- Home

- »

- Next Generation Technologies

- »

-

Core Banking Software Market Size Report, 2026-2033GVR Report cover

![Core Banking Software Market (2026 - 2033)Report]()

Core Banking Software Market (2026 - 2033)

Size, Share & Trends Analysis Report By Component (Solution, Service), By Deployment (Cloud, On-premise), By End-use (Banks, Financial Institutions), By Region, And Segment Forecasts

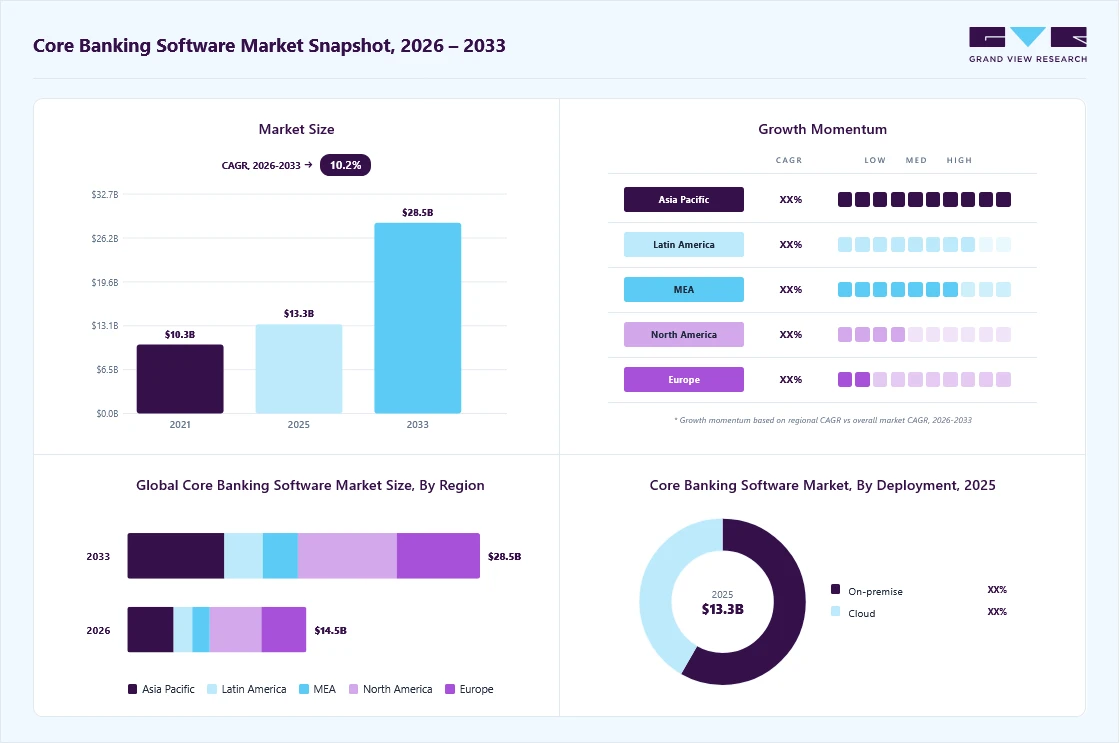

Market Size, 2025

$13.3BMarket Estimate, 2026

$14.5BMarket Forecast, 2033

$28.5BCAGR, 2026–2033

10.2%Core Banking Software Market Summary

The global core banking software market size was valued at USD 13.3 billion in 2025 and is projected to grow from USD 14.5 billion in 2026 to USD 28.5 billion by 2033, at a CAGR of 10.2% from 2026 to 2033. The North America held the largest share of 29.3% of the global market in 2025. The increasing inclination of banking industry participants to incorporate advanced technologies, improved capabilities, and innovation primarily drives the market growth.

Key Market Trends & Insights

- By component: Solution segment held the largest market share of 63.1% in 2025.

- By deployment: On-premise segment held the largest market share in 2025.

