- Home

- »

- Electronic Devices

- »

-

Electronic Waste Recycling Market Size & Share Report 2033GVR Report cover

![Electronic Waste Recycling Market Size, Share & Trends Report]()

Electronic Waste Recycling Market (2026 - 2033) Size, Share & Trends Analysis Report By Material (Metal, Glass, Plastic), By Source (Household Appliances, Consumer Electronics, Industrial & Commercial Equipment, IT & Telecommunication, Medical Equipment), By Recycling Process, By Region, And Segment Forecasts

Market Size, 2025

$45.2BMarket Estimate, 2026

$47.5BMarket Forecast, 2033

$91.5BCAGR, 2026–2033

9.8%Electronic Waste Recycling Market Summary

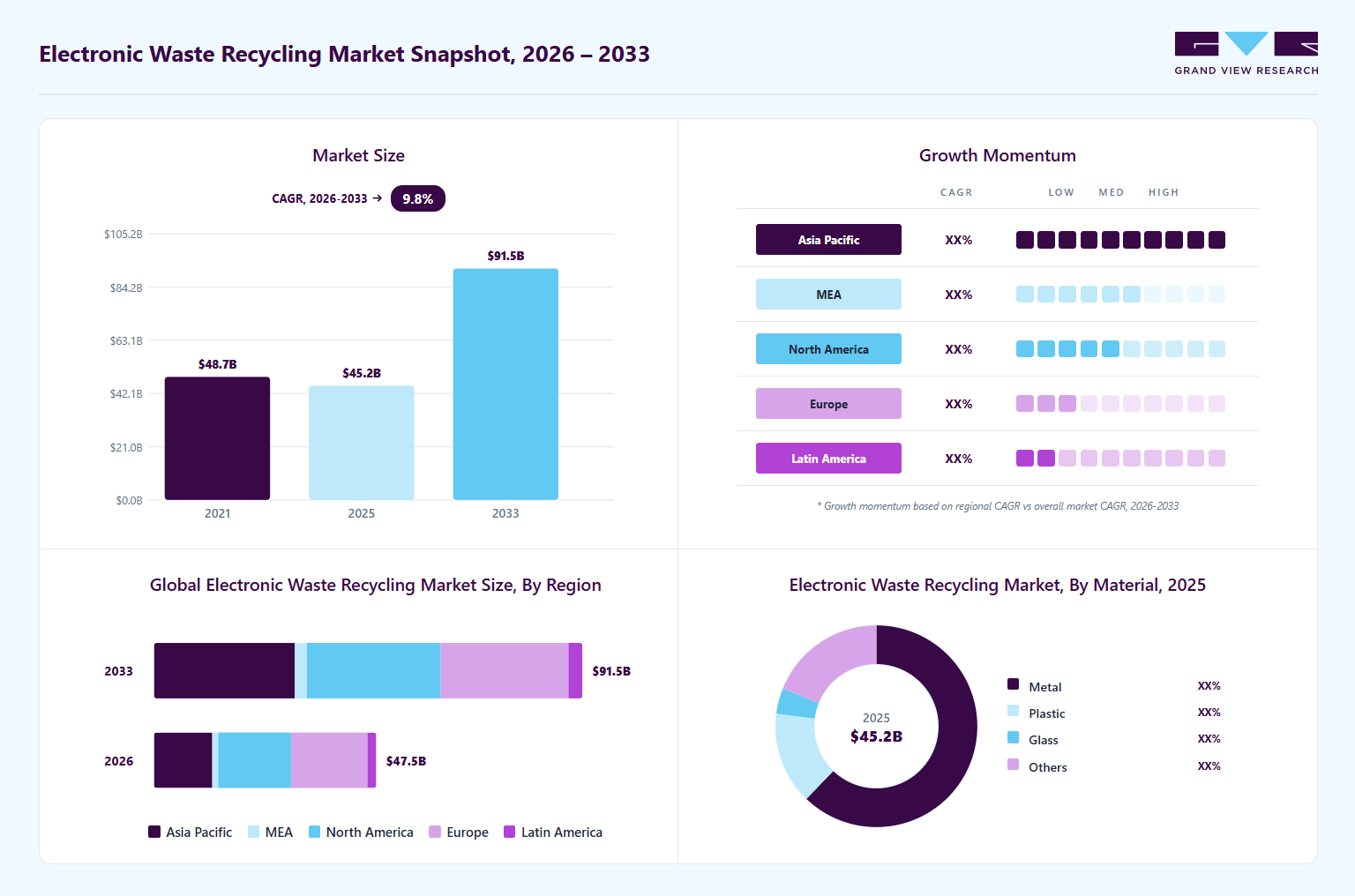

The global electronic waste recycling market size was valued at USD 45.2 billion in 2025 and is projected to grow from USD 47.5 billion in 2026 to USD 91.5 billion by 2033, at a CAGR of 9.8% from 2026 to 2033. Europe electronic waste (e-waste) recycling dominated the global market with the largest revenue share of 35.0% in 2025. The market is growing due to the rapid proliferation of consumer electronics and shortening product life cycles.

Key Market Trends & Insights

- The electronic waste recycling industry in U.S. is expected to grow significantly over the forecast period.

- By material, metal led the market and held the largest revenue share of 62.2% in 2025.

- By source, the IT & telecommunication segment held the dominant position in the market and accounted for the largest revenue share in 2025.

- By recycling process, the hydrometallurgical processing segment is expected to grow at the fastest CAGR from 2026 to 2033.

Market Size & Forecast

- 2025 Market Size: USD 45.2 Billion

- 2033 Projected Market Size: USD 91.5 Billion

- CAGR (2026-2033): 9.8%

- Europe: Largest market in 2025

Increasing penetration of smartphones, laptops, wearables, and IoT-enabled devices has led to a sharp rise in discarded electronic products. Stringent environmental regulations and extended producer responsibility (EPR) frameworks are also driving the electronic waste recycling industry. Governments across regions such as the EU, North America, and parts of Asia Pacific are mandating proper disposal, collection, and recycling of e-waste to mitigate hazardous environmental impacts. Regulations like the EU’s WEEE Directive and similar policies in countries such as India and Japan compel manufacturers and importers to manage e-waste responsibly, thereby accelerating the adoption of formal recycling channels and technologies. India’s 2025 update to Extended Producer Responsibility (EPR) rules raises e-waste recycling targets, requiring producers to recover about 60% of the previous year’s sales by weight, with targets increasing annually to strengthen formal recycling and resource recovery.")

