- Home

- »

- Plastics, Polymers & Resins

- »

-

Plastic Resin Market Size And Trends Report, 2026-2033GVR Report cover

![Plastic Resin Market (2026 - 2033)Report]()

Plastic Resin Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product (Crystalline, Non-crystalline, Engineering Plastic, Super Engineering Plastic), By Application (Packaging, Automotive, Construction, Consumer Goods), By Region, And Segment Forecasts

Market Size, 2025

$832.9BMarket Estimate, 2026

$873.6BMarket Forecast, 2033

$1,140.3BCAGR, 2026–2033

3.9%Plastic Resin Market Summary

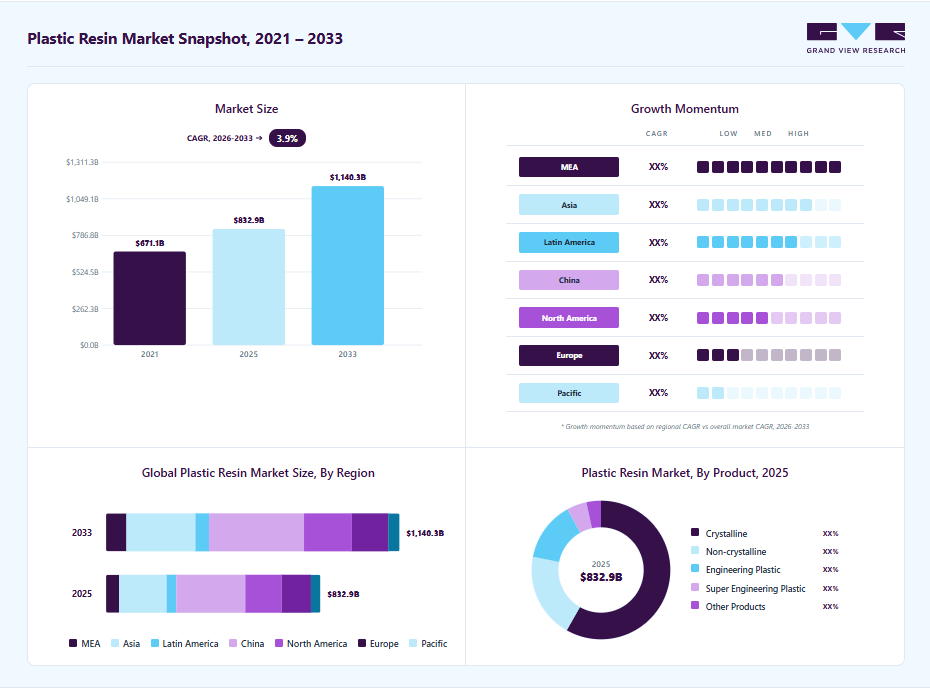

The global plastic resin market size was valued at USD 832.9 billion in 2025 and is projected to grow from USD 873.6 billion in 2026 to USD 1,140.3 billion by 2033, at a CAGR of 3.9% from 2026 to 2033. The market in Asia Pacific dominated with a revenue share of 22.1% in 2025. Capacity additions and feedstock availability are key drivers shaping the global market, as they directly influence supply, cost structures, and regional competitiveness.

Key Market Trends & Insights

- By product: Crystalline segment held the largest market share of 58.2% in 2025.

- By applications: Packaging segment held the largest market share of 41.3% in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (22.1% revenue share, 2025)

- By country: China held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 832.9 Billion

- Estimated market size in 2026: USD 873.6 Billion

- Projected market size by 2033: USD 1,140.3 Billion

- CAGR (2026-2033): 3.9%

Trends in raw material availability for the market are being shaped by feedstock supply, price volatility, and a strong push toward circular and lower-carbon inputs. Producers continue to balance ethane, LPG, and naphtha feedstock mixes to optimize crackers for cost and product slate. North American ethane-advantaged crackers produce ethylene at a lower cost, whereas Europe and parts of Asia remain more naphtha-dependent and therefore more vulnerable to fluctuations in oil prices.

")

Market Dynamics

Polymer innovation is a fundamental driver of the plastic resin market, as it directly enhances material performance and broadens application scopes across key industries, including packaging, automotive, and electronics. Innovations at the monomer and polymerization stages improve properties such as strength, recyclability, thermal resistance, and process efficiency. This evolving technological landscape enables resin producers to meet rising performance expectations while addressing sustainability and regulatory demands.

