- Home

- »

- Medical Devices

- »

-

Immunoassay Market Size, Share & Growth Report 2026-2033GVR Report cover

![Immunoassay Market Size, Share & Trends Report]()

Immunoassay Market (2026 - 2033) Size, Share & Trends Analysis Report By Product, By Technology (Radioimmunoassay, Enzyme Immunoassays, Rapid Test), By Application (Oncology, Cardiology), By End-use, By Specimen, By Region, And Segment Forecasts

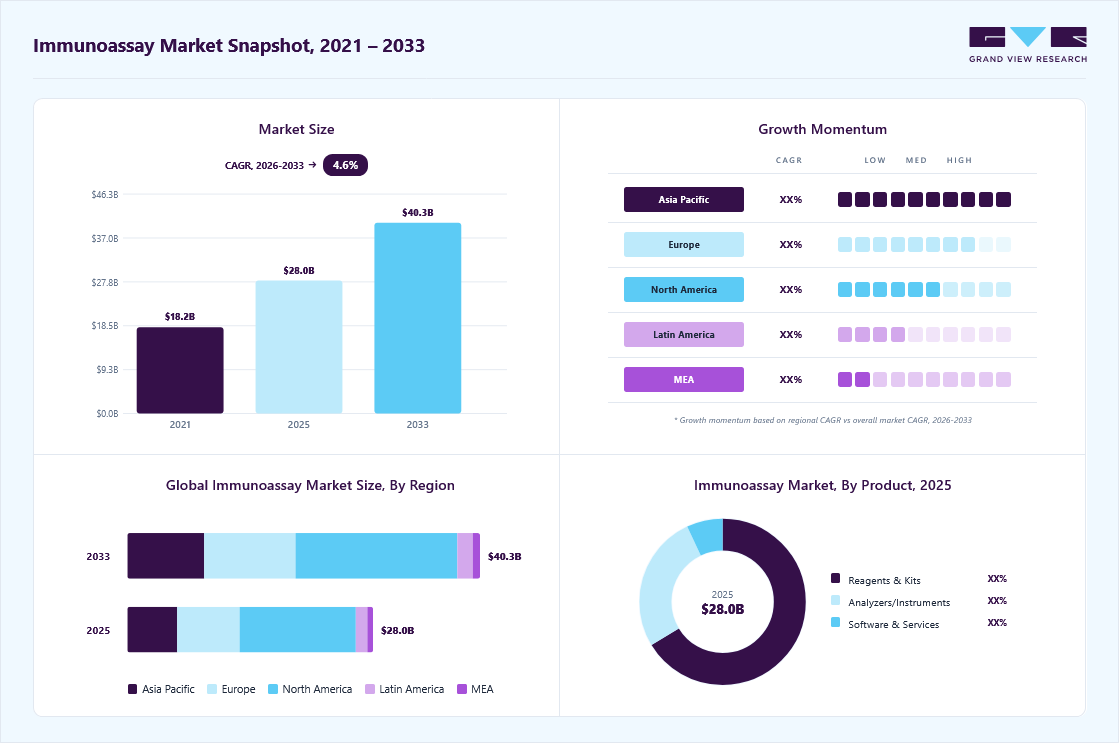

Market Size, 2025

$28.0BMarket Estimate, 2026

$29.3BMarket Forecast, 2033

$40.3BCAGR, 2026–2033

4.6%Immunoassay Market Summary

The global immunoassay market size was estimated at USD 28.0 billion in 2025 and is projected to grow from USD 29.3 billion in 2026 to USD 40.3 billion by 2033, at a CAGR of 4.6% from 2026 to 2033, driven by increasing demand for precision medicine. The market in North America dominated with a revenue share of 47.3% in 2025. Immunoassays play a crucial role in tailoring treatments to individual patients by identifying biomarkers that predict responses to specific therapies.

Key Market Trends & Insights

- By product: Reagents & kits segment held the highest market share of 66.2% in 2025.

- By technology: Enzyme immunoassays (EIA) segment held the largest market share in 2025.

- By specimen: Blood held the largest share of the market, accounting for 41.4% of revenue in 2025.

- By end-use: Hospitals accounted for the largest revenue share of 32.4% in 2025.

- By application: Infectious disease segment held the largest market share in 2025.

Regional Highlights

- Largest regional market: North America (47.3% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- The immunoassay industry in the U.S. is expected to grow significantly over the forecast period.

