- Home

- »

- Next Generation Technologies

- »

-

Cleaning Robot Market Size And Share Report, 2026-2033GVR Report cover

![Cleaning Robot Market (2026 - 2033)Report]()

Cleaning Robot Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type, By Product (In-House, Outdoor), By Charging (Automatic Charging, Manual Charging), By Operation Mode, By Distribution Channel, By End-use, By Region, And Segment Forecasts

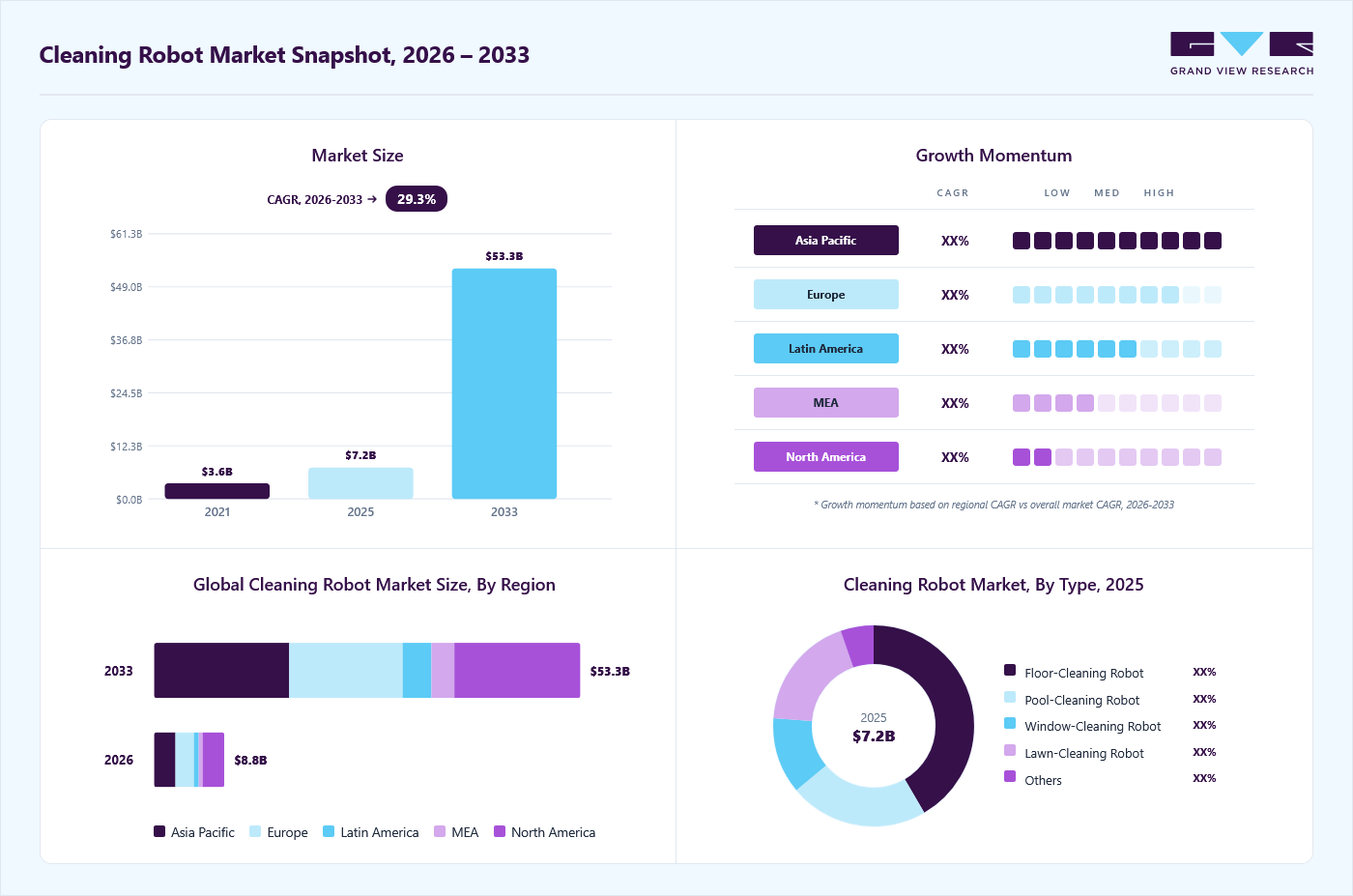

Market Size, 2025

$7.2BMarket Estimate, 2026

$8.8BMarket Forecast, 2033

$53.2BCAGR, 2026–2033

29.3%Cleaning Robot Market Summary

The global cleaning robot market size was valued at USD 7.2 billion in 2025 and is projected to grow from USD 8.8 billion in 2026 to USD 53.2 billion by 2033, growing at a CAGR of 29.3% from 2026 to 2033. North America dominated the global market with the largest revenue share of 31.3% in 2025. The cleaning robot market is witnessing strong growth, driven by the increasing adoption of autonomous cleaning solutions, AI-powered navigation, and smart home integration.

Key Market Trends & Insights

- By type: The floor-cleaning robot segment dominated the market, with a share of 41.6% in 2025.

- By product: The in-house robot segment accounted for the largest market share of 58.8% in 2025.

- By charging: The automatic charging segment dominated the market in 2025.

