- Home

- »

- Medical Devices

- »

-

Fluoroscopy Systems Market Size, Share Report, 2026-2033GVR Report cover

![Fluoroscopy Systems Market (2026 - 2033)Report]()

Fluoroscopy Systems Market (2026 - 2033)

Size, Share & Trends Analysis Report By Product, By Application (Orthopedic, Cardiovascular, Pain Management & Trauma, Neurology), By End Use (Hospitals & Specialty Clinics, Diagnostic Imaging centers), By Region, And Segment Forecasts

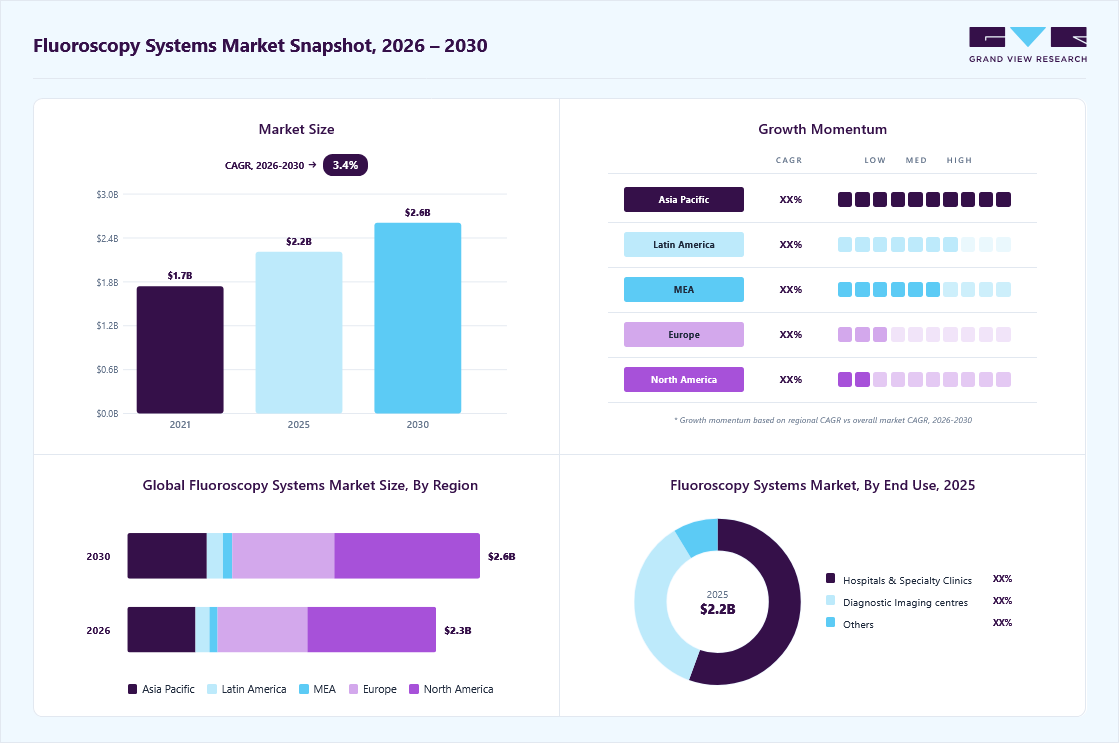

Market Size, 2025

$2.2BMarket Estimate, 2026

$2.3BMarket Forecast, 2033

$2.9BCAGR, 2026–2033

3.4%Fluoroscopy Systems Market Summary

The global fluoroscopy systems market size was valued at USD 2.2 billion in 2025 and is projected to grow from USD 2.3 billion in 2026 to USD 2.9 billion by 2033, at a CAGR of 3.4% from 2026 to 2033. North America dominated the market with the largest revenue share of 42.1% in 2025. The growing geriatric population, chronic diseases, and increasing adoption of fluoroscopy in pain management are key drivers of the market.

Key Market Trends & Insights

- By product: C-arms segment accounted for the largest revenue share of 64.6% in 2025.

- By application: Cardiovascular segment dominated the market with a revenue share of over 29.2% in 2025.

- By end-use: Hospitals & specialty clinics segment led the market with a share of 55.5% in 2025.

Regional Highlights

- Largest regional market: North America (42.1% revenue share, 2025)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 2.2 Billion

- Estimated market size in 2026: USD 2.3 Billion

- Projected market size by 2033: USD 2.9 Billion

- CAGR (2026-2033): 3.4%

For instance, in October 2025, the World Health Organization reported that the global population is aging rapidly, with the proportion of people aged 60 years and above expected to nearly double from 12% in 2015 to 22% by 2050. The organization also noted that by 2030, one in six people worldwide will be aged 60 years or older, reflecting a significant rise in the geriatric population and increasing healthcare needs associated with ageing and chronic diseases. In addition, advancements in fluoroscopy technology, including the shift to digital imaging, methods to reduce radiation dose, incorporation with other imaging techniques, and improved visualization aids, are further driving the market's expansion. These technological advancements enhance the quality of images, safety for patients, and efficiency in procedures, broadening the use of fluoroscopy in various medical settings.")

