- Home

- »

- Network Security

- »

-

Cloud Security Market Size And Share Report, 2026-2033GVR Report cover

![Cloud Security Market (2026 - 2033)Report]()

Cloud Security Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Solution, Services), By Deployment (Private, Hybrid, Public), By Enterprise Size (Large Enterprises, SMEs), By End Use (BFSI, Healthcare, IT & Telecom), By Region, And Segment Forecasts

Market Size, 2025

$39.1BMarket Estimate, 2026

$43.8BMarket Forecast, 2033

$97.9BCAGR, 2026–2033

12.2%Cloud Security Market Summary

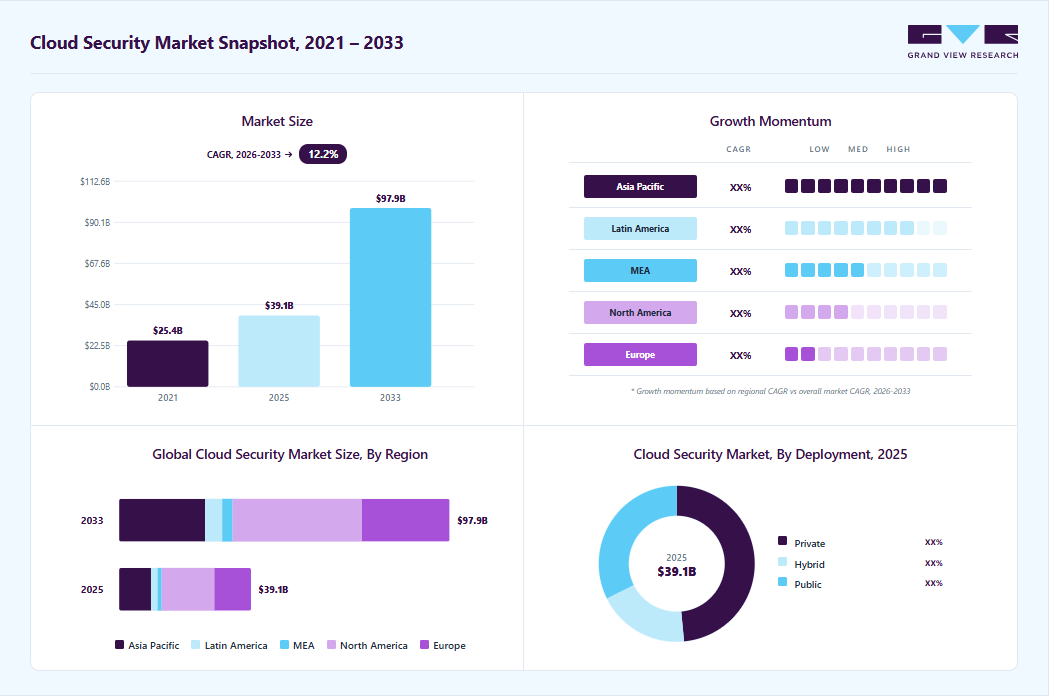

The global cloud security market size was valued at USD 39.1 billion in 2025 and is projected to grow from USD 43.8 billion in 2026 to USD 97.9 billion by 2033, at a CAGR of 12.2% from 2026 to 2033. The market in North America dominated with a revenue share of 39.9% in 2025. Businesses across industries are investing in advanced security solutions to protect against cyber threats, data breaches, and unauthorized access, strengthening the overall cybersecurity market.

Key Market Trends & Insights

- By component: Solution segment held the largest market share of 67.2% in 2025.

- By deployment: Private segment held the largest market share in 2025.

- By enterprise size: Large enterprises segment held the largest market share in 2025.

- By end use: IT & telecom segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (39.9% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 39.1 Billion

- Estimated market size in 2026: USD 43.8 Billion

- Projected market size by 2033: USD 97.9 Billion

- CAGR (2026-2033): 12.2%

The market includes services such as identity management, network security, encryption, threat monitoring, and compliance management for public, private, and hybrid clouds. As organizations migrate critical workloads and data to public, private, and hybrid cloud environments, the need to secure these assets has become paramount in the evolving cloud infrastructure security market. This transition has elevated cloud security from a secondary IT concern to a central strategic imperative. Moreover, the proliferation of remote work models and hybrid workplace environments has expanded the threat surface, necessitating more sophisticated security frameworks and controls tailored to cloud infrastructure.")