- By end use: The residential segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (31.3% revenue share in 2025)

- Fastest growing regional market: Asia Pacific (highest CAGR 30.0%, 2026-2033)

- By Country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 7.2 Billion

- Estimated market size in 2026: USD 8.8 Billion

- Projected market size by 2033: USD 53.2 Billion

- CAGR (2026-2033): 29.3%

The market is experiencing rapid growth, driven by increasing demand for automation and smart home technologies. Advancements in sensors, LiDAR, machine vision, and IoT connectivity are enhancing cleaning efficiency, while rising labor costs and growing demand for automated hygiene and sanitation solutions continue to accelerate market adoption across residential and commercial sectors. Consumers are prioritizing convenience and efficiency, making robotic cleaning solutions a preferred alternative to manual labor. Advances in artificial intelligence (AI) and machine learning have enhanced the adaptability and performance of cleaning robots, further accelerating market expansion. In addition, the rise of interconnected smart home ecosystems powered by the Internet of Things (IoT) has increased demand for remotely controlled cleaning robots. The growing affordability of entry-level models has further broadened consumer adoption. Moreover, as sustainability gains importance, manufacturers are focusing on energy-efficient and eco-friendly designs, aligning with consumers’ rising environmental consciousness.")

One of the key trends in the cleaning robot industry is the increasing integration of artificial intelligence (AI) and smart technology. Cleaning robots are becoming more intelligent and capable of mapping and navigating complex environments through advanced algorithms. AI allows these robots to improve their cleaning efficiency by learning from their surroundings and adapting to various surfaces. Smart features, such as remote control via smartphones and voice assistant integration (e.g., Alexa or Google Assistant), are enhancing the convenience of these devices. As the cleaning robot industry evolves, AI and smart technology will continue to drive the market, providing users with more efficient, automated, and customizable cleaning experiences.

The growing trend toward home automation is significantly driving market growth. Consumers are increasingly adopting smart home solutions that allow for seamless control of household tasks through interconnected devices. Cleaning robots are perfectly aligned with this trend, offering hands-free cleaning that integrates into a broader home automation ecosystem. With the rise of IoT-enabled devices, cleaning robots are becoming part of a smart home setup, where users can schedule, monitor, and control cleaning tasks remotely. This shift toward home automation is transforming the cleaning robot industry, making it an essential part of modern homes and expanding its market reach.

Another prominent trend in the market is the increasing affordability and accessibility of robotic cleaners. As technology has advanced and production costs have decreased, more brands are offering budget-friendly models that maintain high performance. This shift has made cleaning robots more accessible to a wider range of consumers, especially in emerging markets. The affordability of cleaning robots is opening new opportunities in regions where these devices were previously considered a luxury. As the cleaning robot industry continues to innovate, more affordable models will likely continue to drive the market's growth, making robotic cleaning solutions a common household tool.

The trend toward multi-functional cleaning robots is gaining momentum in the market. Consumers are increasingly looking for robots that can handle multiple tasks, such as vacuuming, mopping, and even window cleaning. The cleaning robot industry is responding by developing hybrid robots that can perform a combination of these tasks, reducing the need for multiple devices in the home. These versatile robots are becoming more popular due to their ability to save time and increase convenience for users. As demand for all-in-one cleaning solutions continues to rise, manufacturers in the cleaning robot industry are focusing on innovation to offer more efficient and multi-functional products.

Subscription-based models and software updates are emerging as a trend in the cleaning robot industry. Manufacturers are beginning to offer software and firmware updates on a subscription basis, allowing users to receive regular improvements and new features for their cleaning robots. This model also extends to maintenance services, where consumers can pay for regular check-ups, repairs, or upgrades. The cleaning robot industry is adopting this approach to create recurring revenue streams and build stronger relationships with consumers. As this trend grows, it ensures that clean robots remain up-to-date with the latest technology, making them even more reliable and user-friendly.

An important trend in the cleaning robot industry is the development of advanced navigation and mapping technologies. Modern cleaning robots are equipped with sensors, LiDAR (Light Detection and Ranging), and cameras that help them scan and map out the layout of a home or office. These technologies allow robots to clean more efficiently by ensuring that every area is covered without repeating or missing spots. The cleaning robot industry is focusing on improving these technologies to create robots that are not only more accurate but also faster and smarter at navigating obstacles. As this trend continues, robots will be able to clean more complex spaces, further enhancing their appeal in both residential and commercial markets.

Market Dynamics

The cleaning robot market is witnessing rapid adoption driven by artificial intelligence, machine vision, LiDAR mapping, and sensor-based technologies. These solutions enable users and facility operators to improve cleaning efficiency, reduce labor dependency, maintain consistent hygiene standards, and optimize operational workflows. The growing shift toward smart homes, intelligent buildings, and automated facility management systems, coupled with rising labor costs, increasing awareness of cleanliness and infection control, and continuous advancements in robotics, connectivity, and battery technologies, is accelerating market expansion. The increasing investments in service robotics, IoT-enabled cleaning platforms, and autonomous commercial cleaning solutions are expected to continue driving strong growth in the cleaning robot market across diverse end-use sectors.

