- Home

- »

- Medical Devices

- »

-

Embolotherapy Market Size & Share, Industry Report, 2033GVR Report cover

![Embolotherapy Market Size, Share & Trends Report]()

Embolotherapy Market (2025 - 2033) Size, Share & Trends Analysis Report By Product (Embolization Coils, Embolic Agents, Flow Diverters, Detachable Balloons, Vascular Plugs/Plug Systems, Support Devices), By Application, By End Use, By Region, And Segment Forecasts

- Report Summary

- Table of Contents

- Segmentation

- Methodology

- Download FREE Sample

-

Download Sample Report

Download Sample Report

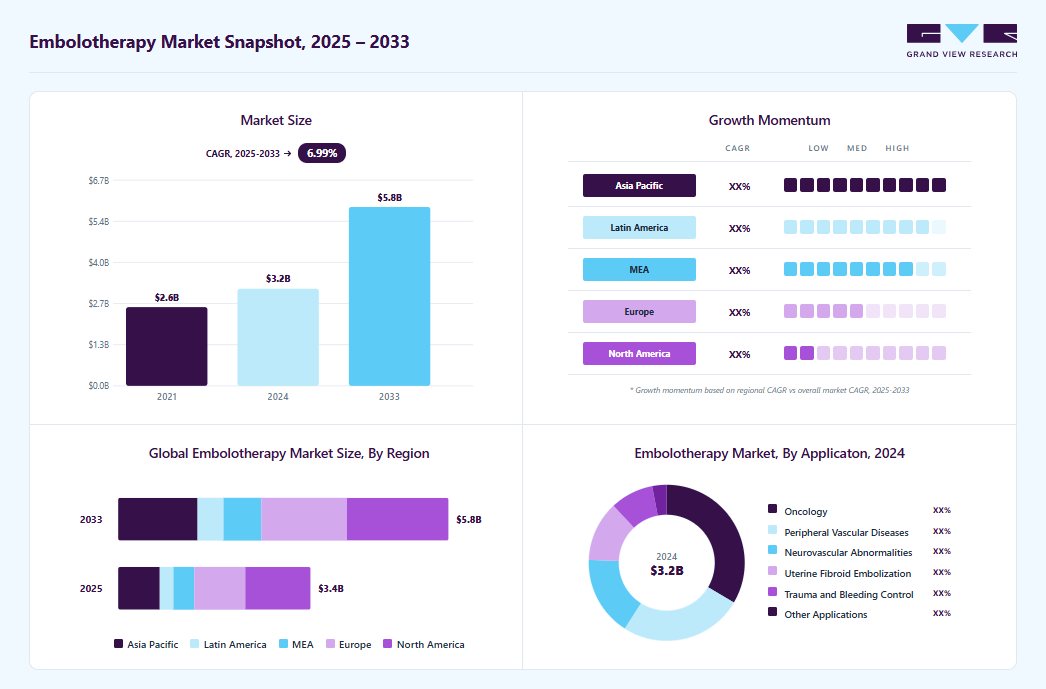

Market Size, 2024

$3.2BMarket Estimate, 2025

$3.4BMarket Forecast, 2033

$5.8BCAGR, 2025–2033

7.0%Embolotherapy Market Summary

The global embolotherapy market size was estimated at USD 3.16 billion in 2024 and is projected to reach USD 5.82 billion by 2033, growing at a CAGR of 6.99% from 2025 to 2033. The market is primarily driven by the rising prevalence of cancer, vascular disorders, and trauma cases, which fuel demand for minimally invasive treatment options.

Key Market Trends & Insights

- North America dominated the embolotherapy market with the largest revenue share of 34.36% in 2024.

- The embolotherapy market in the U.S. accounted for the largest market revenue share of 79.93% in North America in 2024.

- Based on product, the embolic agents segment led the market with the largest revenue share of 34.26% in 2024.

- Based on application, the oncology segment led the market with the largest revenue share of 33.51% in 2024.

- Based on end use, the hospitals and clinics segment led the market with the largest revenue share of 64.86% in 2024.

Market Size & Forecast

- 2024 Market Size: USD 3.16 Million

- 2033 Projected Market Size: USD 5.82 Billion

- CAGR (2025-2033): 6.99%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Technological advancements in embolic agents, such as drug-eluting beads, liquid embolic, and bioresorbable microspheres, along with innovative delivery devices like microcatheters and flow diverters, have improved procedural precision, safety, and clinical outcomes.

