- Home

- »

- Next Generation Technologies

- »

-

Endpoint Security Market Size, Share & Growth Report, 2033GVR Report cover

![Endpoint Security Market (2026 - 2033)Report]()

Endpoint Security Market (2026 - 2033)

Size, Share & Trend Analysis By Component (Solution, Services), By Deployment (Cloud, On-premise), By Enterprise Size (Large Enterprises, SMEs), By Application (BFSI, Healthcare, Retail, IT & Telecom), By Region, And Segment Forecasts

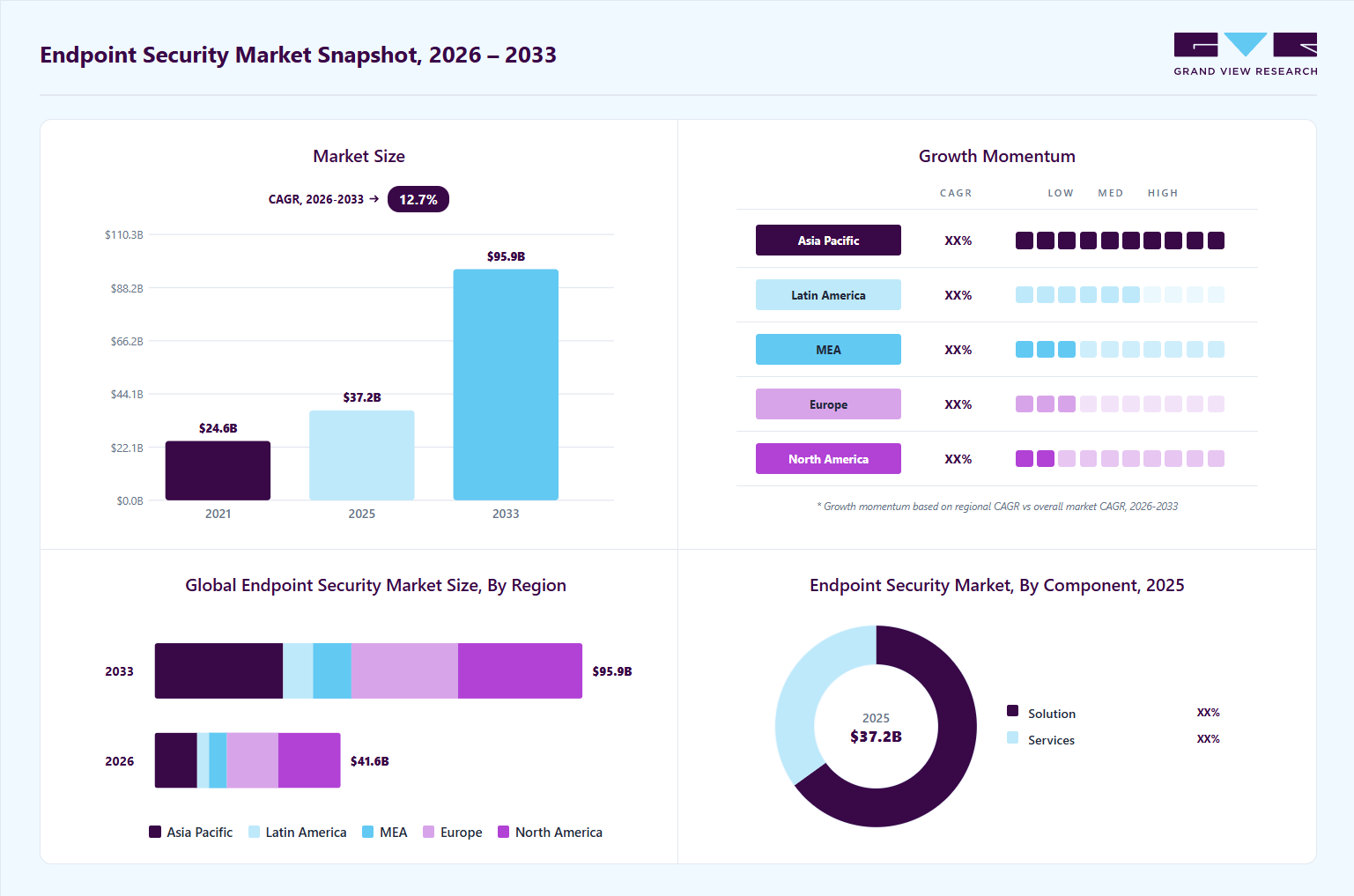

Market Size, 2025

$37.2BMarket Estimate, 2026

$41.6BMarket Forecast, 2033

$95.9BCAGR, 2026–2033

12.7%Endpoint Security Market Summary

The global endpoint security market size was valued at USD 37.2 billion in 2025 and is projected to grow from USD 41.6 billion in 2026 to USD 95.9 billion by 2033, at a CAGR of 12.7% from 2026 to 2033. North America held a 34.4% revenue share of the global market in 2025. The industry is growing steadily as organizations focus on protecting laptops, desktops, mobile devices, servers, and connected endpoints from cyber threats.

Key Market Trends & Insights

- By component: Solution segment held the largest revenue share of 65.0% in 2025.

- By deployment: On-premises segment dominated the market, accounting for the largest revenue share in 2025.

- By enterprise size: Large enterprises segment held the largest revenue share in 2025.

- By application: BFSI segment held a dominant share in the endpoint security market in 2025

Regional Highlights

- Largest regional market: North America (34.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025.

Market Size & Forecast

- Market size in 2025: USD 37.2 Billion

- Estimated market size in 2026: USD 41.6 Billion

- Projected market size by 2033: USD 95.9 Billion

- CAGR (2026-2033): 12.7%

The trend is attributed to increased digital transformation initiatives and rising cybersecurity awareness across enterprises in the region. Businesses are adopting advanced endpoint protection platforms to defend against ransomware, malware, phishing attacks, and unauthorized access. The growing use of cloud computing, remote work, and connected devices is driving increased demand for endpoint security solutions. Companies are also integrating artificial intelligence and automation to improve threat detection and response capabilities. Endpoint security is becoming a core cybersecurity investment across industries worldwide. The Brazil endpoint security market is emerging as a key contributor to South America's cybersecurity landscape, driven by strong enterprise digitalization and growing investments in cybersecurity infrastructure.")