Market Size & Forecast

- Market size in 2025: USD 28.1 Billion

- Estimated market size in 2026: USD 29.3 Billion

- Projected market size by 2033: USD 40.3 Billion

- CAGR (2026-2033): 4.6%

The rising prevalence of cancer, cardiovascular diseases, and autoimmune disorders has driven the need for targeted therapies, where immunoassays help determine the most effective treatment for patients. This approach minimizes adverse effects and enhances treatment efficacy, improving patient outcomes. The shift from a one-size-fits-all treatment approach to personalized medicine is a primary driver of market expansion. Furthermore, pharmaceutical companies are increasingly integrating immunoassays into drug development pipelines to improve the success rate of novel therapeutics, further accelerating market growth.")

Mainstream Immunoassays for Detection of HCoVs Infections

Methods

Applications

Advantages

Limitations

ELISA

Diagnosis in the absence of PCR laboratory conditions; supplemental tests with PCR to improve diagnostic accuracy; seroepidemiological survey; evaluation of vaccine efficacy

High throughput; can be automated; semiquantitative or quantitative

Requires basic laboratory technician and equipment

WB

Confirmatory test for diagnosis or research

Quantitative determination; multiple target detection in one test

Operation complex; high requirement for experience and equipment; time-consuming

IFA

Confirmatory test for diagnosis or research

High sensitivity and specificity

Operation complex; high requirement for experience and equipment; time-consuming

ICT

POCT; self-testing

Rapid and easy to operate; no requirement for a laboratory or technician

Relatively low specificity and sensitivity; high false-negative rate; qualitative determination

Immunosensor

POCT

Portable, rapid, and easy to operate; low LOD

Unstable performance; high economic cost

Market Dynamics

The increasing prevalence of chronic diseases globally is driving the growth of the market, as immunoassays are widely utilized for disease detection, biomarker analysis, and therapeutic monitoring due to their high sensitivity and specificity. Chronic conditions, including cardiovascular diseases, cancer, diabetes, and autoimmune disorders, require continuous diagnostic evaluation, accelerating the adoption of immunoassay-based testing across hospitals and clinical laboratories. According to the World Health Organization 2026 report, noncommunicable diseases account for approximately 74% of all deaths worldwide, with more than three-quarters of NCD-related deaths occurring in low- and middle-income countries. Furthermore, nearly 86% of the 17 million premature deaths caused by NCDs occur before the age of 70, highlighting the growing need for early and accurate diagnostic monitoring solutions. In addition, growing adoption of automated immunoassay analyzers is improving laboratory efficiency, throughput capacity, and diagnostic precision, further strengthening clinical adoption of immunoassay technologies worldwide.

The rising burden of infectious diseases is also contributing to the expansion of the market, as immunoassays are widely used for rapid, accurate pathogen detection. Diseases such as tuberculosis, HIV, hepatitis, influenza, and COVID-19 continue to accelerate demand for reliable diagnostic solutions across healthcare systems. The Global Tuberculosis Report 2023, published by the World Health Organization, stated that approximately 10.6 million people developed tuberculosis in 2022, highlighting the growing need for scalable diagnostic testing technologies. Furthermore, increasing preference for point-of-care diagnostics, stronger emphasis on early disease identification, and broader deployment of automated immunoassay platforms are supporting wider integration of immunoassay-based testing across global healthcare settings.

Cross-reactivity remains one of the major limitations restraining the growth of the market, as structurally similar antigens or biomolecules may unintentionally bind with assay antibodies, resulting in false-positive or inaccurate diagnostic outcomes. This limitation can significantly affect diagnostic precision across infectious disease, oncology, and autoimmune disorder testing, where accurate biomarker identification is essential for effective clinical decision-making. In the market, rapid screening assays occasionally detect non-target proteins or closely related pathogens, reducing test specificity and increasing reliance on confirmatory molecular diagnostic methods such as PCR-based testing.

Recent healthcare surveillance programs have further highlighted specificity challenges within the market during respiratory infection testing, particularly for COVID-19, influenza, and respiratory syncytial virus (RSV). Diagnostic laboratories observed that overlapping viral protein characteristics could influence assay performance in certain rapid immunoassay platforms, especially during periods of high co-infection prevalence. As a result, companies operating in the market are increasingly focusing on advanced multiplex immunoassays, chemiluminescence immunoassays (CLIA), and AI-integrated assay interpretation technologies to improve specificity, reduce cross-reactivity, and strengthen diagnostic reliability across hospitals, clinical laboratories, and point-of-care testing environments.

