- Home

- »

- Advanced Interior Materials

- »

-

Cryocooler Market Size, Share & Growth Report, 2026-2033GVR Report cover

![Cryocooler Market (2026 - 2033)Report]()

Cryocooler Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Gifford-Mcmahon, Pulse-Tube, Stirling, Brayton, Joule Thomson) By Heat Exchanger Type (Regenerative, Recuperative), By Application (Military & Defense, Healthcare), By Region And Segment Forecasts

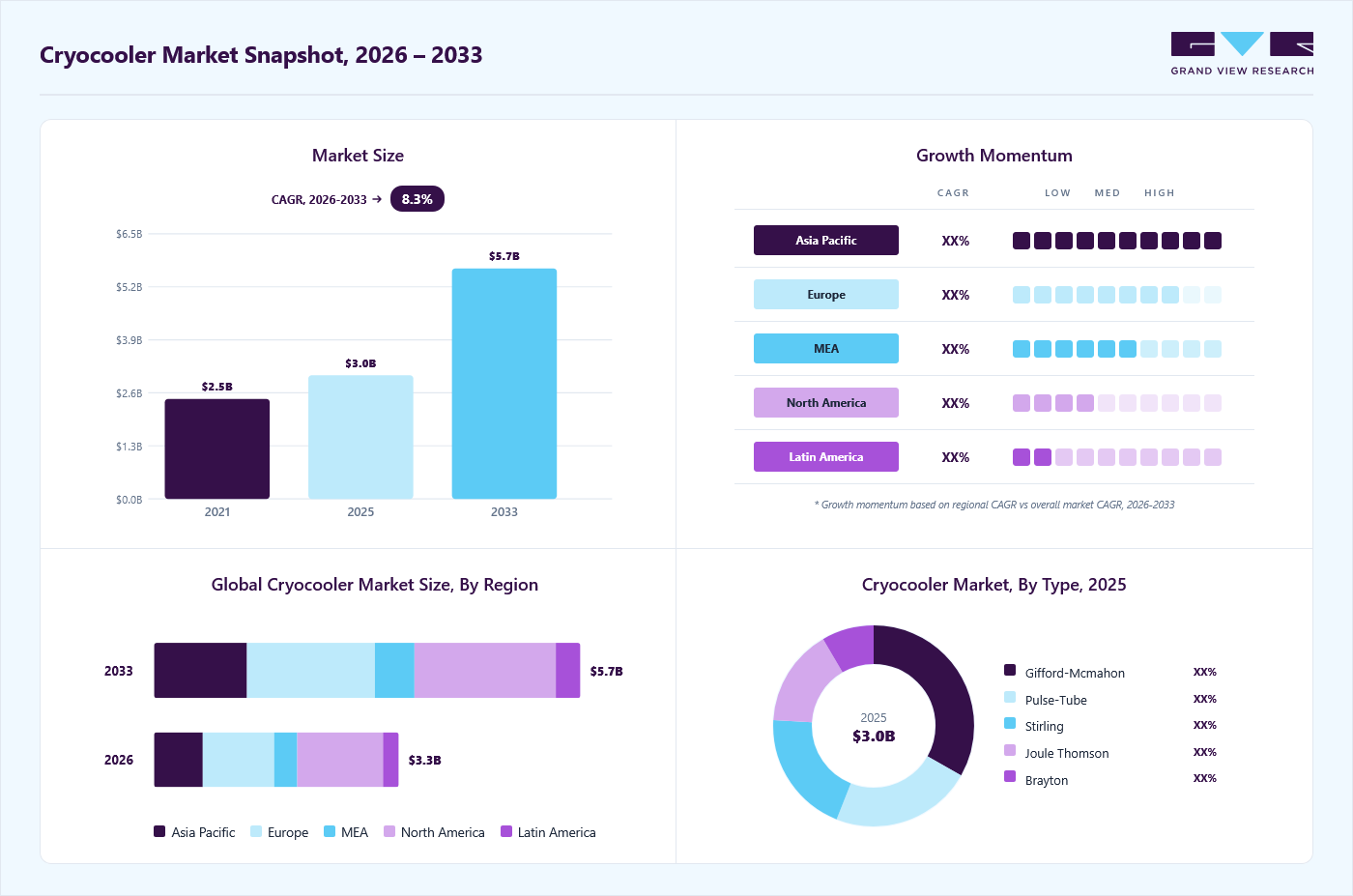

Market Size, 2025

$3.0BMarket Estimate, 2026

$3.3BMarket Forecast, 2033

$5.7BCAGR, 2026–2033

8.3%Cryocooler Market Summary

The global cryocooler market size was valued at USD 3.0 billion in 2025 and is projected to grow from USD 3.3 billion in 2026 to USD 5.7 billion by 2033, at a CAGR of 8.3% from 2026 to 2033. North America dominated the cryocooler market with the largest revenue share of 35.3% in 2025. The adoption of cryocooler is increasing due to their use in cooling down power systems, superconducting magnets, and semiconductors.

Key Market Trends & Insights

- By type: Gifford-Mcmahon segment led the market with the largest revenue share of 33.2% in 2025.

- By heat exchanger type: Regenerative segment led the market with the largest revenue share of 59.1% in 2025.

- By application: Military & defense segment led the market with the largest revenue share of 21.5% in 2025.

Regional Highlights

- Largest regional market: North America (35.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 3.0 Billion

- Estimated market size in 2026: USD 3.3 Billion

- Projected market size by 2033: USD 5.7 Billion

- CAGR (2026-2033): 8.3%

Cryocooler are also used in the defense sector in night vision technology and ground-mounted and airborne military applications. Therefore, the large-scale demand from defense is expected to drive the market growth over the forecast period. Cryocooler play a pivotal role in space exploration, facilitating a range of critical functions in spacecraft and scientific instruments. They are essential components in remote sensing satellites, where they cool infrared sensors to enhance their sensitivity for Earth observation tasks")

Market Dynamics

The cryocooler market is driven by increasing demand for compact and energy-efficient cooling solutions across defense, aerospace, healthcare, semiconductor manufacturing, and scientific research applications. Rising investments in space exploration programs, missile guidance systems, infrared sensors, medical imaging equipment, and quantum computing technologies are accelerating the adoption of advanced cryogenic cooling systems. Technological advancements in pulse-tube and Stirling cryocoolers, which offer higher reliability, lower maintenance requirements, and reduced vibration levels, are further supporting market expansion.

