- Home

- »

- Clinical Diagnostics

- »

-

Endocrine Testing Market Size And Share Report, 2026-2033GVR Report cover

![Endocrine Testing Market (2026 - 2033)Report]()

Endocrine Testing Market (2026 - 2033)

Size, Share & Trends Analysis Report By Test Type (Thyroid Stimulating Hormone (TSH) Test, Testosterone Test), By Technology (Immunoassay, Sensor Technology), By End-use, By Region, And Segment Forecasts

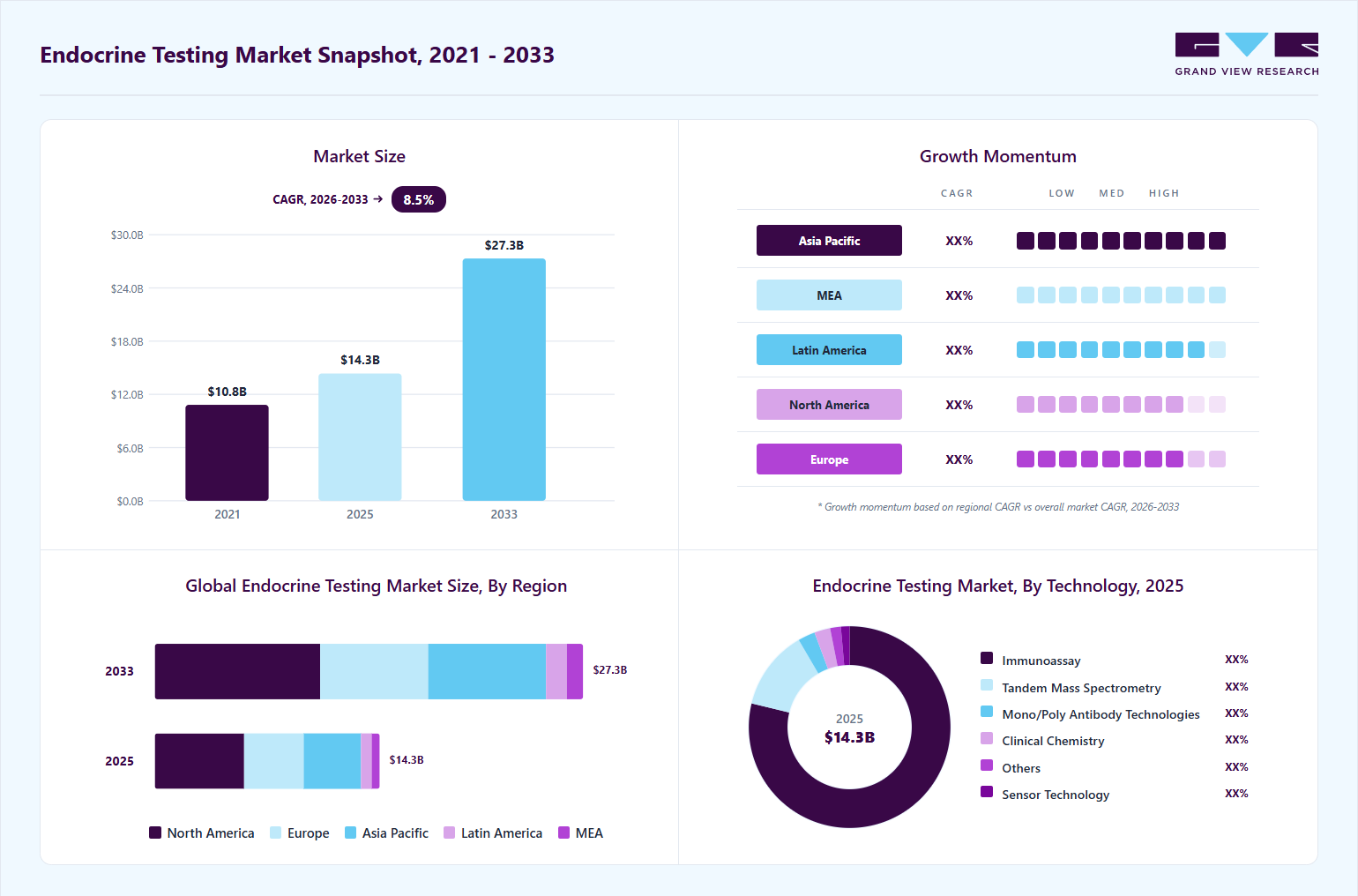

Market Size, 2025

$14.4BMarket Estimate, 2026

$15.5BMarket Forecast, 2033

$27.3BCAGR, 2026–2033

8.5%Endocrine Testing Market Summary

The global endocrine testing market size was valued at USD 14.4 billion in 2025 and is projected to grow from USD 15.5 billion in 2026 to USD 27.3 billion by 2033, at a CAGR of 8.5% from 2026 to 2033. The market in North America dominated with a revenue share of 39.7% in 2025. The market is experiencing steady growth driven by the increasing prevalence of diabetes, thyroid disorders, obesity, fertility-related conditions, and other hormone-associated diseases requiring routine diagnostic monitoring.

Key Market Trends & Insights

- By test type: Thyroid stimulating hormone segment held the largest market share of 29.7% in 2025.

- By technology: Immunoassay segment held the largest market share in 2025.

- By end-use: Commercial laboratories segment held the largest market share of 46.4% in 2025.

Regional Highlights

- Largest regional market: North America (39.7% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 14.4 Billion

- Estimated market size in 2026: USD 15.5 Billion

- Projected market size by 2033: USD 27.3 Billion

- CAGR (2026-2033): 8.5%

The endocrine testing industry’s growth is further supported by rising adoption of automated immunoassay platforms, expanding preventive healthcare awareness, and the growing integration of advanced hormone-testing technologies across hospitals, commercial laboratories, and ambulatory care centers.")

The growth of the global endocrine testing market is primarily driven by the rising burden of metabolic and hormone-related disorders, particularly diabetes, thyroid dysfunction, obesity, reproductive disorders, and adrenal abnormalities. The increasing prevalence of these conditions has significantly expanded routine hormone monitoring across hospitals, commercial laboratories, and ambulatory care settings. Thyroid stimulating hormone (TSH), insulin, cortisol, testosterone, and reproductive hormone tests are witnessing sustained demand as healthcare systems increasingly emphasize early diagnosis and long-term disease management. In parallel, changing