The increasing adoption of point-of-care diagnostics presents a significant growth opportunity for the market, driven by rising demand for rapid, accessible, and decentralized diagnostic testing solutions. Immunoassay-based point-of-care tests are widely utilized for infectious disease detection, cardiac marker testing, pregnancy testing, and chronic disease monitoring due to their fast turnaround time and ease of use. For instance, increasing deployment of rapid antigen immunoassay tests for COVID-19, influenza, and HIV screening across pharmacies, clinics, and home healthcare settings has accelerated global acceptance of portable diagnostic technologies. Furthermore, continuous advancements in lateral flow assays, microfluidics, and digital immunoassay technologies are supporting the development of highly sensitive and user-friendly point-of-care solutions across healthcare systems.

Market Concentration & Characteristics

The degree of innovation in the market is increasing rapidly, driven by continuous advancements in multiplex assays, nanotechnology-based detection systems, biosensor integration, and AI-assisted diagnostic platforms. These technologies enable simultaneous detection of multiple biomarkers, improving diagnostic efficiency, sensitivity, and turnaround time across oncology, cardiology, endocrinology, and infectious disease testing. The integration of artificial intelligence and machine learning is further enhancing immunoassay data interpretation through advanced pattern recognition and predictive analytics, thereby supporting improved clinical decision-making and laboratory workflow automation. Furthermore, the ongoing development of automated, high-throughput immunoassay platforms is strengthening early disease detection capabilities and expanding the adoption of next-generation diagnostic technologies across hospitals, diagnostic laboratories, and point-of-care healthcare settings.

The level of mergers and acquisitions in the market is increasing significantly as companies focus on strengthening immunodiagnostic capabilities, expanding point-of-care testing portfolios, and improving access to decentralized diagnostic solutions. These strategic activities are supporting the development of advanced immunochemistry platforms, high-sensitivity assays, and rapid diagnostic technologies across infectious disease and chronic disease testing. For instance, in July 2024, Roche completed the acquisition of LumiraDx’s Point of Care technology to strengthen its immunoassay and immunochemistry diagnostics portfolio. The acquisition enhanced Roche’s multi-assay point-of-care platform capabilities across immunoassay, clinical chemistry, and molecular diagnostics, supporting broader expansion of decentralized diagnostic testing within the market.

Regulatory frameworks established by agencies such as the U.S. Food and Drug Administration and the European Medicines Agency play a critical role in shaping the growth of the market by ensuring high standards of safety, quality, accuracy, and clinical performance for immunodiagnostic products. Immunoassay manufacturers are required to submit extensive clinical validation data related to assay sensitivity, specificity, precision, and reproducibility before receiving regulatory approval for commercialization. These stringent regulatory requirements are shaping product development strategies in the market, prompting companies to focus on highly reliable, automated, and clinically validated diagnostic solutions. Additionally, evolving regulatory standards are supporting innovation in precision medicine, companion diagnostics, and next-generation biomarker-based immunoassay technologies across global healthcare systems.

Product expansion in the market is growing rapidly as companies focus on developing personalized, disease-specific diagnostic solutions. Immunoassay manufacturers are increasingly introducing customized assays that detect genetic biomarkers, protein expression profiles, and immune responses to support precision medicine and targeted therapeutic decision-making. The rising prevalence of infectious diseases, including COVID-19, HIV, hepatitis, and emerging viral infections, is further accelerating demand for advanced immunoassay products. For instance, in August 2024, the U.S. Food and Drug Administration granted marketing authorization to NOWDiagnostics for the First to Know Syphilis Test, the first over-the-counter home immunoassay for syphilis antibody detection, highlighting the ongoing expansion of rapid, accessible immunodiagnostic products in the market.

Regional expansion in the market is accelerating significantly, driven by increasing adoption of point-of-care testing, personalized medicine, and infectious disease diagnostics across North America, Asia Pacific, Latin America, and the Middle East & Africa. Rising healthcare expenditure, improved laboratory infrastructure, supportive regulatory frameworks, and growing awareness of early disease detection are further driving market penetration in emerging economies. In addition, the increasing prevalence of chronic and infectious diseases is strengthening demand for advanced immunodiagnostic solutions across hospitals, diagnostic laboratories, and decentralized healthcare settings. Companies operating in the market are increasingly focusing on regional partnerships, localized manufacturing, and expansion of distribution networks to improve accessibility, strengthen healthcare outcomes, and expand their global market presence.

Product Insights

In 2025, the kits and reagents accounted for the largest share in the market, driven by rising demand for rapid, high-throughput, and disease-specific diagnostic testing across oncology, infectious disease, cardiology, and neurology applications. ELISA kits, chemiluminescence immunoassays (CLIA), lateral flow assays, and rapid antigen test kits are witnessing significant adoption due to their high sensitivity, ease of use, and faster diagnostic turnaround times. In addition, the expanding adoption of biomarker-based testing and personalized medicine is driving demand for advanced immunoassay reagents and kits across clinical laboratories and hospitals. For instance, in April 2026, Sysmex Corporation launched the HISCL p-Tau217 Assay Kit for research use in Europe, enabling automated measurement of Alzheimer’s disease-related biomarkers through its HISCL immunoassay systems. Such product innovations are strengthening technological advancement and supporting the continued growth of the global market.

