- Home

- »

- Next Generation Technologies

- »

-

Cloud Compliance Market Size And Share Report, 2026-2033GVR Report cover

![Cloud Compliance Market (2026 - 2033)Report]()

Cloud Compliance Market (2026 - 2033)

Size, Share, & Trend Analysis Report By Component (Software, Services), By Model, By Enterprise Size, By Application, By End Use, By Region (North America, Europe, Asia Pacific, Latin America, MEA), and Segment Forecasts

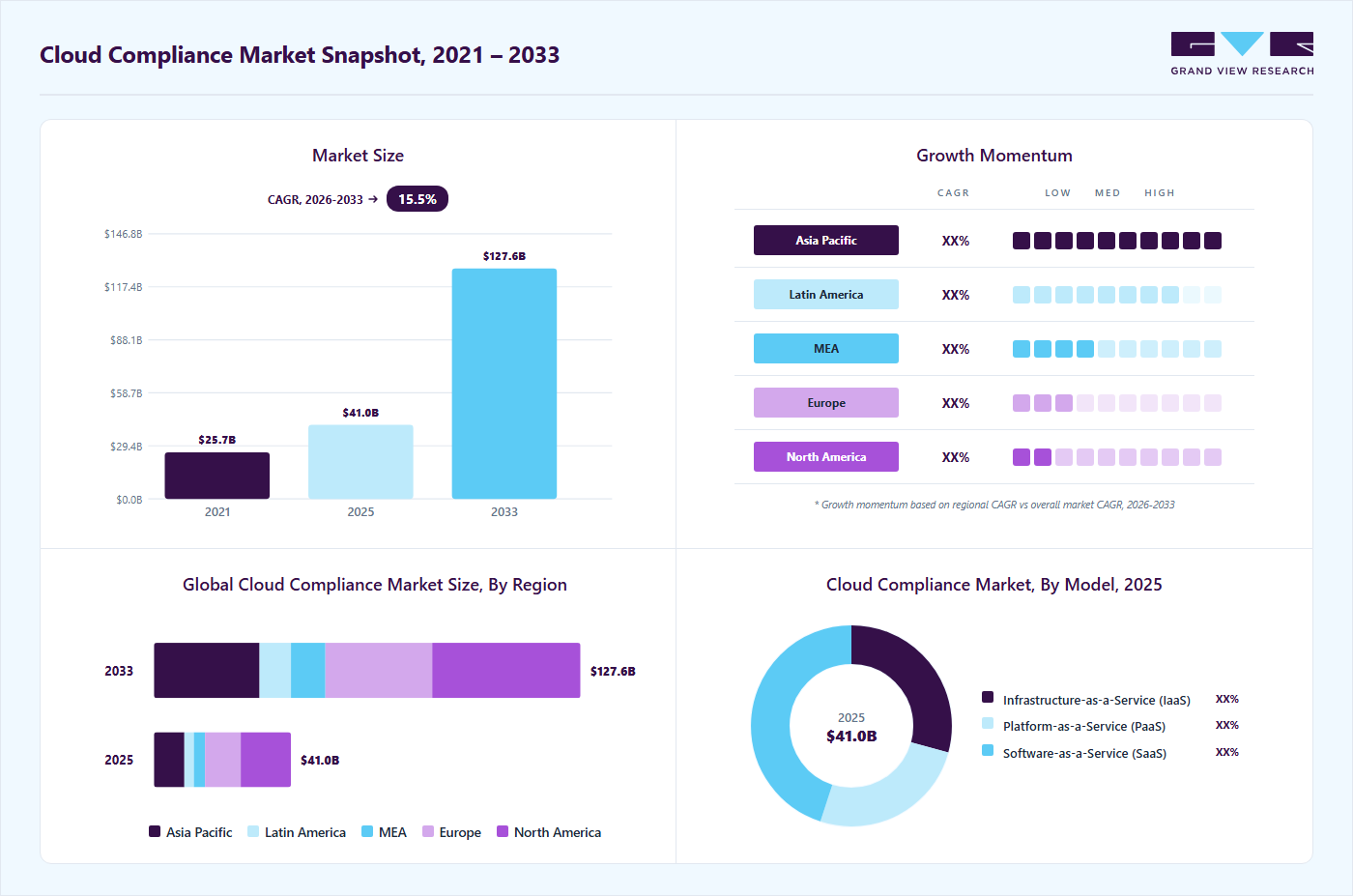

Market Size, 2025

$41.0BMarket Estimate, 2026

$46.6BMarket Forecast, 2033

$127.6BCAGR, 2026–2033

15.5%Cloud Compliance Market Summary

The global cloud compliance market size was valued at USD 41.0 billion in 2025 and is projected to grow from USD 46.6 billion in 2026 to USD 127.6 billion by 2033, at a CAGR of 15.5% from 2026 to 2033. North America held the largest revenue share of 36.6% of the global market in 2025. The industry is experiencing robust growth driven by accelerating cloud adoption, rising regulatory scrutiny, and the increasing complexity of managing compliance across multi-cloud and hybrid IT environments.

Key Market Trends & Insights

- By component: Software segment held the largest revenue share of 69.3% in 2025.

- By model: SaaS segment held the largest revenue share in 2025.

- By enterprise size: Large enterprises held the largest revenue share in 2025.

- By application: Audit & compliance management held the largest revenue share in 2025.

- By end use: BFSI segment held the largest revenue share in 2025.

Regional Highlights

- Largest regional market: North America (36.6% market share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR from 2026–2033)

- By Country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 41.0 Billion

- Market size in 2026: USD 46.6 Billion

- Projected market size by 2033: USD 127.6 Billion

- CAGR (2026–2033): 15.5%

The widespread deployment of SaaS applications, containerized workloads, and distributed cloud infrastructure has significantly expanded organizational data footprints, intensifying the need for continuous compliance monitoring, governance, and risk management. Additionally, growing data privacy mandates, cross-border data transfer regulations, and industry-specific compliance requirements are further propelling demand for automated cloud compliance solutions.

")