The increasing deployment of infrared (IR) imaging systems, thermal cameras, missile seekers, surveillance equipment, and night-vision devices is a major factor driving demand for cryocoolers. Many of these systems require cryogenic temperatures to enhance sensor sensitivity and improve detection accuracy in challenging operational environments. As military organizations worldwide continue to modernize defense infrastructure and strengthen border surveillance capabilities, the need for highly reliable cryogenic cooling technologies is growing significantly.

Rising defense budgets and increasing procurement of next-generation airborne, naval, and ground-based surveillance platforms are creating substantial opportunities for cryocooler manufacturers. Compact Stirling and pulse-tube cryocoolers are increasingly being integrated into advanced defense electronics due to their ability to deliver long operational life, low power consumption, and superior cooling performance. These developments are expected to sustain strong market demand throughout the forecast period.

The high cost associated with cryocooler manufacturing, installation, and maintenance remains a significant restraint for market growth. Cryocoolers require specialized materials, precision engineering, and advanced manufacturing processes to achieve extremely low operating temperatures, resulting in elevated production costs. Furthermore, system integration and maintenance often require skilled technical expertise, increasing the total cost of ownership for end users. These factors can limit adoption among cost-sensitive industries and small-scale organizations, particularly in emerging economies where budget constraints may hinder investments in advanced cryogenic technologies.

The rapid advancement of quantum computing, superconducting electronics, and next-generation semiconductor manufacturing presents a significant growth opportunity for the cryocooler market. Quantum processors and superconducting devices require ultra-low temperature environments to maintain operational stability and performance, creating increasing demand for highly efficient cryogenic cooling systems. As governments, research institutions, and technology companies invest heavily in quantum research and advanced chip fabrication facilities, cryocoolers are becoming critical enabling technologies. This emerging application landscape is expected to open new revenue streams for manufacturers while encouraging innovation in compact, low-vibration, and energy-efficient cryogenic cooling solutions.