lifestyle patterns, aging populations, obesity incidence, and stress-related endocrine disorders are accelerating testing volumes globally. The growing use of endocrine assays in fertility management and women’s health has further strengthened demand for testing for estradiol, progesterone, LH, FSH, and prolactin, particularly in urban healthcare systems with rising preventive healthcare awareness.

A major growth catalyst for the market is the rapid expansion of diabetes and obesity management programs, which continue to increase demand for insulin and metabolic hormone testing. Pharmaceutical innovation in GLP-1 therapies and obesity management has also amplified physician focus on endocrine monitoring and metabolic assessment. The increasing chronic disease burden among younger populations also supports the higher testing frequency. For instance, in June 2024, the NHS reported that diabetes cases among individuals under 40 years of age increased from 173,166 in 2022 to 216,440 in 2023, highlighting the accelerating burden of metabolic disorders and the associated rise in endocrine testing requirements. Similarly, in March 2024, Novo Nordisk received FDA approval for Wegovy (semaglutide) to reduce the risk of major adverse cardiovascular events in adults with obesity or overweight and established cardiovascular disease, reinforcing the expanding clinical importance of endocrine-linked metabolic management. Such developments are increasing long-term monitoring requirements across endocrine diagnostic laboratories globally.

Technological advancements in hormone testing platforms are also contributing significantly to market expansion. Laboratories are increasingly adopting highly automated immunoassay systems and tandem mass spectrometry technologies to improve analytical sensitivity, turnaround time, and testing throughput. The shift toward precision endocrinology and reproductive diagnostics has increased demand for highly specific hormone assays that support complex clinical decisions. In addition, healthcare providers are expanding reproductive endocrinology testing menus due to increasing infertility treatment volumes and delayed pregnancies in developed and developing markets. Siemens Healthineers launched its Anti-Müllerian Hormone (AMH) Assay in March 2024 as an expansion of its reproductive endocrinology testing portfolio, designed to assist physicians in evaluating ovarian reserve for IVF-related treatment decisions. Such product innovations continue to strengthen advanced endocrine testing capabilities across commercial laboratories and hospital diagnostic centers.

