- Home

- »

- Advanced Interior Materials

- »

-

Fencing Market Size, Share And Trends Report, 2026-2033GVR Report cover

![Fencing Market (2026 - 2033)Report]()

Fencing Market (2026 - 2033)

Size, Share & Trends Analysis Report By Material, By Distribution Channel, By Installation, By Application (Residential, Agricultural, Industrial), By End Use, By Region, And Segment Forecasts

Market Size, 2025

$33.8BMarket Estimate, 2026

$35.6BMarket Forecast, 2033

$52.4BCAGR, 2026–2033

5.7%Fencing Market Summary

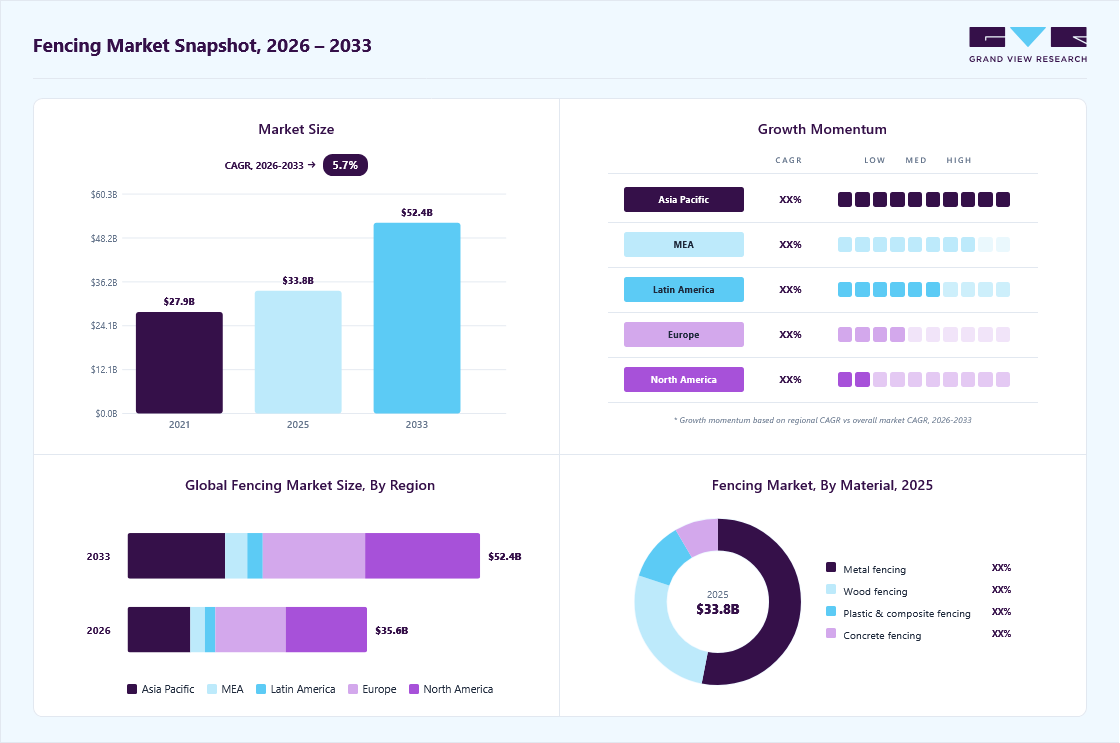

The global fencing market size was valued at USD 33.8 billion in 2025 and is projected to grow from USD 35.6 billion in 2026 to USD 52.4 billion by 2033, at a CAGR of 5.7% from 2026 to 2033. The market in North America dominated with a revenue share of 34.2% in 2025. An unabated rise in new housing construction, home improvement projects, remodeling activities, and commercial construction is expected to drive the growth of the market over the forecast period.

Key Market Trends & Insights

- By material: Metal segment held the largest market share of 53.0% in 2025.

- By application: Residential segment held the largest market share of 62.6% in 2025.

- By distribution channel: Retail segment held the largest market share of 74.1% in 2025.

- By installation: Contractor segment held the largest market share of 78.8% in 2025.

Regional Highlights

- Largest regional market: North America (34.2% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 33.8 Billion

- Estimated market size in 2026: USD 35.6 Billion

- Projected market size by 2033: USD 52.4 Billion

- CAGR (2026-2033): 5.7%

The growing concerns over safety and security coupled with the lower maintenance costs and higher reliability attributes associated with the latest fencing solutions are expected to contribute to the growth of the marketThe demand for fencing products is anticipated to rise in line with the growing need to improve appearance and increase property value, as well as the growing availability of lightweight, affordable, and easy-to-install PVC and plastic fences. As such, cost, quality, design, and aesthetic value are emerging among the major customer criteria. Increased spending on institutional construction and the growing government spending for strengthening the physical security of parks, public places, and government premises also bodes well for the growth of the market.