Analyst Perspective

The cryocooler market is poised for strong long-term growth, supported by increasing demand for compact and reliable cooling solutions across aerospace, defense, healthcare, semiconductor, and scientific research applications. The expanding deployment of infrared sensors, satellite systems, superconducting technologies, and advanced medical imaging equipment is driving the need for highly efficient cryogenic cooling systems. Defense and space programs continue to represent key demand centers, particularly as governments increase investments in surveillance, missile guidance, and space exploration technologies. Additionally, ongoing advancements in semiconductor manufacturing and quantum computing are creating new opportunities for next-generation cryocooler technologies. As end users prioritize higher efficiency, reduced maintenance, and improved system reliability, manufacturers focused on innovation and application-specific solutions are expected to benefit from the market's evolving technological landscape.

Drivers, Opportunities & Restraints

MRI machines extensively utilize cryocoolers to maintain the superconducting magnets at extremely low temperatures, typically below 4 Kelvin (-269°C). These cryocooled magnets generate the strong magnetic fields essential for imaging human tissue with high resolution and clarity. These factors are anticipated to fuel the demand for cryocooler in the coming years.

The availability of substitutes, such as thermoelectric coolers and Stirling coolers, has improved efficiency and performance in recent years, making them more viable options for certain applications. This factor is expected to restrain market growth over the forecast period.

The semiconductor industry has seen a significant increase in investment in recent years, with more companies and governments investing in developing cutting-edge semiconductor technologies. This investment increase drives the demand for advanced cooling technologies, such as cryocooler.

Type Insights

This trend can be linked to the increasing use of infrared focal panels in the military and defense sectors. Stirling cryocoolers are commonly employed in military applications to meet the cooling needs of infrared sensors mounted on the ground, in the air, and on ships. The heightened demand for night vision cameras driven by increased thefts and criminal activities further boosts the market.

Based on type, Gifford-Mcmahon segment led the market with the largest revenue share of 33.2% in 2025. This cryocooler's affordable price and distinct characteristics contribute to its appeal. In recent years, Gifford-Mcmahon cryocoolers have become increasingly popular due to the limitations of nitrogen liquefiers, cryo vacuum devices, helium recondensation systems, and cryogenic setups used in a range of scientific research.

Application Insights

This trend can be linked to the increasing use of infrared focal panels in the military and defense sectors. Stirling cryocoolers are commonly employed in military applications to meet the cooling needs of infrared sensors mounted on the ground, in the air, and on ships. In addition, the heightened demand for night vision cameras driven by increased thefts and criminal activities further boosts the market.

Based on application, military & defense segment led the market with the largest revenue share of 21.5% in 2025. This cryocooler's affordable price and distinct characteristics contribute to its appeal. In recent years, Gifford-McMahon cryocoolers have become increasingly popular due to the limitations of nitrogen liquefiers, cryo vacuum devices, helium recondensation systems, and cryogenic setups used in a range of scientific research.

Heat Exchanger Type Insights

Based on heat exchanger type, regenerative segment led the market with the largest revenue share of 59.1% in 2025. In recent years, applications involving high temperatures have increased, leading to the widespread use of regenerative heat exchangers, driven by the growing demand for waste heat recovery. This type of system allows fluids to flow over heat-storage materials to enhance heat transfer efficiency, subsequently boosting market demand.

The recuperative segment held a 40.6% market share in 2024. The demand for recuperative heat exchangers is rising due to their ability to improve energy efficiency by recovering and reusing waste heat in industrial processes. As industries focus on reducing energy consumption and operating costs, these heat exchangers offer a cost-effective solution for enhancing system performance and sustainability.

Regional Insights

North America dominated the cryocooler market with the largest revenue share of 35.3% in 2025. In North America, the market growth is largely propelled by the increasing demand from sectors such as aerospace, defense, medical, and energy. The region's well-established space exploration programs and advancements in quantum computing and medical imaging are key drivers. Moreover, the presence of major players and ongoing investments in research and development are further fueling the market's expansion.