Moreover, increasing patient preference for less invasive procedures with shorter recovery times, expanding healthcare infrastructure in emerging markets, and supportive regulatory frameworks further accelerate adoption. Together, these factors create sustained growth opportunities and reinforce the market’s upward trajectory.

")

The global rise in cancer treatments, trauma cases, and vascular disorders has amplified the need for advanced embolotherapy solutions. Hospitals, clinics, and interventional radiology centers are witnessing growing procedure volumes, creating continuous demand for effective embolic agents and delivery systems. This trend places additional pressure on healthcare facilities to adopt innovative, minimally invasive techniques that improve patient outcomes while maintaining safety and efficiency. To meet these needs, providers are increasingly turning to next-generation embolotherapy technologies that enable faster procedures, greater precision, and reduced complications.

For instance, in June 2025, Penumbra, Inc. announced that the U.S. Food and Drug Administration (FDA) had cleared and launched the Ruby XL System, the longest, largest, and softest coil available on the market. The Ruby XL System is designed to enable physicians to perform more efficient embolizations, potentially decreasing radiation exposure and improving outcomes-particularly in procedures involving large vessels and high-flow embolizations.

The rising prevalence of cancer and vascular diseases is a major driver of the embolotherapy industry because these conditions often require targeted, minimally invasive treatments to control bleeding, reduce tumor size, or manage abnormal blood vessels. Patients with liver cancer frequently undergo transarterial embolization to block the blood supply to tumors, slowing their growth while preserving surrounding healthy tissue. Arteriovenous malformations or gastrointestinal bleeding cases are increasingly managed with embolotherapy, as it provides an effective alternative to open surgery with shorter recovery times and fewer complications. According to WHO, the estimated number of new cases of liver and intrahepatic bile duct cancers among both sexes (ages 0-85+) is projected to increase from 2022 to 2040, as shown in the data frame and illustrated in the graph below.

Technological advancements in embolic agents and devices are a key driver of the embolotherapy industry as they improve treatment precision, safety, and patient outcomes. Modern innovations such as drug-eluting beads, bioresorbable microspheres, liquid embolics, and image-guided microcatheter systems allow for highly targeted embolization with minimal damage to surrounding tissues. These innovations expand the scope of embolotherapy beyond traditional oncology to include trauma management, vascular malformations, and gastrointestinal bleeding. As procedures become more effective, less invasive, and widely adopted, the demand for advanced embolic technologies continues to accelerate market growth.

In addition, recent product launches, approvals, and commercial availability indicate that the market is poised for significant growth potential during the forecast period. For instance, in February 2025, Guerbet announced that the U.S. Food and Drug Administration (FDA) had granted Breakthrough Device designation to LIPIOJOINT, an innovative transient liquid embolic agent developed to help relieve pain and improve mobility in patients suffering from knee osteoarthritis (KOA).

The rising incidence of trauma and hemorrhage cases is a significant driver for the embolotherapy industry because embolization provides a minimally invasive, life-saving solution for controlling internal bleeding. Patients with traumatic injuries, gastrointestinal hemorrhages, or postpartum bleeding often require rapid, targeted intervention, and embolotherapy allows clinicians to occlude bleeding vessels without open surgery. As trauma rates and hemorrhagic complications increase globally, demand for effective embolization procedures, advanced embolic agents, and support devices grows, directly expanding the market.

Key Opinions of Leaders

Company Name

KOLs

KOL Details

Sirtex

““We are thrilled for the launch of the LAVA Study, which has the potential to lead to the first FDA-approved liquid embolic for a PV application in the U.S.” “We are proud to partner with BlackSwan on its clinical journey and look forward to the potential expansion of treatment options in the endovascular field for interventionalists and patients in need.”

Kevin Smith, Chief Executive Officer of Sirtex

Sirtex

"The approval and availability of LAVA is especially meaningful to our team because it is addressing previously unmet needs in vascular medicine, with the potential to create a significant impact on patients’ lives.” “We are delighted to expand our Sirtex product portfolio with this treatment milestone that directly furthers our mission to improve the quality and longevity of patient lives through innovative medical solutions, and we thank everyone who played a role in achieving it.”

