- Home

- »

- Biotechnology

- »

-

Stem Cells Market Size & Share Report, 2025-2030GVR Report cover

![Stem Cells Market Size, Share & Trends Report]()

Stem Cells Market (2025 - 2030) Size, Share & Trends Analysis Report By Product (Adult Stem Cells, Human Embryonic Stem Cells), By Application (Regenerative Medicine), By Technology, Therapy, End-use, By Region, And Segment Forecasts

Market Size, 2024

$15.1BMarket Estimate, 2026

$18.8BMarket Forecast, 2030

$28.9BCAGR, 2025–2030

11.4%Stem Cells Market Summary

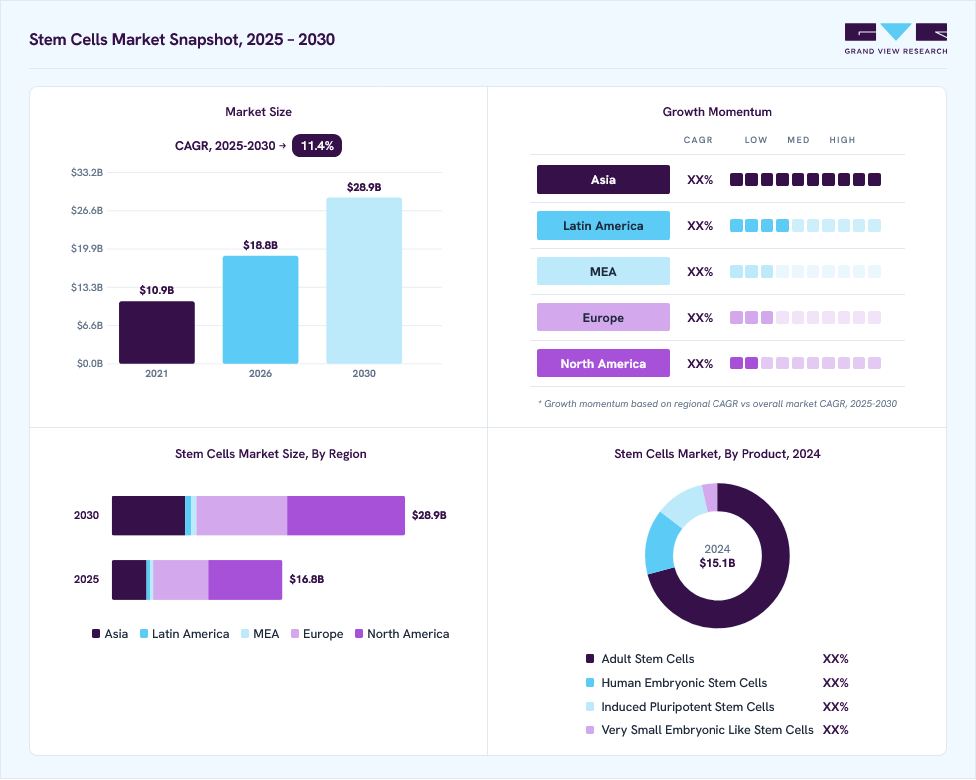

The global stem cells market size was valued at USD 15.1 billion in 2024 and is projected to grow from USD 18.8 billion in 2026 to USD 28.9 billion by 2030, at a CAGR of 11.4% from 2025 to 2030. North America dominated the market, accounting for a revenue share of 43.9% in 2024. The growing development of precision medicine, increase in the number of cell therapy production facilities, and rising number of clinical trials are expected to be major driving factors of the market.

Key Market Trends & Insights

- The stem cells market in Asia Pacific is expected to grow at a rapid rate of 16.08% CAGR during 2025-2030.

- By product, adult stem cells held the largest revenue share of 70.76% of the market in 2024.

- By technology, the cell acquisition segment captured the highest revenue share of 33.43% of the market in 2024.

- By therapy, the allogenic therapy segment captured the largest revenue share of 59.33% in 2024 with regard to revenue generation.

Market Size & Forecast

- 2024 Market Size: USD 15.1 Billion

- 2030 Projected Market Size: USD 28.9 Billion

- CAGR (2025-2030): 11.4%

- North America: Largest market in 2024

Recent advances in stem cells therapeutics and tissue engineering hold the potential to draw attention to the treatment of several diseases. Furthermore, increasing demand for stem cells banking and a rise in research activities about stem cells production, storage, and characterization are also expected to fuel the revenue growth for the market. Technological improvements in the parent and ancillary market for stem cells usage are some of the other factors that reinforce the expected growth in demand for stem cells over the forecast period.")