U.S. Cryocooler Market Trends

The cryocooler market in the U.S. held the largest share in the North America region in 2025, due to advancements in aerospace and defense technologies, where cryocoolers are essential for satellite cooling and space exploration. Furthermore, the growing demand for medical applications, particularly in MRI machines and other diagnostic equipment, is pushing market growth. Another significant driver is the focus on energy-efficient solutions, particularly in the semiconductor and electronics industries. The U.S. also benefits from a well-established research and development ecosystem, further spurring innovation and adoption of cryocoolers.

Europe Cryocooler Market Trends

The cryocooler market in Europe is expected to witness significant growth due to its focus on cutting-edge technologies in industries like healthcare, automotive, and electronics. The adoption of cryocoolers for applications such as MRI machines, particle accelerators, and energy-efficient refrigeration systems is on the rise. Moreover, stringent environmental regulations encourage the shift toward more efficient cooling systems, boosting demand for low-noise, eco-friendly cryocooler solutions.

France cryocooler market is expected to expand at a fast-paced CAGR of 9.0% over the forecast period, propelled by the defense and aerospace industries, where these cooling systems are critical for the operation of satellites and advanced technologies. The country’s focus on expanding its space exploration capabilities and military defense systems is a primary factor driving demand. In addition, Russia’s vast natural gas and oil industry requires cryogenic cooling for efficient processing, creating a strong market for cryocoolers in the energy sector.

The cryocooler market in Russia accounted for 22.4% of the market share in 2024, propelled by the defense and aerospace industries, where these cooling systems are critical for the operation of satellites and advanced technologies. The country’s focus on expanding its space exploration capabilities and military defense systems is a primary factor driving demand. Furthermore, Russia’s vast natural gas and oil industry requires cryogenic cooling for efficient processing, creating a strong market for cryocoolers in the energy sector.

Asia Pacific Cryocooler Market Trends

The cryocooler market in Asia Pacific is expected to grow significantly over the forecast period. Rapid industrialization, increasing investments in the semiconductor and electronics industries, and a growing emphasis on renewable energy technologies are key factors contributing to market growth in Asia Pacific. Countries like China, Japan, and India are witnessing substantial demand for cryocoolers, particularly in electronics manufacturing, where cryogenic cooling is essential for maintaining system performance. The region's expanding space and defense sectors also contribute to the rising adoption of cryocoolers for satellite cooling and other advanced applications.

China cryocooler market is expected to expand at a significant CAGR of 25.1% over the forecast period owing to its booming electronics and semiconductor industries, which require cryogenic cooling for efficient operation and enhanced performance. China’s heavy investments in space exploration and the military sector are also key drivers, with cryocoolers essential for satellite cooling. Moreover, the growing demand for medical devices such as MRI machines and the country's increasing focus on renewable energy technologies are contributing to the adoption of cryocoolers in various sectors. China's rapid industrialization and infrastructure development support the demand for efficient, high-performance cooling systems.

The cryocooler market in India is projected to expand at a rapid CAGR of 9.7% over the forecast period, largely driven by the increasing use of cryocoolers in healthcare, especially for medical imaging and diagnostics, which are becoming more widespread in the country’s expanding healthcare infrastructure. India's growing electronics and semiconductor industries also contribute to market growth, as cryocoolers are essential for cooling sensitive components. Moreover, the rise of space and defense programs in India creates additional demand for cryocoolers in satellite and aerospace applications.

Middle East Cryocooler Market Trends

The cryocooler market in the MEA is expanding due to the rapid development of oil and gas infrastructure, and investments in research and technology. Cooling systems, including cryocoolers, are essential for maintaining performance in extreme heat environments, particularly in the oil and gas sector, where maintaining equipment at optimal temperatures is crucial. In addition, the region’s growing healthcare and electronics industries are increasing the demand for cryocoolers in medical imaging and semiconductor cooling applications.

Latin America Cryocooler Market Trends

The cryocooler market in Latin America is seeing a gradual rise in demand, driven by increasing healthcare infrastructure and the need for cooling solutions in industries such as mining and energy. As the region looks to develop its renewable energy potential, there is growing interest in cryocoolers for energy-efficient applications in power plants and wind turbines. However, the market remains relatively nascent, with growth fueled primarily by the adoption of medical and industrial applications.