The rising frequency and sophistication of cyber threats targeting cloud-based assets also contribute to the growth of the cloud security industry. High-profile data breaches and ransomware attacks have underscored the vulnerabilities inherent in cloud platforms, prompting both regulatory scrutiny and heightened enterprise investments in cloud-native security solutions. In response, vendors are innovating rapidly, developing tools that incorporate advanced technologies such as artificial intelligence (AI), machine learning (ML), and automation to deliver real-time threat detection, automated incident response, and behavioral analytics. These innovations are enhancing the effectiveness and appeal of modern cloud security solutions.

According to the Thales Cloud Security Study 2024, stated that cloud data encryption remains low, with fewer than 10% of enterprises encrypting 80% or more of their cloud data, despite 44% reporting cloud security incidents and 14% experiencing breaches in the past year. This growing concern over cloud vulnerabilities is expected to accelerate demand for advanced cloud security solutions across industries. Increasing investments in AI-driven threat detection, encryption, and automated security platforms will further support market expansion and encourage continuous innovation among cloud security vendors.

Moreover, increasing regulatory mandates, such as the General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA), as well as industry-specific compliance frameworks, are compelling organizations to implement rigorous cloud security measures in the expanding cloud application security market. These compliance requirements are particularly critical in sectors such as healthcare, banking, and government, where data sensitivity is high. Furthermore, the growth of multi-cloud and hybrid cloud strategies is adding complexity to cloud environments, thereby fueling demand for unified, policy-driven security architectures that ensure consistency across platforms.

Market Dynamics

Organizations are adopting Zero Trust security models as traditional perimeter-based security becomes less effective in cloud environments in the cybersecurity market. With remote work, SaaS applications, and cloud-based workloads expanding rapidly, enterprises require continuous user authentication, device verification, and restricted access controls to protect sensitive data. This is driving strong demand in the cloud security software market for cloud security solutions such as cloud identity and access management (IAM), multi-factor authentication (MFA), cloud workload protection, and secure access service edge (SASE) platforms. Large enterprises and the BFSI, healthcare, and government sectors are particularly investing in Zero Trust cloud security frameworks to reduce insider threats and unauthorized access risks.

In addition, the increasing adoption of remote and hybrid work models is further accelerating the implementation of Zero Trust security frameworks in cloud environments. Employees are accessing enterprise applications and data from multiple devices, locations, and networks, which increases the risk of credential theft, unauthorized access, and lateral movement attacks. As a result, organizations are investing in advanced cloud security technologies, such as identity governance, privileged access management (PAM), endpoint verification, and behavioral analytics, to continuously monitor user activity and secure cloud resources.

The growing use of multi-cloud platforms, Kubernetes, containers, and cloud-native applications is creating significant security management challenges for organizations in the cloud infrastructure security market. Enterprises often use services from multiple cloud providers, such as Amazon Web Services, Microsoft Azure, and Google Cloud, which increases the complexity of maintaining consistent security policies, visibility, and compliance controls across environments. Misconfigured APIs, insecure containers, and a lack of centralized monitoring within the cloud network security market can expose sensitive workloads to cyber threats and data breaches. Many organizations struggle to integrate security tools across diverse cloud ecosystems, which increases operational costs and slows cloud security adoption, particularly among SMEs and traditional enterprises.

In addition, the rapid deployment of DevOps and continuous integration/continuous deployment (CI/CD) pipelines is further increasing security complexity in multi-cloud and containerized environments. Development teams frequently deploy applications and micro-services at high speed, making it difficult for organizations to continuously identify vulnerabilities, monitor runtime threats, and enforce security policies across dynamic cloud infrastructures. The shortage of skilled cloud security professionals and limited visibility into east-west traffic within container environments also increases the risk of configuration errors and delayed threat response. These operational and technical challenges continue to restrain the effective implementation of advanced cloud security solutions across enterprises.

The rapid adoption of Cloud-Native Application Protection Platforms (CNAPP), AI-driven threat analytics, and automated security orchestration is creating major growth opportunities in the cloud application security market. Enterprises are investing in integrated platforms that combine CSPM, CWPP, CIEM, and runtime threat detection into a single security framework to protect cloud-native applications and DevSecOps environments. Industries such as BFSI, healthcare, and e-commerce are adopting these solutions to secure APIs, workloads, and sensitive customer data in the cloud data security market against advanced ransomware and identity-based attacks. Leading companies, including Palo Alto Networks, CrowdStrike, and Fortinet, are expanding AI-powered cloud security offerings, creating strong future growth opportunities for the market.