The COVID-19 pandemic had a positive impact on the market. The product applications in the novel coronavirus treatments has increased the interest of medical researchers, increasing clinical trials. Regenerative medicine based on cellular therapies may be a treatment option for patients, resulting in a reduction in mortality and infection rates. Companies and research institutes are collaborating to develop novel treatment options for the disease. For example, Infectious Disease Research Institute and Celularity, announced in April 2020 that the U.S. FDA had approved a clinical trial application to develop cell-based therapy for COVID-19. Hence, growing applications for clinical trials are expected to boost the demand for stem cells during the forecast period.

Moreover, researchers are increasingly attempting to develop stem cells therapies for targeting COVID-19. For instance, in January 2020, researchers from the University of Miami administered two stem cells infusions to COVID-19 patients that were suffering from lung damage. The results concluded that there were no significant side effects, and the therapy was reliable. Growing demand for regenerative medicines is expected to fuel market growth. Regenerative medicines have extensive applications in the treatment of various diseases including neurology, oncology, hepatology, diabetes, injuries, hematology, and orthopedics. In addition, the growing geriatric population and increasing demand for regenerative medicines for early detection and prevention of diseases are some of the factors contributing to market growth.

Regenerative medicines help restore normal functioning of cells. Rapid advancements in this field are anticipated to provide effective therapies for chronic conditions. For instance, in March 2022, Wipro Ltd, and Pandorum Technologies, announced a long-term partnership. Together the companies plan to aim at the development of technologies that will reduce the time-to-market and boost patient outcomes during clinical trials and research and development of regenerative medicine. Biotech Pandorum will use Wipro’s AI facilities for the development of regenerative medicine and advanced therapeutics to enhance patient outcomes.

There is wide global anticipation for stem cell-based therapies as they are safe and effective. Stem cells are gaining attention for the development of regenerative medicine. Regenerative cell therapies have the potential for healing and replacing damaged tissues and organs. For these therapies, stem cells represent a great promising cell source and hence are receiving increasing attention from researchers, clinicians, and scientists. Several factors contribute to the market growth such as increasing collaborations, robust funding, government initiatives, and extensive R&D. For instance, in May 2020, the CiRA Foundation and CGT Catapult launched a new collaborative research project aimed at induced pluripotent stem cell characterization. The companies will combine their competence to investigate novel methods to characterize pluripotent stem cells for the manufacturing of regenerative medicine products.

Significant R&D expenditures are one of the major contributors to market growth. Furthermore, another factor contributing to the increase is the increased need for effective therapeutics to reduce the disease burden during the forecast period. For instance, Celavie Biosciences' 5-year exploratory study on Parkinson's disease progressed in May 2020. The company is working on regenerative stem cell therapies to treat Parkinson's disease and other central nervous system disorders. Celavie Biosciences announced that their preliminary clinical trials utilizing OK99 stem cells for Parkinson's disease were successful.

Moreover, the increasing recognition of precision medicines is further promoting market growth. Scientists are finding new procurement methods that can be further utilized for the development of personalized medicines. For instance, induced pluripotent stem cells therapies are developed by utilizing a small amount of sample from a patient’s skin or blood cell which is later reprogrammed to form new tissue and cells for transplant. Moreover, in September 2022 Century Therapeutics and Bristol Myers Squibb announced a license agreement and research collaboration for the development and commercialization of iPSC-derived allogeneic cell therapies. Hence, with the application of these cells coupled with strategic activities by market players, potential personalized medicines can be developed in the near future.

Market Concentration & Characteristics

The market growth stage is moderate, and the pace is accelerating. The market is expected to witness growth due to the increasing availability of a variety of stem cell types such as mesenchymal stem cells, induced pluripotent stem cells, etc. for various research and development applications. Furthermore, intense competition in the market has led to highly competitive prices for high quality stem cell offerings.

Innovations in the market are improving the precision, scalability, and therapeutic potential of stem cells. Key innovative developments such as CRISPR-based gene editing are pushing the boundaries of stem cell-based therapies for various diseases, such as cancer, cardiovascular disease, etc., and represent a promising growth outlook for the market.

Mergers and acquisitions are contributing to the market expansion and can lead to an increase in the adoption of research and development activities. For instance, in July 2022, Vertex Pharmaceuticals Incorporated acquired ViaCyte focusing on stem cell-derived cell replacement therapies.