The increasing economic value of recovered materials is significantly boosting the e waste recycling market. Electronic waste contains high-value metals such as gold, silver, copper, palladium, and rare earth elements, which can be extracted and reintroduced into the supply chain through advanced recycling technologies. For instance, in June 2025, ETH Zurich introduced an innovative technique to extract rare earth elements from electronic waste more efficiently, marking a significant step toward sustainable recycling practices and reducing dependence on traditional mining. Rare earth elements are essential components in modern technologies, supporting applications such as fluorescent lighting, high-performance magnets used in hard drives, and generators for wind energy systems.

With rising raw material costs and growing supply chain vulnerabilities, the electronic scrap recycling market is gaining momentum as manufacturers increasingly seek cost-effective and sustainable alternatives to virgin resource extraction. This urban mining trend is further accelerating growth in the e-scrap recycling market, particularly among electronics manufacturers aiming to improve resource efficiency and strengthen circular supply chains. In addition, growing environmental awareness and sustainability initiatives among corporations and consumers are driving expansion of the e-waste management market. Organizations are aligning with ESG objectives and circular economy strategies, resulting in higher investments in recycling infrastructure, take-back programs, and partnerships with certified recyclers. Consumers are also becoming more conscious of responsible disposal practices, contributing to rising collection rates and broader participation in electronic waste recycling initiatives.

Market Dynamics

The rapid growth in discarded consumer electronics, IT equipment, industrial electronics, and household appliances is a significant factor driving the growth of the e-waste recycling market. Increasing adoption of smartphones, laptops, electric vehicles, smart home devices, and connected technologies has significantly accelerated the volume of obsolete electronic products globally, creating strong demand for efficient recycling and material recovery solutions. Governments, manufacturers, and environmental agencies are increasingly implementing sustainability initiatives and extended producer responsibility (EPR) regulations to reduce landfill waste, recover valuable metals, and promote circular economy practices across the broader e-waste management market.