Matt Schmidt, Chief Commercial Officer of Sirtex

Market Concentration & Characteristics

The degree of innovation in the embolotherapy industry is expected to be high and continuously evolving. This market has seen significant advances driven by technological developments, new materials, and improved delivery methods. For instance, in January 2025, NEXTBIOMEDICAL CO., LTD, an innovative medical device company listed on the KOSDAQ in South Korea, announced the receipt of Investigational Device Exemption (IDE) approval from the U.S. Food and Drug Administration (FDA) for its clinical trial named "RESORB," featuring the Nexsphere-F. This fast-resorbable embolic microsphere is designed to reduce pain in patients with knee osteoarthritis. The upcoming multi-center trial in the United States represents a crucial step toward obtaining market approval and signifies a major milestone in the company's global expansion efforts.

Regulations play a pivotal role in shaping the embolotherapy industry by ensuring the safety, efficacy, and quality of embolic agents and delivery devices. Global and regional authorities, including the U.S. FDA, European Medicines Agency (EMA), and other regulatory bodies, enforce rigorous standards for clinical validation, manufacturing practices, and post-market surveillance. These requirements drive companies to invest in extensive research, robust clinical trials, and continuous innovation to secure approvals and maintain compliance. As a result, regulations not only safeguard patient outcomes and minimize risks such as non-target embolization but also influence purchasing decisions by hospitals and clinics, creating sustained demand for clinically proven and technologically advanced embolotherapy solutions.

Mergers and acquisitions are increasingly shaping the embolotherapy industry, enabling companies to expand their product portfolios, access innovative technologies, and strengthen market presence. Such strategic activities accelerate growth by combining expertise, enhancing R&D capabilities, and broadening geographic reach. For instance, in June 2025, Balt announced the acquisition of its Canadian distributor, Yocan Medical Systems Ltd., which has been operating as Balt Canada Ltd. since June 2, 2025. This direct presence signifies a new milestone in Balt’s development in Canada and demonstrates its commitment to global growth and expansion.

The end-user concentration in the embolotherapy industry primarily focuses on hospitals, followed by ambulatory surgical centers, specialized interventional radiology centers, oncology clinics, and trauma care units. Hospitals account for the largest share due to high patient volumes, complex procedures, and the need for advanced minimally invasive treatments, driving consistent demand for embolic agents and delivery systems. Specialized clinics and trauma centers are emerging as key contributors as they increasingly adopt advanced embolotherapy technologies to improve clinical outcomes and procedural efficiency. This concentration underscores the critical role of embolization in modern healthcare across diverse clinical settings.

Product Insights

The embolic agents segment accounted for the largest market revenue share in 2024, due to their central role in minimally invasive procedures for treating cancer, vascular disorders, and trauma-related hemorrhages. These agents, including microspheres, liquid embolics, and coils, are essential for effectively occluding blood vessels, controlling bleeding, and delivering targeted therapy to tumors or malformations. The increasing prevalence of liver cancer, arteriovenous malformations, and gastrointestinal bleeding, coupled with the growing preference for minimally invasive interventions, has driven consistent demand. Continuous innovations in embolic materials and delivery technologies, which improve precision, safety, and procedural outcomes, further strengthen this segment’s market dominance.

The flow diverters segment is expected to register at the fastest CAGR from 2025 to 2033, due to the increasing prevalence of intracranial aneurysms and complex vascular disorders, coupled with growing adoption of minimally invasive neurovascular interventions. Continuous technological advancements improving device flexibility, deliverability, and safety further drive demand, positioning flow diverters as a rapidly expanding segment in the embolotherapy industry.

Application Insights

The oncology segment accounted for the largest market revenue share in 2024, because embolization is widely used to treat liver, kidney, and other solid tumors by blocking the tumor's blood supply and delivering targeted therapies. The high prevalence of cancer, increasing adoption of minimally invasive procedures, and favorable clinical outcomes drive consistent demand in this segment, making oncology the dominant application area for embolotherapy worldwide. According to the WHO, the global number of cancer patients is projected to rise from 20.0 million in 2022 to 35.3 million by 2050, reflecting a significant increase in disease burden and driving greater demand for advanced treatment options, including embolotherapy.