Key Cryocooler Company Insights

Some of the key players operating in the market include Sumitomo Heavy Industries, Ltd. and RIX Industries.

-

RIX Industries specializes in manufacturing a diverse range of products, including gas generation systems, precision compressor solutions, and cryogenic cooling technologies. Its comprehensive capabilities involve production, design, engineering, assembly, and testing. The company's extensive offerings serve multiple markets, including marine, aerospace, industrial, medical, energy, and critical infrastructure.

-

Sumitomo Heavy Industries, Ltd. is a comprehensive manufacturer specializing in various products, including cryocoolers. The company manufactures cryocoolers for use in medical devices like MRI machines, advanced scientific fields such as physics and chemistry, and cryopumps for creating ultra-high vacuum environments for semiconductor production

Key Cryocooler Companies

The following key companies have been profiled for this study on the cryocooler market.

-

Sumitomo Heavy Industries, Ltd.

-

RIX Industries

-

Northrop Grumman

-

Bluefors Oy

-

RICOR

-

AMETEK, Inc.

-

ULVAC CRYOGENICS, INC.

-

CryoSpectra GmbH

-

Lihan Cryogenics Co., Ltd.

-

CSSC Pride (Nanjing) Cryogenic Technology Co., Ltd

-

Edwards Vacuum

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (e.g., Sumitomo Heavy Industries, Ltd., Northrop Grumman, AMETEK, Inc., Edwards Vacuum, RIX Industries, ULVAC CRYOGENICS, INC.)

- Invest heavily in R&D to enhance cooling efficiency, reliability, and lifecycle performance for aerospace, defense, healthcare, and semiconductor applications.

- Strengthen market presence through long-term contracts, global distribution networks, and strategic collaborations with government and industrial customers.

- Possess strong technological expertise, extensive patent portfolios, and proven performance in mission-critical cryogenic applications.

- Benefit from established global service networks and diversified product portfolios that support multiple end-use industries.

- Higher production and operational costs can limit competitiveness in price-sensitive markets.

- Large organizational structures may result in slower adaptation to rapidly emerging technologies and niche customer requirements.

Emerging & Regional Players (e.g., Bluefors Oy, RICOR, CryoSpectra GmbH, Lihan Cryogenics Co., Ltd., CSSC Pride (Nanjing) Cryogenic Technology Co., Ltd.)

- Focus on specialized applications such as quantum computing, research laboratories, and advanced industrial cooling systems.

- Expand market share through customized solutions, competitive pricing, and regional partnerships.

- Greater flexibility in product development enables quicker response to evolving customer and technology demands.

- Strong positioning in emerging technology sectors and regional markets supports rapid business growth.

- Limited international distribution and after-sales support capabilities compared to established competitors.

- Lower financial resources and brand recognition can restrict participation in large-scale global projects and government procurements.

Recent Developments

-

In January 2024, the SHI Cryogenics Group unveiled the RJT-100 4K GM-JT Cryocooler. This cutting-edge Gifford-McMahon/Joule-Thomson (GM-JT) Cryocooler represents SHI's latest and most powerful 4K Cryocooler, boasting a capacity of up to 9.0 W at 4.2 K (50/60 Hz).

-

In March 2023, Bluefors Oy acquired Cryomech, a leading cryocooler technology company based in Syracuse, New York, U.S. This strategic move unites nearly 600 experts across multiple countries, enabling Bluefors Oy to enhance its service to customers in quantum technology, physics research, and industrial applications. The acquisition aligns with Bluefors Oy' growth strategy to advance ultra-low temperature cooling technology in R&D and industrial sectors.