Furthermore, the increasing shift toward cloud-native development and serverless computing is accelerating the demand for intelligent CNAPP and AI-based cloud threat detection solutions. Organizations are deploying applications across dynamic and highly distributed cloud environments, where traditional security tools often lack real-time visibility and automated response capabilities. AI-powered cloud security platforms help enterprises detect abnormal user behavior, prioritize critical vulnerabilities, and automate incident remediation with minimal manual intervention. The growing need for faster threat detection, reduced security operation workloads, and continuous compliance management is encouraging enterprises to adopt advanced AI-driven cloud security platforms, thereby creating long-term market growth opportunities.

Market Concentration & Characteristics

The cloud security market is moderately fragmented, with the presence of several global cybersecurity companies, cloud service providers, and specialized security vendors competing across multiple solution categories such as identity and access management, workload protection, cloud-native application protection platforms (CNAPP), zero trust security, and secure access service edge (SASE). Large technology companies such as Cisco Systems, Inc., IBM Corporation, and Palo Alto Networks maintain strong market positions through broad portfolios, global customer reach, and integrated cloud ecosystems.

At the same time, emerging cybersecurity firms continue to gain traction by offering niche and AI-driven security capabilities, creating strong competitive intensity across the market. The industry is also seeing an increase in strategic partnerships and acquisitions as vendors aim to expand platform capabilities and strengthen their cloud-native security offerings.

The market demonstrates strong growth momentum driven by rising enterprise cloud adoption, the increasing frequency of cyberattacks, the expansion of hybrid and multi-cloud environments, and growing regulatory pressure on data protection and privacy compliance. Innovation levels remain very high as vendors continuously invest in AI-powered threat detection, automation, identity-centric security, and real-time monitoring solutions to address evolving attack surfaces.

Regulatory frameworks such as GDPR, CCPA, and regional data security laws are significantly influencing enterprise spending on cloud security solutions. Although integrated cloud-native security tools from hyperscale cloud providers may create moderate substitution pressure for standalone vendors, organizations continue to prefer advanced third-party security platforms for enhanced visibility, compliance management, and multi-cloud protection.

Overall, the market is characterized by rapid technological advancement, active merger and acquisition activity, and expanding enterprise demand across sectors such as BFSI, healthcare, government, retail, and manufacturing.

Component Insights

The solution segment led the market with the largest revenue share of 67.2% in 2025, driven by the increasing complexity and scale of cloud environments that demand robust, scalable, and integrated security tools. As enterprises migrate diverse workloads to cloud platforms, spanning Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS), the need for specialized security solutions such as cloud access security brokers (CASBs), cloud workload protection platforms (CWPPs), cloud security management (CSPM), and identity and access management (IAM) has intensified. These solutions help organizations gain visibility, enforce policies, manage configurations, and detect vulnerabilities across multi-cloud ecosystems, strengthening the cloud application security market.

The services segment is anticipated to grow at the fastest CAGR during the forecast period, driven by the increasing need for specialized expertise and ongoing support to secure complex, multi-layered cloud environments. As organizations adopt hybrid and multi-cloud strategies, they often encounter challenges in managing cloud configurations, maintaining consistent security policies, and ensuring regulatory compliance. This has led to a surge in demand for professional services, including risk assessment, compliance advisory, cloud security architecture design, and implementation support.

Deployment Insights

The private segment accounted for the largest market revenue share in 2025 and is projected to grow at the fastest CAGR during the forecast period. Technological advancements in virtualization and software-defined infrastructure are making private cloud deployments in the cloud infrastructure security market more scalable and cost-efficient, further supporting their adoption. Enterprises are increasingly leveraging hybrid or hosted private clouds operated by third-party vendors, combining the benefits of cloud computing with enterprise-grade security controls. This hybrid approach allows businesses to maintain strict security standards while enjoying the flexibility of modern IT infrastructure.