The increasing frequency of long-term illnesses such as heart issues, stomach problems, and bone-related injuries requires more sophisticated methods for diagnosis and treatment through imaging. Fluoroscopy is essential for diagnosing and treating these conditions, leading to a high demand for fluoroscopy equipment and services. One of the primary drivers of demand is the rising global prevalence of chronic diseases, particularly cardiovascular disorders. Cardiovascular diseases remain the leading cause of death globally and account for nearly 30% of all deaths worldwide, highlighting the growing burden of conditions that require imaging-guided diagnostic and therapeutic procedures. Many cardiovascular treatments, including angiography, catheterization, and stent placement, rely heavily on fluoroscopic imaging to guide instruments within blood vessels in real time. As the number of patients requiring these procedures increases, hospitals are expanding their imaging capabilities, further boosting demand for fluoroscopy systems.

Due to the increasing number of elderly individuals around the globe, there is a growing need for diagnostic imaging tests to help with heart diseases, arthritis, and cancer. The increasing use of fluoroscopy in minimally invasive interventional procedures across various medical fields, including cardiology, orthopedics, oncology, and urology, as well as the growing adoption of image-guided interventions such as angiography, spinal surgeries, and tumor ablations, indicate significant opportunities for market expansion. Increasing healthcare costs, along with advances in medical technology and favorable payment policies, are driving encourage the worldwide adoption of fluoroscopy equipment and services.

Technological innovation in imaging systems is another key factor driving the market. Modern fluoroscopy platforms now incorporate digital flat-panel detectors, advanced image processing, and radiation-dose-reduction technologies, significantly improving image quality while minimizing radiation exposure for patients and healthcare professionals. Research published in Scientific Reports has highlighted the development of real-time radiation monitoring systems that can reduce physician radiation exposure during fluoroscopy-guided procedures by providing immediate feedback during imaging.

The growing trend towards point-of-care imaging solutions, known for their portability, flexibility, and ease of use, is supported by portable fluoroscopy systems, handheld devices, and mobile C-arm units to meet the evolving needs of healthcare providers, particularly in emergency departments, ambulatory surgery centers, and remote areas. The increasing use of minimally invasive surgical techniques, driven by faster recovery times, shorter hospital stays, and lower complication rates, is fueling the popularity of fluoroscopy-guided interventions. Fluoroscopy enables precise visualization and guidance during these procedures, thus driving market growth.

Market Dynamics

Growing geriatric population, chronic diseases and increasing adoption of fluoroscopy in pain management are key drivers fueling market. For instance, in October 2025, the World Health Organization reported that the global population is ageing rapidly, with the proportion of people aged 60 years and above expected to nearly double from 12% in 2015 to 22% by 2050. The organization also noted that by 2030, one in six people worldwide will be aged 60 years or older, reflecting a significant rise in the geriatric population and increasing healthcare needs associated with ageing and chronic diseases. In addition, advancements in fluoroscopy technology, including the shift to digital imaging, methods to reduce radiation dose, incorporation with other imaging techniques, and improved visualization aids, are further driving the market's expansion. These technological advancements enhance the quality of images, safety for patients, and efficiency in procedures, broadening the use of fluoroscopy in various medical settings.

The increasing frequency of long-term illnesses such as heart issues, stomach problems, and bone-related injuries require more sophisticated methods for diagnosis and treatment through imaging. Fluoroscopy is essential for diagnosing and treating these conditions, leading to a high demand for fluoroscopy equipment and services. One of the primary drivers of demand is the rising global prevalence of chronic diseases, particularly cardiovascular disorders. Cardiovascular diseases remain the leading cause of death globally and account for nearly 30% of all deaths worldwide, highlighting the growing burden of conditions that require imaging-guided diagnostic and therapeutic procedures. Many cardiovascular treatments, including angiography, catheterization, and stent placement, rely heavily on fluoroscopic imaging to guide instruments within blood vessels in real time. As the number of patients requiring these procedures increases, hospitals are expanding their imaging capabilities, further boosting demand for fluoroscopy systems.

Despite significant improvements in dose-management technologies, fluoroscopy remains dependent on ionizing radiation. Prolonged or repeated procedures can increase cumulative radiation exposure for both patients and healthcare professionals. Hospitals and regulatory bodies are therefore placing greater emphasis on radiation safety protocols, which can sometimes limit procedure utilization and create additional compliance requirements. According to the U.S. FDA, fluoroscopic procedures can expose patients to radiation doses that are substantially higher than those associated with conventional diagnostic X-ray examinations, particularly during lengthy or complex interventional procedures.

Market Concentration & Characteristics

The fluoroscopy systems market is moderately concentrated, with leading companies such as GE HealthCare, Siemens Healthineers, Koninklijke Philips NV, and Canon Medical Systems Corporation holding significant shares of the market. These players offer advanced fluoroscopy technologies, including fixed fluoroscopy systems, mobile C-arm systems, and digital fluoroscopy platforms, enabling improved real-time imaging, enhanced procedural accuracy, and better patient outcomes. The market is continuously evolving due to technological advancements in imaging software, flat-panel detectors, dose-reduction technologies, and integration with minimally invasive surgical procedures. In addition, the rising prevalence of chronic diseases, increasing demand for image-guided diagnostic and interventional procedures, and growing adoption of fluoroscopy in cardiology, orthopedics, and gastrointestinal applications are driving market growth and encouraging companies to introduce innovative and high-performance fluoroscopy solutions.