Polymer innovation involves developing new resin chemistries and processing technologies that deliver superior performance at competitive cost. Advanced catalysts and tailored polymer structures enable manufacturers to produce resins with specific attributes, such as enhanced clarity, improved mechanical strength, or better heat resistance, without significantly increasing production costs.

Innovations in sustainability, such as bio-based or chemically recycled monomers, also contribute to cost competitiveness by reducing reliance on virgin fossil-based feedstocks. These developments enable resin producers to maintain their margins while meeting evolving market demand.

Raw materials used in plastic resin manufacturing are mainly derived from hydrocarbon-based sources such as crude oil, natural gas, and coal, along with inorganic inputs including salt and sand. In the plastic resin value chain, fluctuations in these upstream feedstocks directly influence the economics of monomer and polymer production, as resin producers rely on energy-intensive cracking, polymerization, and refining processes that are closely tied to feedstock and utility prices.

For example, polyethylene resin production in North America benefits from access to relatively low-cost natural gas and ethane, supporting competitive polymer output and supply stability in the region. Future supply and demand mismatches are expected to keep global plastic resin prices volatile.

Polymer producers are particularly vulnerable, as they must manage cost fluctuations in key base polymers, such as polyethylene, polypropylene, PVC, and styrenics, which are directly tied to monomer availability and energy pricing. Crude oil price volatility, driven by supply disruptions, seasonal demand patterns, and geopolitical uncertainty, leads to fluctuating production costs across the plastic resin manufacturing ecosystem.

Market Concentration & Characteristics

The market growth stage is high, and the pace of growth is accelerating. The market exhibits fragmentation, with key players dominating the industry landscape. Major companies such as BASF SE, SABIC, Dow Inc., DuPont de Nemours, Inc., Evonik Industries AG, Sumitomo Chemical Co., Ltd, Arkema, Celanese Corporation, Eastman Chemical Company, Chevron Phillips Chemical Co., LLC, Lotte Chemical Corporation, Exxon Mobil Corporation, and others play a significant role in shaping the market dynamics. These leading players often drive innovation within the market, introducing new products, technologies, and applications to meet the evolving demands of the industry.

Innovation in the plastic resin industry is currently centered on developing sustainable and high-performance materials that balance functionality with environmental commitments. Advances in bio-based resins derived from renewable feedstocks such as sugarcane and agricultural waste are gaining traction, reducing dependency on fossil feedstocks while maintaining performance parity with conventional polymers. Enhanced recycling technologies, including chemical recycling that regenerates resins to near-virgin quality, are unlocking circular economy value and differentiating producers in competitive end-use sectors.

The plastic resin industry faces substitution pressure from specialty polymers and non-polymer materials that address specific performance gaps or sustainability goals. High-performance resins such as polysulfone, polyphenylene sulfide, and semi-aromatic polyamides serve as engineered alternatives where heat resistance, mechanical stability, or chemical durability is critical. In some applications, materials like glass, metal, wood, and ceramics are also chosen over plastics for environmental or lifecycle reasons. Bio-based and biodegradable polymers increasingly act as lower-impact substitutes for traditional resins.

Product Insights

Crystalline dominated the market across all product segments in terms of revenue, accounting for a 58.23% market share in 2025, and is forecasted to grow at a 3.8% CAGR from 2026 to 2033. Crystalline plastic resins form the backbone of global plastics consumption due to their high volume of usage and broad processing flexibility. Resins such as polyethylene, polypropylene, PET, and epoxy are widely used in packaging, containers, films, fibers, coatings, and structural applications where predictable stiffness and chemical resistance are required. Their ordered molecular structure enables faster processing cycles and consistent mechanical behavior, supporting large-scale production. Demand for these resins is closely tied to consumer goods, packaging, construction materials, and infrastructure development, making them highly sensitive to economic activity and capacity additions across major producing regions.