Cloud-first and hybrid organizations are prioritizing compliance solutions that seamlessly integrate with IaaS, PaaS, and SaaS environments, enabling consistent enforcement of regulatory controls across workloads hosted in public, private, and hybrid clouds. These platforms support continuous compliance through automated assessments, real-time alerts, and remediation workflows aligned with frameworks such as ISO/IEC 27001, NIST, SOC 2, GDPR, HIPAA, PCI DSS, and regional data sovereignty regulations. The growing emphasis on DevSecOps is also driving adoption of compliance-as-code and policy-as-code capabilities embedded directly into cloud development and deployment pipelines.

The cloud compliance market is witnessing increased adoption of AI- and ML-driven analytics to identify misconfigurations, predict compliance risks, and prioritize remediation efforts. Vendors are differentiating through advanced features such as automated evidence collection, continuous audit readiness, cloud security posture management (CSPM), identity and access governance, and compliance reporting dashboards tailored for regulators and internal stakeholders. In addition, the rise of remote work, third-party cloud integrations, and complex supply chains is accelerating demand for managed compliance services and unified governance, risk, and compliance (GRC) platforms.

Moreover, heightened focus on data privacy, sovereignty, and ethical data usage is encouraging enterprises to adopt privacy-by-design and compliance-by-default strategies within their cloud environments. Organizations are increasingly leveraging automated compliance controls to support business agility while reducing regulatory risk and audit costs. As a result, the industry is evolving from point-in-time compliance checks to continuous, intelligence-driven compliance ecosystems that provide real-time assurance, operational transparency, and regulatory confidence. Therefore, cloud compliance has become a strategic enabler for secure digital transformation, helping enterprises balance innovation, governance, and trust in an increasingly regulated digital economy.

Market Dynamics

The increasing complexity of global data privacy regulations and industry-specific compliance mandates is significantly driving the growth of the cloud compliance market. As enterprises rapidly migrate workloads across hybrid and multi-cloud environments, organizations are facing growing challenges in maintaining continuous compliance with evolving frameworks such as GDPR, HIPAA, PCI DSS, DORA, SOC 2, and NIS2. This has accelerated demand for automated cloud compliance solutions capable of providing real-time monitoring, policy enforcement, audit readiness, and centralized governance across distributed cloud infrastructures.