The industry is experiencing significant technological advancements and innovations, including the integration of artificial intelligence (AI), advanced flat-panel detectors, automated dose-reduction technologies, and hybrid imaging platforms that enhance real-time visualization, diagnostic precision, and workflow efficiency during complex procedures such as cardiovascular interventions, orthopedic surgeries, and gastrointestinal examinations. For instance, in December 2024, Siemens Healthineers introduced the Luminos Q.namix platform, a next-generation fluoroscopy and radiography system designed with AI-supported workflow optimization, automated imaging controls, and improved ergonomics to enhance productivity and image quality in radiology departments. These technological advancements are expected to drive the growth of the fluoroscopy systems market.

Partnerships and collaborations play a significant role in the fluoroscopy systems industry, enabling medical imaging companies and healthcare institutions to integrate advanced imaging technologies, improve diagnostic accuracy, and enhance clinical workflows for image-guided procedures. Through such collaborations, healthcare providers gain access to next-generation imaging platforms, including fluoroscopy-guided interventional systems, AI-enabled imaging software, and hybrid operating room technologies that support minimally invasive treatments.

Regulatory approval plays a crucial role in shaping the market by ensuring that imaging equipment meets strict safety, quality, and radiation protection standards before use in clinical settings. Authorities such as the U.S. Food and Drug Administration (FDA) and the European Medical Device Regulation (MDR) classify fluoroscopy systems as medical devices, requiring manufacturers to comply with rigorous regulatory frameworks covering device design, radiation safety, manufacturing quality systems, and clinical performance. In the United States, fluoroscopic X-ray systems are typically regulated as Class II medical devices under 21 CFR 892.1650, meaning manufacturers must demonstrate safety and effectiveness through regulatory pathways such as the 510(k) premarket notification process before commercialization. For instance, in July 2025, the U.S. Food and Drug Administration (FDA) granted 510(k) clearance to Siemens Healthineers for its Luminos Q.namix R and Luminos Q.namix T radiography and fluoroscopy systems.

Product substitutes in the market for fluoroscopy systems include computed tomography (CT) scanners, magnetic resonance imaging (MRI) systems, ultrasound imaging systems, nuclear medicine imaging (PET/SPECT), and endoscopy-based diagnostic techniques, which are widely used for diagnostic imaging and procedural guidance in hospitals. For example, CT and MRI are commonly preferred for detailed cross-sectional imaging of organs and tissues, enabling physicians to evaluate conditions such as tumors, vascular abnormalities, and internal injuries with high spatial resolution. Ultrasound imaging is frequently used as a radiation-free alternative for real-time visualization in procedures such as obstetrics, cardiology, and abdominal examinations.

Regional expansion is gaining momentum across major global regions, driven by increasing demand for real-time diagnostic imaging, the rising prevalence of chronic diseases, and the growing adoption of minimally invasive procedures. Medical imaging companies are actively expanding their geographical presence through strategic partnerships with hospitals and government healthcare programs, distribution agreements, and the installation of advanced imaging infrastructure in emerging healthcare markets. These initiatives help manufacturers strengthen their market reach while improving access to fluoroscopy-guided diagnostic and interventional procedures in developing regions.

Analyst Perspective

The fluoroscopy systems market is positioned at the intersection of several long-term healthcare trends, including the increasing adoption of minimally invasive procedures, growing demand for real-time image-guided interventions, and continuous advancements in diagnostic imaging technologies. The rising prevalence of cardiovascular diseases, orthopedic disorders, gastrointestinal conditions, urological disorders, and neurological diseases is creating significant opportunities for fluoroscopy system manufacturers and healthcare providers as clinicians increasingly rely on real-time imaging to improve procedural accuracy and patient outcomes. In addition, the expanding use of fluoroscopy across interventional cardiology, orthopedic surgery, pain management, trauma care, and vascular procedures, coupled with the ongoing shift toward outpatient and ambulatory surgical settings, is driving demand for both fixed fluoroscopy systems and mobile C-arms.

Product Insights

Based on product, the C-arms segment led the market with the largest revenue share of 64.6% in 2025. Key drivers of market growth include a growing elderly population, increasing chronic disease rates, improved maneuverability and imaging technology, and higher demand for imaging tech from emerging markets. Moreover, mobile C-arms offer real-time guidance during procedures across a hospital, cutting the need for patient transfers, streamlining workflows, and potentially lowering costs. In addition to that, manufacturers are creating compact, lightweight, user-friendly mobile C-arms with enhanced image quality, which may create an impact on the growth of the market. For instance, in February 2024, Royal Philips launched the Zenition 90 Motorized mobile C-arm system, designed to support complex interventional procedures such as cardiac interventions, vascular procedures, and urology. The system features motorized positioning, user-friendly controls, and high-power imaging capabilities that allow surgeons to operate the device directly from the table side while delivering high-quality real-time images.