However, the software and services segment is projected to register the fastest CAGR over the forecast period, driven by increasing adoption of automated diagnostic platforms, laboratory workflow management solutions, and data interpretation services across clinical and research settings. Hospitals, diagnostic laboratories, and research institutions are increasingly relying on external immunoassay testing services and integrated software platforms to improve operational efficiency, diagnostic accuracy, and turnaround times. The growing adoption of AI-enabled laboratory analytics, cloud-based data management systems, and automated immunoassay technologies is further accelerating demand for specialized software and technical support services. In addition, manufacturers are expanding their offerings to include laboratory automation support, assay optimization, operator training, maintenance services, and regulatory consulting to enable efficient use of advanced immunoassay systems. These expanding service capabilities are improving laboratory productivity and supporting broader adoption of advanced technologies across the market.

Application Insights

The infectious disease application segment led the market with a 30.1% revenue share in 2025 and is projected to grow at a CAGR of 5.5% during the forecast period, driven by the increasing prevalence of tuberculosis, HIV, hepatitis, influenza, and other infectious diseases globally. The market is experiencing strong demand for infectious disease testing, driven by the widespread use of immunoassays for rapid pathogen detection, screening, and disease monitoring. According to the World Health Organization, tuberculosis alone caused approximately 1.23 million deaths globally in 2024, highlighting the growing need for accurate and high-throughput immunodiagnostic solutions. In addition, increasing adoption of point-of-care testing, biomarker-based screening, and automated diagnostic platforms is further accelerating the growth of the infectious disease segment within the market.

The oncology and autoimmune disease segments are projected to grow significantly during the forecast period, driven by rising global cancer incidence and the demand for early, accurate biomarker-based diagnostics. Immunoassays play a critical role in tumor marker detection, therapeutic monitoring, and personalized treatment selection across breast, prostate, ovarian, and colorectal cancers. According to the American Cancer Society’s Cancer Facts & Figures 2026 report, approximately 2.11 million new cancer cases and 626,140 cancer deaths are projected in the U.S. in 2026, underscoring the growing need for advanced diagnostic technologies. Increasing adoption of companion diagnostics, targeted therapies, and biomarker-driven testing is further accelerating demand for advanced immunoassay solutions. Additionally, growing regulatory approvals and collaborations between pharmaceutical and diagnostic companies are supporting the expansion of oncology and autoimmune disease applications within the market.

Technology Insights

Enzyme immunoassays dominated the market with a 64.1% revenue share in 2025, driven by increasing adoption across personalized medicine, cancer diagnostics, cardiovascular disease testing, and infectious disease detection. The technology remains widely utilized due to its high sensitivity, specificity, and compatibility with automated laboratory systems. Emerging technologies such as microarray-based immunoassays and lab-on-a-chip platforms are further expanding multiplex biomarker detection and rapid diagnostic capabilities. For instance, in January 2026, Fujirebio launched the Lumipulse G pTau 217 CSF assay for its fully automated LUMIPULSE G immunoassay analyzers, enabling rapid and highly sensitive measurement of Alzheimer’s disease-related biomarkers through chemiluminescent enzyme immunoassay (CLEIA) technology. Such advancements are strengthening innovation and expanding applications within the market.

However, the rapid test segment is projected to grow rapidly in the market during the forecast period, driven by increasing demand for rapid, portable, and point-of-care diagnostic solutions for infectious and chronic disease testing. Technologies including electrochemiluminescence immunoassays (ECLIA), nanoparticle-based immunoassays, biosensor-based assays, and western blot immunoassays are expanding diagnostic sensitivity and real-time testing capabilities. In addition, the growing adoption of microfluidics and nanotechnology is supporting the development of highly accurate, rapid immunodiagnostic platforms. For instance, in September 2024, QuidelOrtho Corporation expanded its rapid immunoassay testing portfolio by developing advanced point-of-care diagnostic solutions for respiratory and infectious disease detection, supporting faster clinical decision-making and decentralized healthcare delivery in the market.