Engineering plastic is anticipated to grow at a substantial CAGR of 5.0% through the forecast period. Engineering plastic resins occupy the middle ground between commodity plastics and high-end specialty polymers. Resins, including nylon, PBT, PC, PU, PPO, and related PA, are chosen for applications that require higher strength, heat resistance, and long-term reliability. They are widely used in automotive systems, electrical and electronic components, industrial equipment, and durable consumer products. Demand for engineering resins is growing as the adoption of vehicle electrification, automation, and higher performance requirements in compact designs increases, where predictable mechanical behavior and extended service life are crucial.

Applications Insights

Packaging dominated the market across the applications segmentation in terms of revenue, accounting for a market share of 41.32% in 2025, and is forecasted to grow at a 4.0% CAGR from 2026 to 2033. Packaging is the largest single application that pulls resin demand across multiple supply chains. Brands, retailers, and converters require consistent volumes of low-cost, processable resins for a wide range of applications, including primary food packaging, transportation, and protective packaging. That consistent, high-volume pull shapes where producers allocate capacity and how c ompounders formulate grades for barrier, sealability, or stiffness.

Agriculture is expected to expand at a substantial CAGR of 5.4% through the forecast period. Agricultural applications generate continuous, season-timed resin demand as farmers and agri-businesses invest in productivity and water efficiency solutions. Drivers include the need to increase yields and reduce post-harvest losses through the use of protective films, irrigation systems, and durable containers. LDPE and LLDPE films are heavily utilized for mulching, greenhouse covers, and silage wraps due to their film-forming and UV resistance properties.

Regional Insights

The region’s resin landscape is increasingly shaped by large, country-level upstream capacity additions and feedstock economics, rather than downstream demand growth. India is emerging as a key center for upstream growth. Government-led programs such as PCPIRs, plastic parks, and incentive schemes are supporting multiple greenfield cracker and monomer projects. These investments are expanding domestic ethylene, propylene, and PVC capacity, gradually reducing structural import dependence.

China Plastic Resin Market Trends

The plastic resin market in China held the largest share, accounting for 44.70% of the revenue in 2025, and is expected to grow at the fastest CAGR of 3.9% over the forecast period, driven by continued refinery and petrochemical investment, as well as state-backed capacity expansions. The production of primary feedstocks, such as ethylene and propylene, is large-scale and increasingly integrated with refining, which keeps supply growth supply-led rather than demand-pulled. According to the National Bureau of Statistics of China, ethylene output in May 2024 was 2.57 million tons, underscoring the country’s massive upstream throughput that helps explain why resin exports and inter-regional shipments originate from China’s integrated complexes.

North America Plastic Resin Market Trends

The plastic resin market in North America is anchored by a large, feedstock-driven petrochemical complex centered on the U.S. Gulf Coast. Cheap and abundant natural gas liquids, particularly ethane from shale plays, provide U.S. crackers with a cost advantage for ethylene and downstream PE production. This feedstock strength supports large-scale capacity additions, export-oriented polymer flows, and a cluster of integrated producers that schedule resin output to match global demand windows. According to the U.S. Energy Information Administration, U.S. ethane production was forecast to average about 2.8 million barrels per day in both 2024 and 2025, supporting higher domestic ethane consumption and rising exports.

The U.S. plastic resin market remains one of the world’s largest producers of primary plastic resins, underpinned by competitive feedstock economics from abundant shale gas. Ethylene and propylene production along the U.S. Gulf Coast, supported by low-cost ethane and propane, drives domestic PE (PE), PP (PP), and PVC resin output more than end-market demand conditions. Polyolefins dominate the supply base, with PE and PP making up a significant share of primary resin production and setting the regional pricing tone. According to the American Chemistry Council, total U.S. resin production increased in 2024 by approximately 5% across key thermoplastics from 2023, including PE and high-density grades, reflecting continued upstream capacity utilization and modest supply growth.

Europe Plastic Resin Market Trends

The plastic resin market in Europe is defined by high energy and feedstock costs, regulatory burden, and ongoing capacity rationalization. Unlike shale-rich regions, much of Europe’s polymer production relies on naphtha feedstock and imported intermediates, which increases variable costs when oil prices and carbon costs rise. Producers have responded with plant shutdowns and deferrals, and recent industry studies show material capacity reductions announced across 2023 and 2024, which tighten local availability for certain polymers and push more trade flows toward import reliance.