The increasing penetration of smart home technologies is significantly accelerating the adoption of autonomous cleaning solutions among consumers. Modern cleaning robots are being integrated with connected home ecosystems, enabling users to schedule, monitor, and control cleaning activities remotely through mobile applications and voice-enabled assistants. This enhanced convenience aligns with evolving consumer preferences for automated household management, reducing the time and effort required for routine cleaning tasks while improving overall living standards.

Advancements in artificial intelligence, machine vision, LiDAR mapping, and sensor technologies are further strengthening the capabilities of autonomous cleaning systems. These technologies enable accurate navigation, obstacle avoidance, room mapping, and adaptive cleaning performance across diverse residential environments. As households continue investing in connected devices and intelligent home infrastructure, demand for cleaning robots is increasing due to their ability to deliver efficient, consistent, and hands-free cleaning experiences.

The relatively high cost of advanced cleaning robots remains a key challenge affecting wider adoption, particularly among price-sensitive consumers and small businesses. Premium models equipped with intelligent navigation systems, self-emptying docks, AI-powered mapping, and enhanced connectivity often require a significant investment. This cost barrier can discourage potential buyers from switching from conventional cleaning methods, despite the operational benefits of robotic solutions.

In addition to purchase expenses, ongoing maintenance requirements contribute to total ownership costs. Battery replacements, software updates, component servicing, and occasional repairs can increase long-term costs for users. Furthermore, consumers may remain hesitant to evaluate the return on investment for robotic cleaning systems, particularly in regions where manual labor remains relatively affordable and readily available for routine cleaning.

The growing emphasis on cleanliness, compliance with hygiene standards, and operational efficiency in commercial facilities is creating substantial opportunities for autonomous cleaning technologies. Airports, healthcare institutions, educational campuses, retail complexes, hospitality establishments, and corporate offices are increasingly exploring robotic cleaning systems to maintain consistent sanitation standards while reducing reliance on manual cleaning personnel. These environments require frequent and large-scale cleaning operations that can benefit from automation and standardized performance.

Technological advancements are enabling cleaning robots to perform specialized tasks such as floor scrubbing, disinfection, waste collection, and continuous facility monitoring. Enhanced navigation capabilities, cloud-based fleet management platforms, and real-time performance analytics are improving deployment effectiveness across large facilities. As organizations seek scalable solutions to address workforce shortages, rising labor expenses, and stricter hygiene requirements, autonomous sanitation systems are becoming an increasingly attractive operational investment.

Market Concentration & Characteristics

The cleaning robot market is moderately concentrated, comprising established robotics manufacturers, consumer electronics companies, automation technology providers, and a growing number of specialized robotic cleaning solution developers. The market is expanding due to increasing adoption of autonomous cleaning systems across residential, commercial, and industrial environments, rising demand for labor-saving technologies, and growing emphasis on hygiene maintenance. Strategic partnerships between robotics developers, smart home platform providers, and facility management companies are becoming increasingly common as organizations focus on improving operational efficiency and cleaning effectiveness. Continuous advancements in AI, machine vision, LiDAR-based navigation, sensor technologies, and IoT connectivity are emerging as competitive strategies in the market.

The market is characterized by a very high level of innovation, driven by rapid developments in intelligent mapping systems, autonomous navigation capabilities, obstacle recognition technologies, self-maintenance features, and cloud-connected fleet management platforms. The industry is witnessing moderate merger and acquisition activity as companies seek to strengthen technological capabilities, expand product portfolios, and enhance market presence. Competition from conventional cleaning equipment and manual cleaning services remains moderate, particularly in cost-sensitive segments, although automated cleaning solutions continue to gain wider acceptance. Increasing investments in smart buildings, connected home ecosystems, autonomous facility management solutions, and advanced robotics technologies are expected to further support market expansion.

Analyst Perspective

The cleaning robot market is experiencing strong expansion driven by the increasing adoption of autonomous cleaning technologies, rising demand for labor-saving solutions, and growing integration of artificial intelligence, machine vision, and advanced sensor systems across residential, commercial, and industrial environments. The industry is benefiting from a shift toward automated facility management and smart home ecosystems, where efficient cleaning operations, consistent hygiene standards, and reduced manual intervention are becoming key priorities for end users. Growing investments in smart buildings, commercial automation, and robotic sanitation solutions are supporting wider deployment of cleaning robots in healthcare facilities, hospitality, retail centers, warehouses, and public infrastructure environments, strengthening long-term market adoption.

Type Insights

Based on type, the floor-cleaning robot segment led the market with the largest revenue share of 41.6% in 2025 and is expected to grow at a considerable CAGR over the forecast period. The growth is primarily driven by increasing urbanization and the adoption of automation in households and commercial spaces. Consumers, particularly working professionals, are drawn to these robots for their ability to save time and effort. The integration of AI, IoT, and machine learning technologies has enhanced their functionality, enabling features such as real-time mapping, obstacle detection, and voice assistant compatibility. A key trend in this segment is the rising demand for multi-functional robots that combine vacuuming and mopping capabilities. Floor-cleaning robots are increasingly integrated with smart home systems, allowing users to control them via apps or voice commands. The commercial sector, including offices and healthcare facilities, is also adopting these robots to maintain high hygiene standards efficiently.

