

Enables assessment of competitive intensity, identification of technology gaps (AI-based imaging, automated viability analysis), evaluation of partnership/M&A opportunities, and refinement of differentiation strategies in the automated cell counting ecosystem.

Frequently Asked Questions About This Report

Consumables & accessories dominated the market and accounted for a share of 54.2% in 2025. Consumables and accessories, such as reagents, kits, and sample preparation tools, are crucial for precise cell counting.

The global cell counting market size was valued at USD 10.2 billion in 2025 and is expected to reach USD 11.0 billion in 2026.

The global cell counting market is expected to grow at a compound annual growth rate of 9.3% from 2026 to 2033 to reach USD 20.5 billion by 2033.

North America dominated the global market with the largest share of 37.0% in 2025.

The complete blood count (CBC) segment held the largest share, 59.0%, in 2025, while stem cell research is the fastest growing segment.

Research & academic institutes led the market, accounting for 39.8% of revenue in 2025, while pharmaceutical & biotechnology is the fastest growing segment.

Key players include Thermo Fisher Scientific Inc.; Merck KGaA; Agilent Technologies, Inc.; PerkinElmer; BD; Danaher Corporation; Bio-Rad Laboratories, Inc.; GE HealthCare; DeNovix

Key factors include the rising prevalence of chronic diseases such as cancer, HIV, and Alzheimer’s. The increasing prevalence of these diseases has surged clinical research activities, consequently propelling the demand for cell counting instruments and consumables. Government initiatives working to promote the development of cell therapeutics, wherein cell counting plays an imperative role, are also expanding growth prospects for the market.

About the Author(s)

Biotechnology Research Team

Healthcare · BiotechnologyThis report was authored by the biotechnology research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the biotechnology segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.