Fixed fluoroscopy devices are expected to register a robust CAGR over the forecast period. Continual advancements in fluoroscopy machines, for instance, in March 2025, Canon Medical Systems USA announced the launch of the Adora DRFi system, a hybrid imaging platform that integrates digital radiography and low-dose fluoroscopy into a single system. The platform allows hospitals to perform both static and dynamic imaging in the same room, improving diagnostic workflow efficiency and supporting advanced interventional procedures. This shift toward digital imaging, reduced doses, combined with other imaging methods, and improving visualization tools, is driving market growth. In addition, as the global population continues to age, there is an increasing need for diagnostic imaging to detect problems related to aging, such as heart disease, joint inflammation, and tumors. The increasing use of fluoroscopy in minimally invasive interventional procedures across medical fields such as cardiology, orthopedics, oncology, and urology, paired with the growing popularity of image-guided interventions such as angiography, spinal surgeries, and tumor ablations, indicates significant opportunities for market expansion.

Application Insights

Based on application, the cardiovascular segment led the market with the largest revenue share of 29.2% in 2025. According to the World Health Organization, cardiovascular diseases (CVDs) are the primary reason for global mortality. The increased prevalence results in a higher demand for diagnostic and interventional procedures using fluoroscopy. For instance, as per the data published by the World Health Organization in July 2025, Cardiovascular diseases (CVDs) are the leading cause of death globally, responsible for about 19.8 million deaths in 2022, representing around 32% of all global deaths. This highlights the strong demand for fluoroscopy systems in cardiovascular treatment procedures. Fluoroscopy is essential for various cardiovascular procedures such as coronary angiography, stenting, and electrophysiology studies. These procedures are less invasive than open surgery due to fluoroscopy guidance. In addition to that, manufacturers are continuously enhancing fluoroscopy systems to cater to the specific requirements of cardiovascular procedures. Flat-panel detectors and improved image processing technologies have led to a substantial market presence for cardiovascular applications in the global fluoroscopy systems market.

The orthopedic segment is expected to register the fastest CAGR during the forecast period. Fluoroscopy is essential in minimally invasive orthopedic procedures such as arthroscopy, kyphoplasty, bone fracture reduction, and Joint replacement surgery. Minimally invasive techniques are increasingly used in orthopedic procedures such as bone fracture reduction, joint replacements, and spine surgeries. For example, in May 2025, a study published in Nature Scientific Reports evaluated different techniques for C1-C2 pedicle screw placement in spinal surgery, comparing O-arm navigation, 3D-printed guides, and traditional C-arm fluoroscopy guidance. The research highlighted that fluoroscopy remains a widely used imaging method in orthopedic spine procedures because it provides real-time intraoperative visualization that assists surgeons in accurate screw placement and surgical navigation. These highlight the continued importance of fluoroscopy-guided imaging in minimally invasive orthopedic surgeries and spinal fixation procedures.

End Use Insights

Based on end-use, the hospitals & specialty clinics segment led the market with the largest revenue share of 55.5% in 2025. In hospitals, a variety of medical conditions are treated that require the fluoroscopic guidance. This covers a range of procedures from less intrusive surgeries such as gallbladder removal or cardiac catheterization to injections for pain management and reducing fractures. Hospitals usually have the resources to acquire advanced fluoroscopy systems. These systems provide functions such as high-quality imaging, reduced radiation exposure, and robotic arms for better control. Moreover, rising installation of fluoroscopy systems across these facilities highlights the segment’s growth. For instance, in November 2024, Morton Plant Hospital installed the Omega E-View AI fluoroscopy system from Omega Medical Imaging to support its endoscopy program. The system improves imaging quality and can reduce radiation exposure by up to 84%, enhancing patient and clinician safety during image-guided procedures. Specialized clinics often emphasize particular characteristics related to their specialty. In a cardiology clinic, having a fluoroscopy system with high-quality images of blood vessels is a top priority. Health facilities regularly update technology to give optimal patient care, and fluoroscopy plays a crucial role in this effort.

Diagnostic imaging centers are expected to register the fastest CAGR during the forecast period. The rapid growth is due to patients’ preference for outpatient imaging services over hospitals, driven by factors such as shorter wait times and flexible scheduling. Diagnostic imaging centers focus on meeting these needs by offering a range of imaging techniques, such as fluoroscopy. There is a growing trend among diagnostic imaging centers to focus on specific areas, such as musculoskeletal imaging and women's health. Fluoroscopy is used in multiple procedures in these fields, making it worthwhile for these facilities to purchase specialized fluoroscopy systems.

Regional Insights

North America dominated the fluoroscopy systems market with the largest revenue share of 42.1% in 2025, primarily driven by well-established healthcare infrastructure, increasing geriatric population, rapid technological advancements, and the growing use of fluoroscopy in pain management and cardiovascular procedures. The region also experiences a high burden of chronic diseases, particularly cardiovascular disorders, which significantly increases the demand for advanced imaging technologies used in interventional procedures. According to the American Heart Association’s latest statistics update, cardiovascular disease remains the leading cause of death in the United States, with approximately 915,973 deaths reported in 2023, meaning that one person dies from cardiovascular disease every 34 seconds. The rising prevalence of cardiovascular diseases has led to an increasing number of diagnostic and interventional procedures, such as angioplasty, cardiac catheterization, and vascular imaging, many of which rely heavily on fluoroscopy systems for real-time imaging guidance. The strong presence of advanced hospitals, ambulatory surgical centers, and specialized pain management clinics also supports the widespread adoption of fluoroscopy systems across the region.