Specimen Insights

Blood held the largest share of the market, accounting for 41.4% of revenue in 2025, as blood-based specimens remain the most widely used sample type for immunoassay testing across oncology, infectious disease, cardiology, and endocrinology applications. Components, including plasma, serum, and whole blood, are extensively analyzed for the detection of proteins, antibodies, hormones, and disease-specific biomarkers using ELISA, chemiluminescent immunoassays, western blot assays, and rapid antigen tests. For instance, in May 2026, Roche received CE mark approval for its Elecsys pTau217 blood test for Alzheimer’s disease detection, enabling minimally invasive blood-based biomarker analysis through automated immunoassay systems. Such advancements are accelerating the adoption of blood-based diagnostic testing and supporting the continued expansion of the market globally.

Urine is projected to be the fastest-growing specimen segment in the market during the forecast period, driven by its non-invasive nature, ease of collection, and expanding application across infectious disease testing, pregnancy testing, drug screening, kidney disease diagnostics, and oncology monitoring. Urine-based immunoassays are increasingly adopted in point-of-care and decentralized healthcare settings due to their convenience, rapid turnaround time, and cost-effectiveness. Advancements in rapid lateral flow immunoassays, fluorescence immunoassays, and automated urine screening technologies are further improving diagnostic sensitivity and operational efficiency. In addition, expanding workplace drug testing programs, rising demand for home-based diagnostics, and growing adoption of automated laboratory systems are accelerating the use of urine-based immunodiagnostic solutions, supporting continued global expansion of the market.

End-use Insights

In 2025, hospitals accounted for the largest revenue share of 32.4% in the market, driven by increasing adoption of advanced diagnostic technologies for oncology, infectious disease, cardiology, and chronic disease testing. Hospitals extensively utilize immunoassays for early disease detection, biomarker analysis, therapeutic monitoring, and personalized treatment selection due to their high sensitivity and rapid diagnostic capabilities. In addition, hospitals are increasingly adopting automated high-throughput immunoassay systems and digital laboratory workflows to improve diagnostic accuracy and operational efficiency. For instance, in February 2026, QuidelOrtho Corporation entered a strategic supply agreement with Lifotronic Technology Co., Ltd. to expand access to high-throughput immunoassay analyzer platforms and broader assay menus for hospital and clinical laboratory environments across international markets. Such developments are supporting the expansion of advanced hospital-based diagnostic infrastructure within the market.

Clinical laboratories are projected to experience robust growth in the market during the forecast period, driven by increasing demand for high-throughput diagnostic testing, biomarker analysis, and automated laboratory workflows across oncology, infectious diseases, cardiology, and autoimmune disease applications. Clinical laboratories extensively use immunoassays for their high sensitivity and specificity, as well as their ability to support rapid, large-scale sample processing. The growing adoption of chemiluminescence immunoassays (CLIA), multiplex assays, and AI-enabled laboratory analytics is further improving diagnostic efficiency and turnaround times. In addition, increasing outsourcing of diagnostic testing services and expansion of centralized laboratory networks are supporting broader utilization of advanced immunodiagnostic platforms. Such developments are strengthening operational efficiency and accelerating the growth of the clinical laboratories segment within the market.

Regional Insights

North America immunoassay market dominated the global industry for immunoassays, accounting for 47.3% of revenue in 2025, primarily driven by advanced healthcare infrastructure, the high prevalence of chronic and infectious diseases, and the growing adoption of innovative diagnostic technologies across hospitals and clinical laboratories. The region is witnessing increasing demand for biomarker-based testing, personalized medicine, and automated immunoassay systems for diagnostics in oncology, cardiology, infectious diseases, and neurological disorders. In addition, the strong presence of leading market players, favorable reimbursement policies, and supportive regulatory frameworks are accelerating technological advancements in immunodiagnostics. Increasing investments in laboratory automation, high-throughput diagnostic platforms, and precision medicine initiatives are further supporting the continued growth of the market across North America.

U.S. Immunoassay Market Trends

The U.S. immunoassay industry represents a major contributor to the global market, driven by strong technological advancements, advanced healthcare infrastructure, and increasing demand for early and accurate diagnostic testing. Growing adoption of automated immunoassay systems, biomarker-based diagnostics, and personalized medicine is further accelerating market expansion across oncology, infectious disease, cardiology, and neurological disorder applications. In addition, periodic regulatory approvals from the U.S. Food and Drug Administration for novel immunodiagnostic tests and increasing competition among biotechnology and diagnostic companies are supporting continuous product innovation. Rising investments in laboratory automation, AI-assisted diagnostics, and high-throughput testing platforms are further strengthening growth prospects for the U.S. market.