The pool-cleaning robot segment is expected to witness a significant CAGR of 25.2% from 2026 to 2033, fueled by growing health consciousness and the need for maintaining clean swimming environments in residential and commercial spaces such as hotels and resorts. These robots offer an efficient solution for removing debris, algae, and contaminants from pools without manual intervention, aligning with public health priorities. Advanced pool-cleaning robots equipped with AI-driven navigation and energy-efficient motors are gaining traction. Features such as smartphone control and scheduling are increasingly popular among users. In addition, solar-powered pool cleaners are emerging as a trend for eco-conscious consumers seeking sustainable cleaning solutions.

Product Insights

Based on product, the in-house segment led the market with the largest revenue share of 58.8% in 2025. The segmental growth is driven by the growing demand for time-saving and convenient cleaning solutions in residential spaces. As urbanization increases and lifestyles become busier, consumers are increasingly looking for automated devices to help with daily chores like vacuuming and mopping. In addition, the rise of smart homes, where devices are interconnected through IoT, has further boosted the popularity of in-house cleaning robots, as they can be controlled remotely via smartphones or voice assistants. With advancements in artificial intelligence (AI) and improved navigation technologies, these robots are becoming more efficient, user-friendly, and capable of cleaning complex spaces, which is driving their adoption among tech-savvy consumers.

The outdoor robot segment is expected to record the fastest CAGR from 2026 to 2033. The outdoor cleaning robot segment is driven by the growing need for automated solutions in large-scale commercial and industrial environments. As cities expand and infrastructure projects increase, there is a greater demand for efficient cleaning of outdoor spaces such as streets, parking lots, and large public areas. In addition, with the rise in demand for maintenance in residential outdoor spaces such as gardens, pools, and driveways, robotic lawnmowers and pool cleaners are gaining popularity. The commercial sector, particularly in tourism-heavy regions, is also driving demand for outdoor robots, as businesses in hospitality, retail, and public service industries seek to reduce operational costs and improve the efficiency of outdoor cleaning tasks, such as sweeping and scrubbing.

Charging Insights

Based on charging, the automatic charging segment accounted for the largest revenue share of 63.6% in 2025. Consumers and businesses are seeking robots that can operate autonomously without the need for manual intervention, including charging. With automatic charging, cleaning robots can dock themselves to recharge when their battery runs low, ensuring that they are always ready for the next cleaning session. This feature is particularly popular in residential and commercial markets, where users prioritize ease of use and uninterrupted performance. The trend is moving toward even smarter automatic charging systems, with robots that can return to specific charging stations or recharge themselves more quickly. As these robots become more efficient and affordable, automatic charging is expected to become the standard in both residential and commercial cleaning solutions.

The manual charging segment is expected to record the fastest CAGR from 2026 to 2033, primarily driven by a preference for more cost-effective and simpler robotic cleaning solutions, especially in lower-priced models. Manual charging requires the user to place the robot on a charging dock to recharge, which may appeal to consumers who do not mind performing this small task in exchange for a lower initial purchase price. While manual charging may be less convenient than automatic charging, it is still widely used in entry-level cleaning robots. Trends in this segment include the continued use of manual charging for budget-conscious consumers and in regions where affordability is a higher priority than advanced features. In addition, manual charging robots are often more straightforward in design, making them a more accessible option for consumers who prefer a basic, no-frills cleaning solution.

Operation Mode Insights

Based on operation mode, the self-drive segment held the largest market share of 60.7% in 2025, primarily driven by the increasing demand for fully autonomous, hands-off cleaning solutions. Consumers and businesses prefer robots that can navigate and clean spaces on their own without requiring manual intervention or remote control. This feature is particularly popular in both residential and commercial environments, as it offers convenience and efficiency. The trend is leaning toward robots with advanced AI and sensor technologies that enable them to map, plan, and clean in complex environments. Self-drive robots are becoming more sophisticated, with capabilities such as real-time navigation, obstacle detection, and even smart scheduling, allowing users to set cleaning routines and leave the robots to handle tasks autonomously. As technology improves, self-drive robots are expected to dominate the market due to their ease of use and increasing effectiveness.

The remote control segment is expected to record the fastest CAGR from 2026 to 2033, fueled by the preference for greater user control and customization, where consumers and businesses can direct the robot’s movements and cleaning tasks. While self-drive robots are becoming more popular, remote-controlled robots still appeal to users who want more manual input or control over specific areas of cleaning. This mode is particularly prevalent in industrial and commercial settings, where cleaning robots might need to be directed in more specialized ways or to clean specific zones. The trend in this segment is toward the development of more intuitive and user-friendly remote-control interfaces, often integrated with smartphone apps or advanced remotes. In addition, remote control robots are also appealing to those who may want to supervise the cleaning process or intervene in areas that require more detailed attention.

Distribution Channel Insights

Based on distribution channel, the online segment accounted for the largest revenue share of 53.5% in 2025. The segmental growth is driven by the growing preference for convenience, competitive pricing, and the wide variety of options available to consumers. E-commerce platforms offer a convenient shopping experience where customers can compare different brands, read reviews, and access promotional discounts, making it easier to find cleaning robots that suit their needs. The trend is toward increased reliance on online platforms, especially with the rise of direct-to-consumer sales models from leading robot manufacturers. In addition, the growing influence of online retailers such as Amazon and specialized home automation stores has expanded access to cleaning robots globally, further accelerating adoption. With home delivery services and easier return policies, online shopping has become the preferred method for purchasing cleaning robots.