Key Plastic Resin Company Insights

The industry is highly competitive, with several key players dominating the landscape. Major companies include BASF SE, SABIC, Dow Inc., DuPont de Nemours, Inc., Evonik Industries AG, Sumitomo Chemical Co., Ltd, Arkema, Celanese Corporation, Eastman Chemical Company, Chevron Phillips Chemical Co., LLC, Lotte Chemical Corporation, Exxon Mobil Corporation, Formosa Plastics Corporation, Covestro AG, Toray Industries, Inc., Mitsui & Co. Plastics Ltd., TEIJIN LIMITED, INEOS Group, Eni S.p.A., LG Chem, LANXESS AG, CHIMEI Corporation, Huntsman International LLC, and LyondellBasell Industries Holdings B.V. The industry is characterized by a competitive landscape with several key players driving innovation and market growth. Major companies in this sector are investing heavily in research and development to enhance the performance, cost-effectiveness, and sustainability of their products.

Key Plastic Resin Companies:

The following key companies have been profiled for this study on the plastic resin market

- BASF SE

- SABIC

- Dow

- DuPont de Nemours, Inc.

- Evonik Industries AG

- Sumitomo Chemical Co., Ltd.

- Celanese Corporation

- Eastman Chemical Company

- Chevron Phillips Chemical Co., LLC

- LOTTE Chemical Corporation

- Exxon Mobil Corporation

- Formosa Plastics Corporation

- TORAY INDUSTRIES, INC.

- MITSUI & CO. LTD

- TEIJIN LIMITED

- LG Chem

- Avient Corporation

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: BASF SE; SABIC; Dow Inc.; DuPont de Nemours, Inc.; Sumitomo Chemical Co. Ltd. - Expansion of product facilities

- Strong product portfolio

- Research and Development initiatives

- Vast geographical presence which ensures product availability and accessibility

- Strong financial performance

- Increased focus on merger and acquisitions

- Limited focus on the small sized customer based

Emerging Players: Evonik Industries AG; Celanese Corporation; Eastman Chemical Company; LANXESS AG - Strong foothold in the local market catering to customized client demand

- High focus on product distribution

- Strong small and medium size client base

- Area specific monopoly

- Limited geographical presence

- Limited financial capability for global expansion

Recent Developments

-

In May 2025, Aster Chemicals and Energy reached an agreement to acquire Chevron Phillips Singapore Chemicals (owner of a 400 kilotons per year HDPE plant). While a derivatives asset, the transaction signals a reshaping of the portfolio around petrochemical assets and can indirectly affect local monomer feedstock demand and commercial flows in Southeast Asia.

-

In January 2025, Howard Energy Partners closed the acquisition of EPIC Midstream’s ethylene pipeline system. The purchase secures a strategic midstream asset that transports ethylene monomer from Gulf Coast crackers to storage hubs, improving logistics for downstream resin manufacturers and merchant monomer traders.

Plastic Resin Market Report Scope

Report Attribute

Details

Market size in 2025

USD 832.9 billion

Estimated market size in 2026

USD 873.6 billion

Projected market size by 2033

USD 1,140.3 billion

Growth rate

CAGR of 3.9% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Market Segmentation

Product, applications, region

Regional scope

North America; Europe; China, Asia Pacific; Central & South America; Middle East & Africa

Country Scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Poland; Spain; India; Japan; South Korea; Singapore; Malaysia; Thailand; Indonesia; Vietnam; Australia; Brazil; Argentina; Saudi Arabia; UAE; Oman

Key companies profiled

BASF SE; SABIC; Dow Inc.; DuPont de Nemours, Inc.; Evonik Industries AG; Sumitomo Chemical Co., Ltd; Celanese Corporation; Eastman Chemical Company; Chevron Phillips Chemical Co., LLC; Lotte Chemical Corporation; Exxon Mobil Corporation; Formosa Plastics Corporation; Toray Industries, Inc.; MITSUI & CO. LTD; TEIJIN LIMITED; LG Chem; Avient Corporation

Customization scope

Free report customization (equivalent to up to 8 analyst working days) with purchase. Addition or alteration to country, regional & segment scope

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Plastic Resin Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the plastic resin market report based on product, applications, and region:

-

Product Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Crystalline

-

Epoxy

-

Polyethylene

-

Polyethylene Terephthalate (PET)