Another key market driver is the increasing integration of connected endocrine monitoring technologies and biomarker-based disease management solutions. While traditional laboratory testing remains central to endocrine diagnostics within the market scope, healthcare providers are increasingly integrating continuous metabolic monitoring with laboratory-based endocrine assessments to support long-term disease management. Strategic collaborations between diagnostics manufacturers and diabetes management companies are accelerating ecosystem expansion across endocrine-related care pathways. Furthermore, growing investment in hormone-monitoring technologies and biomarker-driven diagnostics is expected to support innovation across the fertility, thyroid, and metabolic testing segments over the forecast period.

Market Concentration & Characteristics

The endocrine testing market is characterized by high innovation driven by continuous advancements in hormone detection technologies, laboratory automation, and precision diagnostics. Immunoassay platforms continue to dominate routine endocrine testing due to their scalability and cost efficiency, while tandem mass spectrometry (LC-MS/MS) is witnessing increasing adoption for complex steroid hormone analysis, including testosterone, cortisol, estradiol, and DHEAS testing. Major diagnostic companies such as Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, Danaher Corporation, and Beckman Coulter are investing heavily in highly automated analyzers, high-sensitivity hormone assays, and integrated endocrine testing workflows to improve laboratory throughput, assay precision, and turnaround time. The increasing integration of AI-enabled analytics, automated sample handling, and connected diabetes-monitoring technologies is further enhancing endocrine disease management across hospitals and commercial laboratories.

The endocrine testing industry currently demonstrates moderate consolidation, with major participants primarily focusing on strategic collaborations, assay expansion, and biomarker-focused acquisitions rather than large-scale mergers. Companies are increasingly partnering with diabetes technology providers, fertility clinics, and precision medicine developers to strengthen endocrine testing capabilities and expand access to integrated metabolic monitoring solutions. For instance, in August 2024, Abbott announced a global partnership with Medtronic to integrate Abbott’s FreeStyle Libre continuous glucose monitoring technology with Medtronic’s automated insulin delivery and smart insulin pen systems, reflecting the growing convergence between endocrine diagnostics and connected metabolic disease management. In addition, strategic investments into reproductive endocrinology and biomarker-based testing continue to accelerate innovation in ovarian reserve assessment, fertility monitoring, and metabolic hormone evaluation.

Regulatory oversight plays a significant role in the endocrine testing market, given the clinical importance of accurate hormone quantification for disease diagnosis and long-term treatment management. Endocrine diagnostic assays and laboratory platforms must comply with stringent quality and performance standards established by agencies such as the U.S. Food and Drug Administration (FDA), European Medicines Agency (EMA), and other national regulatory authorities. Hormone assays, particularly for testosterone, cortisol, thyroid hormones, and fertility biomarkers, require high analytical specificity and reproducibility because even minor measurement deviations can significantly affect clinical decision-making. As laboratories increasingly adopt high-sensitivity immunoassays and LC-MS/MS technologies, regulatory requirements for assay standardization, validation, and calibration are becoming more rigorous. While these regulations support diagnostic reliability and patient safety, they also increase development timelines and operational costs for manufacturers.

The endocrine testing market faces moderate substitution pressure, as endocrine testing remains an essential component of chronic disease management, fertility assessment, metabolic monitoring, and reproductive healthcare. Although wearable sensors, continuous glucose monitoring systems, and saliva-based hormone tracking technologies are emerging, laboratory-based endocrine testing continues to dominate due to its higher analytical accuracy, broader biomarker coverage, and established clinical validation. Within the market, there is a gradual transition from conventional immunoassays to more advanced tandem mass spectrometry-based testing for improved hormone specificity and sensitivity. At the same time, hospitals and commercial laboratories are increasingly shifting toward centralized, high-throughput endocrine testing platforms to manage rising testing volumes for diabetes, thyroid disorders, obesity, and reproductive health conditions.