Stringent guidelines govern research and clinical practices in the market and compliance with regulations may lead to additional procedural costs and increased research and development timelines which may restrict the market growth.

The market has moderate levels of product and regional expansion. The increase in market expansion pace has led to the availability of stem cell technologies to local healthcare providers and researchers which has led to advancements in personalized medicine, tissue engineering, and therapeutic applications of stem cells. This factor is expected to boost the market growth in the near future.

Product Insights

Adult stem cells held the largest revenue share of 70.76% of the market in 2024 as these cells do not involve the destruction of embryos, which is the case in embryonic stem cells. Furthermore, there is no risk of graft rejection in the case of adult stem cells. Development of cell banking services and advancements in bio-preservation and cryopreservation are expected to further boost the demand for adult stem cells. Lesser ethical concerns surrounding adult cells further propel the growth of this segment. The benefits of adult stem cell banking such as the capacity for autologous transformation, low risk of tumor formation, and availability of established treatment options are factors that are expected to boost the segment’s growth during the forecast period.

Mesenchymal Stem Cells (MSCs), hematopoietic stem cells, epithelial/skin stem cells, and neural stem cells, are all subtypes of ASCs. The MSC segment is expected to witness the fastest CAGR during the forecast period due to its use in autologous transplantation, substantial clinical trials that demonstrated its application for treating various diseases, and extensive ongoing research to investigate its therapeutic applications.

The induced pluripotent stem cells segment is expected to grow at the CAGR of 11.08% from 2025 to 2030, owing to increased investment in developing regenerative medicines using induced pluripotent stem cells, ensuring reproducibility and maintenance, ability to differentiate into all cell types, and high proliferative ability. Many leading companies are also expanding services related to iPSCs as their importance in the treatment of various diseases grows. For instance, in January 2021, REPROCELL launched a new personalized induced pluripotent stem cell production service for generating patient-specific iPSC. The service will assist in the preparation and storage of an individual's iPSCs for the development of regenerative medicines to treat future illnesses or injury. They are developed from mature cells using ready-to-use RNA reprogramming technology.

Application Insights

Regenerative medicine and drug discovery and development are two applications within the application segment. Increased approvals for clinical trials on stem cell therapies targeting various diseases have resulted in the regenerative medicine segment capturing the larger market share of 85.62% in 2024. Longeveron LLC, for example, announced in June 2020 that Japan's Pharmaceutical and Medical Devices Agency (PMDA) had approved the start of a Phase 2 clinical trial to evaluate the safety and efficacy of their mesenchymal stem cells that can be used to treat aging frailty.

Furthermore, several governments are heavily investing in the development of regenerative medicines. For instance, the Government of Canada invested around USD 6.9 million in regenerative medicine research in March 2020. This fund will be used to support nine translational projects and four clinical trials aimed at developing new therapies in the field of regenerative medicine. The developed regenerative medicines will aid in the treatment of a variety of blood disorders, heart diseases, diabetes, and vision loss.

The drug discovery and development segment is expected to grow at a faster CAGR from 2025-2030. As it is useful in studying human disease etiology, identifying pathological mechanisms, and developing therapeutic strategies for tackling various diseases, market products are seeing increased penetration across the drug discovery process. Because they can mimic patients' molecular and cellular phenotypes, iPSC-based models are preferred over phenotypic screening. Pharmaceutical companies can use these to test hypothesized drug mechanisms in vitro in a cost-effective manner before conducting clinical trials.

Technology Insights

The cell acquisition segment captured the highest revenue share of 33.43% of the market in 2024. The discovery of embryonic stem cells has paved the way for the development of novel treatments for several diseases. These cells are pluripotent and can be used to differentiate many cell types in the body. However, obtaining embryonic cells directly from the embryo has raised ethical concerns. Hence, researchers discovered an alternative—iPS cells. For instance, in September 2020, a collaborative team of researchers from Singapore and Australia studied the molecular changes, which occur when adult skin cells become induced pluripotent stem cells (iPSCs). This led to the creation of new stem cells that could produce placenta tissue which could possibly lead to the development of new treatments for placenta complications arising during pregnancy.

The cell acquisition segment is further segmented into bone marrow harvest, umbilical blood cord, and apheresis. The bone marrow harvest segment captured the highest revenue share owing to factors such as rising awareness, increasing prevalence of blood cancer, and easy access to bone marrow transplantation therapy.