")

A looming surge in real estate development, growing industrialization, and the aggressive investments public and private organizations are making in the construction industry, especially in emerging countries, such as China and India, are driving the need for physical safety and security solutions. Increasing instances of security breaches and the subsequent need for innovative safety and security solutions are prompting market players to offer enhanced fencing solutions in line with the continuously evolving end-user demands, thereby contributing to the growth of the market.

Eco-friendly fencing is getting popular, but the high level of maintenance eco-friendly fencing requires is driving the demand for low-maintenance fencing solutions, such as vinyl fencing. Plastic fencing is also emerging as a relatively economical, lightweight, and easy-to-install alternative. For farmers looking forward to protecting their property and livestock, market players are offering smart solutions that can provide accurate, data-driven insights. However, the rising number of unlicensed contractors offering inferior products and rising raw material prices are expected to restrain the growth of the market.

Market Concentration & Characteristics

Market growth stage is medium, and pace of the market growth is accelerating. The market can be described as a highly competitive market characterized by a high degree of fragmentation and dominated by a large number of local manufacturers catering to the needs of the customers in their respective regions. At this juncture, innovation and advances in technology and designs would be crucial for market players to cement their position in the market.

There is a medium threat of substitution for the fencing market owing to the presence of cement wall as a fencing substitute. However, the threat of internal substitution is low as no major technology is expected to be developed to replace fencing in the market in the near future.

Prominent players in the market are continuously looking to acquire small or medium-sized players in the market for mergers and acquisitions to maintain their leading positions. There is intense competition among players on a local level. Companies are competing intensely and adopting different marketing and advertising strategies to expand their market share.

Material Insights

The metal segment accounted for the largest revenue share of over 53.0% in 2025. Metal fencing is particularly used in public places and by government organizations. The growing preference for chain links fences and ornamental fences is expected to drive the growth of the segment. The growing need to install a stronger fence to enhance security can also be considered one of the key factors driving the popularity of metal fencing. The growing preference for durable fences that can potentially withstand the changing weather conditions bodes well for the growth of the segment.

The plastic and composite fencing segment is expected to grow at a CAGR of 6.6% over the forecast period, due to its durability, low maintenance, and resistance to weathering, corrosion, and pests. Unlike traditional wood fencing, composite materials do not require frequent painting or sealing, making them a cost-effective long-term solution for residential and commercial users. Increasing environmental awareness is also driving demand, as many composite fences are made from recycled plastics and wood fibers. In addition, advancements in manufacturing technologies have improved the aesthetic appeal of these fences, offering wood-like finishes with enhanced longevity. Growing construction activities, particularly in urban housing and landscaping projects, are further supporting segment growth. The segment is also benefiting from rising consumer preference for sustainable and easy-to-install fencing solutions.

Distribution Channel Insights

The retail segment dominated the market with a revenue share of 74.1% in 2025. The retail distribution channel provides customers with instant access to the products offered by key vendors. It also helps vendors in reducing their marketing budget, thereby contributing to the growth of the segment. Customers looking for customized fences prefer visiting retail stores. Given that customized solutions are rarely available on popular online marketplaces, customers can conveniently visit retail outlets to procure fences as per their requirements.

The online segment is expected to register the fastest growth over the forecast period. There are several benefits associated with online distribution channels. Setting up an online distribution channel calls for relatively lower startup costs as compared to a retail store. Besides, online channels also allow customers to check out all the products on offer and compare those with each other in real time. The growing awareness about the benefits associated with online channels is also encouraging vendors to opt for online distribution channels, thereby driving the growth of the segment.

Installation Insights

The contractor segment dominated the fencing market with a revenue share of 78.8% in 2025. There are several contractors present in the market offering adequate expertise in installing fences according to customers’ suggestions related to aesthetics. Contractors possess material handling capability usually hard to establish on the customers' part. Contractors can also deploy skilled professionals capable of installing fences with utmost efficiency. Hence, customers prefer getting fences installed through contractors. All these factors are allowing the contractor segment to dominate the market.

The Do-It-Yourself segment is poised for significant growth over the forecast period in line with the customers’ growing preference for customized fences. There are numerous Do-It-Yourself (DIY) fencing kits available in the market. In most cases, fences constructed using DIY kits tend to be vinyl fences as they are the easiest to install. However, although installing a fence as a DIY activity can be an option for customers, it is often highly time-consuming. In other words, customers opting for DIY kits may have to cope with a lengthy fence construction process.