For instance, in 2025, enterprises across Europe and North America increased investments in automated cloud governance and compliance tools following the implementation of stricter digital resilience and cybersecurity regulations such as the EU’s Digital Operational Resilience Act (DORA) and NIS2 directive. These regulations require organizations to continuously monitor cloud environments, strengthen third-party risk oversight, and maintain auditable cybersecurity controls, encouraging widespread adoption of cloud compliance automation platforms. Additionally, the growing use of SaaS applications, remote work infrastructure, and cross-border data processing is increasing the need for continuous compliance visibility and automated regulatory reporting. Therefore, the rising pressure to manage dynamic regulatory requirements efficiently across cloud ecosystems is significantly contributing to the growth of the cloud compliance market.

Restraints: Complexity of managing compliance across diverse cloud ecosystems limiting market growth

The complexity of managing compliance across diverse cloud platforms and rapidly evolving regulatory environments is one of the major factors restraining the growth of the cloud compliance market. Many organizations operate across multiple public, private, and hybrid cloud infrastructures, each with different security configurations, access policies, and compliance requirements. This creates challenges related to policy standardization, visibility gaps, data classification inconsistencies, and fragmented governance processes.

For instance, enterprises managing multi-cloud environments face difficulties in mapping compliance controls consistently across AWS, Microsoft Azure, Google Cloud, and third-party SaaS platforms, particularly when regulations differ across regions and industries. Organizations also struggle with continuous monitoring of dynamic cloud workloads, shadow IT risks, and maintaining accurate audit trails for rapidly changing cloud resources. Additionally, the shortage of skilled cloud governance and compliance professionals, combined with integration challenges between legacy systems and cloud-native compliance tools, increases operational complexity and implementation costs. As a result, many organizations face delays in achieving unified cloud compliance management, which can hinder broader adoption of advanced compliance automation solutions.

Market Concentration & Characteristics

The cloud compliance market is moderately fragmented, with the presence of major cloud service providers, cybersecurity companies, governance-risk-compliance (GRC) vendors, and specialized compliance automation firms competing across the ecosystem. Large players such as Microsoft, IBM, Oracle, Palo Alto Networks, AWS, Google Cloud, and ServiceNow hold significant market share due to their integrated cloud security, governance, and compliance management capabilities. At the same time, the market includes numerous niche vendors offering specialized solutions for continuous compliance monitoring, cloud security posture management (CSPM), data governance, audit automation, and regulatory reporting, contributing to competitive fragmentation.

In terms of characteristics, the market demonstrates a high degree of innovation, driven by advancements in artificial intelligence (AI), automation, cloud-native security architectures, real-time compliance analytics, and policy-as-code frameworks. Vendors are increasingly integrating AI-driven risk assessment, automated remediation, and continuous monitoring features to help organizations manage dynamic regulatory requirements across hybrid and multi-cloud environments. The market is also witnessing moderate merger and acquisition (M&A) activity, as cybersecurity, cloud security, and governance software companies acquire niche compliance automation and risk management providers to strengthen cloud governance portfolios. Regulatory impact is extremely significant, with evolving data privacy and cybersecurity regulations such as GDPR, HIPAA, PCI DSS, SOC 2, NIS2, DORA, and industry-specific compliance mandates acting as major market growth drivers. Service substitutes remain limited because enterprises increasingly require automated and continuous cloud compliance management solutions rather than manual auditing processes. Additionally, the market exhibits high end-user concentration among BFSI, healthcare, government, IT & telecom, and retail sectors due to their stringent regulatory obligations, high cloud adoption rates, and elevated data security requirements.

Component Insights

The software segment accounted for the largest revenue share of 69.3% in the global cloud compliance market in 2025, driven by the growing need for automated and continuous compliance management across complex multi-cloud and hybrid environments. Enterprises are adopting cloud-native compliance software to replace manual approaches, as these platforms enable real-time visibility, policy enforcement, automated evidence collection, and alignment with evolving regulatory frameworks such as GDPR, ISO/IEC 27001, SOC 2, HIPAA, and PCI DSS. Besides, the rapid adoption of DevSecOps, compliance-as-code, and continuous control monitoring is further accelerating demand for software solutions that integrate seamlessly with IaaS, PaaS, and SaaS environments while reducing operational overhead and compliance risk. For instance, in April 2025, the Cloud Security Alliance (CSA) launched its Compliance Automation Revolution, aimed at transforming IT compliance and assurance through automated, cloud-native compliance capabilities that streamline regulatory mapping, continuous validation, and audit readiness across cloud ecosystems. Consequently, the software segment continues to dominate the market as organizations prioritize intelligent, policy-driven platforms that enable continuous compliance, regulatory confidence, and secure digital transformation.