One major growth driver for the endpoint security market is the rising sophistication of cyberattacks and the growing number of connected business devices. Organizations are shifting from traditional antivirus tools toward AI-powered endpoint detection and response solutions to improve protection. Businesses prefer integrated security solutions that provide visibility across endpoints, cloud environments, and user activities. Moreover, industry partnerships and platform integration strategies are further supporting market growth by helping organizations simplify and strengthen security operations. For instance, in January 2026, Next Dimension and Todyl announced a strategic partnership to strengthen cybersecurity capabilities in the endpoint security market. By combining endpoint detection and response, SIEM, and managed security services into a single platform, the partnership helps mid-sized businesses improve threat detection, reduce security complexity, and strengthen cyber defense with a more unified, scalable security approach. The market is also gaining traction, supported by increasing adoption of cloud-based security solutions and rising demand for enterprise-grade cybersecurity tools.

Technology innovation is also supporting market expansion as vendors continue launching modern endpoint security capabilities. Companies are focusing on automation, behavioral analytics, zero-trust security models, and AI-powered monitoring to strengthen protection systems. Endpoint security platforms are evolving beyond antivirus protection to include broader visibility across devices, applications, browsers, and cloud workloads. Organizations are investing in unified security platforms to reduce complexity and improve operational efficiency. These developments are creating long-term opportunities for endpoint security providers globally. The Brazil endpoint security industry is further benefiting from increasing enterprise cybersecurity modernization initiatives across BFSI, IT, and government sectors.

The endpoint security market is expected to maintain strong growth as businesses continue strengthening their cybersecurity infrastructure against evolving threats. Rising digital transformation initiatives, remote working environments, and increased endpoint connectivity will continue to support market demand. Vendors are expected to focus more on AI-based protection, automation, and integrated cybersecurity ecosystems. Organizations across industries are likely to prioritize endpoint security investments to improve resilience and reduce cyber risks. As cybersecurity challenges increase, endpoint security will remain a critical component of enterprise security strategies. The Argentina endpoint security market is projected to grow steadily over the forecast period, supported by rising awareness of advanced threat protection and regulatory compliance requirements.