Therapy Insights

The allogenic therapy segment captured the largest revenue share of 59.33% in 2024 with regard to revenue generation. Factors such as high pricing and growth in stem cell banking have contributed to the segment’s growth. Moreover, many cell therapy companies are shifting their business toward the development of allogeneic cell therapy products. This, in turn, is expected to result in the significant growth of this segment.

In addition, strategic activities by key market players to strengthen their product portfolio will further offer lucrative opportunities in the review period. For instance, In March 2021, Acepodia announced the closing of its USD 47 million Series B financing to advance the pipeline of allogenic cell therapy candidates. In June 2022, Immatics and Bristol Myers Squibb expanded their strategic alliance for the development of gamma delta allogeneic cell therapy programs.

However, autologous therapy is expected to witness a higher CAGR from 2025 to 2030. This is primarily due to the low risk of complications associated with autologous treatment. Other factors anticipated to propel the growth of this segment include affordability, improved survival rate of patients, no need for identifying an HLA-matched donor, and no risk of graft-versus-host diseases. Furthermore, autologous MSCs are investigated for their potential in the treatment of osteoarthritis as they can differentiate into cartilage and bone tissues.

MSCs have the ability to migrate to the site of injury, promote tissue repair by releasing anabolic cytokines, inhibit pro-inflammatory pathways, and differentiate into specialized connective tissues. Thus, the adoption of autologous MSCs in regenerative medicine has increased, which is expected to propel the market growth during the forecast period.

End-use Insights

The pharmaceutical and biotechnology companies segment captured the largest revenue share of 54.19% in 2024. Some of the factors that can be attributed to the segment's share are the rising prevalence of chronic disease, an increase in clinical trials, and an upsurge in strategic activities along with improvements in healthcare services. For instance, in August 2022, StemCyte, Inc. obtained approval from the U.S. FDA for their Phase II clinical trial for post-COVID syndrome using umbilical cord blood stem cell therapy. Moreover, in April 2022, the U.S. FDA granted clearance to BioCardia’s Investigational New Drug (IND) application to initiate a Phase I/II clinical trial of BCDA-04 in adults improving from acute respiratory distress syndrome linked with COVID-19.

")

Moreover, the increasing number of clinical trials coupled with the approval of stem cell-based therapies from regulatory bodies will further offer lucrative opportunities. For instance, there are around 5,000 listed clinical trials involved in stem cells research on ClinicalTrials.gov, with new clinical trials being offered every day in this field.

Regional Insights

North America stem cell market accounted for the largest revenue share of 43.89% in 2024. The presence of innovators and key market players has resulted in higher penetration of market products in the region. North America leads the market owing to the strong biotechnology industry, the presence of key players, extensive R&D, and the promotion of personalized medicines. The region accounts for the highest revenue share. Moreover, growth in this region can be further attributed to rising government initiatives for promoting stem cell therapies. For instance, in March 2020, the government of Canada invested around USD 7 million in regenerative medicine and stem cell research. It will support 9 transnational projects and 4 clinical trials in the country for the growing regenerative medicine sector.

Asia Pacific Stem Cells Market Trends

The stem cells market in Asia Pacific is expected to grow at a rapid rate of 16.08% CAGR during 2025-2030 owing to strong product pipelines of therapies based on stem cells and a huge patient population base. The market is expected to grow at a rapid rate due to the increasing incidence rate of diseases such as cancer, neurological disorders, and diabetes. Moreover, government funding to accelerate research on stem cells further strengthens the growth of this region. For instance, In February 2022, the government of India set up state-of-the-art stem cell research facilities in 40 leading health research and educational institutions. The government has also spent USD 80 million through the Indian Council of Medical Research (ICMR) in the last three years on certain research projects.

Key Stem Cells Company Insights

Key players in this market are developing new products and undertaking collaborative initiatives to increase their product portfolio, customer reach, and geographic presence. These strategies are expected to favor market growth in the coming years as more players enter the market and try to secure their market position.

Key Stem Cells Companies:

The following are the leading companies in the stem cells market. These companies collectively hold the largest market share and dictate industry trends.

- Thermo Fisher Scientific, Inc

- STEMCELL Technologies, Inc.

- Merck KGaA

- Sartorius AG (CellGenix GmbH)

- PromoCell GmbH

- Takara Holdings, Inc.

- Lonza

- ATCC

- AcceGen

- Cell Applications, Inc.

- Bio-Techne

- Cellular Engineering Technologies

Recent Developments

-

In April 2024, PromoCell GmbH launched the Cryo-SFM Plus cryopreservation medium to preserve primary cells, stem cells, or established cell lines.