The services segment is expected to register the fastest CAGR during the forecast period, driven by increasing enterprise reliance on consulting, integration, and managed compliance services to navigate complex and evolving regulatory landscapes. Organizations operating across multi-cloud and hybrid environments are seeking expert support for compliance strategy development, regulatory mapping, risk assessments, and continuous monitoring, particularly as in-house compliance expertise remains limited. Growing demand for managed compliance services, third-party audits, and ongoing advisory support is further fueling segment growth, enabling enterprises to maintain regulatory alignment while focusing on core business operations. Consequently, cloud compliance services are gaining traction as a critical enabler for scalable governance, reduced compliance risk, and sustained regulatory readiness across industries.

Model Insights

The Software-as-a-Service (SaaS) segment accounted for the largest market share in 2025, driven by enterprise adoption of subscription‑based, cloud‑native compliance solutions that offer rapid deployment and seamless updates across multi‑cloud environments. SaaS‑based compliance platforms enable real‑time monitoring, centralized policy enforcement, automated evidence collection, and continuous alignment with regulatory frameworks such as GDPR, HIPAA, ISO/IEC 27001, and PCI DSS, making them attractive for organizations seeking to streamline compliance operations and reduce overhead. These solutions also integrate easily with IaaS and PaaS offerings, supporting DevSecOps, compliance‑as‑code, and continuous control validation across distributed workloads. For instance, in November 2025, Cleura launched a new SaaS platform for AI regulation on Cleura Cloud, highlighting the expanding role of SaaS models in addressing emerging compliance needs,including regulatory guidance for AI systemsthrough flexible, cloud‑hosted services. Consequently, the SaaS segment continues to lead the cloud compliance market as enterprises prioritize agile, automated, and subscription‑based compliance solutions that support rapid innovation and regulatory confidence.

The Infrastructure‑as‑a‑Service (IaaS) model segment is experiencing strong growth, driven by the increasing need for deeper control over cloud infrastructure, secure configuration management, and customizable compliance controls across virtualized resources. As organizations modernize their IT environments and adopt multi‑cloud strategies, IaaS platforms are being leveraged to enforce consistent compliance policies, protect sensitive data, and support governance across compute, storage, and networking layers. Additionally, IaaS compliance solutions are valuable for regulatory reporting, risk assessment, and secure key management, enabling businesses to tailor compliance measures to their specific operational and industry requirements. For instance, in March 2025, ArubaCloud’s IaaS cloud hosting solution underscores the growing adoption of infrastructure‑level cloud services that combine scalability with robust compliance and governance features. Subsequently, the IaaS segment is gaining momentum as enterprises seek infrastructure‑centric compliance capabilities that enhance visibility, control, and accountability across evolving cloud deployments.

Enterprise Size Insights

The large enterprises segment accounted for the largest market share in the cloud compliance industry in 2025, driven by complex regulatory obligations, multi-cloud deployments, and the need for scalable, automated compliance solutions. Enterprises are seeking cloud platforms that provide centralized policy enforcement, real-time risk visibility, and seamless integration with global operations to efficiently manage tax, regulatory, and industry-specific requirements. For instance, in February 2024, Sovos introduced its Compliance Cloud to help global businesses navigate complex tax and regulatory environments with enhanced automation, scalability, and evidence-ready reporting, highlighting the growing adoption of enterprise-grade, integrated compliance platforms. Therefore, the large enterprises segment continues to dominate the market as organizations prioritize strategic and compliance-aligned cloud governance capabilities.

The SMEs segment is projected to witness the fastest CAGR during the forecast period, driven by the increasing adoption of cloud technologies and the need for cost-effective, scalable compliance solutions. Small and medium enterprises are seeking cloud-native platforms that offer automated policy enforcement, real-time monitoring, and simplified regulatory reporting without the need for extensive in-house compliance teams. As organizations in sectors such as retail, IT, healthcare, and professional services embrace digital transformation, the demand for subscription-based compliance software, managed services, and advisory support is growing rapidly. In conclusion, the SME segment is expected to expand faster than large enterprises, enabling smaller organizations to achieve regulatory alignment, reduce compliance risk, and operate securely across multi-cloud and hybrid environments.