Moreover, several global electronics manufacturers expanded investments in closed-loop recycling programs and sustainable material recovery initiatives to strengthen supply chain resilience and reduce dependence on virgin raw materials. For instance, in January 2026, TÜV Rheinland launched a new closed-loop recycled material verification program tailored for large and complex industrial supply chains. Developed in accordance with ISO 14021, ISO 22095, and EN 15343 standards, the initiative provides a transparent and traceable system covering the full recycling lifecycle, from waste collection and processing to the incorporation of recycled materials into new products. The third-party verification framework has already been adopted by several electronics supply chain partners through a pilot project led by TÜV Rheinland, involving multiple specialized recyclers handling diverse material streams.

The e-scrap recycling market faces significant challenges due to high capital investment requirements for advanced recycling facilities, complex material recovery processes, and inadequate waste collection infrastructure in several developing regions. E-waste streams often contain mixed materials, hazardous substances, and non-standardized product designs, making dismantling, sorting, and recycling operations technically challenging and labor-intensive. In addition, informal recycling activities and unregulated disposal practices in certain countries create inefficiencies in material recovery and reduce the availability of recyclable waste for organized recyclers.

Market Concentration & Characteristics

The electronic waste recycling market is moderately fragmented, with the presence of global recycling companies, environmental service providers, metal recovery firms, waste management companies, and specialized e-waste processing operators competing alongside regional recyclers and refurbishment providers. Leading companies maintain strong market positions through integrated recycling facilities, advanced material recovery technologies, certified disposal services, and strategic partnerships with electronics manufacturers, governments, and corporate organizations. These companies offer comprehensive services including electronic asset disposition, secure data destruction, component refurbishment, battery recycling, precious metal recovery, and environmentally compliant waste processing solutions. High infrastructure investment requirements, environmental regulations, and technological complexities associated with material recovery create moderate barriers to entry in the market.

In terms of market characteristics, the industry is highly sustainability-driven and increasingly focused on resource recovery, automation, and circular economy integration. Growing pressure on governments and enterprises to reduce landfill waste, lower carbon emissions, and recover valuable raw materials from discarded electronics is significantly driving market demand. The market is witnessing increasing adoption of AI-powered sorting systems, robotic dismantling technologies, automated recycling facilities, and environmentally sustainable processing methods to improve recycling efficiency and operational scalability.

Material Insights

The metal segment dominated the market and accounted for the revenue share of 62.2% in 2025 due to the rising strategic importance of critical and rare metals used in advanced electronics and clean energy technologies. Increasing demand for materials such as cobalt, lithium, nickel, and rare earth elements essential for electric vehicles, renewable energy systems, and semiconductors is pushing recyclers to focus on efficient recovery from e-waste as a secondary supply source.

The plastic segment is anticipated to grow at the highest CAGR during the forecast period due to the increasing volume of polymer-rich components in modern electronics, including casings, connectors, and insulation materials. Growing regulatory pressure to reduce plastic waste and limit landfill dependency is pushing recyclers to recover and reprocess engineering plastics such as ABS, HIPS, and polycarbonate from e-waste streams. In parallel, advancements in polymer separation technologies such as density-based sorting, electrostatic separation, and chemical recycling are enabling higher purity outputs suitable for reuse in electronics manufacturing.

Source Insights

The IT & telecommunication segment dominated the market and accounted for the largest revenue share in 2025, driven by due to the rapid expansion and continuous upgrade cycles of digital infrastructure, including data centers, telecom networks, and enterprise IT systems. The global rollout of 5G technology is driving large-scale replacement of legacy networking equipment such as routers, switches, and base stations, generating substantial volumes of high-value e-waste. In addition, the accelerated adoption of cloud computing by enterprises is leading to frequent server refresh cycles in hyperscale and colocation data centers, increasing disposal rates of obsolete hardware.