Test Type Insights

The thyroid stimulating hormone (TSH) test segment accounted for the largest revenue share of 29.67% in 2025, primarily due to the high prevalence of thyroid disorders, increasing routine health screening practices, and the widespread use of TSH assays as a first-line diagnostic tool for thyroid dysfunction assessment. TSH testing remains widely integrated across hospitals, commercial laboratories, and outpatient diagnostic settings due to its cost-effectiveness, high testing frequency, and clinical importance in monitoring hypothyroidism, hyperthyroidism, metabolic disorders, and thyroid-related complications. Demand has further strengthened with the growing aging population, rising obesity prevalence, and increasing incidence of autoimmune thyroid diseases globally. The segment also benefits from broad reimbursement coverage and strong integration into preventive healthcare programs across developed healthcare systems. For instance, in October 2023, Eli Lilly presented Phase 3 LIBRETTO-431 and LIBRETTO-531 results for Retevmo (selpercatinib) at the ESMO Congress, supporting advancements in RET-mutant medullary thyroid cancer management and reinforcing the growing importance of endocrine-related diagnostic monitoring in oncology care pathways.

The Dehydroepiandrosterone Sulfate (DHEAS) test segment is projected to grow at the fastest CAGR during the forecast period, driven by rising awareness regarding adrenal disorders, hormonal imbalance assessment, PCOS diagnosis, and advanced androgen profiling applications. The increasing adoption of tandem mass spectrometry technologies is significantly improving the accuracy and sensitivity of DHEAS testing, particularly in specialized endocrine laboratories and reproductive health centers. Growing focus on personalized hormone management and biomarker-driven endocrinology is further accelerating segment expansion across developed and emerging healthcare markets. In September 2024, Trinity Biotech acquired Metabolomics Diagnostics to strengthen its presence in biomarker-based endocrine and maternal health diagnostics, highlighting the increasing industry focus on advanced hormone biomarker analysis and precision endocrine testing solutions.

Technology Insights

The immunoassay segment accounted for the largest revenue share of the endocrine testing market in 2025, driven by its extensive use in routine hormone analysis, high-throughput laboratory workflows, and strong compatibility with automated diagnostic platforms. Immunoassay technologies remain the preferred approach for large-volume endocrine testing, including TSH, insulin, hCG, testosterone, cortisol, and fertility hormone analysis due to their cost efficiency, rapid turnaround time, and scalability across hospitals and commercial laboratories. The widespread adoption of chemiluminescence immunoassay systems and automated analyzers has further strengthened market penetration, particularly in centralized laboratory settings handling large endocrine testing volumes. The segment also benefits from rising chronic disease burden and the expansion of preventive healthcare screening programs globally. In March 2024, Siemens Healthineers launched its Anti-Müllerian Hormone (AMH) Assay to expand reproductive endocrinology testing capabilities, highlighting the growing industry focus on automated hormone testing solutions for fertility assessment and ovarian reserve evaluation.

The tandem mass spectrometry segment is projected to grow at the fastest CAGR of 12.61% over the forecast period, driven by increasing demand for highly sensitive and specific hormone quantification technologies. Laboratories are progressively adopting LC-MS/MS platforms for advanced steroid hormone testing, particularly for testosterone, cortisol, estradiol, and DHEAS assays, where traditional immunoassays may face specificity limitations. The rising emphasis on precision endocrinology, biomarker standardization, and the evaluation of complex endocrine disorders is accelerating adoption across reference laboratories and specialized diagnostic centers. In addition, regulatory focus on assay accuracy and harmonization is supporting the transition toward mass spectrometry-based hormone analysis. For instance, in May 2026, Siemens Healthineers reaffirmed that its Atellica IM TSTII assay maintained CDC HoSt-TT certification for total testosterone testing, demonstrating equivalence to LC-MS/MS standards and reflecting the growing importance of highly standardized hormone measurement technologies in endocrine diagnostics.