Application Insights

The audit and compliance management segment accounted for the largest share of the global market in 2025, owing to the ongoing shift toward continuous compliance validation, real‑time reporting, and automated audit readiness across complex cloud environments. Companies are prioritizing solutions that streamline audit processes, enforce policy controls, and provide transparent evidence trails to meet stringent regulatory expectations and internal governance requirements. Cloud audit and compliance platforms that integrate with IaaS, PaaS, and SaaS environments enable centralized oversight, reduce manual effort, and improve accuracy for risk assessments and regulatory filings. For instance, in June 2025, Caseware launched its next‑generation cloud audit solution for Singapore audit professionals, underscoring the growing demand for advanced, cloud‑native audit and compliance tools that support efficiency, scalability, and regulatory confidence. Consequently, the audit and compliance management segment continues to dominate as enterprises seek to strengthen governance frameworks and ensure continuous alignment with evolving compliance standards.

The threat detection and remediation segment is expected to grow at the significant CAGR during the forecast period, driven by the increasing sophistication of cyber threats targeting cloud environments and the need for automated, real‑time response capabilities that minimize risk exposure. Organizations are prioritizing solutions that combine advanced analytics, behavioral monitoring, and integrated remediation workflows to detect, investigate, and contain threats across distributed workloads and hybrid infrastructures. This growth is further supported by the rising adoption of AI/ML‑powered security technologies that enhance threat visibility and reduce incident response times. For instance, in October 2025, Illumio launched an AI agent for fast, radically simplified threat detection and containment, highlighting the accelerating demand for intelligent, automated threat detection and remediation solutions in cloud ecosystems. Therefore, the threat detection and remediation segment is poised to expand rapidly as enterprises seek proactive, resilient defenses that complement broader cloud compliance and governance strategies.

End Use Insights

The BFSI segment accounted for the largest market share in 2025, owing to stringent regulatory requirements, high volumes of sensitive financial data, and the critical need for real‑time risk visibility and compliance assurance across cloud environments. Financial institutions are increasingly adopting advanced cloud compliance platforms that streamline audit reporting, enforce policy controls, and provide continuous monitoring to meet mandates such as PCI DSS, Basel III, and anti‑money‑laundering regulations while supporting digital transformation initiatives. For instance, in September 2024, Oracle introduced a new cloud service that helps banks quickly identify financial crime risk, underscoring the rising demand for cloud solutions that integrate compliance, risk analytics, and real‑time detection capabilities in the BFSI sector. Consequently, the BFSI segment continues to lead the cloud compliance market as banks and financial services firms invest in scalable, secure, and regulatory‑aligned cloud governance solutions.

The healthcare segment is expected to register the fastest growth during the forecast period in the global cloud compliance market, driven by the increasing digitization of patient records, telemedicine adoption, and stringent regulatory requirements such as HIPAA and GDPR. Healthcare organizations are prioritizing cloud compliance solutions that provide real-time monitoring, automated policy enforcement, and secure data handling across multi-cloud and hybrid environments, while ensuring patient privacy and regulatory adherence. The growing use of IoT-enabled medical devices, remote patient monitoring, and cloud-based health analytics is further accelerating demand for automated compliance platforms that reduce risk and enhance operational efficiency. Consequently, the healthcare segment is poised to expand rapidly as providers invest in scalable, secure, and policy-driven cloud compliance solutions to support digital transformation and maintain regulatory confidence.

Regional Insights

The cloud compliance industry in North America accounted for the largest market share of 36.6% in 2025, driven by high cloud adoption, stringent regulatory requirements, and the presence of major cloud service providers and compliance solution vendors in the region. Organizations across industries such as BFSI, healthcare, IT & telecom, and government are increasingly deploying cloud compliance platforms to ensure real-time monitoring, policy enforcement, and regulatory alignment across multi-cloud and hybrid environments. The region’s strong focus on data privacy, cybersecurity, and digital transformation initiatives is further fueling the adoption of automated, scalable, and cloud-native compliance solutions. Consequently, North America continues to dominate the market as enterprises seek robust, integrated, and policy-driven platforms to manage regulatory obligations and support secure digital operations.