Market Dynamics

The endpoint security market is growing as businesses need stronger data protection across their environments. Organizations are managing large volumes of sensitive information across laptops, mobile devices, cloud platforms, SaaS applications, and connected systems, creating greater security challenges. Cyberattacks targeting endpoint devices and business data are becoming increasingly sophisticated, prompting companies to adopt intelligent security solutions with real-time monitoring and automated threat response capabilities. Businesses are also looking for unified endpoint security platforms that improve visibility and reduce operational complexity.

For instance, in March 2026, CrowdStrike introduced Falcon Data Security to strengthen endpoint security by protecting sensitive information across endpoints, cloud environments, SaaS applications, browsers, and AI systems. The platform combines AI-powered data classification, real-time threat detection, and automated security enforcement to reduce risks related to data theft and unauthorized access. Such developments highlight how organizations are increasingly investing in advanced endpoint security technologies to improve protection and simplify cybersecurity operations. This growing focus on intelligent, integrated security solutions is expected to continue driving growth in the endpoint security market.

The high total cost of ownership is a major restraint affecting the growth of the endpoint security market. Modern endpoint security platforms increasingly include advanced capabilities such as AI-based threat detection, extended detection and response (XDR), zero-trust security frameworks, cloud workload protection, and automated incident response. While these technologies improve security effectiveness, they also increase deployment, licensing, infrastructure, integration, and maintenance expenses for organizations.

Small and medium-sized businesses are particularly affected because limited IT budgets can make large security investments difficult. In addition to software costs, organizations often require cybersecurity specialists, employee training, and continuous system updates to maintain security performance. As businesses balance security requirements with operational spending, higher ownership costs can slow endpoint security adoption, creating a barrier to broader market expansion despite rising cybersecurity threats.

Market Concentration & Characteristics

The endpoint security market is moderately concentrated, with a mix of large cybersecurity companies and specialized security providers competing across the industry. Major vendors hold a significant market presence due to their broad product portfolios and enterprise customer base, while smaller companies continue to introduce advanced technologies to strengthen competition. The market is witnessing moderate growth, supported by rising cyber threats, increasing cloud adoption, and the expansion of remote work. At the same time, the market growth pace is accelerating as businesses continue increasing investments in endpoint protection solutions to secure devices, applications, networks, and sensitive enterprise data.

The market is also characterized by a high degree of innovation, as companies develop AI-powered threat detection, automation, and real-time monitoring capabilities. Merger and acquisition activity remains moderate to strong, with vendors expanding cybersecurity capabilities and strengthening market position through partnerships and acquisitions. The impact of regulations is high, as organizations increasingly adopt endpoint security solutions to meet data privacy and cybersecurity compliance requirements. The availability of service substitutes remains relatively low because traditional antivirus solutions cannot fully replace advanced endpoint protection platforms. Additionally, end-user concentration is moderate to high, with large enterprises driving significant demand while small and medium-sized businesses continue increasing adoption, supporting long-term market expansion.

Component Insights

The solution segment held the largest market share of 65.0% in 2025. With the rise in cyber threats and sophisticated attacks, organizations are prioritizing stronger endpoint protection to secure business devices and sensitive information. This has created growing demand for comprehensive endpoint security solutions that protect against malware, ransomware, phishing attacks, and other evolving cyber risks. Businesses are increasingly adopting advanced technologies such as AI-driven threat detection, endpoint detection and response (EDR), and automated monitoring to strengthen cybersecurity operations. In addition, the growing adoption of remote work models, cloud platforms, and connected devices is driving demand for integrated endpoint security solutions across industries.

The services segment is projected to register the fastest CAGR over the forecast period. Many organizations need help acquiring and retaining skilled cybersecurity professionals to handle their endpoint security needs. Building an in-house team with the required expertise can be time-consuming and costly. By opting for managed security services or outsourcing their endpoint security needs, organizations can leverage service providers' knowledge and experience through dedicated teams of cybersecurity experts. This allows companies to overcome skill gaps and resource constraints while benefiting from robust endpoint security solutions.

Deployment Insights

The on-premises segment dominated the market, accounting for the largest revenue share in 2025. On-premises deployment offers greater flexibility for customization and integration with existing systems. Companies can tailor the endpoint security solution to meet their requirements, integrating it seamlessly with their other on-premise security tools and infrastructure. This level of customization enables better alignment with existing workflows, security policies, and business processes, resulting in more efficient and effective security management.