The hybrid segment is expected to grow at a significant CAGR over the forecast period, driven by the rising importance of business continuity and disaster recovery, which is influencing hybrid cloud adoption. Many organizations prefer hybrid models for their ability to seamlessly fail over from private to public clouds, or vice versa, in the event of a system outage or cyber incident. Security solutions designed for hybrid deployments now feature built-in redundancy, backup encryption, and cross-environment monitoring, making them essential components of resilient cloud strategies.

Enterprise Size Insights

The large enterprises segment accounted for the largest market revenue share in 2025. The acceleration of remote and hybrid workforces has introduced new security challenges for large organizations. With thousands of endpoints and users accessing enterprise resources from diverse locations and devices, the attack surface has expanded dramatically. In response, large enterprises are increasingly adopting Zero Trust architectures and cloud-native security technologies such as Secure Access Service Edge (SASE), Cloud Access Security Brokers (CASB), and Identity and Access Management (IAM) to secure user access and data across distributed environments. These investments are driving the need for a scalable, interoperable, and AI-driven cloud security platform.

The SME segment is expected to grow at the fastest CAGR during the forecast period, driven by the increasing availability of managed security services, which lower the barrier to entry for SMEs in the cloud data security market. Managed Security Service Providers (MSSPs) offer continuous monitoring, incident response, and threat intelligence as part of cost-efficient packages, allowing SMEs to outsource critical security functions. This is particularly attractive for small businesses that lack the personnel or budget to maintain an in-house security team. These service-based models not only improve security resilience but also allow SMEs to scale their protection in line with business growth.

End Use Insights

The IT & telecom segment accounted for the largest market revenue share in 2025. As core facilitators of cloud infrastructure, telecom operators and IT service providers are at the forefront of cloud adoption and innovation. They operate complex, high-volume networks that handle sensitive customer data, large-scale communications, and mission-critical applications, making them prime targets for cyberattacks. The need to ensure data privacy, service availability, and compliance is pushing this sector to invest heavily in robust cloud security solutions that provide comprehensive protection against threats such as distributed denial-of-service (DDoS) attacks, data breaches, and insider threats.

The healthcare segment is expected to grow at the fastest CAGR over the forecast period, due to the rapid digital transformation of healthcare services and the rising adoption of cloud-based electronic health records (EHR), telemedicine, and health information exchange (HIE) platforms. These technologies have enabled healthcare providers to enhance patient care, operational efficiency, and data accessibility. However, they also introduce significant cybersecurity risks due to the sensitive nature of personal health information (PHI) and the industry's status as a high-value target for cybercriminals.

Regional Insights

North America dominated the cloud security market with the largest revenue share of 39.9% in 2025, driven by its mature cloud adoption ecosystem and a high incidence of sophisticated cyberattacks. The region hosts many of the world’s largest cloud service providers and digital-first enterprises, creating significant demand for advanced security solutions. Enterprises across sectors are investing in next-generation security tools such as Zero Trust architectures, Extended Detection and Response (XDR), and cloud workload protection platforms (CWPP).

U.S. Cloud Security Market Trends

The cloud security industry in the U.S. accounted for the largest market revenue share in North America in 2025, driven by the growing digital transformation across federal, state, and enterprise-level operations. Critical infrastructure sectors, including healthcare, finance, and energy, are moving core workloads to the cloud, which elevates the need for stringent cloud security measures. Another key driver is the legal landscape, with mandates such as HIPAA, SOX, and FedRAMP requiring cloud providers and users to adopt auditable, compliant security practices.

Europe Cloud Security Market Trends

The cloud security industry in Europe is anticipated to register at a considerable CAGR from 2026 to 2033, driven by strong regulatory pressure and a rising demand for data sovereignty. The General Data Protection Regulation (GDPR) has had a profound impact on how data is stored, processed, and secured in the cloud, compelling both domestic and international firms to adopt cloud security solutions that ensure compliance. In addition, the growing adoption of hybrid and multi-cloud environments across enterprises is increasing the need for centralized security management and threat monitoring solutions. European organizations are also investing heavily in identity and access management, encryption, and zero-trust security frameworks to strengthen cloud protection.

The UK cloud security market is expected to witness at a significant CAGR over the forecast period. The shift toward digital government services and NHS modernization programs is significantly boosting the adoption of cloud security tools. British enterprises are particularly focused on securing customer trust, and this has driven the adoption of advanced threat detection, encryption, and identity management tools. In addition, increasing adoption of remote and hybrid work models across financial services and public sector organizations is accelerating demand for secure cloud access solutions. The growing emphasis on compliance with the UK Data Protection Act and cybersecurity resilience requirements is also encouraging enterprises to strengthen their cloud security infrastructure.