Application Insights

The residential segment led the market in 2025 with a revenue share of 62.6%. The increasing residential construction and remodeling activities allowed the segment to dominate the market. The strong emphasis households are putting on security and privacy and the increasing levels of disposable income are driving the investments in fencing products for residential applications. The preference for installing customized fences and enhancing the aesthetic appeal of the residential properties is also emerging as one of the key factors driving the growth of the segment.

The growing need to safeguard farm animals, crops, and farm areas from wild animals and thieves is anticipated to drive the demand for fences for agricultural applications. The rise in the instances of agricultural area intrusions is propelling the demand for fencing for agricultural applications. Fences used in agricultural applications are typically designed and manufactured according to customers’ requirements using good-quality raw materials. Meanwhile, the industrial segment is anticipated to grow in line with the growing demand for fencing solutions from industrial and manufacturing units.

End Use Insights

The military & defense segment accounted for the largest market share in 2025. The growing need for adequate border control and safety is expected to drive the growth of the segment. Meanwhile, the energy & power segment is expected to emerge as the fastest-growing End Use segment over the forecast period. The growing demand for high-security fencing, such as anti-cut and anti-climb perimeter fencing and partitioning to protect critical power grid infrastructure is estimated to drive the growth of the segment over the forecast period.

Petroleum companies and chemical companies are making significant investments in upgrading their existing refineries and processing plants as well as developing new industrial infrastructure. Activities carried out in these facilities often involve the release of hazardous chemicals and gases, which can be harmful to both trespassers and other individuals invading the premises knowingly or unknowingly. Hence, these companies are installing strong and durable fencing to counter any potential instances of trespassing, thereby driving the growth of the petroleum & chemicals segment.

Regional Insights

North America dominated the fencing market in 2025 with a revenue share of 34.2%. The unabated growth in construction activities across North America is allowing the region to dominate the global market. The U.S. alone is home to more than 50,000 fence contractors. These contractors provide materials and services around the world. The regional market is also poised for significant growth over the forecast period. The growing demand for home decoration products from households across North America is estimated to drive the growth of the regional market.

U.S. Fencing Market Trends

U.S. dominated the fencing market in North America region in 2025. The U.S. fencing market is driven by residential construction and increasing demand for privacy and security. Homeowners are investing in decorative and customized fencing solutions. Technological integration, such as automated gates and surveillance-linked fencing, is gaining popularity. The commercial sector also contributes significantly, particularly in warehouses and industrial facilities. Demand for sustainable materials is rising. Replacement and repair activities further boost market growth. Overall, innovation and customization define the U.S. market.

Asia Pacific Fencing Market Trends

The Asia Pacific regional market is anticipated to register the fastest CAGR over the forecast period. The growing concerns over safety among consumers and the initiatives being pursued by various governments in the region to develop and improve public infrastructure are expected to contribute to the growth of the regional market. Continued urbanization and the strong emphasis farmers are putting on safeguarding their property and assets are anticipated to drive the growth of the regional market. The increased spending on institutional construction in India also bodes well for the growth of the regional market.

China Fencing Market Trends

China’s fencing market is driven by large-scale infrastructure projects and industrial expansion. The country’s focus on urban development and smart city initiatives is increasing demand for advanced fencing systems. Agricultural fencing is also growing due to modernization in farming practices. Domestic manufacturers dominate the market with cost-effective solutions. Export-oriented production further strengthens China’s position globally. The adoption of metal and smart fencing is rising steadily. Government investments in public safety infrastructure are also contributing to market growth.

Europe Fencing Market Trends

Europe’s fencing market is influenced by strict regulations related to safety and environmental sustainability. Demand is high in residential and public infrastructure sectors. The region is witnessing increased adoption of eco-friendly fencing materials. Modern architectural trends are driving the demand for aesthetically pleasing fencing solutions. Agricultural fencing remains important in rural economies. Technological advancements in security fencing are also gaining traction. Western Europe leads the market due to higher spending capacity.

Germany is a key market in Europe, driven by industrial growth and infrastructure development. The country emphasizes high-quality and durable fencing solutions. Demand for metal and automated fencing systems is particularly strong. Sustainability and environmental compliance play a crucial role in product selection. Residential applications also contribute significantly to market demand. Technological innovation in security fencing is a major trend. Germany’s well-established construction sector supports steady growth.

Latin America Fencing Market Trends

Latin America is experiencing moderate growth in the fencing market due to increasing urbanization and security concerns. Residential and commercial sectors are the primary contributors. Economic development and infrastructure investments are driving demand. The adoption of cost-effective fencing materials is common in the region. Agricultural fencing is also significant, especially in rural areas. Brazil and Mexico are key markets. However, economic volatility may impact growth to some extent.