Europe Immunoassay Market Trends

Europe immunoassay industry accounted for a significant share of the global market, led by Germany, France, and the UK, driven by strong healthcare infrastructure and high demand for diagnostic testing across oncology, infectious diseases, cardiology, and autoimmune diseases. The region benefits from supportive regulatory frameworks, rising healthcare investments, and widespread adoption of advanced immunoassay technologies across hospitals and clinical laboratories. In addition, the increasing prevalence of chronic diseases and the growing focus on early disease detection and personalized medicine are further supporting market expansion. Germany’s rising disease burden and increasing adoption of automated diagnostic systems are also contributing to the growth of the market. Overall, these factors are positioning Europe for sustained expansion in the global market.

The immunoassay industry in the UK is propelled by the rising prevalence of chronic diseases, which is fueling the demand for advanced immunoassay analyzers in diagnostics. In the UK, over 5.6 million people have diabetes, with 90% affected by type 2 diabetes, according to Diabetes UK. Government initiatives, such as the NHS Diabetes Prevention Program (DPP), developed in collaboration with Public Health England and Diabetes UK, are actively working to reduce the impact of the disease. Industry leaders are also contributing to these efforts by advancing immunoassay-based diagnostics. For example, LumiraDx is expanding the commercialization of its Rapid Microfluidic Immunoassay HbA1c Test, improving diabetes detection and management across various healthcare facilities. These developments highlight the crucial role of immunoassay technologies in addressing the growing burden of diabetes and enhancing early diagnosis, treatment, and disease monitoring, ultimately driving the growth of the market.

The immunoassay industry in Germany is primarily driven by increasing demand for early diagnosis, chronic disease management, and oncology diagnostics. Germany is also a major producer and exporter of diagnostic devices, with numerous global and regional players setting up manufacturing facilities or partnerships in the country. Automated lab solutions, point-of-care testing, and personalized medicines are the upcoming market trends. In vitro diagnostic regulations and compliance with European standards facilitate high standards of quality, safety, and accuracy.

Asia Pacific Immunoassay Market Trends

The Asia Pacific immunoassay industry is expected to grow at the fastest CAGR, propelled by healthcare reforms, infrastructure enhancements, and a large patient pool. The APAC region is witnessing rapid growth in the market, fueled by emerging economies like Japan, China, and India. Growing healthcare infrastructure, rising prevalence of chronic diseases, and improving healthcare facilities are key drivers of the rising demand for immunoassays. The region’s high burden of chronic diseases, including cancer, and a rising population underscore the need for effective diagnostic solutions. China’s market growth is supported by lifestyle changes, dietary shifts, and an aging population. At the same time, Japan’s focus on technological innovation, driven by substantial government funding, underscores the region’s strong growth potential.

The immunoassay industry in Japan is witnessing growth, driven by a rising prevalence of chronic diseases and investments in healthcare initiatives. Japan’s regulatory framework ensures a strict approval process and harmonizes global standards. Japan’s government has been investing in healthcare and preventive care, which encourages the use of advanced diagnostic technologies, including immunoassays. This dynamic market environment is expected to continue leading the adoption of advanced diagnostics, driven by technological innovations in biomarker detection and automated testing systems.

Latin America Immunoassay Market Trends

The Latin America immunoassay industry is fueled by the swift development of precision medicine and numerous research and development projects. Increasing healthcare awareness and rising demand for diagnostic tests due to the growing burden of diseases like cancer, cardiovascular diseases, and infectious diseases. Brazil’s healthcare sector is characterized by a mix of public and private providers, with public health being managed by the Unified Health System (SUS) and private healthcare playing a substantial role in urban centers.

Middle East and Africa Immunoassay Market Trends

The Middle East and Africa (MEA) immunoassay industry is significantly growing. Both the private and public sectors in the MEA region are increasing their healthcare budgets, driving greater adoption of advanced diagnostics, including immunoassays, across hospitals, clinics, and point-of-care settings. Governments' regulatory systems are country-specific, and stringent processes ensure the quality of medicines. South Africa, in particular, is expected to see a surge in the adoption of immunoassays, driven by increased government involvement and growing awareness of the benefits of personalized treatment. These developments underscore the MEA region’s potential for steady market growth in the coming years.

Key Immunoassays Company Insights

Leading companies operating in the immunoassay industry, including Abbott, Siemens Healthineers, Danaher Corporation (Beckman Colter), bioMérieux, QuidelOrtho Corporation, Sysmex Corporation, Bio-Rad Laboratories, Inc., Roche, Becton, Dickinson and Company, and Thermo Fisher Scientific, are actively focusing on technological innovation and portfolio expansion to strengthen their market position. Companies are increasingly adopting strategies such as product launches, strategic collaborations, geographic expansion, regulatory approvals, and mergers and acquisitions to enhance immunodiagnostic capabilities and expand access to advanced testing solutions. In addition, growing investments in automated immunoassay systems, biomarker-based diagnostics, point-of-care testing, and AI-integrated laboratory technologies are intensifying competition and supporting the continued growth of the global market.