- By end-use: Banks segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (29.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest share in 2025

Market Size & Forecast

- Market size in 2025: USD 13.3 Billion

- Estimated market size in 2026: USD 14.5 Billion

- Projected market size by 2033: USD 28.5 Billion

- CAGR (2026-2033): 10.2%

The banking industry is undergoing rapid transformation, fueled by ongoing technological advancements. At the center of this evolution are modern core banking solutions that enable financial institutions to deliver seamless services, strengthen security frameworks, and enhance the overall customer experience. The financial services sector is increasingly shifting from traditional operating models to digitally driven processes across multiple business functions. This transition is supported by the growing availability of customized solutions and easier access to innovation-led software technologies. As a result, these factors are expected to create significant growth opportunities for the core banking solutions market.")

Smartphones and other electronic devices have become essential to modern business operations, particularly in the financial ecosystem. The rapid expansion of the e-commerce sector, along with the emergence of quick commerce in developing economies such as India, has significantly accelerated the adoption of digital technologies for financial transactions. In addition, the increasing penetration of web-based applications has further strengthened this trend. The widespread use of smartphones, coupled with the rise of technologies such as the Unified Payments Interface (UPI) and digital and mobile payment solutions, has heightened demand for more advanced, efficient banking software. As financial transactions become increasingly digital, banks and financial institutions are relying heavily on large volumes of customer data generated across multiple platforms. This growing dependence is driving the need for robust, scalable, and secure banking software solutions.

Beyond enabling customers to manage their accounts remotely via online and mobile banking channels, core banking software offers several additional advantages. These solutions integrate multiple bank branches into a centralized system, ensuring seamless connectivity and enabling efficient data access, search, and comparison across the network. Banks can leverage core banking platforms to analyze operational and customer data, thereby improving decision-making and enhancing internal processes. Furthermore, built-in capabilities such as transaction monitoring and screening support regulatory compliance by helping detect and prevent fraudulent activities, including money laundering.

The regulatory landscape is being shaped by stringent compliance requirements and evolving financial regulations across regions. Regulations related to data protection, cybersecurity, and anti-money laundering (AML) are being enforced to ensure the safety and integrity of financial systems. Compliance with standards such as know-your-customer (KYC) and data privacy regulations is being mandated, driving the adoption of advanced core banking solutions with built-in compliance functionalities. Moreover, regulatory support for digital banking and financial inclusion is being promoted in several countries, further encouraging market expansion.

High implementation and maintenance costs associated with core banking software are expected to hinder the market’s growth. In addition, challenges related to system integration, data migration, and compatibility with legacy infrastructure are being encountered during the transition to modern platforms. Concerns regarding data security, operational risks, and potential system downtime are also being highlighted as factors limiting adoption. Furthermore, a shortage of skilled professionals capable of managing advanced banking technologies is being identified as an ongoing challenge.

Component Insights

The solution segment dominated the market in 2025 and accounted for the largest share of 63.1%. This dominance is attributed to the growing number of banks and financial institutions seeking solutions that enhance operational capabilities and ensure hassle-free customer experiences. Multiple banks and financial organizations have adopted new solutions and advanced technologies to add novel capabilities to existing infrastructure and networks. Core banking solutions for loans encompass a comprehensive set of digital tools designed to streamline and optimize the loan management process within a financial institution. The loan solutions enhance operational efficiency, customer experience, and regulatory compliance throughout the lifecycle of loan products. Moreover, automation of the loan application and approval process, including data capture, credit scoring, and documentation verification, accelerates loan approval times and reduces manual errors. Solutions for the loans segment are expected to add lucrative opportunities.

The services segment is expected to grow at the fastest CAGR during the forecast period. Core banking software must be tailored to meet each financial institution's requirements and workflows. Professional service providers enable banks customize the software to meet their business needs. The primary growth factor for the professional service segment is the increasing need for support services at each level of software deployment, such as the pre-implementation of scope and consulting, project management, and integration.

Deployment Insights

The on-premise segment accounted for the largest market share in 2025. Under this model, full responsibility for system integration, maintenance, and security is assumed by the organization, allowing greater control over IT infrastructure and data management. Financial institutions operating on legacy platforms are often supported by specialized IT service providers to facilitate data recovery, ensure system continuity, and mitigate security risks while optimizing operational costs. The on-premise approach is preferred by institutions that require high levels of customization, data control, and regulatory compliance within their operational environment.