U.S. Cloud Compliance Market Trends

The U.S. cloud compliance industry is experiencing strong growth, driven by increasing cloud adoption across enterprises, stringent regulatory frameworks, and the rising complexity of managing compliance in multi-cloud and hybrid IT environments. Organizations are increasingly investing in automated, cloud-native compliance solutions that provide real-time monitoring, policy enforcement, and audit-ready reporting to meet regulations such as GDPR, HIPAA, PCI DSS, and ISO/IEC 27001. The growing emphasis on DevSecOps, continuous compliance, and integration of compliance controls into cloud workflows is further accelerating market expansion. Consequently, the U.S. market is emerging as a key driver of global cloud compliance demand, as enterprises prioritize scalable, intelligent, and policy-aligned platforms to ensure regulatory adherence and secure digital transformation.

Europe Cloud Compliance MarketTrends

The cloud compliance industry in Europe is anticipated to register significant growth from 2026 to 2033, fueled by stringent data protection and privacy regulations such as the General Data Protection Regulation (GDPR) and an emphasis on data sovereignty that compels organizations to adopt advanced compliance solutions. Europe’s regulatory landscape has made it one of the most mature markets for cloud compliance platforms, with enterprises across BFSI, healthcare, government, and retail increasingly investing in automated tools for real‑time monitoring, policy enforcement, audit readiness, and risk mitigation to ensure adherence with evolving mandates and avoid substantial penalties. European countries such as Germany, the United Kingdom, and France are leading adoption, supported by proactive national data protection laws and government initiatives that reinforce compliance priorities in cloud environments. As a result, Europe holds a significant share of the global market and is expected to sustain robust growth through the forecast period, reflecting both regulatory rigor and digital transformation trends.

The UK cloud compliance industry is experiencing strong growth as businesses seek to meet stringent regulatory and data sovereignty requirements while accelerating cloud adoption across industries. Driven by evolving UK GDPR standards, increasing emphasis on data residency, and the shift toward hybrid and multi‑cloud strategies, organizations are investing in cloud compliance platforms that ensure continuous monitoring, audit readiness, and secure data governance across distributed environments. UK enterprises, particularly in finance, healthcare, and public services,are prioritizing local data handling and compliance tools to navigate both national and cross‑border regulatory frameworks, while also responding to broader concerns around data transparency and vendor lock‑in.

The cloud compliance industry in Germany is witnessing robust growth as organizations across industries prioritize data protection, regulatory adherence, and secure cloud deployments in response to stringent regulations such as the EU General Data Protection Regulation (GDPR) and national data sovereignty requirements. German enterprises are increasingly adopting cloud compliance solutions that enable automated governance, robust data encryption, access control, and continuous monitoring to meet complex compliance demands while supporting digital transformation and hybrid cloud strategies. Businesses are also favoring private and hybrid cloud environments to enhance operational control and compliance with local regulations, reflecting a broader trend toward managing compliance risk in distributed IT landscapes.

Asia Pacific Cloud Compliance Market Trends

The cloud compliance industry in the Asia Pacific is expected to register the fastest CAGR from 2026 to 2033, driven by rapid digital transformation, accelerated cloud adoption, and evolving regulatory frameworks across key countries such as China, India, Japan, and Australia. Enterprises in the region are increasingly investing in cloud-native compliance platforms to ensure real-time monitoring, policy enforcement, audit readiness, and risk management across multi-cloud and hybrid environments. The growing adoption of SaaS applications, IoT devices, and remote work solutions is further driving demand for automated, scalable, and integrated compliance solutions that reduce operational overhead and improve regulatory alignment. Thus, Asia Pacific is emerging as a high-growth region, with organizations prioritizing cloud compliance solutions to support secure digital transformation, maintain data sovereignty, and meet increasingly complex regional and industry-specific regulations.