-

Polypropylene

-

-

Non-crystalline

-

Polyvinyl Chloride (PVC)

-

Polystyrene (PS)

-

Acrylonitrile butadiene styrene (ABS)

-

Polymethyl Methacrylate (PMMA)

-

-

Engineering Plastic

-

Nylon

-

Polybutylene Terephthalate (PBT)

-

Polycarbonate (PC)

-

Polyurethane (PU)

-

Polyphenylene Oxide (PPO)

-

Polyamide

-

-

Super Engineering Plastic

-

Polyphenylene Sulfide (PPS)

-

Polyether Ether Ketone (PEEK)

-

Polysulfone (PSU)

-

Polyphenylsulfone (PPSU)

-

Liquid Crystal Polymer (LCP)

-

-

Other Products

-

-

Applications Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Packaging

-

Food

-

Beverage

-

Medical

-

Retail

-

Other packaging applications

-

-

Automotive

-

Construction

-

Electrical & Electronics

-

OA Equipment and Home Appliances

-

Electronic Materials

-

Other E&E applications

-

-

Logistics

-

Consumer Goods

-

Textiles & Clothing

-

Clothing

-

Industrial use

-

Other textile & clothing applications

-

-

Furniture & Bedding

-

Agriculture

-

Medical Devices

-

Other applications

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Poland

-

Spain

-

-

China

-

Asia

-

India

-

Japan

-

South Korea

-

Singapore

-

Malaysia

-

Thailand

-

Indonesia

-

Vietnam

-

Australia

-

-

Pacific

-

Central & South America

-

Brazil

-

Argentina

-

-

Middle East and Africa

-

Saudi Arabia

-

UAE

-

Oman

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cross-segmentation

The report was customized to provide product-by-application cross-segmentation for the plastic resins market, covering key resin types such as PE, PP, PVC, PET, PS, ABS, and engineering plastics across applications including packaging, automotive, construction, electrical & electronics, consumer goods, and industrial products.

Helped the client understand which resin types were most relevant for each application, identify high-growth product-application combinations, and prioritize commercially attractive demand pockets. Trade Analysis

A customized trade analysis section was incorporated to assess import-export flows of major plastic resins across target countries, including trade value, trade volume, key origin and destination markets, dependency on imports, export competitiveness, and potential tariff or logistics implications.

Provided the client with a clear view of supply-demand gaps, import reliance, regional sourcing opportunities, and trade-driven market risks affecting resin availability and pricing.

Supplier-Buyer Mapping

The study included supplier-buyer mapping across the plastic resins value chain, identifying key resin producers, compounders, distributors, converters, packaging manufacturers, OEMs, and major end-use buyers across priority applications.

Enabled the client to map the market ecosystem, identify potential suppliers and customers, assess partnership opportunities, and strengthen sales targeting and procurement strategy.

Frequently Asked Questions About This Report

Asia Pacific dominated with a 22.1% revenue share in 2025.

Which applications segment dominated the plastic resin market?

The global plastic resin market is expected to grow at a compound annual growth rate of 3.9% from 2026 to 2033 to reach USD 1,140.3 billion by 2033.

The global plastic resin market size was estimated at USD 832.9 billion in 2025 and is expected to reach USD 873.6 billion in 2026.

Some key players operating in the plastic resin market include BASF SE, SABIC, Dow Inc., DuPont de Nemours, Inc., Evonik Industries AG, Sumitomo Chemical Co., Ltd, Arkema, Celanese Corporation, Eastman Chemical Company, Chevron Phillips Chemical Co., LLC, Lotte Chemical Corporation, and Exxon Mobil Corporation.

Capacity additions and feedstock availability are key drivers shaping the global plastic resin market, as they directly influence supply, cost structures, and regional competitiveness.

Crystalline dominated the market across all product segments in terms of revenue, accounting for a 58.2% market share in 2025, and is forecasted to grow at a 3.8% CAGR from 2026 to 2033.

About the Author(s)

Plastics, Polymers & Resins Research Team

Bulk Chemicals · Plastics, Polymers & ResinsThis report was authored by the plastics, polymers & resins research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the plastics, polymers & resins segment of the bulk chemicals industry. All findings are based on proprietary bulk chemicals databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.