- Home

- »

- Power Generation & Storage

- »

-

District Heating Market Size And Share Report, 2026-2033GVR Report cover

![District Heating Market (2026 - 2033)Report]()

District Heating Market (2026 - 2033)

Size, Share & Trends Analysis Report By Heat Source (Natural Gas, Renewables, Oil & Petroleum Products), By Type, By Application, By Plant Type, By Region, And Segment Forecasts

Market Size, 2025

$207.2BMarket Estimate, 2026

$217.6BMarket Forecast, 2033

$318.8BCAGR, 2026–2033

5.6%District Heating Market Summary

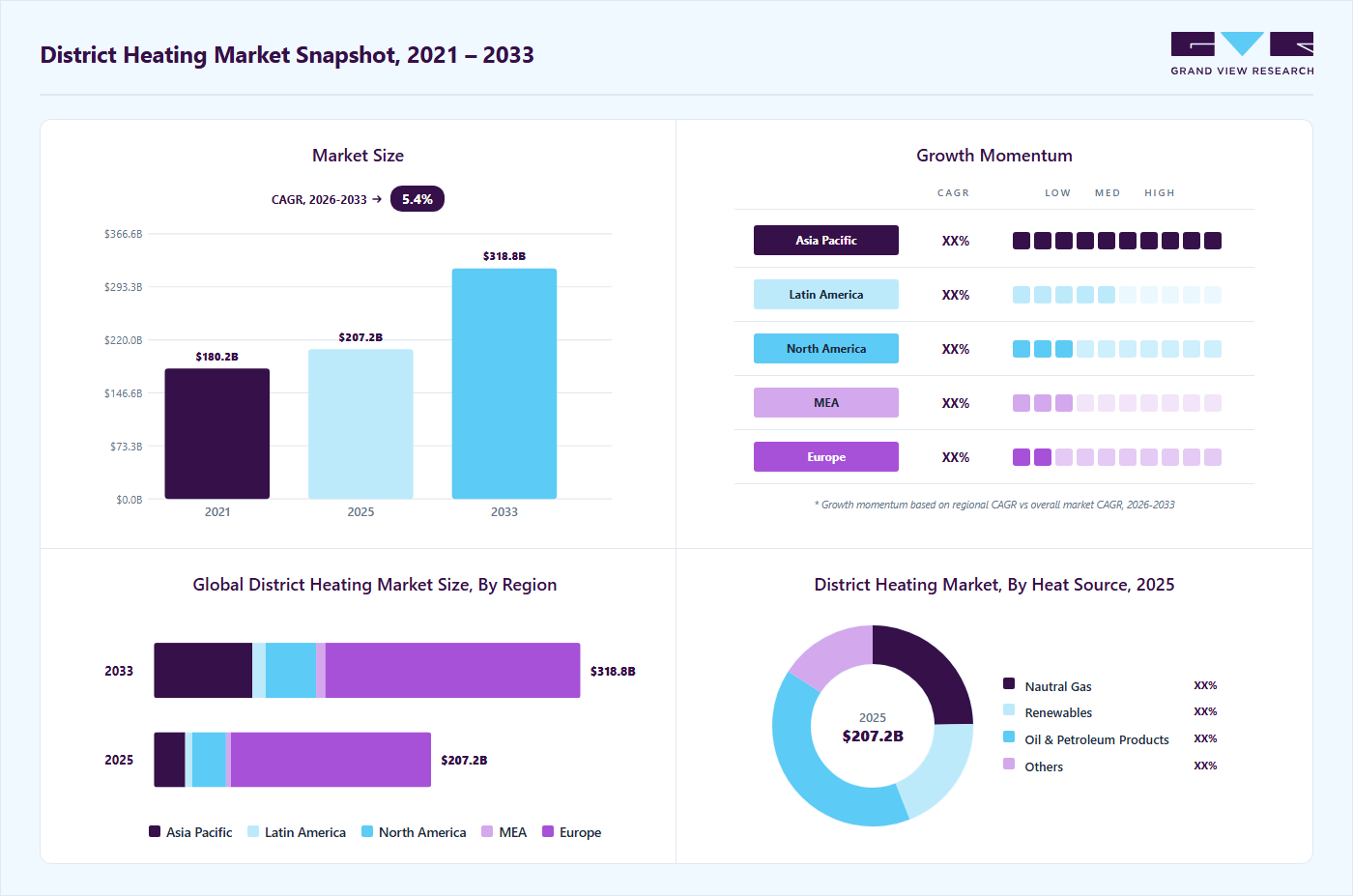

The global district heating market size was valued at USD 207.2 billion in 2025 and is projected to grow from USD 217.6 billion in 2026 to USD 318.8 billion by 2033, at a CAGR of 5.6% from 2026 to 2033. The market in Europe dominated with a revenue share of 72.2% in 2025. District heating systems operate by generating heat at a centralized facility using energy sources such as waste heat, biomass, geothermal, or renewables, and distributing it through insulated pipelines to end users.

Key Market Trends & Insights

- By heat source: Oil & petroleum products segment held the largest market share of 40.1% in 2025.

- By type: Biomass & biofuel segment held the largest market share of 63.4% in 2025.

- By plant type: Combined heat & power segment held the largest market share of 60.8% in 2025.

- By application: Residential segment held the largest market share of 67% in 2025.

Regional Highlights

- Largest regional market: Europe (72.2% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

Market Size & Forecast

- Market size in 2025: USD 207.2 Billion

- Estimated market size in 2026: USD 217.6 Billion

- Projected market size by 2033: USD 318.8 Billion

- CAGR (2026-2033): 5.6%

This centralized distribution framework serves as the foundation of the district heating pipeline network market, enabling efficient transmission of thermal energy for residential, commercial, and industrial applications. Increasing investments in sustainable heat infrastructure, technological advancements in thermal storage, and the growing shift toward renewable-based networks, particularly the accelerating solar district heating market, are key factors driving industry expansion.")