U.S. Fluoroscopy Systems Market Trends

The fluoroscopy systems market in the U.S. held the largest share in the North America region in 2025 due to the rising incidence of trauma and injuries, including sprains, muscle sprains, and supraspinatus tendinitis. According to recent injury statistics from the National Safety Council, exercise and exercise equipment alone accounted for approximately 564,845 injuries in the U.S. in 2024, making it the leading cause of sports and recreational-related injuries treated in medical facilities. In addition, around 4.4 million people were treated in U.S. emergency departments for sports and recreational injuries in 2024, with activities such as cycling, basketball, and fitness training contributing significantly to the injury burden. The increasing number of emergency visits related to musculoskeletal injuries is expected to boost the demand for advanced medical imaging technologies, including fluoroscopy systems used in orthopedic and trauma procedures.

Europe Fluoroscopy Systems Market Trends

The fluoroscopy systems industry in Europe was identified as a lucrative region in 2025 due to the increasing need for less invasive procedures, expanding elderly demographic, and the rising utilization of fluoroscopy in managing pain. Moreover, in Europe, there is a high prevalence of medical conditions that require fluoroscopy, such as cardiovascular diseases and gastrointestinal disorders, and there has been an increase in the adoption of advanced healthcare solutions and investments in innovative technologies. According to recent data from the European Commission and OECD, cardiovascular diseases remain the leading cause of death in the European Union, accounting for around 1.7 million deaths annually and affecting nearly 62 million people across the region. The rising burden of cardiovascular disorders has increased the demand for diagnostic imaging and interventional procedures such as cardiac catheterization, angioplasty, and vascular interventions, which rely heavily on fluoroscopy systems for real-time imaging guidance. This highlights the rising demand for fluoroscopy systems across the region.

The UK fluoroscopy systems industry is expected to grow rapidly in the coming years, due to a rise in technological advancements, greater affordability rates for treatments, and the annual growth in the number of diagnostic procedures. Besides, the increasing incidence of neurological conditions, such as brain tumors are projected to drive market growth. According to Cancer Research UK and the UK Parliament research briefing (2026), more than 12,000 people are diagnosed with a primary brain tumour in the UK each year, highlighting the significant burden of neurological diseases that require advanced imaging for diagnosis and treatment planning. Additionally, the demand for imaging services in the UK continues to rise; NHS England reported about 47.2 million imaging tests conducted in England in the year ending March 2024, representing a 4.8% increase from the previous year, reflecting the expanding utilization of diagnostic imaging technologies across the healthcare system. These factors are expected to drive the adoption of fluoroscopy systems for diagnostic and interventional procedures in the UK.

The fluoroscopy systems industry in Germanyheld a substantial market share in 2025. Germany is a dominant player in the European medical technology sector, with significant participation from major companies such as Siemens Healthineers. In addition, the healthcare system is strong and involves significant expenditure. This has the potential to increase the investment rate in cutting-edge fluoroscopy technology. Moreover, Germany is experiencing a rapid population aging. This shift is expected to increase the need for fluoroscopy procedures in the realms of diagnosis and treatment.

Asia Pacific Fluoroscopy Systems Market Trends

The fluoroscopy systems industry in the Asia Pacific is anticipated to witness significant growth. Main factors fueling the market include an increasing need for minimally-invasive surgeries, a growing elderly population, the high occurrence of chronic diseases, and a rise in the use of fluoroscopy for pain management. The growing burden of chronic diseases has further increased the need for diagnostic and interventional procedures, including cardiovascular and gastrointestinal interventions that rely on fluoroscopy for real-time imaging guidance, thereby supporting the growth of the market in the region.

The Japan fluoroscopy systems industry is expected to grow rapidly in the coming years. As life expectancy increases, demand for medical procedures that involve fluoroscopy for diagnosis and treatment may increase. According to data from Japan’s Ministry of Internal Affairs and Communications, the number of people aged 65 and older reached about 36.19 million in 2025, accounting for around 29.4% of Japan’s total population, the highest proportion among major developed economies. The growing elderly population increases the incidence of age-related conditions such as cardiovascular diseases, gastrointestinal disorders, and orthopedic problems that require image-guided procedures. In addition, Japanese companies such as Shimadzu Corporation and Hitachi Medical Systems are leading in fluoroscopy technology in Japan. Technological Improvements such as flat-panel detectors that provide clearer images and reduce radiation exposure, make these systems more appealing to healthcare professionals.

Latin America Fluoroscopy Systems Market Trends

The fluoroscopy systems industry in Latin America is witnessing steady growth due to the increasing burden of chronic diseases, the rising demand for minimally invasive procedures, and expanding healthcare infrastructure across the region. Cardiovascular diseases remain a major public health challenge in Latin America, with more than 2 million deaths annually attributed to cardiovascular conditions, according to the Pan American Health Organization (PAHO). The high prevalence of hypertension and heart disease has significantly increased the number of diagnostic and interventional procedures, such as angiography, cardiac catheterization, and vascular interventions, all of which rely heavily on fluoroscopic imaging for real-time visualization during treatment.

The Brazil fluoroscopy systems industry is growing steadily, supported by the rising burden of cardiovascular diseases, increasing adoption of minimally invasive procedures, and continuous improvements in healthcare infrastructure across the country. The high prevalence of hypertension, obesity, and diabetes has led to a growing number of interventional cardiology procedures such as angiography, cardiac catheterization, and angioplasty, all of which require fluoroscopic imaging for real-time visualization during treatment. As a result, hospitals and cardiac care centers are increasingly investing in fluoroscopy systems to support these procedures.