End-use Insights

The commercial laboratories segment accounted for the largest revenue share of 46.38% in 2025, driven by the growing shift toward centralized, high-throughput diagnostic testing and the increasing preference for outsourced laboratory services among healthcare providers. Commercial laboratories benefit from advanced automation capabilities, broad endocrine assay menus, economies of scale, and strong integration with preventive healthcare and chronic disease monitoring programs. Rising testing volumes for thyroid disorders, diabetes management, fertility assessment, and metabolic hormone evaluation have further strengthened demand for large independent diagnostic laboratory networks globally. In addition, commercial laboratories are increasingly adopting advanced immunoassay and tandem mass spectrometry platforms to improve testing efficiency and analytical precision. For instance, in March 2025, Dexcom announced integration of its G7 sensor with Novo Nordisk’s NovoPen 6 and NovoPen Echo Plus in Germany, enabling consolidated glucose and insulin management data through a single application, highlighting the growing importance of integrated endocrine and metabolic monitoring ecosystems supported by centralized diagnostic infrastructures.

The hospitals segment continued to hold a significant share of the endocrine testing industry, owing to the high volume of inpatient and outpatient endocrine evaluations conducted within hospital-based laboratory settings. Hospitals remain critical centers for hormone testing, including emergency care, chronic disease management, oncology-related endocrine assessment, reproductive health evaluation, and surgical monitoring. The segment also benefits from increasing adoption of advanced diagnostic analyzers within tertiary care hospitals and multispecialty healthcare institutions. Furthermore, hospitals are witnessing rising endocrine testing demand linked to obesity-related complications, metabolic disorders, and endocrine-driven chronic diseases requiring long-term clinical management.

Regional Insights

North America endocrine testing market held the largest revenue share of over 39.66% in 2025 and is anticipated to maintain its position during the forecast period. North America leads the endocrine testing market owing to its highly developed diagnostics infrastructure, strong reimbursement systems, and high adoption of preventive healthcare screening. The region demonstrates significant testing volumes for thyroid disorders, diabetes management, obesity-related metabolic monitoring, and fertility diagnostics across hospitals and commercial laboratories. The growing adoption of automated immunoassay systems, the integration of continuous glucose monitoring, and advanced hormone testing platforms continue to support market expansion. The presence of major diagnostics manufacturers and large independent laboratory networks further strengthens regional market dominance across endocrine and metabolic disease management.

U.S. Endocrine Testing Market Trends

The U.S. represents the largest country-level market globally due to high healthcare expenditure, strong endocrine disease awareness, and extensive utilization of laboratory-based hormone testing across hospitals and commercial laboratories. Rising obesity prevalence, increasing diabetes burden, and growing demand for reproductive endocrinology testing continue to support sustained market growth. The country also leads in the adoption of advanced endocrine diagnostic technologies, including high-sensitivity immunoassays and tandem mass spectrometry platforms. Furthermore, strong regulatory support and rapid commercialization of metabolic disease therapies continue to increase endocrine monitoring requirements across clinical care settings.

Europe Endocrine Testing Market Trends

Europe holds a significant share of the endocrine testing industry, supported by universal healthcare coverage, strong laboratory infrastructure, and increasing focus on chronic disease management. The region demonstrates high adoption of thyroid, insulin, fertility, and cortisol testing across centralized diagnostic laboratories and hospital-based healthcare systems. The increasing aging population and rising incidence of metabolic disorders continue to support endocrine diagnostics utilization. Additionally, regulatory emphasis on assay standardization and diagnostic accuracy is encouraging adoption of highly sensitive endocrine testing technologies, particularly across Western European healthcare systems.

The Germany endocrine testing market is one of Europe’s largest markets due to its advanced healthcare infrastructure, strong reimbursement framework, and extensive adoption of automated laboratory technologies. The country has a well-established network of commercial laboratories and tertiary healthcare institutions performing high-volume hormone testing for thyroid disorders, diabetes management, and reproductive health assessment. Demand for highly accurate endocrine assays is further supporting the adoption of tandem mass spectrometry technologies across specialized diagnostic laboratories. Germany also benefits from strong preventive healthcare awareness and routine chronic disease monitoring practices among aging patient populations.

The endocrine testing market in France maintains a strong position, owing to broad public healthcare access, high endocrine testing penetration, and growing demand for fertility and metabolic hormone diagnostics. The increasing incidence of thyroid disorders, obesity, and diabetes-related endocrine complications continues to drive testing volumes across hospital and commercial laboratory settings. The country also benefits from a strong preventive healthcare culture and the widespread integration of endocrine assays into routine diagnostic workflows. Demand for reproductive endocrinology testing and ovarian reserve assessment is also increasing steadily with rising fertility treatment adoption.