Key Immunoassays Companies:

The following key companies have been profiled for this study on the immunoassays market.

- Abbott

- Siemens Healthineers

- Danaher Corporation (Beckman Coulter)

- bioMérieux SA

- Quidel Corporation

- Sysmex Corporation

- Ortho Clinical Diagnostics

- Bio-Rad Laboratories, Inc.

- F. Hoffmann-La Roche AG

- Becton, Dickinson, and Company

- Thermo Fisher Scientific, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Player: Abbott

- Focus on expanding automated and high-throughput immunoassay platforms to improve laboratory efficiency and testing capacity.

- Invest in strategic collaborations, mergers, and acquisitions to strengthen biomarker portfolios and global market presence.

- Develop advanced technologies including multiplex immunoassays, chemiluminescence immunoassays (CLIA), and AI-enabled diagnostic systems.

- Maintain strong global distribution networks and established relationships with hospitals and diagnostic laboratories.

- Possess extensive R&D capabilities and broad product portfolios across infectious disease, oncology, and chronic disease testing.

- Benefit from strong regulatory expertise, manufacturing scale, and brand recognition in the immunoassay market.

- Face high operational, manufacturing, and compliance costs associated with advanced diagnostic systems.

- Experience lengthy regulatory approval timelines for new immunoassay products and technologies.

- Dependence on sophisticated laboratory infrastructure may limit adoption in resource-constrained settings.

Emerging Players: QuidelOrtho Corporation

- Focus on niche diagnostic applications such as rapid infectious disease and point-of-care immunoassay testing.

- Offer cost-effective and portable immunoassay solutions to target underserved and developing healthcare markets.

- Expand through regional partnerships, localized manufacturing, and flexible commercialization strategies.

- Demonstrate faster innovation cycles and greater flexibility in responding to changing diagnostic trends.

- Benefit from competitive pricing strategies and strong focus on decentralized healthcare diagnostics.

- Quickly adapt products for regional healthcare requirements and emerging disease outbreaks.

- Limited global brand recognition and smaller distribution networks compared to established companies.

- Face challenges related to manufacturing scalability, quality consistency, and regulatory expansion.

- Restricted financial resources may limit large-scale R&D investment and international market penetration.

Recent Developments

-

In January 2026, Fujirebio launched the Lumipulse G pTau 217 CSF assay for its fully automated LUMIPULSE G immunoassay analyzers, expanding advanced chemiluminescent enzyme immunoassay (CLEIA)-based neurological biomarker testing capabilities within the market. The assay enables rapid and highly sensitive quantitative measurement of pTau217 biomarkers associated with Alzheimer’s disease using cerebrospinal fluid samples. The launch further strengthened Fujirebio’s neurodiagnostic portfolio and supported growing demand for automated, high-throughput, and biomarker-driven immunoassay solutions for early neurological disease detection and research applications.

-

In February 2026, QuidelOrtho Corporation entered into a strategic supply agreement with Lifotronic Technology Co., Ltd. to expand its global immunoassay portfolio through new analyzer platforms and more than 25 additional immunoassays. The collaboration enhanced QuidelOrtho’s ability to provide scalable, cost-efficient, and high-throughput diagnostic solutions across diverse laboratory settings, including low- to high-volume clinical laboratories. The agreement also strengthened the company’s assay menu breadth and supported expansion across Europe, Asia-Pacific, Latin America, and the Middle East & Africa within the market.

-

In January 2025, Anbio Biotechnology announced the launch of its Dry Chemiluminescence Immunoassay (CLIA) Solution ADL-1000, designed to deliver rapid, reliable, and cost-effective diagnostic results across diverse clinical settings. The system features freeze-dried reagents, whole-blood testing capabilities, rapid emergency testing, and high-throughput performance, supporting streamlined laboratory workflows and expanding applications across infectious disease, cardiovascular, neurological, and hormone diagnostics in the market.

-

In April 2024, Mindray addressed evolving customer demands by introducing its New Solutions for Mid-Volume Laboratories, featuring two stand-alone analyzers and two integrated solutions. With a compact design and high efficiency, these innovations highlight Mindray’s commitment to advancing chemiluminescence immunoassay and clinical chemistry technologies.