-

In January 2024, STEMCELL Technologies, Inc. acquired Propagenix Inc., enabling STEMCELL to develop products based on Propagenix’s EpiX technology in regenerative medicine.

-

In December 2023, the University of Texas at San Antonio (UTSA) and GenCure, a subsidiary of BioBridge Global, formalized their collaboration through the signing of a master services agreement. This agreement outlines their joint efforts in advancing the development of cellular therapy products, services, and testing.

-

In October 2023, bit.bio, a company dedicated to programming human cells for innovative treatments, unveiled its latest product, ioCRISPR-Ready Cells. These cells are tailored for scientists aiming to create gene knockouts in human cells with physiological relevance.

-

In September 2023, SKAN Research Trust (SKAN) collaborated with the Wellcome-MRC Cambridge Stem Cell Institute (CSCI) based in the UK. The partnership includes a joint research initiative focused on investigating the genomic patterns associated with age-related neurodegenerative diseases within an Indian cohort.

Stem Cells Market Report Scope

Report Attribute

Details

Market size in 2024

USD 15.1 billion

Estimated market size in 2026

USD 18.8 billion

Projected market size by 2030

USD 28.9 billion

Growth rate

CAGR of 11.4% from 2025 to 2030

Actual data

2018 - 2024

Forecast period

2025 - 2030

Revenue in USD million/billion and CAGR from 2024 to 2030

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, technology, therapy, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; South Korea; Australia; Thailand; Brazil; Mexico; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Thermo Fisher Scientific Inc; STEMCELL Technologies, Inc.; Merck KGaA; Sartorius AG (CellGenix GmbH); PromoCell GmbH; Takara Holdings, Inc.; Lonza; ATCC; AcceGen; Cell Applications, Inc.; Bio-Techne; Cellular Engineering Technologies

Customization scope

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional and segment scope.

Global Stem Cells Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest trends in each of the sub-segments from 2018 to 2030. For this report, Grand View Research has segmented the global stem cells based on the product, application, technology, therapy, end use, and region.

-

Product Outlook (Revenue, USD Million, 2018 - 2030)

-

Adult Stem Cells (ASCs)

-

Hematopoietic

-

Mesenchymal

-

Neural

-

Epithelial/Skin

-

Others

-

-

Human Embryonic Stem Cells (HESCs)

-

Induced Pluripotent Stem Cells (iPSCs)

-

Very Small Embryonic Like Stem Cells

-

-

Application Outlook (Revenue, USD Million, 2018 - 2030)

-

Regenerative Medicine

-

Neurology

-

Orthopedics

-

Oncology

-

Hematology

-

Cardiovascular and Myocardial Infraction

-

Injuries

-

Diabetes

-

Liver Disorder

-

Incontinence

-

Others

-

-

Drug Discovery and Development

-

-

Technology Outlook (Revenue, USD Million, 2018 - 2030)

-

Cell Acquisition

-

Bone Marrow Harvest

-

Umbilical Blood Cord

-

Apheresis

-

-

Cell Production

-

Therapeutic Cloning

-

In-vitro Fertilization

-

Cell Culture

-

Isolation

-

-

Cryopreservation

-

Expansion and Sub-Culture

-

-

Therapy Outlook (Revenue, USD Million, 2018 - 2030)

-

Autologous

-

Allogeneic

-

-

End-use Outlook (Revenue, USD Million, 2018 - 2030)

-

Pharmaceutical and Biotechnology Companies

-

Hospitals & Cell Banks

-

Academic & Research Institutes

-

-

Regional Outlook (Revenue, USD Million, 2018 - 2030)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global stem cells market size was estimated at USD 15.10 billion in 2024 and is expected to reach USD 16.84 billion in 2025.

The global stem cells market is expected to grow at a compound annual growth rate of 11.41% from 2025 to 2030 to reach USD 28.89 billion by 2030.

Adult stem cells dominated the stem cells market with a share of 70.76% in 2024 owing to their high penetration over other stem cell types and the presence of a substantial number of approved adult stem cell therapies for clinical use.

Some key players operating in the stem cells market include Advanced Cell Technology Inc., STEMCELL Technologies Inc., PromoCell GmbH, Cellular Engineering Technologies Inc., and others.

Key factors that are driving the stem cells market growth include the rising number of stem cell banks, the growing focus on increasing the therapeutic potential of these products, and extensive research for the development of regenerative medicines.

About the Author(s)

Biotechnology Research Team

Healthcare · BiotechnologyThis report was authored by the biotechnology research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the biotechnology segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.