Asia Pacific Endocrine Testing Market Trends

The Asia Pacific endocrine testing industry is projected to grow at the fastest CAGR during the forecast period, driven by expanding healthcare infrastructure, rising diabetes prevalence, growing thyroid disorder burden, and increasing preventive healthcare awareness across emerging economies. The rapid expansion of private diagnostic laboratory chains and the improvement in access to advanced endocrine testing technologies are accelerating market development across China, India, and Southeast Asia. The region additionally benefits from large patient populations requiring long-term metabolic and reproductive hormone monitoring. Increasing healthcare investments and rising adoption of automated laboratory systems continue to strengthen endocrine diagnostics capacity throughout the region.

The China endocrine testing market is the largest in Asia Pacific, driven by its large patient population, rapidly modernizing healthcare infrastructure, and increasing burden of diabetes and thyroid disorders. Government-led healthcare expansion initiatives and rising preventive healthcare awareness are contributing to higher endocrine testing penetration across hospitals and independent laboratories. The country is also witnessing the growing adoption of advanced automated immunoassay systems and centralized laboratory testing models to improve diagnostic efficiency. Increasing urbanization and rising healthcare expenditure continue to support long-term market growth across metabolic and reproductive hormone testing applications.

The endocrine testing market in Japanholds a substantial regional share, due to its aging population, highly advanced diagnostics infrastructure, and strong culture of routine health screening. The country demonstrates high utilization of thyroid, insulin, cortisol, and reproductive hormone testing across hospital and laboratory settings. Japan is also among the leading adopters of high-throughput automated analyzers and precision endocrine diagnostics technologies. Growing focus on chronic disease management and long-term metabolic monitoring continues to sustain demand for highly sensitive endocrine testing solutions within the country’s mature healthcare ecosystem.

Latin America Endocrine Testing Market Trends

Latin America is witnessing steady growth in the endocrine testing industry, driven by expanding private healthcare infrastructure, rising awareness of diabetes and thyroid disorders, and improved diagnostic accessibility. Brazil and Argentina continue to represent the largest regional markets due to relatively stronger laboratory infrastructure and increasing chronic disease testing volumes. However, uneven healthcare access and reimbursement limitations across several countries continue to moderate overall regional market penetration. Rising investments in private diagnostics laboratories and preventive healthcare services are expected to support gradual market expansion over the forecast period.

Middle East and Africa Endocrine Testing Market Trends

The Middle East and Africa endocrine testing industry is expanding steadily due to increasing government healthcare investments, rising obesity and diabetes prevalence, and improving diagnostic infrastructure across major urban healthcare centers. Gulf Cooperation Council countries are demonstrating growing adoption of advanced hormone testing technologies and integrated metabolic disease management solutions. Meanwhile, South Africa continues to serve as a key diagnostics hub within Sub-Saharan Africa. Despite ongoing infrastructure improvements, limited laboratory access and uneven healthcare coverage across several African economies continue to constrain broader endocrine testing penetration within the region.

Key Endocrine Testing Company Insights

Some of the leading players operating in the endocrine testing market include F. Hoffmann-La Roche Ltd., Quest Diagnostics Incorporated, and Abbott. Companies focus on capturing the market by increasing their presence using various business initiatives, such as partnerships & collaborations with government. Moreover, these companies have well-established end-use portfolios, which help them capture major market share.

AB Sciex; Agilent Technologies Inc.; and bioMérieux SA are some of the emerging participants in the endocrine testing industry. Developing & launching new and improved diagnostic tools that offer faster results, higher accuracy, and easier usability are prevalent operating strategies for these companies. The players may face challenges in penetrating the market due to competition and regulatory hurdles.

Key Endocrine Testing Companies:

The following key companies have been profiled for this study on the endocrine testing market.

- Abbott Laboratories

- AB Sciex

- Agilent Technologies Inc.

- bioMerieux SA

- Bio-Rad Laboratories Inc.

- DiaSorin S.p.A.

- F. Hoffmann-La Roche Ltd.