The uterine fibroid embolization segment is anticipated to grow at the fastest CAGR during the forecast period, due to increasing awareness of minimally invasive treatments for fibroids, rising prevalence of uterine fibroids among women of reproductive age, and the benefits of shorter recovery times and reduced complications compared to traditional surgery. Growing adoption of UFE procedures across hospitals and specialized clinics is driving rapid market expansion for this segment.

End Use Insights

The hospitals and clinics segment led the market with the largest revenue share of 64.86% in 2024 due to high patient volumes, availability of advanced interventional radiology infrastructure, and the ability to perform complex procedures across oncology, vascular, and trauma indications. Their central role in delivering minimally invasive treatments drives consistent demand for embolic agents, support devices, and related technologies.

The ambulatory surgical centers segment is expected to witness at the fastest CAGR over the forecast period. The increasing shift toward outpatient minimally invasive procedures, rising patient preference for shorter recovery times, and expanding adoption of advanced embolization technologies in these centers. These centers offer cost-effective care, greater procedural efficiency, and flexible scheduling, making them attractive for both patients and healthcare providers. In addition, the growing focus on reducing hospital congestion and improving patient throughput further accelerates the adoption of embolotherapy in ambulatory settings.

Regional Insights

North America dominated the embolotherapy market with the largest revenue share of 34.36% in 2024. The growth is driven by the high prevalence of cancer, vascular disorders, and trauma cases, along with the widespread adoption of minimally invasive procedures. The U.S. leads the region due to advanced healthcare infrastructure, strong regulatory oversight from agencies such as the FDA, and favorable reimbursement policies that support the use of innovative embolic agents and devices in hospitals and specialized clinics.

U.S. Embolotherapy Market Trends

The embolotherapy market in the U.S. accounted for the largest market revenue share of 79.93% in North America in 2024, driven by technological advancements, rising prevalence of cancer and vascular disorders, and increasing preference for minimally invasive procedures. Embolotherapy is widely employed for treating conditions such as arteriovenous malformations (AVMs), hypervascular tumors, peripheral hemorrhages, and other vascular anomalies. The growing incidence of stroke, cancer, and traumatic injuries has boosted demand for effective embolization therapies. Key players in the U.S. market with FDA-approved products include Medtronic, Johnson & Johnson, Boston Scientific Corporation, and Terumo. In addition, innovations in embolic agents, including cyanoacrylate-based, non-adhesive, and ethylene vinyl alcohol copolymer materials, have enhanced procedural safety and efficacy. The increasing trend toward outpatient procedures and adoption of embolotherapy in ambulatory surgical centers is further driving market growth by offering cost-effective and convenient treatment options for patients.

Europe Embolotherapy Market Trends

The embolotherapy market in Europe is witnessing significant growth, driven by increasing prevalence of cancer and vascular disorders, a well-established healthcare infrastructure, and the rising adoption of minimally invasive procedures. Demand for advanced embolic agents, flow diverters, and support devices is growing across the region, supported by investments in state-of-the-art interventional radiology facilities. Countries such as Germany, France, the UK, and the Nordics are actively upgrading hospital infrastructure and adopting innovative embolotherapy technologies to enhance procedural precision, patient safety, and clinical outcomes, reinforcing Europe’s strong position in the market.

The UK embolotherapy market is largely driven by the increasing prevalence of cancer and vascular disorders, the growing adoption of minimally invasive procedures, and continuous technological advancements in embolic agents and delivery devices. Healthcare providers are guided by stringent regulatory standards and clinical best practices that emphasize safety, efficacy, and procedural precision. Hospitals and specialized interventional radiology centers are investing in advanced embolotherapy systems and support devices to meet these standards, improve patient outcomes, and maintain compliance with national healthcare guidelines.

Asia Pacific Embolotherapy Market Trends

The embolotherapy market in the Asia Pacific is anticipated to grow at the fastest CAGR from 2025 to 2033. Fueled by expanding healthcare infrastructure, rising patient volumes, and increasing adoption of minimally invasive procedures. The growing prevalence of cancer, vascular disorders, and trauma cases drives strong demand for embolotherapy across hospitals, clinics, and specialized interventional radiology centers. Governments in countries such as India, China, Japan, and Thailand are actively investing in healthcare modernization, enhancing access to advanced embolic agents, delivery devices, and state-of-the-art interventional facilities, which aligns with international standards and supports market expansion.