Asia Pacific Cloud Security Market Trends

The cloud security industry in the Asia Pacific is expected to grow at the fastest CAGR from 2026 to 2033, driven by increased cloud adoption among SMEs, government digitization efforts, and rising cybersecurity awareness. Markets such as Australia, South Korea, and India are investing heavily in cyber resilience as digital infrastructure expands. The rapid growth of e-commerce, digital banking, and 5G deployment across the region is further increasing the need for advanced cloud security solutions to protect sensitive customer and enterprise data. In addition, rising investments in local cloud data centers and stricter data protection regulations are encouraging organizations to adopt stronger cloud security frameworks and compliance solutions.

The China cloud security market is expected to grow at a significant CAGR over the forecast period, driven by strong government mandates for cybersecurity and cloud computing. The introduction of the Cybersecurity Law and Data Security Law imposes stringent requirements on both domestic and foreign cloud providers operating in China, prompting significant investments in localized cloud security solutions. In addition, the rapid expansion of domestic cloud platforms and smart city initiatives is increasing demand for advanced threat monitoring, data encryption, and network security solutions. The growing adoption of AI, industrial IoT, and digital payment platforms across the manufacturing and financial sectors is also driving the need for stronger cloud security infrastructure in the country.

Key Cloud Security Company Insights

Key players operating in the global cloud security industry are Extreme Networks, Inc., F5, Inc., Forcepoint, Fortinet, Inc., Check Point Software Technologies Ltd., and others. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals.

Key Cloud Security Companies:

The following key companies have been profiled for this study on the cloud security market.

- Amazon Web Services, Inc.

- Broadcom, Inc.

- Check Point Software Technologies Ltd.

- Cisco Systems, Inc.

- Extreme Networks, Inc.

- Fortinet, Inc.

- F5, Inc.

- Forcepoint

- IBM Corporation

- Imperva

- Palo Alto Networks, Inc.

- Proofpoint, Inc.

- Sophos Ltd.

- Trellix

- Zscaler, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: Palo Alto Networks; Cisco Systems; Fortinet; Check Point Software Technologies; IBM Corporation

- Focus on platform-based integrated cloud security solutions combining CNAPP, SASE, zero trust, and AI-driven threat detection.

- Expand market presence through acquisitions, strategic partnerships, and continuous investment in hybrid and multi-cloud security capabilities.

- Strong global enterprise customer base with established brand recognition and extensive partner ecosystems.

- Broad product portfolios with advanced threat intelligence, compliance management, and large-scale deployment capabilities.

- Higher solution and implementation costs compared to smaller or specialized vendors.

- Complex product architectures may require skilled cybersecurity professionals and longer deployment timelines.

Emerging Players: Zscaler; Proofpoint; Trellix; Sophos; Forcepoint

- Focus on cloud-native, AI-driven, and zero-trust security innovations to address modern cloud security challenges.

- Expand rapidly in high-growth segments such as SSE, MDR, XDR, cloud DLP, and SaaS security.

- Agile product innovation with simplified and scalable cloud-delivered security platforms.

- Strong specialization in specific security domains such as email security, SSE, insider threat protection, or managed detection and response.

- Limited global enterprise penetration and smaller partner ecosystems compared to mature players.

- Narrower product portfolios and lower brand recognition in highly competitive cloud security markets.

Recent Developments

-

In March 2026, Amazon Web Services, Inc. expanded its partnership with Google Cloud to strengthen cloud security against rising AI-driven cyber threats. The collaboration combines Google Security Operations, Wiz capabilities, and Amazon Web Services, Inc.’s cybersecurity services to improve threat detection, secure multi-cloud environments, accelerate SIEM migration, and support organizations in building stronger and more resilient cloud security infrastructure.

-

In January 2026, PwC collaborated with Google Cloud with an investment of USD 400 million, focusing on AI-powered security operations. This collaboration aims to strengthen cloud security by improving threat detection, automating security workflows, enhancing cyber resilience, and helping organizations manage complex hybrid and multi-cloud security environments more effectively.