The Japan cloud compliance industry is experiencing strong growth as businesses increasingly adopt cloud technologies and face stringent regulatory requirements such as the Act on the Protection of Personal Information (APPI) and other national data protection mandates, compelling organizations to implement robust compliance and governance solutions across cloud environments. Japan’s regulatory landscape and emphasis on data sovereignty are driving demand for automated compliance tools, continuous monitoring, and risk management capabilities, particularly in sectors such as finance, healthcare, and manufacturing, where compliance and data protection are critical. For instance, in 2025, Fujitsu and PwC Japan partnered to enhance the compliance and reliability of sovereign cloud solutions under Japan’s Economic Security Promotion Act, providing practical frameworks for critical infrastructure operators to implement mandatory risk management and compliance measures while promoting cloud adoption. Consequently, the Japanese market is poised for continued expansion as enterprises invest in scalable, policy‑aligned platforms that support secure digital transformation and regulatory adherence in an evolving regulatory environment.

The cloud compliance industry in China is experiencing rapid expansion as businesses increasingly adopt cloud technologies and face stringent domestic data protection and cybersecurity requirements under laws such as the Cybersecurity Law, the Data Security Law, and the Personal Information Protection Law (PIPL). These regulatory frameworks are compelling organizations to implement automated cloud compliance solutions that ensure secure data handling, real‑time policy enforcement, and robust governance across multi‑cloud and hybrid environments. Domestic cloud providers such as Alibaba Cloud, Tencent Cloud, and Huawei Cloud are leading the market by offering compliance tools and platforms tailored to China’s regulatory landscape, with Alibaba Cloud alone holding a substantial share of the tools market.

The India cloud compliance industry is rapidly expanding as businesses accelerate cloud adoption and respond to evolving regulatory and data protection requirements, including data localization mandates and emerging privacy laws. Regulatory pressures such as data residency norms from the Reserve Bank of India and emerging data protection frameworks are further driving adoption as enterprises seek cloud compliance platforms that support secure data management and regulatory alignment. Consequently, India’s cloud compliance landscape is poised for sustained growth, with both domestic and global vendors expanding offerings to meet increasing demand for automated, scalable, and regulation‑aligned cloud governance solutions.

Key Cloud Compliance Company Insights

Key players operating in the cloud compliance industry are Amazon Web Services (AWS), Cisco Systems, Google (Google Cloud), IBM, and Microsoft, among others. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives:

-

In December 2025, Oracle and AWS expanded collaboration with Oracle Database, enabling enterprises to run Oracle workloads with enhanced security and compliance across more AWS regions worldwide.

-

In May 2025, Salesforce announced the acquisition of Informatica (approximately USD 8B) to enhance its data governance and compliance capabilities within its cloud ecosystem, strengthening compliance data management.

-

In March 2025, Google Cloud signed a definitive agreement to acquire Wiz for USD 32 billion to enhance multicloud security, creating a unified platform that scans cloud resources, code, and applications across AWS, Azure, and other clouds for better compliance in hybrid environments.

Key Cloud Compliance Companies:

The following key companies have been profiled for this study on the cloud compliance market.

- Amazon Web Services (AWS)

- Cisco Systems

- Google (Google Cloud)

- IBM

- Microsoft

- Nutanix

- OneTrust

- Oracle

- Palantir

- Qualys

- Rackspace Technology

- Salesforce

- ServiceNow

- Tenable

- Zscaler

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Amazon Web Services (AWS); Google Cloud; Microsoft; IBM; Cisco Systems; Oracle; Salesforce; ServiceNow; OneTrust; Rackspace Technology

- Embedding automated compliance auditing tools directly into the cloud infrastructure, making compliance an "always-on" baseline feature of cloud consumption.

- Standardizing workflows across vast enterprise platforms to automatically translate single security controls to dozens of global legal regimes simultaneously (GDPR, DORA, NIS2).

- Holding direct ownership over the underlying physical data centers or global enterprise software layers, establishing an inescapable first line of compliance monitoring.

- Possessing the immense capital scale required to warehouse, index, and query petabytes of historical compliance log data for years without introducing latency or heavy cloud cost overhead.

- Native cloud platform tools are frequently optimized to enforce compliance within their own ecosystem, struggling to offer deep, unbiased compliance oversight in complex multi-cloud environments.

- Enterprise-wide GRC platforms can be remarkably heavy, occasionally requiring extensive third-party consulting retainers to fully integrate and adopt.