Cryocooler Market Report Scope

Report Attribute

Details

Market size in 2025

USD 3.0 billion

Estimated Market size in 2026

USD 3.3 billion

Projected Market size by 2033

USD 5.7 billion

Growth rate

CAGR of 8.3% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, heat exchanger type, application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; Russia; Italy; China; India; Japan; South Korea; Australia; Brazil; Argentina; South Africa; Saudi Arabia

Key companies profiled

Sumitomo Heavy Industries, Ltd.; RIX Industries; Northrop Grumman; Bluefors Oy; RICOR; AMETEK, Inc.; ULVAC CRYOGENICS, INC.; CryoSpectra GmbH; Lihan Cryogenics Co., Ltd.; CSSC Pride (Nanjing) Cryogenic Technology Co., Ltd; Edwards Vacuum.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Cryocooler Market Report Segmentation

This report forecasts revenue growth at global, regional & country levels and provides an analysis of the industry trends in each of the sub-segments from 2018 to 2030. For this study, Grand View Research has segmented the global cryocooler market based on type, heat exchanger type, application, and region:

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Gifford-Mcmahon

-

Pulse-Tube

-

Stirling

-

Brayton

-

Joule Thomson

-

-

Heat Exchanger Type (Revenue, USD Million, 2021 - 2033)

-

Regenerative

-

Recuperative

-

-

Application (Revenue, USD Million, 2021 - 2033)

-

Military & Defense

-

Healthcare

-

Power & Energy

-

Aerospace

-

Research & Development

-

Transport

-

Mining & Metals

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Russia

-

Italy

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

-

Research Methodology

Segment Definition

Type

Revenue Capture Definition

Gifford-Mcmahon

Revenue is generated from the sale and integration of Gifford-McMahon cryocoolers used in MRI systems, laboratory equipment, superconducting magnets, and industrial cryogenic applications.

Pulse-Tube

Revenue capture includes sales of pulse-tube cryocoolers utilized in aerospace, defense, semiconductor, and scientific research applications.

Stirling

Revenue is derived from Stirling cryocoolers deployed in infrared imaging systems, missile guidance systems, thermal cameras, and portable cryogenic devices.

Brayton

Revenue includes the commercialization of Brayton cryocoolers used in large-scale aerospace, satellite, and industrial cooling applications requiring continuous and efficient cryogenic operation.

Joule Thomson

Revenue capture comprises sales of Joule-Thomson cryocoolers employed in compact defense systems, gas liquefaction processes, and scientific instruments.

Heat Exchanger Type

Revenue Capture Definition

Regenerative

Revenue is generated by cryocoolers utilizing regenerative heat exchanger technology, including equipment sales and replacement of regenerator materials and components.

Recuperative

Revenue includes cryocooler systems based on recuperative heat exchanger designs used in Brayton and other continuous-flow cooling systems.

Application

Revenue Capture Definition

Military & Defense

Revenue is captured from cryocoolers integrated into missile seekers, thermal imaging systems, surveillance equipment, radar systems, and night-vision devices.

Healthcare

Revenue originates from cryocoolers used in MRI systems, medical imaging equipment, cryosurgery devices, and biomedical research instruments.

Power & Energy

Revenue is generated through the deployment of cryocoolers in superconducting power systems, energy storage technologies, hydrogen infrastructure, and advanced energy research applications.

Aerospace

Revenue capture includes cryocoolers supplied for satellites, space telescopes, earth observation systems, and space exploration missions.

Research & Development

Revenue is derived from cryocoolers utilized in universities, national laboratories, research institutes, and scientific facilities conducting advanced experiments.

Transport

Revenue includes cryocoolers used in cryogenic fuel storage, LNG transportation systems, hydrogen-powered mobility solutions, and temperature-sensitive transport technologies.

Mining & Metals

Revenue is generated from cryocoolers employed in materials research, metallurgical testing, superconducting applications, and specialized industrial processes within the mining and metals sector.

Others

Revenue capture comprises cryocoolers used in agricultural seed banks, environmental monitoring instruments, climate research equipment, biological sample preservation, and life science laboratories.

Estimation Model

Layer Name

Core Question

Functional Description

End-Use Industry Demand Layer

Who primarily utilizes cryocoolers across industries?

The estimation begins by analyzing demand from key end-use sectors including defense, aerospace, healthcare, semiconductor manufacturing, research laboratories, power & energy, and transportation. Adoption rates of cryogenic cooling systems within these industries are assessed to determine the potential demand base for cryocooler technologies globally.

Technology Adoption Layer

Which cryocooler technologies are gaining market traction?