The offline segment is expected to record the fastest CAGR from 2026 to 2033. The segmental growth is driven by consumers' preference for hands-on interaction and the ability to physically examine products before purchase. In traditional brick-and-mortar stores, customers can receive direct support and demonstrations from sales personnel, which can be particularly valuable for those unfamiliar with robotic technology. This is especially important in regions where consumers prioritize trust in the product and wish to see the robot in action before buying. The trend in offline sales is also supported by the growing presence of consumer electronics retailers and department stores, where cleaning robots are being integrated into product displays.

End-use Insights

Based on end use, the residential segment dominated the market with the largest revenue share of 55.9% in 2025. driven by the increasing demand for convenience and time-saving solutions as modern lifestyles become busier. Consumers are seeking automated cleaning devices that can efficiently handle daily chores, such as vacuuming, mopping, and even window cleaning, without the need for constant supervision. In addition, the growing adoption of smart home technologies, where robots can be integrated with voice assistants and controlled remotely via smartphones, is driving market growth. As these robots become more affordable, compact, and capable of handling complex tasks, the trend toward automation in homes is expected to continue, with many consumers preferring models that offer advanced navigation systems, improved cleaning performance, and multi-functional capabilities.

The industrial segment is expected to record the fastest CAGR from 2026 to 2033, fueled by the increasing need for automation in large-scale manufacturing, warehouse, and logistics operations, where cleaning tasks are often labor-intensive and require high efficiency. As companies seek to reduce operational costs and improve workplace safety, they are turning to robots to handle hazardous cleaning tasks, such as those involving chemicals or heavy machinery. The trend in this segment is the adoption of highly specialized robots, such as floor scrubbing machines and robotic sweepers, designed for harsh industrial environments. In addition, advancements in AI, robotics, and sensor technologies are enabling these robots to navigate complex spaces, operate autonomously, and enhance productivity, which is making them increasingly attractive to industrial operators.

Regional Insights

North America dominated the cleaning robot market with the largest revenue share of 31.3% in 2025. The market growth is driven by the high adoption rates of smart home technologies, increasing disposable incomes, and a growing demand for automation in household chores. The region benefits from advanced technological infrastructure, including widespread 5G networks and IoT integration, which significantly enhances the functionality of cleaning robots. In addition, in North America, heightened hygiene standards in workplaces have led to partnerships and collaborations aimed at leveraging advanced technologies for maintaining cleanliness and safety.

U.S. Cleaning Robot Market Trends

The cleaning robot market in the U.S. held the largest share in the North America region in 2025. The U.S. market is driven by advancements in automation technologies, increasing demand for time-saving solutions, and the widespread adoption of smart home ecosystems. Urban consumers, particularly those with busy lifestyles, are embracing cleaning robots for their ability to operate autonomously and efficiently, reducing the need for manual intervention. In addition, the National Institute for Occupational Safety and Health (NIOSH) in the U.S. has been actively working on robotics safety through its Center for Occupational Robotics Research.

Europe Cleaning Robot Market Trends

The Europe cleaning robot industry was identified as a lucrative region in 2025. Market growth is driven by increasing investments in robotics and automation across residential, commercial, and industrial sectors. The region's focus on digital transformation and smart technologies, such as IoT and AI, has accelerated the adoption of cleaning robots. Rising awareness about hygiene and cleanliness, especially post-pandemic, has further fueled demand for these solutions in homes, offices, healthcare facilities, and public spaces.

The cleaning robot industry in the UK is driven by the increasing demand for automation and cost-efficiency in both commercial and residential spaces. With the rise of dual-income households and busy urban lifestyles, there is a growing preference for time-saving solutions like cleaning robots. In addition, the UK has a high adoption rate of smart home technologies, which drives the integration of robotic cleaners into connected home ecosystems.

Germany’s cleaning robot industry is largely driven by the country’s robust industrial and manufacturing sectors, where automation is highly valued to improve operational efficiency. German businesses, particularly in manufacturing, logistics, and healthcare, are increasingly adopting robotic cleaners to reduce labor costs and ensure consistent cleanliness in large facilities. The country’s strong focus on technological innovation also contributes to the market's growth, as businesses are quick to adopt the latest advancements in robotics for both commercial and residential cleaning applications.

Asia-Pacific Cleaning Robot Market Trends

The cleaning robot industry in the Asia Pacific region is expected to grow at the fastest CAGR of over 24.4% from 2026 to 2033. The APAC region is witnessing a surge in demand for advanced cleaning robots equipped with AI-driven navigation, real-time mapping, and voice assistant compatibility. In densely populated cities across China and South Korea, compact and efficient cleaning robots are becoming increasingly popular due to space constraints. Japan is leading the trend of specialized robots, such as window-cleaning robots for high-rise buildings. The commercial sector across APAC is also adopting disinfection robots in response to heightened hygiene standards post-pandemic, particularly in healthcare and hospitality industries.

The cleaning robot industry in China is driven by the country's strong manufacturing base and rapid urbanization. Chinese consumers are increasingly adopting cleaning robots due to their growing disposable incomes and preference for smart home technologies. A key trend in China is the increasing popularity of high-end models equipped with AI-powered navigation and real-time mapping, catering to a tech-savvy consumer base.