Middle East & Africa Fencing Market Trends

The Middle East & Africa region is witnessing growing demand for fencing due to infrastructure development and security requirements. Investments in commercial and industrial projects are key drivers. High-security fencing is particularly important in oil & gas and defense sectors. Urbanization and smart city initiatives are boosting adoption. The use of durable materials suitable for harsh climatic conditions is increasing. Government regulations and large-scale projects support market growth. The region offers significant opportunities for expansion.

Key Fencing Company Insights

The market players are extensively adopting various inorganic growth strategies, including mergers and acquisitions, to consolidate their market position amid a competitive environment. Market players are primarily focusing on acquiring local players as the latter have a dedicated customer base. Vendors are also focusing on increasing their product penetration by leveraging their product offerings and broader geographical footprint to serve customers across the globe and by pursuing cross-selling opportunities.

Key Fencing Companies:

The following key companies have been profiled for this study on the fencing market.

- Allied Tube & Conduit

- Ameristar Fence Products Incorporated

- Associated Materials LLC

- Bekaert

- Betafence NV

- CertainTeed Corporation

- Gregory Industries, Inc.

- Jerith Manufacturing Company Inc.

- Long Fence Company Inc.

- Ply Gem Holdings Inc.

- Poly Vinyl Creations Inc.

Recent Developments

-

In January 2025, Ply Gem Holdings Inc. launched Catalyst Fence Solutions, consolidating multiple fencing brands into a unified platform for residential markets.

-

In August 2024, Poly Vinyl Creations Inc. expanded its PVC fencing product lines, focusing on low-maintenance residential solutions.

-

In July 2024, Gregory Industries, Inc. opened a new G-STRUT manufacturing facility in Alabama, strengthening infrastructure-related product capabilities.

Fencing Market Report Scope

Report Attribute

Details

Market size in 2025

USD 33.8 billion

Estimated Market size in 2026

USD 35.6 billion

Projected Market size by 2033

USD 52.4 billion

Growth rate

CAGR of 5.7% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, competitive landscape, growth factors, and trends

Segments covered

Material, distribution channel, installation, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Middle East & Africa; Latin America

Country scope

U.S.; Canada; Germany; France; Italy; UK; Belgium; Poland; China; Japan; India; Brazil; Mexico; Saudi Arabia; UAE

Key companies profiled

Allied Tube & Conduit; Ameristar Fence Products Incorporated; Associated Materials LLC; Bekaert; Betafence NV; CertainTeed Corporation; Gregory Industries, Inc.; Jerith Manufacturing Company Inc.; Long Fence Company Inc.; Ply Gem Holdings Inc.; Poly Vinyl Creations Inc.

Customization scope

Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Fencing Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For the purpose of this study, Grand View Research has segmented the global fencing market report on the basis of material, distribution channel, installation, application, end use, region:

-

Material Outlook (Revenue, USD Billion, 2021 - 2033)

-

Metal

-

Wood

-

Plastic & Composite

-

Concrete

-

-

Distribution Channel Outlook (Revenue, USD Billion, 2021 - 2033)

-

Online

-

Retail

-

-

Installation Outlook (Revenue, USD Billion, 2021 - 2033)

-

Do-It-Yourself

-

Contractor

-

-

Application Outlook (Revenue, USD Billion, 2021 - 2033)

-

Residential

-

Agricultural

-

Industrial

-

-

End Use Outlook (Revenue, USD Billion, 2021 - 2033)

-

Government

-

Petroleum & Chemicals

-

Military & Defense

-

Mining

-

Energy & Power

-

Transport

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Belgium

-

Poland

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Latin America

-

Brazil

-

Mexico

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

-

Frequently Asked Questions About This Report

The global fencing market is expected to grow at a CAGR of 5.7% from 2026 to 2033 to reach USD 52.4 billion by 2033.

North America dominated the fencing market with a share of 34.2% in 2025.

Some key players operating in the fencing market include CertainTeed Corporation; Bekaert; Ameristar Fence Products Incorporated; Allied Tube & Conduit; and Ply Gem Holdings Inc.

Key factors that are driving the fencing market growth include rising interest in home enhancement, increasing disposable income, increasing residential and commercial projects, and rising preference for personal safety and security.

The global fencing market size was estimated at USD 33.8 billion in 2025 and is expected to reach USD 35.6 billion in 2026.

Metal segment led with a 53.0% revenue share in 2025.

Residential segment held the largest revenue share 62.6% in 2025.

Retail fencing segment held the largest share (over 74.1%) in 2025.

Contractor segment led with a 78.8% revenue share in 2025.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.