The cloud segment is expected to grow at the fastest CAGR over the forecast period. To reduce expenditure and investment, organizations are focusing on adopting cloud-based services. Besides, there is a shift from on-premises to cloud services, as the former requires more maintenance and is more expensive. Cloud-based endpoint security solutions offer centralized management, enabling companies to monitor and manage security measures across their entire network of endpoints from a single console. This centralized approach simplifies security administration, improves visibility into potential threats, and enables faster response times.

Enterprise Size Insights

The large enterprise segment accounted for the large revenue share in 2025. The need to upgrade the existing threat-prevention system is expected to accelerate further the growth of endpoint security services in large enterprises. SMBs' reluctance to outsource security services to third parties is hindering their adoption. However, the rising number of data breaches in these organizations is expected to boost the adoption of endpoint security services over the forecast period.

The SME segment is expected to grow at a significant CAGR over the forecast period. Many SMEs operate in industries with specific data protection and security regulatory requirements, such as healthcare, finance, and legal. Endpoint security solutions help SMEs meet these compliance standards by providing features such as data encryption, access controls, and activity monitoring. By ensuring compliance, SMEs can avoid legal penalties, financial loss, and damage to their reputation.

Application Insights

The BFSI segment held a dominant share in the endpoint security market in 2025 due to the growing need to protect sensitive financial information, digital banking systems, and customer transactions from cyber threats. Financial institutions manage large numbers of endpoints, including employee systems, mobile banking platforms, and cloud-connected applications, making strong endpoint protection essential. The rise in online banking, digital payments, and regulatory compliance requirements is further driving investments in advanced endpoint security solutions that provide real-time monitoring, threat detection, and data protection capabilities.

The healthcare segment is expected to grow significantly, with a CAGR over the forecast period. The healthcare industry has witnessed a surge in cybersecurity threats, including ransomware attacks, data breaches, and malware infections. Cybercriminals target healthcare organizations due to the valuable data they possess and the potential impact on patient safety. These threats have led to increased awareness and investment in endpoint security solutions to protect against malicious activities. Consequently, the healthcare segment has become a significant market for endpoint security vendors.

Regional Insights

The North America endpoint security industry dominated the market, accounting for the largest revenue share of 34.4% in 2025. The region has many key participants offering advanced solutions to segments such as BFSI, automotive, and healthcare. Moreover, North America has stringent compliance requirements and regulations, such as the California Consumer Privacy Act (CCPA) and the General Data Protection Regulation (GDPR). These regulations impose strict data protection and privacy measures on organizations. Endpoint security solutions help organizations meet these compliance requirements by securing sensitive data and preventing unauthorized access or data breaches.

U.S. Endpoint Security Market Trends

The endpoint security industry in the U.S. holds a major position globally due to the high adoption of digital technologies, growing cyberattack risks, and strong cybersecurity investments across industries. Businesses in sectors such as BFSI, healthcare, government, retail, and IT are increasingly deploying endpoint security solutions to protect laptops, mobile devices, servers, and cloud-connected systems from ransomware, phishing attacks, and data breaches. The presence of major cybersecurity companies, the increasing adoption of remote work, and rising regulatory focus on data protection are further supporting growth in the U.S.

The Canada endpoint security industry is expanding steadily, supported by growing awareness of advanced threat protection and increasing demand for enterprise-grade security solutions. In addition, Canada has also witnessed increasing cybersecurity investments and rising adoption of cloud-based security solutions across enterprises.

Europe Endpoint Security Market Trends

The endpoint security industry in Europe holds a significant position in the market due to increasing digital transformation, expanding cloud adoption, and rising cybersecurity investments across industries such as BFSI, healthcare, manufacturing, and government. A major growth driver is the strengthening of cybersecurity and data privacy regulations, including GDPR and regional cyber resilience initiatives, which are encouraging organizations to deploy advanced endpoint protection solutions to secure connected devices, remote work environments, and enterprise networks. The growing frequency of ransomware attacks and sophisticated cyber threats is further accelerating endpoint security adoption, supporting continued market growth across Europe.

The UK endpoint security industry is growing steadily due to increasing cyber threats, expanding digital infrastructure, and higher cybersecurity spending across industries such as BFSI, healthcare, government, and retail. A key growth driver is the rapid rise in hybrid work environments and cloud-based business operations, which has increased the number of endpoints requiring protection against ransomware, phishing, and credential-based attacks. In addition, stronger cybersecurity regulations and growing enterprise focus on data security are encouraging organizations to adopt advanced endpoint protection solutions, supporting long-term market expansion in the UK.