District heating systems continue to be preferred due to their ability to deliver superior energy efficiency and lower lifecycle costs compared to decentralized heating units. Modern installations increasingly incorporate integrated district heating & cooling configurations, enhancing system flexibility and overall performance within the broader district heating & cooling market. Furthermore, the adoption of advanced control mechanisms, automation technologies, and digital monitoring platforms is supporting the evolution of next-generation district heating solution market offerings. The ongoing transition toward low-carbon and renewable heat sources is expected to strengthen market demand further over the forecast period.

Drivers, Opportunities & Restraints

The global industry continues to advance on the back of rising demand for reliable, efficient, and low-emission thermal energy systems, particularly in regions accelerating the shift from fossil-fuel-based boilers to cleaner heat sources. Utilities, municipalities, and energy developers are increasing investments in centralized heating networks to support decarbonization goals and improve cost efficiency, where distributed renewable adoption remains uneven. The ability of district heating systems to integrate diverse energy sources, waste heat, biomass, geothermal, and the rapidly expanding solar district heating market positions them as a key enabler of sustainable urban heating. Ongoing modernization of thermal grids, combined with the need to upgrade aging pipelines and substations, is further supporting growth across the district heating pipeline network market, as well as demand for components within the district heating pipe market and district heating valves market.

Significant opportunities are emerging from the development of low-temperature district heating networks, advanced heat pumps, and hybrid district heating & cooling configurations, all of which enhance system flexibility within the broader district heating & cooling market. Digital technologies such as predictive maintenance, real-time demand forecasting, and intelligent control systems are improving operational performance and reducing lifecycle costs. Rising urbanization, expanding building footprints, and increasing adoption of sustainable infrastructure solutions are also encouraging the deployment of next-generation offerings in the district heating solution market. However, the market faces notable constraints, including high upfront investment requirements, integration challenges associated with retrofitting older buildings, and lengthy project approval timelines. Uncertain regulatory environments and the need for coordinated public-private financing models remain additional hurdles that may limit the pace of large-scale expansion.