The cloud segment is expected to grow at the fastest CAGR during the forecast period. This is attributed to financial institutions and banks with existing on-premise infrastructure focusing on adopting cloud-based solutions to compete against more innovative digital opponents. Cloud technology automates workflows and operations, increasing efficiency, cost savings, and security. Cloud-based core banking solutions are flexible and easy to expand or reduce on demand, thereby meeting the IT requirements of the target organization.

End-use Insights

The banks segment dominated the market in 2025, driven by increasing investments in modern IT infrastructure and digital transformation initiatives. Automated core banking systems are being implemented to ensure accurate data entry and streamlined processing, thereby reducing the likelihood of errors. In addition, access to real-time data and advanced analytics is enabling banks to derive actionable insights into customer behavior, preferences, and financial trends. These capabilities are supporting more informed, data-driven decision-making and enhancing overall operational efficiency within banking institutions.

The financial institutions segment is expected to grow at a notable CAGR during the forecast period. Financial institutions widely adopt core banking software with real-time banking facilities to prevent theft and fraud. The rising adoption rate can also be attributed to the need to fill the gap between customer expectations and traditional banks' operations. These factors are expected to create growth opportunities for the financial institutions segment.

Regional Insights

North America core banking software market dominated the global industry and accounted for a share of 29.3% in 2025. This is attributed to the strong telecom & IT industry operating in the region, the presence of multiple banks focused on digital transformation, and the ease of availability driven by the accessibility to advanced technologies

U.S. Core Banking Software Market Trends

The U.S. core banking software market held a dominant position in the region in 2025. This is attributed to the robust IT sector actively operating in the country, numerous banks and financial institutions seeking to modernize core banking capabilities, and multiple collaborations among solution providers and banks or financial institutions.

Asia Pacific Core Banking Software Market Trends

The Asia Pacific core banking software market is expected to grow at the fastest CAGR during the forecast period. The increasing number of digital transactions primarily influences this market, consumers' growing use of digital technology, and the rising need for secure and scalable technologies associated with core banking. Entry of multiple global players from the banking and finance industry in the unexplored markets of this region is also adding to the growth.

Core banking software market in India is expected to grow at the fastest growth rate in the region during the forecast period. The country’s market growth is driven by digital transformation and government initiatives. Programs such as India Stack, which includes Aadhaar for biometric authentication and Unified Payments Interface (UPI), have accelerated the adoption of CBS solutions. In addition, regulatory requirements from the Reserve Bank of India (RBI), such as the Account Aggregator (AA) framework, push banks to modernize their IT infrastructure. Public Sector Banks (PSBs) are also undergoing digital transformation under reforms such as EASE (Enhanced Access and Service Excellence), further driving the demand for core banking software.

The China core banking software market held a significant market share in 2025. This is attributed to the growth experienced by the country's IT and telecom sector and growing partnerships among banks and IT solutions providers based in China. The rising adoption of online banking services and increasing use of digital platforms for financial services are expected to add growth opportunities to this market over the forecast period.

Europe Core Banking Software Market Trends

Core banking software market in Europe is expected to register a moderate CAGR from 2026 to 2033. This is attributed to the growing focus of multiple banks and financial organizations on digital transformation and modernizing existing core banking software technology to ensure improved processing performance and friction-free customer experiences. The availability of solutions delivered by expert IT companies worldwide adds lucrative growth opportunities to this market.

The Germany core banking software market held a substantial market share in 2025. This market is mainly driven by the growing inclination among the banking and financial services industry to upgrade existing core banking technologies to enhance performance and improve customer engagement. Increasing demand for centralized account management and changing customer requirements have stimulated the modernization trend in the industry.

Core banking software market in the UK is expected to grow at the significant growth rate during the forecast period. The core banking software market in the UK is experiencing strong growth, supported by rapid digital transformation across the financial services sector.