Middle East & Africa Fluoroscopy Systems Market Trends

The fluoroscopy systems industry in the Middle East and Africa is experiencing steady growth, supported by the rising burden of chronic diseases, expanding healthcare infrastructure, and increasing adoption of minimally invasive procedures across the region. Non-communicable diseases such as cardiovascular diseases, diabetes, and cancer are increasing significantly in both the Middle East and parts of Africa due to urbanization, aging populations, and lifestyle changes. Fluoroscopy plays a critical role in procedures such as angiography, cardiac catheterization, gastrointestinal studies, and orthopedic interventions, which is driving its demand in hospitals and specialized care centers.

The Saudi Arabia fluoroscopy systems industry is expanding steadily, driven by the rising burden of cardiovascular diseases, increasing demand for minimally invasive procedures, and strong government investments in healthcare infrastructure. Cardiovascular diseases represent a significant health challenge in the country, with studies indicating that around 1.6% of the Saudi population aged 15 years and older has diagnosed cardiovascular disease, with prevalence increasing significantly among older age groups. These conditions require interventional procedures such as coronary angiography, cardiac catheterization, and vascular interventions, all of which rely on fluoroscopic imaging for real-time guidance during diagnosis and treatment. As the incidence of cardiovascular disorders and related risk factors continues to rise, hospitals and cardiac care centers across Saudi Arabia are increasing the adoption of advanced fluoroscopy systems to support these procedures.

Key Fluoroscopy Systems Company Insights

The fluoroscopy systems market is highly competitive with several key players. The major market players are focusing on expanding their geographical presence, forming partnerships, and enhancing their product portfolios with advanced imaging technologies, leveraging strategic collaborations, and exploring mergers and acquisitions.

Key Fluoroscopy Systems Companies:

The following key companies have been profiled for this study on the fluoroscopy systems market

-

Canon Medical Systems Corporation.

-

Hitachi Medical Systems

-

Siemens Healthineers

-

Koninklijke Philips NV

-

GE HealthCare

-

Ziehm Imaging GmbH

-

Shimadzu

-

Orthoscan Inc.

-

Hologic Inc.

-

Carestream Health.

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (GE Healthcare, Siemens Healthineers, Koninklijke Philips N.V., UMG/Del Medical)

- Focus on expanding comprehensive fluoroscopy portfolios that include fixed fluoroscopy systems, mobile C-arms, hybrid operating room solutions, and interventional imaging platforms. Invest heavily in flat-panel detector technology, dose-reduction software, AI-enabled image enhancement, and integrated workflow solutions to improve procedural efficiency. Strengthen market presence through long-term hospital partnerships, service contracts, equipment replacement programs, and expansion into emerging healthcare markets.

- Strong brand recognition and long-standing relationships with hospitals, imaging centers, and healthcare systems worldwide. Extensive installed base and service networks create recurring revenue opportunities through maintenance agreements, software upgrades, and equipment replacements. Broad imaging portfolios spanning radiography, CT, MRI, ultrasound, and fluoroscopy enable bundled purchasing agreements and cross-selling opportunities. Significant R&D capabilities support continuous innovation in image quality, radiation safety, and interventional imaging technologies.

- High research, manufacturing, and regulatory compliance costs associated with advanced imaging systems. Dependence on hospital capital expenditure budgets can result in delayed purchasing decisions during periods of economic uncertainty. Large organizational structures may slow product development cycles and limit flexibility in addressing niche market requirements. Increasing pricing pressure from regional manufacturers and refurbished equipment providers may affect margins.

Emerging Players (Canon Medical Systems, Shimadzu Corporation, Dornier MedTech)

- Focus on cost-effective fluoroscopy solutions, mobile C-arms, and specialty imaging systems designed for orthopedic, pain management, and outpatient surgical applications. Emphasize affordability, ease of use, and compact system designs to target ambulatory surgical centers, specialty clinics, and mid-sized hospitals. Expand market penetration through distributor partnerships, flexible financing models, and localized service support. Focus on niche applications and incremental technological innovations to differentiate from larger competitors.

- Greater operational flexibility enables faster response to customer needs and market opportunities. Ability to offer competitively priced systems appealing to budget-conscious healthcare providers and emerging markets. Strong focus on specialized applications and customized solutions can create differentiation in underserved clinical segments. Leaner organizational structures often support faster implementation of product enhancements and customer support initiatives.

- Limited financial resources and smaller global distribution networks compared with multinational imaging leaders. Lower brand recognition and a smaller installed base can create challenges in securing large hospital contracts and government tenders. Limited service infrastructure and post-sales support capabilities may restrict geographic expansion. Greater exposure to regulatory approval delays, pricing competition, and rapid technological advancements introduced by established market participants.

Recent Developments

-

In August 2025, Paris Regional Health announced that it added the advanced GE P180 Fluoroscopy System to its diagnostic imaging services, enhancing its ability to perform a wide range of procedures with superior imaging quality, lower radiation exposure, and improved workflow, marking a significant upgrade in patient care and diagnostic efficiency.

-

In July 2023, Canon Medical Systems launched a multipurpose fluoroscopic table with new functions, Zexira i9 digital X-ray RF system. It is a digital X-ray RF system which is equipped with all the essential features to meet clinical demands.