The consumer electronics segment is expected to grow at a significant CAGR during the forecast period due to the surge in household device ownership and increasingly fragmented device ecosystems. Consumers now use multiple personal gadgets simultaneously smartphones, tablets, smart TVs, wearables, and smart home devices leading to higher cumulative disposal volumes as these products reach end-of-life. The growing popularity of Internet of Things-enabled devices is accelerating replacement cycles, as users upgrade to maintain compatibility within interconnected environments.

Recycling Process Insights

The pyrometallurgical processing segment dominated the market and accounted for the largest revenue share in 2025, driven by its capability to handle heterogeneous and contaminated e-waste streams at industrial scale, particularly printed circuit boards and metal-rich fractions that are difficult to pre-sort. High-temperature smelting enables efficient recovery of base and precious metals in a single processing route, making it attractive for large integrated recycling facilities seeking throughput optimization and operational robustness. The process is also gaining traction due to its compatibility with existing metallurgical infrastructure, allowing e-waste to be co-processed in conventional smelters, thereby reducing the need for entirely new capital-intensive setups.

The hydrometallurgical processing segment is expected to grow at a significant CAGR over the forecast period due to its superior selectivity and ability to recover high-purity metals from complex e-waste streams using aqueous chemistry-based extraction techniques. This process is particularly effective for extracting precious and critical metals from low-grade materials and finely shredded electronic scrap, where conventional methods face efficiency limitations. Its relatively lower operating temperatures and reduced energy intensity make it a more environmentally sustainable option, aligning with tightening emission standards and decarbonization goals across the recycling industry.

Regional Insights

North America electronic waste recycling held a significant share in the global market in 2025, driven by the rapid expansion of hyperscale data centers and enterprise IT infrastructure modernization, which generate large volumes of high-specification electronic scrap requiring advanced recycling solutions. The presence of established IT asset disposition (ITAD) ecosystems and certified recycling networks supports efficient collection and processing.

U.S. Electronic Waste Recycling Market Trends

The electronic waste recycling market in the U.S. is expected to grow significantly at a CAGR of 9.5% from 2026 to 2033, due to state-level policy fragmentation that encourages localized innovation in recycling models, alongside a mature secondary materials market that integrates recycled outputs into domestic manufacturing. The growing volume of end-of-life consumer appliances and high penetration of smart home technologies are also contributing to diversified e-waste streams.

Europe Electronic Waste Recycling Market Trends

The electronic waste recycling market in Europe dominated the global market with the largest revenue share of 35.0% in 2025 is anticipated to register considerable growth from 2026 to 2033 due to the region’s strong circular economy orientation, where recycling is integrated into broader resource efficiency strategies across industries. High landfill diversion targets and advanced waste segregation infrastructure enable consistent collection of e-waste.

The UK electronic waste recycling market is expected to grow rapidly in the coming years, owing the increasing emphasis on refurbish-and-reuse models before recycling, which extends product lifecycles and creates structured downstream recycling demand for residual waste. The rise of electronics leasing and subscription-based ownership models is also generating predictable return flows of devices, improving collection efficiency.

The Germany electronic waste recycling market held a substantial market share in 2025 due to its advanced industrial base and strong integration of recycled materials into manufacturing supply chains, particularly in automotive and electronics sectors. High technological sophistication in dismantling and pre-processing operations enhances recovery rates of complex components

Asia Pacific Electronic Waste Recycling Market Trends

Asia Pacific electronic waste recycling held a significant share in the global market in 2025, due to the rapid expansion of electronics manufacturing hubs, which generate significant volumes of production scrap alongside post-consumer waste. The region’s growing investment in formal recycling zones and industrial parks is improving processing capacity and compliance standards.

The Japan electronic waste recycling market is expected to grow rapidly in the coming years, driven by high recovery efficiency requirements and advanced material separation technologies tailored for precision recycling. The country’s strong focus on resource security, due to limited domestic raw material availability, encourages intensive extraction of valuable materials from e-waste.