The China embolotherapy market is witnessing significant growth, driven by the rising prevalence of liver cancer, gastrointestinal bleeding, and vascular disorders. Technological advancements in embolic agents and delivery systems are improving procedure efficacy and safety, expanding clinical applications. Increasing investments in healthcare infrastructure and the growing availability of interventional radiology services enhance access to embolotherapy treatments nationwide. These factors collectively position China as a rapidly expanding market with strong future growth potential.

Latin America Embolotherapy Market Trends

The embolotherapy market in Latin America is growing moderately, supported by rising incidences of liver cancer, gastrointestinal bleeding, and vascular disorders. Expanding adoption of minimally invasive procedures, along with improved healthcare infrastructure in countries like Brazil and Mexico, is driving demand. The increasing availability of advanced embolic agents and growing medical tourism are further fueling market expansion. However, uneven access to specialized interventional radiology services across rural areas continues to restrain widespread adoption.

Middle East Africa Embolotherapy Market Trends

The embolotherapy market in the Middle East and Africa is witnessing significant growth driven by the rising prevalence of cancer, trauma, and gastrointestinal bleeding cases. Increasing investments in healthcare infrastructure, coupled with improving access to minimally invasive procedures, are supporting adoption. Favorable government initiatives and the expansion of interventional radiology services are further boosting demand. However, limited specialist availability and higher treatment costs in certain regions remain key challenges to wider market penetration.

Key Embolotherapy Company Insights

The embolotherapy industry is highly fragmented, with both global and regional players. As companies intensify efforts to capture greater market share, competition is expected to become increasingly fierce. Market participants actively pursue product launches, mergers and acquisitions, and geographic expansion strategies to strengthen their competitive position. With these strategic initiatives, the embolotherapy industry will grow significantly over the forecast period.

Key Embolotherapy Companies:

The following are the leading companies in the embolotherapy market. These companies collectively hold the largest market share and dictate industry trends.

- Medtronic

- Johnson & Johnson

- B. Braun SE

- Terumo

- Boston Scientific Corporation

- Meril

- Gem srl

- Balt

- Sirtex (BlackSwan Vascular, Inc.)

- INVAMED

- Stryker

- Penumbra

- Merit Medical Systems

- Abbott

- Acandis GmbH

- Cook Medical

Recent Developments

-

In September 2025, Penumbra Inc. announced that it had obtained CE Mark approval for its SwiftPAC neuroembolization coil. The device is now commercially available in Europe and is a component of the company’s Swift coil system.

-

In August 2025, Instylla, Inc., a privately held company specializing in innovative resorbable embolics for peripheral vascular embolization, announced that it had received premarket approval (PMA) from the U.S. Food and Drug Administration (FDA) for its flagship product, Embrace Hydrogel Embolic System. Embrace HES is approved for embolizing hypervascular tumors in peripheral arteries measuring 5mm or less.

-

In June 2025, Embolization, Inc. obtained 510(k) clearance from the U.S. Food and Drug Administration (FDA) for its Nitinol Enhanced Device (NED). The NED is designed as a vascular embolization tool for use in arterial and venous embolization within the peripheral vasculature.

-

In June 2025, Penumbra, Inc. announced that the U.S. Food and Drug Administration (FDA) had cleared and launched the Ruby XL System, the longest, largest, and softest coil available on the market. The Ruby XL System is designed to enable physicians to perform more efficient embolizations, potentially decreasing radiation exposure and improving outcomes-particularly in procedures involving large vessels and high-flow embolizations.

-

In July 2025, Medtronic announced the enrollment of the first patient in the Peripheral Onyx Liquid Embolic (PELE) clinical trial. This study aims to assess the safety and efficacy of the Onyx Liquid Embolic System (LES) for the embolization of arterial hemorrhages in the peripheral vasculature.

-

In June 2025, Balt announced the acquisition of its Canadian distributor, Yocan Medical Systems Ltd., which has been operating as Balt Canada Ltd. since June 2, 2025. This direct presence signifies a new milestone in Balt’s development in Canada and demonstrates its commitment to global growth and expansion.

-

In February 2025, Guerbet announced that the U.S. Food and Drug Administration (FDA) had granted Breakthrough Device designation to LIPIOJOINT, an innovative transient liquid embolic agent developed to help relieve pain and improve mobility in patients suffering from knee osteoarthritis (KOA).