- Laboratory Corporation of America Holdings

- Quest Diagnostics Incorporated

- Ortho Clinical Diagnostics

Recent Development

-

In May 2026, the FDA approved Pfizer’s Veppanu (vepdegestrant) for ER+/HER2-negative, ESR1-mutated advanced breast cancer following prior endocrine therapy, while simultaneously clearing the Guardant360 CDx liquid biopsy as a companion diagnostic for ESR1 mutation identification.

-

In December 2025, the FDA approved Novo Nordisk’s once-daily oral Wegovy (25 mg semaglutide), marking the first oral GLP-1 receptor agonist indicated for chronic weight management and cardiovascular risk reduction in adults with obesity or overweight.

-

In August 2025, subcutaneous semaglutide received accelerated FDA approval for the treatment of metabolic dysfunction-associated steatohepatitis (MASH) in adults with moderate-to-advanced liver fibrosis.

-

In January 2025, Eli Health launched Hormometer at CES, an AI-powered saliva-based hormone monitoring platform enabling real-time multi-hormone analysis through disposable cartridge technology

Endocrine Testing Market Report Scope

Report Attribute

Details

Market size in 2025

USD 14.4 billion

Estimated market size in 2026

USD 15.5 billion

Projected market size by 2033

USD 27.3 billion

Growth rate

CAGR 8.5% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Test type, end-use, technology, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Abbott Laboratories; AB Sciex; Agilent Technologies Inc.; bioMerieux SA; Bio-Rad Laboratories Inc.; DiaSorin S.p.A.; F. Hoffmann-La Roche Ltd.; Laboratory Corporation of America Holdings; Quest Diagnostics Incorporated; Ortho Clinical Diagnostics

Customization scope

Free report customization (equivalent to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Global Endocrine Testing Market Report Segmentation

This report forecasts revenue growth and provides an analysis on the latest trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global endocrine testing market report based on test type, end-use, technology, and region:

-

Test Type Outlook (Revenue, USD Million, 2021 - 2033)

-

Thyroid Stimulating Hormone (TSH) Test

-

Insulin Test

-

Testosterone Test

-

Cortisol Test

-

Human Chorionic Gonadotropin (hCG) Hormone Test

-

Follicle Stimulating Hormone (FSH) Test

-

Luteinizing Hormone (LH) Test

-

Estradiol (E2) Test

-

Progesterone Test

-

Prolactin Test

-

Dehydroepiandrosterone Sulfate (DHEAS) Test

-

Others

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Immunoassay

-

Tandem Mass Spectrometry

-

Monoclonal & Polyclonal Antibody Technologies

-

Clinical Chemistry

-

Sensor Technology

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospital

-

Commercial Laboratory

-

Ambulatory Care Centers

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

Japan

-

China

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Frequently Asked Questions About This Report

The global endocrine testing market size was valued at USD 14.4 billion in 2025 and is estimated at USD 15.5 billion for 2026.

The global endocrine testing market is expected to grow at a CAGR of 8.5% from 2026 to 2033, reaching USD 27.3 billion by 2033.

North America dominated with a 39.7% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

Key players include Abbott Laboratories; AB Sciex; Agilent Technologies Inc.; bioMerieux SA; Bio-Rad Laboratories Inc.; DiaSorin S.p.A.; F. Hoffmann-La Roche Ltd.; Laboratory Corporation of America Holdings; Quest Diagnostics Incorporated; Ortho Clinical Diagnostics

Key factors that are driving the global endocrine testing market growth include growing incidences of life style diseases, endocrine disorders & awareness of reproductive functions such as obesity, hyperthyroidism, diabetes, infertility and adrenal insufficiency.

The thyroid stimulating hormone segment led with a 29.7% revenue share in 2025, while the dehydroepiandrosterone sulfate segment is the fastest-growing.

The immunoassay segment held the largest revenue share in 2025, while the tandem mass spectrometry segment is the fastest-growing.

The commercial laboratories segment led with a 46.4% revenue share in 2025, while the hospitals segment is the fastest-growing.

About the Author(s)

Clinical Diagnostics Research Team

Healthcare · Clinical DiagnosticsThis report was authored by the clinical diagnostics research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the clinical diagnostics segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.