The China electronic waste recycling market held a substantial market share in 2025, due to large-scale industrialization of recycling operations supported by government-backed infrastructure and centralized processing facilities. The country’s dominance in electronics production leads to substantial volumes of both pre-consumer and post-consumer e-waste.

Key Electronic Waste Recycling Company Insights

Key players operating in the electronic waste recycling industry are Umicore, Glencore, Veolia, Electronic Recyclers International (ERI), Sims Limited, Aurubis AG, and Waste Management Inc. The companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In March 2026, Electronic Recyclers International (ERI) and ITOCHU Corporation entered into a strategic partnership to introduce advanced e-waste recycling and IT asset disposition (ITAD) services in Japan. The collaboration will establish ERI Japan, marking ERI’s first international expansion, with the aim of delivering high-standard recycling solutions and strengthening sustainable electronics management in the Japanese market.

-

In October 2025, Glencore’s Britannia Refined Metals has opened a sampling plant in Kent to process copper-bearing waste and recover critical minerals. The facility can handle up to 25,000 tonnes annually, supporting recycling efforts and expanding the company’s operations beyond lead refining into copper recovery.

-

In September 2025, Aurubis AG inaugurated its new U.S. facility, Aurubis Richmond, marking a significant expansion of its operations in Georgia. The site will focus on producing critical materials including copper, nickel, tin, and precious metals-resources considered vital for strengthening the American economy. These metals play a key role in supporting the growth of data centers and AI technologies, as well as advancing energy systems, high-tech manufacturing, and defense capabilities.

Key Electronic Waste Recycling Companies

The following key companies have been profiled for this study on the electronic waste recycling market

-

Attero Recycling

-

Aurubis AG

-

Boliden Group

-

Dell Inc

-

DOWA Holdings Co., Ltd.

-

Electronic Recyclers International (ERI)

-

Glencore

-

Kuusakoski

-

Paprec Group

-

Sembcorp Industries

-

Sims Limited

-

Stena Recycling

-

Umicore

-

Veolia

-

Waste Management Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weakness

Mature Players: Umicore, Glencore, Veolia, Electronic Recyclers International (ERI), Sims Limited, Aurubis AG, and Waste Management Inc.

- Expanding integrated e-waste collection, material recovery, metal refining, battery recycling, and secure electronic disposal services across industrial and consumer sectors.

- Investing in AI-enabled waste sorting, automated dismantling systems, hydrometallurgical recovery technologies, and sustainable recycling infrastructure.

- Strengthening partnerships with electronics manufacturers, municipalities, IT asset disposition providers, and automotive battery suppliers to support circular economy initiatives.

- Strong global recycling infrastructure and long-term contracts with electronics manufacturers, enterprises, and government agencies.

- Broad service portfolios covering e-waste collection, secure data destruction, precious metal recovery, battery recycling, refurbishment, and environmental compliance services.

- Extensive processing capabilities, global logistics networks, and established regulatory expertise across multiple regions.

- High capital expenditure requirements for advanced recycling and material recovery infrastructure.

- Complex recycling processes and environmental compliance obligations can increase operational costs and deployment timelines.

- Large organizational structures may reduce flexibility in adapting to rapidly changing electronics waste streams and evolving recycling technologies.

Emerging Players: DOWA Holdings Co., Ltd., Sembcorp Industries, Paprec Group, Stena Recycling

- Focusing on specialized recycling technologies for lithium-ion batteries, rare earth material recovery, and urban mining applications.

- Developing modular and automated recycling systems that improve recovery efficiency and reduce environmental impact.

- Targeting niche areas such as EV battery recycling, sustainable electronics recovery, and circular material supply chains.

- Faster innovation cycles and greater operational agility in adopting advanced recycling technologies and sustainability-focused business models.

- Strong specialization in targeted segments such as battery recycling, metal recovery optimization, and environmentally sustainable waste processing.

- Flexible service models and scalable recycling solutions attractive to regional enterprises and sustainability-focused organizations.

- Limited global operational scale and smaller recycling infrastructure networks compared to established industry leaders.

- Dependence on partnerships and third-party collection systems for broader end-to-end recycling operations.

- Lower brand visibility among multinational electronics manufacturers and large enterprise customers.