The cleaning robot industry in India is driven by rising disposable incomes, increasing urbanization, and a growing awareness of automated solutions for household chores. Indian consumers are particularly drawn to robotic vacuum cleaners that are affordable and capable of handling diverse floor types common in Indian homes. A key driver is the post-pandemic focus on hygiene, which has encouraged households and businesses to adopt cleaning robots for enhanced sanitation. Another notable trend in India is the growing presence of international brands such as iRobot alongside local players offering budget-friendly options.

Key Cleaning Robot Company Insights

Some of the key players operating in the market include iRobot Corporation and LG Electronics

-

iRobot Corporation is a leader in the home cleaning robot industry, best known for its Roomba series of robotic vacuum cleaners. The company focuses on delivering autonomous cleaning solutions with intelligent navigation and mapping features. Over the years, iRobot has expanded its portfolio to include other robots, such as mopping robots (Braava). With its strong brand presence, iRobot continues to dominate the global market and innovate with new, advanced cleaning technologies.

-

LG Electronics is a well-established player in the consumer electronics sector, offering a range of robotic cleaning products, including the LG CordZero robotic vacuum series. Their cleaning robots are equipped with AI-powered sensors and advanced navigation systems for efficient and precise cleaning. LG also integrates smart home features into their robots, making them compatible with voice assistants like Google Assistant and Alexa. With a focus on smart, energy-efficient devices, LG remains a dominant force in the cleaning robot industry.

Ecovacs Robotics Inc. and Neato Robotics Inc are some of the emerging participants in the cleaning robot industry.

-

Ecovacs Robotics Inc. is an emerging player known for its Deebot series of robotic vacuums and mops, which have gained popularity in recent years due to their affordability and effective performance. The company emphasizes the integration of advanced features like AI-driven navigation and real-time mapping. Ecovacs has also developed cleaning robots for more specialized tasks, such as window and pool cleaning. With a growing global footprint, Ecovacs is rapidly positioning itself as a significant competitor in the robotic cleaning space.

-

Neato Robotics Inc is an innovative company that specializes in the design of D-shaped robotic vacuums that provide superior edge-cleaning capabilities compared to traditional round-shaped models. Their products feature laser-guided mapping and advanced navigation, allowing them to clean large areas with precision. Neato is also focused on developing robots that are easy to maintain, with features such as washable filters. Though newer to the market, Neato’s focus on design and efficiency has made it stand out in the cleaning robots industry.

Key Cleaning Robot Companies:

The following key companies have been profiled for this study on the cleaning robot market.

-

Ecovacs Robotics Inc.

-

ILIFE Robotics Technology

-

iRobot Corporation

-

LG Electronics

-

Maytronics

-

Milagrow Business and Knowledge Solutions Pvt. Ltd.

-

Neato Robotics Inc.

-

Nilfisk Group

-

Pentair Plc

-

Samsung Electronics Co. Ltd.

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (iRobot Corporation, Samsung Electronics Co. Ltd., LG Electronics)

- Established players focus on expanding intelligent cleaning ecosystems through AI, IoT, and smart home partnerships.

- Invest heavily in robotic navigation and the development of autonomous cleaning platforms.

- Strong global distribution networks, established brand recognition, and extensive customer base.

- Ability to deliver reliable, feature-rich, and technologically advanced cleaning solutions.

- Dependence on premium pricing strategies may limit penetration among budget-conscious customers.

- Large organizational structures can reduce flexibility in responding to emerging trends.

Emerging Players (Ecovacs Robotics Inc., ILIFE Robotics Technology, Milagrow Business and Knowledge Solutions Pvt. Ltd.)

- Focus on developing affordable autonomous cleaning solutions targeting underserved customer segments.

- Invest in AI navigation capabilities and smart connectivity features for differentiation.

- Greater operational flexibility enables faster product innovation and market responsiveness.

- Ability to address niche cleaning applications through specialized robotic solutions.

- Limited brand recognition may restrict customer acquisition across competitive markets.

- Smaller financial resources can constrain large-scale expansion and technology investments.

Recent Developments

-

In February 2025, Nilfisk launched its next generation of vacuum cleaners, including the VP300 and VP400 compact canister vacuums, engineered for high performance with intuitive controls and easy maneuverability, and the VU200 cordless stick vacuum, designed for quick and efficient spot cleaning. These vacuums, certified for professional use, offer enhanced filtration systems, user-friendly designs, and are part of Nilfisk’s wide range of next-generation solutions launching throughout 2025.

-

In January 2025, Ecovacs Robotics, Inc. introduced its latest innovations at CES 2025, including the DEEBOT X8 PRO OMNI with advanced self-washing mopping technology and the GOAT A3000 LiDAR robotic lawn mower featuring multi-technology navigation. The company also expanded its WINBOT series for enhanced window cleaning. The DEEBOT X8 PRO OMNI and T50 MAX PRO were launched in February.

-

In December 2024, Skyline Robotics partnered with Alimak Group to automate building maintenance using Alimak’s access solutions and Skyline’s robotics technology. The collaboration aims to focus on autonomous window cleaning, starting with Skyline's Ozmo robot, to improve efficiency, sustainability, and address labor shortages in the construction industry. Alimak Group has also invested in Skyline to support this initiative.