Immunoassay Market Report Scope

Report Attribute

Details

Market size in 2025

USD 28.1 billion

Estimated Market size in 2026

USD 29.32 billion

Projected Market size in 2033

USD 40.25 billion

Growth rate

CAGR of 4.63% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, technology, application, specimen, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; Denmark; Sweden; Norway; China; Japan; India; Australia; South Korea; Thailand; Brazil; Argentina; South Africa; Saudi Arabia; UAE; Kuwait

Key companies profiled

Abbott; Siemens Healthineers; Danaher Corporation (Beckman Coulter); bioMérieux SA; Quidel Corporation; Sysmex Corporation; Ortho Clinical Diagnostics; Bio-Rad Laboratories, Inc.; F. Hoffmann-La Roche AG; Becton, Dickinson, and Company; Thermo Fisher Scientific, Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Immunoassay Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global immunoassay market report based on product, specimen, technology, application, end-use, and region:

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Reagents & Kits

-

ELISA Reagents & Kits

-

Rapid Tests Reagents & Kits

-

ELISPOT Reagents & Kits

-

Western Blot Reagents & Kits

-

Other Reagents & Kits

-

-

Analyzers/Instruments

-

Open-Ended Systems

-

Closed-Ended Systems

-

-

Software & Services

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Therapeutic Drug Monitoring

-

Oncology

-

Cardiology

-

Endocrinology

-

Infectious Disease Testing

-

Autoimmune Diseases

-

Others

-

-

Technology Outlook (Revenue, USD Million, 2021 - 2033)

-

Radioimmunoassay (RIA)

-

Enzyme Immunoassays (EIA)

-

Chemiluminescence Immunoassays (CLIA)

-

Fluorescence Immunoassays (FIA)

-

-

Rapid Test

-

Others

-

-

Specimen Outlook (Revenue, USD Million, 2021 - 2033)

-

Blood

-

Saliva

-

Urine

-

Others

-

-

End-use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals

-

Blood Banks

-

Clinical Laboratories

-

Pharmaceutical and Biotech Companies

-

Academic Research Centers

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Cross-matrix analysis across assay type, application area, and end use

Developed a multi-dimensional cross-matrix integrating assay technology (ELISA, CLIA, FIA, rapid immunoassays, multiplex assays), application area (infectious diseases, oncology, cardiology, endocrinology, autoimmune diseases), and end users (hospitals, diagnostic labs, academic institutes, blood banks).

Enabled identification of high-growth assay categories and application-specific demand opportunities across healthcare settings.

Comparative benchmarking of ELISA, CLIA, FIA, and rapid immunoassays

Conducted side-by-side assessment of assay platforms across sensitivity, specificity, throughput, turnaround time, automation compatibility, scalability, and cost efficiency.

Supported evaluation of technology transition trends and platform prioritization strategies.

Competitive benchmarking of immunoassay manufacturers

Benchmarked global and regional companies based on product portfolio, analyzer installed base, reagent offerings, pricing, regulatory approvals, and innovation pipeline.

Enabled strategic positioning and competitor differentiation planning.

Workflow transition analysis from manual to automated immunoassay systems

Evaluated the migration trend from conventional/manual immunoassay workflows toward fully automated analyzers and integrated laboratory platforms.

Highlighted workflow optimization opportunities and automation-driven market expansion areas.

Cross-segment analysis by disease indication and testing volume

Developed mapping across high-volume disease applications, screening programs, and testing settings to assess utilization trends and future demand patterns.

Provided visibility into high-growth therapeutic areas and testing demand drivers.

Frequently Asked Questions About This Report

Key factors that are driving the immunoassay market growth include an increase in chronic & infectious diseases globally, a rise in the geriatric population prone to such chronic and infectious diseases, and high demand for portable and automated immunoassays.

Some key players operating in the immunoassay market include Siemens Healthineers, BD (Becton, Dickinson & Company), BioMérieux SA, Abbott, F. Hoffmann-La Roche AG, Danaher , Ortho-clinical diagnostics, Sysmex Corporation, Thermo Fisher Scientific, Inc., and Quidel Corporation.

The global immunoassay market size was valued at USD 28.0 billion in 2025 and is estimated at USD 29.3. billion in 2026.

The global immunoassay market is expected to grow at a CAGR of 4.6% from 2026 to 2033, reaching USD 40.3 billion.

Enzyme immunoassays held the largest share (over 64.10%) in 2025, while rapid test is the fastest-growing rapid test segment.

Kits and reagents held the largest revenue share in 2025, while software and services is the fastest-growing segment.

The infectious disease application segment led with a 30.07% revenue share in 2025.

North America dominated with a 47.3% revenue share in 2025.

Asia Pacific is the fastest-growing region over the forecast period.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.