Fluoroscopy Systems Market Report Scope

Report Attribute

Details

Market size in 2025

USD 2.2 billion

Estimated market size in 2026

USD 2.3 billion

Projected market size by 2033

USD 2.9 billion

Growth rate

CAGR of 3.4% from 2026 to 2033

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Product, application, end use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; China; Japan; India; South Korea; Australia; Thailand; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait;

Key companies profiled

Canon Medical Systems Corporation; Hitachi Medical Systems; Siemens Healthineers; Koninklijke Philips NV; GE HealthCare; Ziehm Imaging GmbH; Shimadzu; Orthoscan Inc.; Hologic Inc.; Carestream Health.

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Fluoroscopy Systems Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global fluoroscopy systems market report based on product, application, end use, and region

-

Product Outlook (Revenue, USD Million, 2021 - 2033)

-

Fixed Fluoroscopy Devices

-

C-arms

-

Mini C-arms

-

Full-size C-arms

-

-

-

Application Outlook (Revenue, USD Million, 2021 - 2033)

-

Orthopedic

-

Cardiovascular

-

Pain Management & Trauma

-

Neurology

-

Gastrointestinal

-

Urology

-

General Surgery

-

Others

-

-

End Use Outlook (Revenue, USD Million, 2021 - 2033)

-

Hospitals & Specialty Clinics

-

Diagnostic Imaging centers

-

Others

-

-

Regional Outlook (Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East and Africa (MEA)

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Research Methodology

Segment Definition

Segment - Product

Revenue capture definition

Fixed Fluoroscopy Devices

Revenue is generated through the sale and installation of fixed fluoroscopy systems used in hospitals, interventional suites, and diagnostic imaging departments. Manufacturers derive income from equipment sales, software licenses, image-processing upgrades, service and maintenance contracts, system integration services, and replacement components. Additional revenue is generated through long-term support agreements and workflow optimization solutions that enhance procedural efficiency and imaging performance.

C-arms

Revenue is generated from the commercialization of mobile and mini C-arm imaging systems used in surgical, orthopedic, cardiovascular, and pain management procedures. Market participants earn revenue from equipment sales, software enhancements, service contracts, accessories, replacement parts, and imaging upgrades. Recurring income is also derived from maintenance services, training programs, and technology upgrades that improve image quality and radiation dose management.

Segment - Application

Revenue capture definition

Orthopedic

Revenue is generated through the utilization of fluoroscopy systems during fracture fixation, joint replacement procedures, spinal surgeries, and trauma interventions. Demand is driven by the need for real-time imaging guidance to improve surgical precision and procedural outcomes.

Cardiovascular

Revenue is derived from the use of fluoroscopy systems in diagnostic and interventional cardiology procedures, including angiography, angioplasty, stent placement, electrophysiology studies, and structural heart interventions. Increased adoption of minimally invasive cardiovascular procedures supports revenue growth in this segment.

Pain Management & Trauma

Revenue is generated from fluoroscopy-guided pain management procedures such as epidural injections, nerve blocks, radiofrequency ablations, and trauma-related interventions. Healthcare providers utilize fluoroscopic imaging to improve procedural accuracy and patient safety, contributing to equipment demand.

Neurology

Revenue flows from the use of fluoroscopy systems in neurovascular interventions, spinal procedures, cerebrospinal fluid management, and other neurological applications requiring real-time imaging guidance. Growth is supported by increasing adoption of minimally invasive neurological procedures.

Gastrointestinal

Revenue is generated through fluoroscopy-assisted gastrointestinal examinations and interventions, including barium studies, endoscopic procedures, feeding tube placements, and therapeutic gastrointestinal treatments. The segment benefits from the continued need for dynamic visualization of digestive tract functions and abnormalities.

Urology

Revenue is derived from fluoroscopic imaging used during urinary tract evaluations, stone removal procedures, stent placements, and other urological interventions. The need for accurate real-time imaging during minimally invasive urological procedures supports market demand.

General Surgery

Revenue is generated from the application of fluoroscopy systems across a broad range of surgical procedures requiring intraoperative imaging guidance. These systems assist surgeons in device placement, anatomical visualization, and procedural navigation, supporting equipment utilization and replacement demand.

Others

Revenue is generated from fluoroscopy applications across additional clinical specialties, including pulmonology, gynecology, vascular surgery, and emergency medicine. Growth is supported by the expanding use of image-guided procedures across diverse healthcare settings.

Segment – End-use

Revenue capture definition

Hospitals & Specialty Clinics

Revenue is generated through the procurement and utilization of fluoroscopy systems in hospitals, multispecialty healthcare facilities, and specialized clinics. Demand is driven by high procedural volumes, increasing adoption of minimally invasive interventions, equipment upgrades, and investments in advanced imaging infrastructure. Manufacturers also generate recurring revenue through maintenance agreements, software updates, and service contracts.

Diagnostic Imaging Centres

Revenue is derived from fluoroscopy systems used in dedicated imaging centers for diagnostic examinations and outpatient procedures. Income is supported by growing demand for cost-effective diagnostic services, imaging workflow optimization, and equipment modernization initiatives aimed at improving patient throughput and image quality.