Asia Pacific Endpoint Security Market Trends

The endpoint security industry in the Asia Pacific is experiencing strong growth due to rapid digital transformation, expanding internet penetration, and increasing enterprise cloud adoption across countries such as China, India, Japan, and South Korea, along with Southeast Asian economies. A major regional growth driver is the rapid expansion of mobile banking, digital payment platforms, and e-commerce ecosystems, which is increasing endpoint vulnerabilities and cybersecurity risks across businesses and financial institutions. Rising government cybersecurity initiatives, growing adoption of remote workforces, and increasing investments in advanced endpoint protection technologies are further supporting market expansion, positioning the Asia Pacific as a high-growth region for endpoint security solutions.

The China endpoint security industry is experiencing significant growth due to rapid digital transformation, expanding cloud infrastructure, and theincreasing adoption of connected technologies across industries such as manufacturing, BFSI, government, and telecommunications. A major regional growth driver is China's large-scale industrial digitization and smart manufacturing expansion, supported by initiatives focused on industrial automation, AI integration, and connected enterprise environments, which are increasing the number of endpoints requiring protection. Growing cybersecurity regulations, rising ransomware threats, and increased investments in enterprise security infrastructure are further driving endpoint security adoption, contributing to continued market expansion in China.

Key Endpoint Security Company Insights

Key players in the endpoint industry include CrowdStrike Holdings, Inc., Fortinet, Inc., IBM Corporation, and ESET, spol. s r.o., Check Point Software Technologies Ltd., and others. Companies are focusing on various strategic initiatives, including new product development, partnerships & collaborations, and agreements to gain a competitive advantage over their rivals. The following are some instances of such initiatives.

-

In February 2026, Palo Alto Networks announced the acquisition of Koi, a specialist in agentic endpoint security. This move strengthens Palo Alto’s ability to secure AI agents, plugins, and scripts running on endpoints. It creates a new category, Agentic Endpoint Security (AES), that enhances visibility and control in AI-driven environments when integrated with Cortex XDR and Prisma AIRS.

-

In March 2026, CrowdStrike expanded its Falcon Next-Gen SIEM capabilities by integrating support for Microsoft Defender for Endpoint telemetry without requiring additional endpoint sensors. The enhancement strengthens endpoint security operations by improving real-time threat detection, reducing security management complexity, lowering operational costs, and helping organizations modernize cybersecurity infrastructure across diverse IT environments.

-

In March 2026, Huntress expanded its endpoint security capabilities by introducing Managed Endpoint Security Posture Management (ESPM) and Identity Security Posture Management (ISPM). The solutions help organizations reduce endpoint risks by identifying security gaps, preventing unauthorized access, improving compliance, and strengthening cyber resilience through automated protection and AI-driven security operations.

Key Endpoint Security Companies

The following key companies have been profiled for this study on the endpoint security market.

-

Bitdefender SRL

-

Broadcom Inc.

-

Check Point Software Technologies Ltd.

-

Cisco Systems, Inc.

-

CrowdStrike Holdings, Inc.

-

ESET, spol. s r.o.

-

Fortinet, Inc.

-

IBM Corporation

-

Kaspersky Lab

-

Microsoft Corporation

-

Palo Alto Networks

-

SentinelOne, Inc.

-

Sophos Ltd.

-

Trellix

-

Trend Micro Incorporated

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Mature Players: IBM Corporation; Broadcom Inc.; Palo Alto Networks; Fortinet, Inc.; Trend Micro Incorporated; and Microsoft Corporation

- Focus on integrated cybersecurity ecosystems combining endpoint, network, cloud, and identity security.

- Invest heavily in acquisitions, AI-driven security capabilities, and enterprise platform expansion.

- Strong global customer base and established enterprise relationships across industries.

- Broad product portfolios with large R&D investments and global distribution networks.

- Complex product environments may increase deployment and management challenges.

- Large organizational structures can slow innovation compared to specialized cybersecurity vendors.

Emerging Players: CrowdStrike Holdings, Inc.; SentinelOne, Inc.; Trellix; and Bitdefender SRL

- Focus on AI-powered endpoint protection, cloud-native architectures, and real-time threat intelligence.

- Expand market presence through platform innovation and strategic partnerships.

- Faster innovation cycles and strong specialization in endpoint security technologies.