Emerging Players: Palantir; Nutanix; Qualys; Tenable; Zscaler

- Unifying standard IT compliance tracking with active threat-exposure management to shift compliance from a "paper exercise" to live technical risk mitigation.

- Delivering lightweight, unified management layers that allow enterprises to maintain identical compliance and security profiles across private servers and public clouds seamlessly.

- Operating as an objective, unbiased platform that scans across AWS, Azure, and Google Cloud equally, generating a singular, untampered source of compliance truth.

- Going beyond traditional static point-in-time compliance checks by actively terminating non-compliant cloud configurations or over-privileged user access automatically.

- Point-product specialist tools often focus beautifully on cloud infrastructure tracking but lack the broader non-technical compliance features.

- Adopting dedicated point-product compliance tools forces security operations teams to actively balance and manage an additional vendor relationship alongside their main hyper-scaler contracts.

Cloud Compliance Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 41.0 billion

Estimated Market size in 2026

USD 46.6 billion

Projected Market size by 2033

USD 127.6 billion

Growth rate

CAGR of 15.5% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report Coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, model, enterprise size, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East and Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Amazon Web Services (AWS); Cisco Systems; Google (Google Cloud); IBM; Microsoft; Nutanix; OneTrust; Oracle; Palantir; Qualys; Rackspace Technology; Salesforce; ServiceNow; Tenable; Zscaler

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cloud Compliance Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global cloud compliance market report based on component, model, enterprise size, application, end use, and region.

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Software

-

Services

-

-

Model Outlook (Revenue, USD Billion, 2021 - 2033)

-

Infrastructure-as-a-Service (IaaS)

-

Platform-as-a-Service (PaaS)

-

Software-as-a-Service (SaaS)

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

SMEs

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Audit and Compliance Management

-

Threat Detection and Remediation

-

Activity Monitoring and Analytics

-

Visibility and Risk Assessment

-

Others

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

IT & Telecom

-

Retail & Consumer Goods

-

Manufacturing

-

Energy & Utilities

-

Healthcare

-

Government & Public Sector

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Multi-cloud compliance readiness assessment for a BFSI enterprise.

- Evaluation of compliance management challenges across AWS, Azure, and Google Cloud environments.

- Analysis of regulatory alignment with GDPR, PCI DSS, DORA, and SOC 2 frameworks.

- Identified cloud governance gaps and compliance risks.

- Supported development of a unified multi-cloud compliance strategy.

Healthcare cloud compliance and data protection assessment.

- Evaluation of HIPAA compliance requirements and cloud security challenges across healthcare organizations.

- Analysis of patient data governance and third-party cloud risk management practices.

- Identified sector-specific compliance opportunities.

- Supported tailored cloud governance and healthcare security strategy.

Cloud audit and continuous compliance monitoring opportunity assessment for an IT services provider.

- Analysis of enterprise demand for automated audit readiness and continuous compliance tracking solutions.

- Evaluation of managed cloud compliance service adoption trends.

- Highlighted opportunities in managed compliance services.

- Supported service portfolio expansion and recurring revenue strategy.

Frequently Asked Questions About This Report

North America dominated with 36.6% market share in 2025.

Asia Pacific is the fastest-growing region.

Software segment led with 69.3% share in 2025, while services segment is expected to grow fastest.

SaaS segment led the market in 2025, while IaaS segment is growing significantly.

The global cloud compliance market is expected to grow at a compound annual growth rate of 15.5% from 2026 to 2033 to reach USD 127.6 million by 2033.

The BFSI segment dominated the cloud compliance market in 2025 owing to stringent regulatory requirements, high volumes of sensitive financial data, and the critical need for real‑time risk visibility and compliance assurance across cloud environments.

Some key players operating in the market include Amazon Web Services (AWS), Cisco Systems, Google (Google Cloud), IBM, Microsoft, Nutanix, OneTrust, Oracle, Palantir, Qualys, Rackspace Technology, Salesforce, ServiceNow, Tenable, Zscaler, and Others.

Factors such as the accelerating cloud adoption, rising regulatory scrutiny, and the increasing complexity of managing compliance across multi-cloud and hybrid IT environments plays a key role in accelerating the cloud compliance market.

The global cloud compliance market size was estimated at USD 41.0 billion in 2025 and is expected to reach USD 46.6 billion in 2026.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.