Cleaning Robot Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 7.2 billion

Market size value in 2026

USD 8.8 billion

Revenue forecast in 2033

USD 53.2 billion

Growth rate

CAGR of 29.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, Volume in thousand units, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, product, charging, operation mode, distribution channel, end-use, and region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico, U.K.; Germany; France; China; Japan; India; South Korea; Australia; Brazil; South Africa; Saudi Arabia; UAE

Key companies profiled

Ecovacs Robotics Inc.; ILIFE Robotics Technology; iRobot Corporation; LG Electronics; Maytronics; Milagrow Business and Knowledge Solutions Pvt. Ltd.; Neato Robotics Inc.; Nilfisk Group; Pentair Plc; Samsung Electronics Co. Ltd.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cleaning Robot Market Report Segmentation

This report forecasts and estimates revenue and volume growth at the global, regional, and country levels and analyzes the latest market trends in each one of the sub-segments from 2021 to 2033. For this study, Grand View Research has further segmented the global cleaning robot market report based on type, product, charging, operation mode, distribution channel, end-use, and region:

-

Type Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Floor-Cleaning Robot

-

Pool-Cleaning Robot

-

Window-Cleaning Robot

-

Lawn-Cleaning Robot

-

Others

-

-

Product Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

In-House

-

Outdoor

-

-

Charging Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Automatic Charging

-

Manual Charging

-

-

Operation Mode Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Self-Drive

-

Remote Control

-

-

Distribution Channel Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Online

-

Offline

-

-

End-use Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

Residential

-

Commercial

-

Industrial

-

-

Regional Outlook (Volume, Thousand Units; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

UK

-

Germany

-

Rest of Europe

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Rest of Asia

-

-

Latin America

-

Brazil

-

Mexico

-

Rest of Latin America

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

Rest of Middle East & Africa

-

-

Research Methodology

The cleaning robot market figures in this report are based on a proven research process that combines executive interviews with secondary research from proprietary databases, company filings, and recognized regulatory and institutional sources. Market size is built through value-chain sizing - reconciling supply-side and demand-side estimates - and triangulated with bottom-up and top-down approaches. Every estimate passes multiple levels of expert validation before publication, with each cleaning robot segment quantified using the revenue-capture definitions in the table below.

Segment Definition

Segment - Type

Revenue capture definition

Floor-Cleaning Robot

Revenue is captured through autonomous robotic vacuum cleaners, mopping robots, scrubbing robots, and hybrid floor-cleaning systems used across residential, commercial, and industrial environments. This segment is driven by increasing demand for automated floor maintenance and growing adoption of smart home cleaning solutions.

Pool-Cleaning Robot

Revenue is generated through robotic systems designed for automated swimming pool cleaning, including debris removal, wall scrubbing, and waterline maintenance. This segment is driven by rising installation of residential and commercial pools, increasing focus on maintenance efficiency, and demand for labor-saving cleaning technologies.

Window-Cleaning Robot

Revenue is captured through robotic devices that automate glass surface cleaning in residential buildings, commercial complexes, and high-rise structures. This segment is driven by growing urbanization, the construction of multi-story buildings, and rising demand for safer, more efficient exterior maintenance solutions.

Lawn-Cleaning Robot

Revenue is generated through autonomous robotic systems used for lawn maintenance, debris collection, and grass management in residential and commercial outdoor spaces. This segment is driven by increasing adoption of smart gardening equipment, labor cost reduction initiatives, and demand for automated landscape maintenance.

Others

Revenue is generated through specialized cleaning robots, such as solar panel-cleaning robots, gutter-cleaning robots, disinfection robots, and industrial surface-cleaning systems. This segment is driven by expanding application areas, increasing automation requirements, and growing investments in advanced service robotics.

Segment - Product

Revenue capture definition

In-House

Revenue is generated through robotic cleaning solutions designed for indoor applications, including homes, offices, healthcare facilities, hospitality establishments, and retail environments. This segment is driven by increasing demand for automated indoor cleaning, smart building integration, and rising emphasis on hygiene management.

Outdoor

Revenue is captured through robotic cleaning systems deployed in outdoor environments such as gardens, public spaces, swimming pools, solar farms, and industrial facilities. This segment is driven by growing infrastructure development, expanding outdoor maintenance requirements, and increasing adoption of autonomous service robots.

Segment - Charging

Revenue capture definition

Automatic Charging

Revenue is generated through cleaning robots equipped with self-docking capabilities that automatically return to charging stations when battery levels are low. This segment is driven by increasing consumer preference for fully autonomous operation, enhanced convenience, and advancements in robotic battery management systems.

Manual Charging

Revenue is captured through robotic cleaning systems requiring direct user intervention for battery charging and power management. This segment is driven by demand for cost-effective robotic solutions and adoption among budget-conscious residential and commercial users.

Segment - Charging

Revenue capture definition

Self-Drive

Revenue is generated through autonomous cleaning robots capable of independent navigation, route planning, obstacle avoidance, and task execution using advanced sensors and artificial intelligence technologies. This segment is driven by rising demand for hands-free cleaning solutions and continuous advancements in robotic autonomy.