- Agile product development enables quicker response to evolving cyber threats.

- Smaller enterprise penetration compared to large diversified technology vendors.

- Competitive pressure from established cybersecurity providers with broader security ecosystems.

Endpoint Security Market Report Scope

Report Attribute

Details

Market size in 2025

USD 37.2 billion

Estimated Market size in 2026

USD 41.6 billion

Projected Market size by 2033

USD 95.9 billion

Growth rate

CAGR of 12.7% from 2026 to 2033

Actual data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD Billion and CAGR from 2026 to 2033

Report Coverage

Revenue forecast, company share, competitive landscape, growth factors, and trends

Segments covered

Component; deployment; enterprise size; application; region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; UK; Germany; France; China; India; Japan; Australia; South Korea; Southeast Asia; Brazil; UAE; Kingdom of Saudi Arabia; South Africa

Key companies profiled

Bitdefender SRL; Broadcom Inc.; Check Point Software Technologies Ltd.; Cisco Systems, Inc.; CrowdStrike Holdings, Inc.; ESET, spol. s r.o.; Fortinet, Inc.; IBM Corporation; Kaspersky Lab; Microsoft Corporation; Palo Alto Networks; SentinelOne, Inc.; Sophos Ltd.; Trellix; Trend Micro Incorporated

Customization scope

Free report customization (equivalent to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Endpoint Security Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends across sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global endpoint security market report by component, deployment, enterprise size, application, and region:

-

Component Outlook (Revenue, USD Billion, 2021 - 2033)

-

Solution

-

Antivirus

-

Application Control

-

Endpoint Encryption

-

Endpoint Detection and Response

-

Firewall

-

Mobile Security Tools

-

Others

-

-

Services

-

Consulting

-

Managed

-

Training & Support

-

-

-

Deployment Outlook (Revenue, USD Billion, 2021 - 2033)

-

Cloud

-

On-premise

-

-

Enterprise Size Outlook (Revenue, USD Billion, 2021 - 2033)

-

Large Enterprises

-

SMEs

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

BFSI

-

Healthcare

-

Retail

-

IT & Telecom

-

Government & Defense

-

Industrial

-

Education

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Australia

-

Southeast Asia

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

UAE

-

Saudi Arabia

-

South Africa

-

-

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Region-specific endpoint security market assessment for Europe

Added country-wise market sizing, growth trends, regulatory landscape, cybersecurity investment patterns, and competitive benchmarking for major European countries.

Helped the client identify high-growth regional opportunities and strengthen market entry and expansion strategies with localized business intelligence. The addition of more key players beyond the standard competitive landscape covered in the endpoint security market report.

Expanded company profiling section by adding emerging cybersecurity vendors, startup innovators, product portfolio analysis, strategic developments, and technology positioning.

Provided broader competitive visibility, helping the client understand market competition and identify partnership, acquisition, and differentiation opportunities. Inclusion of additional country-specific endpoint security vendors for the China and Japan markets.

Added country-level cybersecurity companies with analysis of local market presence, endpoint security offerings, strategic initiatives, and regional competitive positioning.

Enabled stronger understanding of domestic competition and supported country-specific business planning, distribution strategies, and regional market penetration decisions. Frequently Asked Questions About This Report

The global endpoint security market size was estimated at USD 37.2 billion in 2025 and is expected to reach USD 41.6 billion in 2026.

The global endpoint security market is expected to grow at a compound annual growth rate of 12.7% from 2026 to 2033 to reach USD 95.9 billion by 2033.

The North America endpoint security market dominated with a share of 34.4% in 2025.

Some key players operating in the endpoint security market include Broadcom, Trend Micro Incorporated, Sophos Ltd., Microsoft, AO Kaspersky Lab, Panda Security, F-Secure, IBM Corporation, McAfee, LLC., ESET, spol. s r.o., Cisco Systems, Inc., and Bitdefender.

Key factors that are driving the market growth include the rising number of enterprise endpoints and mobile devices having access to critical enterprise data, the rise of remote working trends, IoT, regulatory complaints, AI, and machine learning, among others.

The Asia Pacific is the fastest-growing region over the forecast period.

The solution segment led with a 65.0% revenue share in 2025.

On-premises segment dominated the market, accounting for the largest revenue share in 2025.

BFSI segment held a dominated share in the endpoint security market in 2025.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.