Heat Source Insights

The oil & petroleum products segment held the largest share at 40.1% in 2025, supported by its reliability and compatibility with existing large-scale boiler systems. Many legacy district heating networks continue to rely on petroleum-based fuels for stable, high-temperature output during peak demand seasons. Modernization initiatives are simultaneously driving upgrades across the district heating pipeline network market, including increased use of advanced pipes and valves. These factors together sustain the prominence of oil-based systems despite the sector’s broader shift toward cleaner heat sources.

The renewables segment is projected to record the fastest CAGR of 6.6%, driven by strong policy support for low-carbon heating and the growing integration of geothermal, biomass, and the expanding solar district heating market. Adoption of low-temperature networks and heat-pump-based systems is accelerating the transition toward sustainable district heating models. These advancements are also strengthening demand within the broader district heating & cooling market as cities modernize thermal infrastructure. Increasing deployment of advanced district heating solution market technologies further enhances system efficiency and operational performance.

Type Insights

The biomass & biofuel segment dominated the district heating market with a 63.4% share in 2025, driven by strong policy support for renewable heat, abundant feedstock availability, and the ability of biomass-based plants to deliver a stable baseload thermal supply. Their compatibility with existing boiler infrastructure and competitive operating costs has further accelerated adoption across municipal and industrial networks. Modernization of heat grids supported by upgrades in the district heating pipeline network market and more efficient piping systems continues to reinforce the preference for biomass-based district heating. As cities transition toward carbon-neutral heating strategies, biomass and biofuel technologies remain integral to near-term decarbonization pathways.

The biomass & biofuel segment is expected to expand at the fastest CAGR of 7.4%, supported by the increasing shift to low-carbon thermal sources and rising investments in waste-to-energy and biofuel-fired district heating plants. Growth in hybrid systems integrating biomass with heat pumps and solar collectors, especially within the evolving solar district heating market, is further enhancing system efficiency and operational flexibility. Ongoing deployment of advanced technologies in the district heating solution market and district heating & cooling market is making biomass-based systems more scalable and cost-effective. Supportive regulatory frameworks and expanding thermal storage capacities are set to strengthen the segment’s leading position over the forecast period.

Plant Type Insights

The combined heat & power (CHP) segment captured 60.8% of the total market in 2025, retaining its position as the leading plant type in district heating systems. CHP plants offer high overall efficiency by producing electricity and usable heat simultaneously, making them ideal for densely populated urban networks with consistent thermal demand. Their ability to reduce fuel consumption, lower emissions, and enhance energy security continues to drive adoption across new-build and retrofit projects.

Ongoing modernization of heat networks supported by investments in the district heating pipeline network market and high-efficiency transfer stations is further reinforcing the dominance of CHP-based district heating infrastructure.

The CHP segment is expected to expand at the fastest CAGR of 6.4%, driven by increasing deployment of low-carbon and renewable-integrated systems, including biomass-CHP and solar-assisted hybrid plants within the solar district heating market. Improvements in turbine efficiency, waste-heat recovery, and digital optimization platforms are strengthening growth within the broader district heating solution market. CHP’s capability to deliver both stable baseload heat and flexible thermal output aligns well with expanding district heating & cooling market requirements, especially as cities pursue decarbonization targets. These advantages position CHP as the most scalable and economically viable plant type for district energy networks moving forward.

Application Insights

The residential segment accounted for 67% of total revenue in 2025, maintaining its position as the dominant application category. Growing urban density, rising heating demand in multi-dwelling buildings, and increasing adoption of centralized heating systems continue to strengthen residential reliance on district energy networks. Ongoing upgrades in the district heating pipeline network market, along with improved insulation standards and smart metering technologies, are making residential district heating more efficient and cost-effective. Supportive policies promoting clean, shared heating infrastructure and reductions in individual boiler emissions further reinforce the segment’s leading share in both new developments and retrofit projects.