-

In December 2025, Amazon Web Services introduced AI-enhanced cloud security innovations, including AI security agents, automated threat detection, and advanced identity management solutions. These developments strengthen protection across cloud environments, improve incident response capabilities, and support growing enterprise demand for secure AI adoption and resilient cloud security infrastructure.

Cloud Security Market Report Scope

Report Attribute

Details

Market size in 2025

USD 39.1 billion

Estimated market size in 2026

USD 43.8 billion

Projected market size by 2033

USD 97.9 billion

Growth rate

CAGR of 12.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component, deployment, enterprise size, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Saudi Arabia; South Africa

Key companies profiled

Amazon Web Services, Inc.; Broadcom, Inc.; Check Point Software Technologies Ltd.; Cisco Systems, Inc.; Extreme Networks, Inc.; Fortinet, Inc.; F5, Inc.; Forcepoint; IBM Corporation; Imperva; Palo Alto Networks, Inc.; Proofpoint, Inc.; Sophos Ltd.; Trellix; Zscaler, Inc.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cloud Security Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global cloud security market report based on component, deployment, enterprise size, end use, and region.

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Solution

-

CASB

-

CDR

-

CSPM

-

CIEM

-

CWPP

-

Others

-

-

Services

-

Professional Services

-

Managed Services

-

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Private

-

Hybrid

-

Public

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

SMEs

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Healthcare

-

Retail & E-commerce

-

IT & Telecom

-

Government

-

Energy & Utilities

-

Manufacturing

-

Aerospace & Defense

-

Transportation & Logistics

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Client requested additional analysis on multi-cloud security risks and compliance trends across banking organizations.

Added insights on cloud misconfiguration and identity access management risks

Included BFSI-focused compliance analysis and regulatory trends

Provided competitor benchmarking and cloud security adoption analysis

Helped the client understand major cloud security risk areas

Supported strategic planning for cloud security investments

Assisted in evaluating suitable cloud security vendors and solutions

Client requested a deeper analysis of AI-driven cloud threat detection solutions and ransomware protection trends in healthcare.

Added healthcare-specific cloud threat and ransomware analysis

Included adoption trends of AI-based threat detection solutions

Provided profiles and recent developments of key cloud security vendors

Supported evaluation of emerging cloud security technologies

Helped strengthen cybersecurity strategy discussions internally

Assisted in future budget planning for cloud security initiatives

Client requested inclusion of additional emerging and regional cloud security vendors in the competitive landscape section.

Added profiles of emerging and regional cloud security companies

Included analysis of product portfolios and service offerings

Provided benchmarking based on technology focus and regional presence

Added recent partnerships, acquisitions, and product launch updates

Offered broader visibility into the competitive environment

Helped evaluate potential competitors and partnership opportunities

Supported competitor monitoring and positioning strategies

Improved understanding of market differentiation among vendors

Frequently Asked Questions About This Report

The global cloud security market size was valued at USD 39.1 billion in 2025 and is estimated at USD 43.8 billion for 2026.

The global cloud security market is expected to grow at a CAGR of 12.2% from 2026 to 2033, reaching USD 97.9 billion by 2033.

North America dominated with a 39.9% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include Amazon Web Services, Inc.; Broadcom, Inc.; Check Point Software Technologies Ltd.; Cisco Systems, Inc.; Extreme Networks, Inc.; Fortinet, Inc.; F5, Inc.; Forcepoint; IBM Corporation; Imperva; Palo Alto Networks, Inc.; Proofpoint, Inc.; Sophos Ltd.; Trellix; Zscaler, Inc.

The growth of the cloud security market is driven by the accelerating global adoption of cloud computing across enterprises of all sizes. As organizations increasingly migrate critical workloads and data to public, private, and hybrid cloud environments, the need to secure these assets has become paramount. This transition has elevated cloud security from a secondary IT concern to a central strategic imperative.

The solution segment led with a 67.2% revenue share in 2025, while the services segment is the fastest-growing.

The private segment held the largest revenue share in 2025, while the hybrid segment is the fastest-growing.

The large enterprises segment held the largest revenue share in 2025, while the SME segment is the fastest-growing.

The IT & telecom segment held the largest revenue share in 2025, while the healthcare segment is the fastest-growing.

About the Author(s)

Network Security Research Team

Technology · Network SecurityThis report was authored by the network security research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the network security segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.