Remote Control

Revenue is captured through robotic cleaning systems operated through remote-control devices, mobile applications, or wireless communication interfaces. This segment is driven by user preference for operational flexibility, controlled cleaning activities, and deployment in specialized cleaning applications.

Segment - Distribution Channel

Revenue capture definition

Online

Revenue is generated through e-commerce platforms, company-owned websites, online marketplaces, and digital retail channels offering robotic cleaning products directly to consumers and businesses. This segment is driven by increasing online shopping penetration, product accessibility, and availability of competitive pricing options.

Offline

Revenue is captured through electronics stores, specialty retail outlets, distributors, wholesalers, and direct sales networks. This segment is driven by consumer preference for physical product evaluation, personalized assistance, and established retail distribution infrastructure.

Segment - End Use

Revenue capture definition

Residential

Revenue is generated through the adoption of robotic cleaning solutions for automated floor, window, lawn, and pool cleaning. This segment is driven by increasing smart home adoption, busy lifestyles, and growing demand for convenient household automation technologies.

Commercial

Revenue is captured through deployments in offices, shopping centers, hotels, healthcare facilities, educational institutions, airports, and public infrastructure. This segment is driven by rising hygiene standards, labor optimization initiatives, and demand for efficient large-area cleaning operations.

Industrial

Revenue is generated through robotic cleaning systems utilized in manufacturing facilities, warehouses, logistics centers, production plants, and industrial complexes. This segment is driven by increasing industrial automation, workplace safety requirements, and the need for efficient maintenance of large-scale operational environments.

Estimation Model

Layer Name

Key Question

Description

Application Base Layer

Who are the potential adopters?

Identifies the total addressable base, including households, commercial facilities, healthcare institutions, hospitality establishments, educational campuses, retail centers, industrial facilities, warehouses, airports, and public infrastructure operators that require automated cleaning, sanitation, and maintenance solutions.

Automation Readiness Layer

Who can implement autonomous cleaning systems?

Adoption is determined by factors such as automation readiness, smart building infrastructure availability, labor cost considerations, facility size, digital connectivity, budget allocation for robotics investments, and organizational willingness to integrate autonomous cleaning technologies into daily operations.

Deployment Layer

Who actively deploys cleaning robot solutions?

Applies adoption levels across end-use environments where cleaning robots are actively utilized, including robotic vacuum cleaners in residential settings, autonomous floor scrubbers in commercial facilities, sanitation robots in healthcare institutions, pool-cleaning robots, window-cleaning robots, and industrial cleaning systems in manufacturing and logistics facilities.

Revenue Generation Layer

How is revenue generated?

Revenue is generated through the sale of robotic vacuum cleaners, floor-cleaning robots, window-cleaning robots, pool-cleaning robots, lawn-cleaning robots, industrial cleaning systems, maintenance services, replacement components, battery systems, and recurring revenue from connected robotic cleaning solutions and service contracts.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Autonomous Cleaning Deployment Assessment & Operational Feasibility Evaluation

Conducted detailed evaluation of autonomous cleaning systems across residential, commercial, and industrial environments, integrating AI-powered navigation, LiDAR mapping, obstacle detection technologies, fleet management platforms, and automated maintenance capabilities to optimize cleaning performance and resource utilization.

Enables efficient cleaning operations, reduces labor dependency, improves facility maintenance consistency, and enhances overall operational productivity.

Smart Facility Cleaning Automation Integration Strategy

Assessed deployment of robotic cleaning technologies within smart buildings, healthcare facilities, hospitality establishments, retail centers, and corporate environments, integrating IoT connectivity, cloud-based monitoring systems, automated scheduling tools, and real-time performance analytics.

Enhances cleaning efficiency, improves hygiene compliance, supports predictive maintenance, and enables intelligent facility management operations.

Commercial Sanitation Robotics Optimization & Infrastructure Planning

Evaluated implementation of advanced floor-cleaning robots, disinfection systems, window-cleaning robots, and industrial cleaning solutions across large-scale facilities, supported by AI-driven route optimization, autonomous charging infrastructure, and centralized robotic fleet management platforms.

Enables scalable sanitation operations, improves cleaning quality, reduces operating costs, and supports continuous maintenance across high-traffic environments.

Frequently Asked Questions About This Report

The global cleaning robot market size was valuedat USD 7.2 billion in 2025 and is expected to reach USD 8.8 billion in 2026.

The global cleaning robot market is expected to grow at a compound annual growth rate of 29.3% from 2026 to 2033 to reach USD 53.2 billion by 2033.

North America dominated the cleaning robot market with a share of nearly 31.3 % in 2025.

Some key players operating in the cleaning robot market include Ecovacs Robotics, Inc.; ILIFE Robotics Technology; iRobot Corporation; LG Electronics; Maytronics; Milagrow Business and Knowledge Solutions (Pvt.) Limited; Neato Robotics, Inc.; Nilfisk Group; Pentair plc; and Samsung Electronics Co., Ltd.

Key factors that are driving the cleaning robot market growth include penetration of automation in household appliances and the development of AI-enabled and voice-controlled smart cleaning robots.

The floor-cleaning robot segment dominated the market, with a share of 41.6% in 2025.

The in-house robot segment accounted for the largest market share of 58.8% in 2025.

The automatic charging segment dominated the market in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.