The residential segment is projected to expand at the fastest CAGR of 6.4%, driven by accelerating demand for low-carbon heating, improved building energy codes, and growing integration of renewable heat sources, including solar-assisted systems within the solar district heating market. Rising investments in energy-efficient buildings and smart thermal networks are enhancing the appeal of centralized solutions across urban regions. Continued innovation in the district heating solution market and broader district heating & cooling market, including digital control platforms, advanced substations, and thermal storage, supports scalable, flexible residential expansion. This trend positions the residential application as the primary growth engine of the district heating industry over the forecast period.

Regional Insights

Europe District Heating Market Trends

Europe dominated the global district heating landscape with a 72.2% market share in 2025, driven by strong decarbonization policies and large-scale adoption of renewable heat. Extensive modernization of thermal networks and expansion of the European district heating market continue to accelerate the uptake of advanced low-temperature systems. Investment in biomass, geothermal, and solar-assisted networks is reshaping regional energy strategies, including growth within the UK district heating market. Europe's commitment to climate-neutral heating solutions positions it as the global leader in district energy innovation.

Asia Pacific District Heating Market Trends

The district heating market in Asia Pacific is projected to register the fastest CAGR of 15.4%, fueled by rapid urbanization, rising household heating demand, and expanding industrial clusters. Strong investment in integrated district heating & cooling systems and hybrid renewable networks supports the region's transition away from coal-based heat. Countries such as China, South Korea, and Japan are increasingly adopting solar-assisted solutions, boosting the solar district heating market across APAC. Government-led infrastructure buildouts and digital grid enhancements further strengthen the region's growth trajectory.

North America District Heating Market Trends

The district heating market in North America is experiencing steady growth supported by the modernization of urban heat networks and the rising adoption of clean thermal systems. Expansion of the North America district heating & cooling market is driven by increasing integration of geothermal, biomass, and solar heat, particularly in university campuses and dense urban districts. Federal incentives promoting low-carbon heating technologies are boosting the deployment of renewable-assisted systems, including the North American solar district heating market. Growing demand for energy-efficient building stock further propels market development.

U.S. District Heating Market Trends

The district heating market in the U.S. is expanding due to upgrades in aging steam networks and greater investment in sustainable thermal infrastructure across cities and institutional campuses. Increasing emphasis on decarbonizing building heat is driving the adoption of advanced district heating solutions and low-temperature networks. Growth in state-level clean energy mandates is accelerating the shift toward biomass, waste heat, and solar-assisted district systems. Rising demand for energy resilience and efficient heating options continues to strengthen the U.S. market outlook.

Latin America District Heating Market Trends

The district heating market in Latin America is tied to rising urban development, energy diversification, and early adoption of renewable-assisted heating networks. Countries are pursuing modern, centralized heating solutions to reduce emissions and improve urban energy efficiency. Investment in biomass and waste-heat-based district systems is gradually strengthening the regional infrastructure base. Government incentives and private-sector participation are supporting long-term district heating expansion.

Middle East & Africa District Heating Market Trends

The district heating market in the Middle East & Africa region is witnessing increasing adoption of district energy systems driven by urban growth and rising interest in efficient thermal infrastructure. Cooling-dominated climates are encouraging the deployment of integrated district heating & cooling market solutions for large developments. Waste heat recovery and solar-assisted networks are gaining attention as part of broader sustainability goals. Government-backed infrastructure programs and industrial expansion support continued market development.

Key District Heating Company Insights

Key players operating in the district heating market are undertaking various initiatives to strengthen their presence and increase the reach of their products and services. Strategies such as expansion activities and partnerships are key in propelling the market growth. Some of the key players operating in the global district heating market include Vattenfall AB, ENGIE, among others.

-

Vattenfall AB is one of the most influential participants in the global district heating market, operating some of Europe’s largest and most advanced heat networks across Sweden, Germany, and the Netherlands. The company specializes in developing low-carbon and fossil-free district heating systems powered by biomass, waste heat recovery, large-scale heat pumps, geothermal integration, and renewable-based thermal storage. Vattenfall continues to drive innovation through digital heat-network optimization, thermal balancing solutions, and sector-coupling strategies that integrate electricity, heating, and cooling.