Key Core Banking Software Company Insights

Some of the key companies in the core banking software industry include Capgemini, Finastra, Infosys Limited, Temenos, Fiserv, Inc. and others. To address growing competition and increasing demand, the key market participants are adopting different strategies such as partnerships, new product launches, and more.

-

Temenos provides advanced banking technology solutions to nearly 950 core banking and approximately 600 digital banking clients worldwide. It offers an extensive platform and solutions portfolio to multiple industries, including retail banking, corporate banking, business banking, wealth management, payments, funds, and others.

-

Capgemini is an IT services and consulting company that acts as a technology and transformation partner for multiple organizations. It offers many solutions and technology assistance services. Its service portfolio is mainly associated with cloud, cybersecurity, data and artificial intelligence, enterprise management, intelligent industry, sustainability, and more.

Key Core Banking Software Companies:

The following key companies have been profiled for this study on the core banking software market.

- Capgemini

- Finastra

- FIS

- Fiserv, Inc.

- HCL Technologies Limited

- Infosys Limited

- Jack Henry & Associates, Inc.

- Oracle Corporation

- Temenos Group

- Unisys

Recent Developments

- In March 2026, 10x Banking, a cloud-native core banking platform provider, announced the launch of version 10.0 of its platform, marking its 100th release and a decade of continuous innovation. This milestone highlights the company’s ongoing efforts to enable financial institutions to achieve faster time-to-market, reduce operational costs, and support real-time transactions at near-unlimited scale.

-

In April 2025, AppTech Payments Corp. announced the launch of its core banking solution, fully integrated with the FINZEO platform, along with the onboarding of its first banking client. This development marks the company’s entry into the digital banking and retail financial services space, enabling it to deliver advanced technology solutions while also bringing an established customer base to financial institutions.

Core Banking Software Market Report Scope

Report Attribute

Details

Estimated market size in 2026

USD 14.46 billion

Projected market size by 2033

USD 28.48 billion

Growth rate

CAGR of 10.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, deployment, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; Japan; India; South Korea; Australia; Brazil; KSA; UAE; South Africa

Key companies profiled

Capgemini; Finastra; FIS; Fiserv, Inc.; HCL Technologies Limited; Infosys Limited; Jack Henry & Associates, Inc.; Oracle Corporation; Temenos Group; Unisys

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Core Banking Software Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global core banking software market report based on component, deployment, end-use, and region:

-

Component Outlook (Revenue, USD Million, 2021 - 2033)

-

Solution

-

Deposits

-

Loans

-

Enterprise Customer Solutions

-

Others

-

-

Service

-

Professional Service

-

Managed Service

-

-

-

Deployment Outlook (Revenue, USD Million, 2021 - 2033)

-

Cloud

-

On-premise

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Banks

-

Financial Institutions

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East and Africa (MEA)

-

KSA

-

UAE

-

South Africa

-

-

Frequently Asked Questions About This Report

Key factors that are driving the core banking software market growth include increasing customer demand for advanced banking technologies and growing demand for managing customer accounts from a single server.

The solution segment led with a 63.1% revenue share in 2025, while the services segment is the fastest-growing.

The on-premise segment held the largest revenue share in 2025, while the cloud segment is the fastest-growing.

The banks segment held the largest revenue share in 2025, while the financial institutions segment is is expected to grow at a notable CAGR.

Asia Pacific is the fastest-growing region over the forecast period.

The global core banking software market size was estimated at USD 13.3 billion in 2025 and is expected to reach USD 14.5 billion in 2026.

The global core banking software market is expected to grow at a compound annual growth rate of 10.2% from 2026 to 2033 to reach USD 28.5 billion by 2030.

North America dominated the core banking software market with a share of 29.3% in 2025. This is attributable to the large-scale adoption of advanced core banking software by prime banks in the North American region.

Some key players operating in the core banking software market include Capgemini, Finastra, FIS, Fiserv, Inc., HCL Technologies Limited, Infosys Limited, Jack Henry & Associates, Inc., Oracle Corporation, Temenos Group, and Unisys

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.