The potential market demand is further evaluated through the adoption of various cryocooler technologies such as Gifford-McMahon, Pulse-Tube, Stirling, Brayton, and Joule-Thomson systems. Industry-specific technology preferences, performance requirements, cooling capacities, and technological advancements are analyzed to estimate segment-wise penetration levels.

Equipment Deployment Layer

How many cryocoolers are being installed and upgraded?

Annual demand is estimated based on new installations, replacement cycles, defense modernization programs, satellite launches, medical equipment deployment, semiconductor fabrication expansion, and scientific research investments. Increasing demand for quantum computing and advanced sensing technologies also contributes to equipment deployment estimates.

Revenue Layer

How much revenue is generated from cryocooler solutions?

Market revenue is calculated by aggregating earnings generated from cryocooler equipment sales. Revenue contributions are analyzed across technology types, applications, and geographic regions to derive the overall cryocooler market size.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Competitive Landscape and Company Benchmarking Analysis

A detailed assessment of the cryocooler market competitive environment was delivered, including profiling of key manufacturers, company categorization into established and emerging players, market positioning analysis, product portfolios, strategic initiatives, and technological capabilities across major industry participants.

Enabled the client to identify leading competitors, evaluate market concentration levels, understand technology leadership trends, and benchmark strategic positioning for future business expansion and partnership opportunities.

Application-Level Demand Assessment and Opportunity Mapping

Comprehensive analysis was provided across defense, aerospace, healthcare, power & energy, transport, research, mining, agriculture, environmental monitoring, and biological applications. The study highlighted revenue contribution, adoption trends, and growth potential of each application segment.

Assisted the client in identifying high-growth end-use sectors, prioritizing investment areas, and understanding emerging application opportunities such as quantum computing, biological preservation, and environmental monitoring.

Technology Segmentation and Market Revenue Evaluation

Delivered an in-depth evaluation of cryocooler technologies including Gifford-McMahon, Pulse-Tube, Stirling, Brayton, and Joule-Thomson systems, along with regenerative and recuperative heat exchanger technologies. Revenue capture frameworks and market dynamics were also developed for each segment.

Provided actionable insights into technology adoption patterns, future innovation trends, and revenue-generating segments, enabling more informed product development, market entry, and long-term growth strategies.

Frequently Asked Questions About This Report

The global cryocoolers market size was estimated at USD 3.0 billion in 2025 and is expected to reach USD 3.3 billion in 2026.

The global cryocoolers market, in terms of revenue, is expected to grow at a compound annual growth rate of 8.3% from 2026 to 2033 to reach USD 5.7 billion by 2033.

Key factors driving the cryocoolers market include the increasing demand for efficient cooling solutions in aerospace, healthcare, and semiconductor industries. Technological advancements, such as the development of compact, energy-efficient systems, along with growing investments in space exploration and renewable energy, are also fueling market growth.

North America dominated the cryocooler market with the largest revenue share of 35.3% in 2025.

Asia Pacific is anticipated to be one of the fastest-growing regional markets over the forecast period, driven by increasing investments in semiconductor manufacturing, space programs, and defense modernization initiatives.

The regenerative segment accounted for the largest revenue share of 59.1% in 2025.

The military & defense segment led the market with the largest revenue share of 21.5% in 2025.

The Gifford-Mcmahon segment dominated the market in 2025 accounting for 33.2% of the overall revenue share. The growing demand for Gifford-McMahon cryocoolers is driven by their efficiency and reliability in applications requiring low temperatures, such as in aerospace, medical imaging, and scientific research. Their ability to deliver stable cooling at cryogenic temperatures with relatively low maintenance makes them a preferred choice in both industrial and laboratory settings

Some of the key players operating in the cryocoolers market are Sumitomo Heavy Industries, Ltd.; RIX Industries; Northrop Grumman; Bluefors Oy; RICOR; AMETEK, Inc.; ULVAC CRYOGENICS, INC.; CryoSpectra GmbH; Lihan Cryogenics Co., Ltd.; CSSC Pride (Nanjing) Cryogenic Technology Co., Ltd; Edwards Vacuum.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.