-

ENGIE plays a pivotal role in shaping the global district heating landscape, operating one of the world’s largest portfolios of district heating and cooling networks across Europe, North America, and Asia. The company focuses on sustainable heat generation through biomass, biogas, geothermal energy, waste-to-energy plants, and high-efficiency combined heat and power (CHP) facilities. ENGIE’s long-term strategy centers on reducing carbon intensity by deploying low-temperature networks, smart substations, and digital monitoring platforms that optimize thermal distribution and reduce system losses.

Key District Heating Companies:

The following are the leading companies in the district heating market. These companies collectively hold the largest Market share and dictate industry trends.

- ALFA LAVAL

- Dall Energy

- Danfoss Group

- ENGIE

- Fortum

- FVB Energy Inc.

- General Electric Company

- Helen

- Ramboll

- Uniper SE

- Vattenfall AB

- Veolia

Recent Developments

- In November 2025, Veolia launched its new “Ecothermal Grid” initiative to accelerate the expansion of low-carbon district heating networks across the U.K. The program includes a USD 1.27 billion pipeline of potential heat-network projects scheduled through 2030, aimed at supporting the country’s long-term decarbonization strategy. The first phase focuses on upgrading and extending existing waste to energy powered district heating systems, enabling wider adoption of renewable and recovered heat.

District Heating Market Report Scope

Report Attribute

Details

Market size in 2025

USD 207.2 billion

Estimated market size in 2026

USD 217.6 billion

Projected market size by 2033

USD 318.8 billion

Growth rate

CAGR of 5.6% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Heat source, type, application, plant type, region

Regional scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; South Korea; Brazil; Saudi Arabia; UAE

Key companies profiled

ALFA LAVAL; Dall Energy; Danfoss Group; ENGIE; Fortum; FVB Energy Inc.; General Electric Company; Helen; Ramboll; Uniper SE; Vattenfall AB; Veolia

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

District Heating Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global district heating market report on the basis of heat source, type, application, plant type, and region.

-

Heat Source Outlook (Revenue, USD Million, 2021 - 2033)

-

Natural Gas

-

Renewables

-

Oil & Petroleum Products

-

Others

-

-

Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Geothermal

-

Biomass & Biofuel

-

Others

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Commercial

-

Residential

-

Industrial

-

-

Plant Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Boiler Plant

-

Combined Heat & Power

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

Asia Pacific is the fastest-growing region over the forecast period.

The oil & petroleum products segment led with a 40.1% revenue share in 2025, while the renewables segment is the fastest-growing.

The biomass & biofuel segment led with a 63.4% revenue share in 2025, and is the fastest-growing type.

The combined heat & power segment led with a 60.8% revenue share in 2025, while the CHP segment is the fastest-growing.

Residential segment held the largest share (over 67.0%) in 2025, while the residential segment is the fastest-growing.

The global district heating market size was valued at USD 207.2 billion in 2025 and is estimated at USD 217.6 billion for 2026.

The global district heating market is expected to grow at a CAGR of 5.6% from 2026 to 2033, reaching USD 318.8 billion by 2033.

Europe dominated with a 72.2% revenue share in 2025.

Some of the key vendors operating in the global district heating market include Vattenfall AB, ENGIE, Danfoss Group, Alfa Laval, Veolia, Ramboll, and Fortum, among others.

The key factors driving the District Heating market include the growing focus on decarbonizing urban heating systems, increasing integration of renewable heat sources such as biomass, geothermal, and solar thermal, and the rising need for energy-efficient, centralized heating solutions that reduce emissions and operating costs compared to individual heating systems.

About the Author(s)

Power Generation & Storage Research Team

Energy & Power · Power Generation & StorageThis report was authored by the power generation & storage research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the power generation & storage segment of the energy & power industry. All findings are based on proprietary energy & power databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.