-

In March 2024, CERENOVUS, a division of Johnson & Johnson MedTech, announced the launch of the TRUFILL n-BCA Liquid Embolic System Procedural Set. This new offer expands CERENOVUS’s hemorrhagic stroke portfolio by providing a comprehensive procedural set that includes two configuration options and all necessary accessories for preparing and delivering the TRUFILL n-BCA Liquid Embolic System. Designed to streamline procedure preparation, the set simplifies the process by consolidating essential components into a single sterilized package.

-

In July 2024, Arsenal Medical announced that the EMBO-01 clinical trial, an open-label, multicenter, prospective study of NeoCast, successfully met its primary feasibility and safety goals. The study demonstrated that NeoCast achieved predictable and well-controlled vascular occlusion, showcasing its effectiveness as a shear-responsive liquid embolic material engineered for deep distal penetration into the microvasculature.

- In October 2023, Sirtex Medical announced the commercial launch of the LAVA Liquid Embolic System, the first and only liquid embolic approved for the treatment of peripheral vascular hemorrhage.

Embolotherapy Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 3.39 billion

Revenue forecast in 2033

USD 5.82 billion

Growth rate

CAGR of 6.99% from 2025 to 2033

Base year for estimation

2024

Historical data

2021 - 2023

Forecast period

2025 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2025 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, end use,region

Regional scope

North America; Europe; Asia Pacific; Latin America; and Middle East & Africa (MEA)

Country scope

U.S.; Canada; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; Japan; China; India; Australia; Thailand; South Korea; Brazil; Mexico; Argentina; South Africa; Saudi Arabia; Kuwait and UAE.

Key companies profiled

Medtronic; Johnson & Johnson; B. Braun SE; Terumo; Boston Scientific Corporation; Meril; Gem srl; Balt; Sirtex (BlackSwan Vascular, Inc.); INVAMED; Stryker; Penumbra; Merit Medical Systems; Abbott; Acandis GmbH; Cook Medical

Customization scop

Free report customization (equivalent up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Embolotherapy Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global embolotherapy market report based on the product, application, end use, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Embolization Coils

-

Detachable Coils

-

Pushable Coils

-

-

Embolic Agents

-

Liquid Embolic Agents

-

Ethylene Vinyl Alcohol Copolymer (EVOH)

-

N-BCA (n-Butyl Cyanoacrylate)

-

N-HCA (n-Hexyl Cyanoacrylate)

-

-

Cyanoacrylates

-

Others

-

-

Microspheres

-

-

Flow Diverters

-

Detachable Balloons

-

Vascular Plugs/Plug Systems

-

Support Devices

-

Guidewires

-

Microcatheters

-

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Oncology

-

Liver Cancer (Hepatocellular carcinoma)

-

Renal Cell Carcinoma

-

Lung Cancer

-

Others

-

-

Peripheral Vascular Diseases

-

Neurovascular Abnormalities

-

Uterine Fibroid Embolization

-

Trauma and Bleeding Control

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals and Clinics

-

Ambulatory Surgical Centers

-

Other End-Use

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

Thailand

-

South Korea

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global embolotherapy market size was estimated at USD 3.16 billion in 2024 and is projected to reach USD 3.39 billion by 2025.

The global embolotherapy market is projected to grow at a CAGR of 6.99% from 2025 to 2033 to reach USD 5.82 billion by 2033.

The embolic agents segment accounted for the largest revenue share of 34.26% in the embolotherapy market in 2024 due to their central role in minimally invasive procedures for treating cancer, vascular disorders, and trauma-related hemorrhages. These agents, including microspheres, liquid embolics, and coils, are essential for effectively occluding blood vessels, controlling bleeding, and delivering targeted therapy to tumors or malformations.

Some of the key players include Medtronic, Johnson & Johnson, B. Braun SE, Terumo, Boston Scientific Corporation, Meril, Gem srl, Balt, Sirtex (BlackSwan Vascular, Inc.), INVAMED, Stryker, Penumbra, Merit Medical Systems, Abbott, Acandis GmbH, and Cook Medical.

The embolotherapy market is primarily driven by the rising prevalence of cancer, vascular disorders, and trauma cases, which fuel demand for minimally invasive treatment options.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Share this report with your colleague or friend.

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.