Electronic Waste Recycling Market Report Scope

Report Attribute

Details

Market size in 2025

USD 45.2 billion

Market size in 2026

USD 47.5 billion

Revenue forecast in 2033

USD 91.5 billion

Growth rate

CAGR of 9.8% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2025 - 2033

Quantitative units

Revenue in USD billion and CAGR from 2026 to 2033

Report enterprise size

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Material, Source, Enterprise Size, Recycling Process, and Region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Attero Recycling; Aurubis AG; Boliden Group; Dell Inc.; DOWA Holdings Co., Ltd.; Electronic Recyclers International (ERI); Glencore; Kuusakoski; Paprec Group; Sembcorp Industries; Sims Limited; Stena Recycling; Umicore; Veolia; Waste Management Inc.

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Electronic Waste Recycling Market Report

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global electronic waste recycling market report based on material, source, recycling process, and region.

-

Material Outlook (Revenue, USD Billion, 2021 - 2033)

-

Metal

-

Plastic

-

Glass

-

Others

-

-

Source Outlook (Revenue, USD Billion, 2021 - 2033)

-

Household Appliances

-

Consumer Electronics

-

Industrial & Commercial Equipment

-

IT & Telecommunication

-

Medical Equipment

-

Others

-

-

Recycling Process Outlook (Revenue, USD Billion, 2021 - 2033)

-

Mechanical Processing

-

Pyrometallurgical Processing

-

Hydrometallurgical Processing

-

Biometallurgical Processing

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Electronic waste recycling investment trend analysis

Analysis of funding activities, mergers & acquisitions, strategic partnerships, and investments in e-waste recycling and circular economy markets.

Evaluation of emerging recycling technology providers, battery recycling startups, and urban mining innovation ecosystems.

Identified attractive investment and partnership opportunities within the recycling value chain.

Supported market entry and acquisition targeting strategies.

Enabled understanding of innovation trends shaping the electronic waste recycling landscape.

Consumer behavior and recycling participation analysis

Assessment of consumer awareness, device disposal behavior, trade-in programs, and recycling participation rates across regions.

Analysis of incentives, take-back programs, and sustainability-driven purchasing trends.

Identified factors influencing recycling participation and collection efficiency.

Supported customer engagement and awareness campaign strategies.

Highlighted opportunities to improve formal recycling channel adoption.

Smart city and municipal e-waste management assessment

Analysis of government-led e-waste collection initiatives, smart recycling infrastructure deployments, and municipal waste digitization programs.

Evaluation of public-private partnerships supporting urban recycling ecosystems.

Identified infrastructure modernization opportunities in municipal recycling markets.

Supported strategic engagement with public-sector recycling initiatives.

Highlighted regions with increasing government investments in formal e-waste management systems.

Frequently Asked Questions About This Report

The global electronic waste recycling market size was estimated at USD 45.2 billion in 2025 and is expected to reach USD 47.5 billion in 2026.

The global electronic waste recycling market is expected to grow at a compound annual growth rate of 9.8% from 2026 to 2033 to reach USD 91.5 billion by 2033.

Europe dominated the electronic waste recycling market, accounting for 35.0% in 2025. This is attributable to the region’s strong circular-economy orientation, in which recycling is integrated into broader resource-efficiency strategies across industries.

Some key players operating in the electronic waste recycling market include Attero Recycling, Aurubis AG, Boliden Group, Dell Inc., DOWA Holdings Co., Ltd., Electronic Recyclers International (ERI), Glencore, Kuusakoski, Paprec Group, Sembcorp Industries, Sims Limited, Stena Recycling, Umicore, Veolia, Waste Management Inc.

Key factors that are driving the market growth include the rapid proliferation of consumer electronics and shortening product life cycles. Increasing penetration of smartphones, laptops, wearables, and IoT-enabled devices has led to a sharp rise in discarded electronic products.

About the Author(s)

Electronic Devices Research Team

Semiconductors & Electronics · Electronic DevicesThis report was authored by the electronic devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the electronic devices segment of the semiconductors & electronics industry. All findings are based on proprietary semiconductors & electronics databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.