Others

Revenue is generated from fluoroscopy system utilization in ambulatory surgical centers, academic and research institutions, military healthcare facilities, and other healthcare settings. Market participants earn revenue through equipment sales, service agreements, and technology upgrades tailored to specialized clinical requirements.

Estimation Model

Step Title

Guiding Question

Process Steps

Data Sources

Scope Definition

What is being studied?

- Define the market and include equipment used for the market (key imaging/diagnostic modalities and interventional procedures). - Segment the market by product type and application. - Set geographic boundaries (e.g., regions). - Align volume base for market inclusion (2018–2028).

Annual reports, SEC filings, revenue presentations, company websites

Build the Product Base

How large is the end-use market for our company base?

- Identify key players (top manufacturers) and understand business-specific revenue split (Company Annual Reports/SEC filings). - Map company data on product offerings including different technology volumes and revenues. - Analyze regional revenue distribution using company disclosures, sales footprints, and annual reports. - Establish the final product base using key variables in the final volume mapping system.

Company annual reports, investor presentations, revenue statements, product catalogs

Estimate Penetration

Where is the frequency demand generated?

- Assess installed base of fluoroscopy systems using trade data, specifications, and usage trends. - Equalize procedure volumes across major application areas including cardiovascular, orthopedic, gastrointestinal, urology, and others. - Estimate penetration based on current procedure volumes and exam areas. - Adjust final base values using procurement trends, replacement rates, and installed base growth.

Annual reports, healthcare facility inventories, government healthcare reports

Revenue Conversion

How is total revenue calculated and projected?

- Analyze average selling prices (ASPs) of fluoroscopy systems across product categories and regions. - Understand base equipment pricing, equipment age cycles, and inflation before finalizing ASPs. - Forecast demand and revenue growth trends based on replacement rates, installed base growth, and procedure volumes. - Translate volume metrics into revenue based on average selling prices, installed base, and replacement rates.

Annual reports, distributor price listings, healthcare expenditure databases

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Added

E2E and B2C Analysis of Fluoroscopy System Market

Conducted a comprehensive assessment of the fluoroscopy systems value chain across both business-to-business (B2B) and business-to-consumer (B2C) channels. The study evaluated procurement pathways among hospitals, specialty clinics, diagnostic imaging centers, ambulatory surgical centers, and government healthcare institutions, including purchasing models such as direct sales, distributor-led sales, leasing agreements, and managed equipment services. The analysis further examined end-user demand drivers influencing procedure volumes, including the growing adoption of minimally invasive interventions, outpatient surgical procedures, and patient preferences for image-guided treatments. Additionally, the study assessed stakeholder relationships among manufacturers, distributors, healthcare providers, payers, and patients to understand purchasing and utilization dynamics.

This enables stakeholders to understand the complete fluoroscopy ecosystem, identify high-value customer segments, and recognize emerging business models influencing purchasing behavior across healthcare settings. Supports strategic decision-making for manufacturers in optimizing product portfolios and identifying new opportunities in outpatient and ambulatory care segments that drive future equipment demand.

U.S.-Specific Fluoroscopy System Market Analysis

Conducted a detailed assessment of the U.S. fluoroscopy systems market, including relevant healthcare infrastructure, hospital density, imaging center distribution, procedural volumes, reimbursement frameworks, and capital equipment replacement trends. The study evaluated regional adoption patterns for fixed fluoroscopy systems and C-arms across key clinical applications such as cardiovascular interventions, orthopedics, pain management, gastrointestinal procedures, and urology. Further, the analysis incorporated macroeconomic factors, healthcare expenditure, outpatient procedure trends, and regulatory requirements, including safety standards and equipment replacement life cycles on market growth across different states and healthcare systems.

This analysis enables stakeholders to identify high-growth states and healthcare networks, assess regional demand variations, and evaluate reimbursement and regulatory investment opportunities. Supports strategic expansion initiatives, distributor partnerships, and procurement planning for manufacturers by providing a granular understanding of fluoroscopy system adoption across the U.S. healthcare landscape.

Market Analysis Based on CPT Codes

Conducted a detailed analysis of the fluoroscopy systems market using relevant Current Procedural Terminology (CPT) codes associated with fluoroscopy-guided diagnostic and interventional procedures. The study evaluated procedure volumes, reimbursement trends, site-of-service shifts, and adoption patterns across cardiovascular, orthopedic, pain management, gastroenterology, urology, and general surgical applications. Additionally, the analysis mapped out code-based procedure volumes by hospital and outpatient utilization rates, identifying future demand generation by specialty, healthcare setting, and geographical region. The study further examined the influence of reimbursement frameworks on future procedure growth and equipment procurement decisions.

This analysis enables stakeholders to quantify demand drivers using procedural-level data, identify high-volume and high-growth clinical applications, evaluate reimbursement trends, and forecast future equipment adoption using CPT-based volume forecasts. Supports product positioning, sales optimization, and resource targeting, helping manufacturers and distributors align fluoroscopy system portfolios with procedural activity and revenue-generating demand trends.

Frequently Asked Questions About This Report

Key factors that are driving the market growth include the growing geriatric population, chronic diseases and the increasing adoption of fluoroscopy in pain management.

The C-arms segment led the market with the largest revenue share of 64.6% in 2025.

The global fluoroscopy systems market size was estimated at USD 2.2 billion in 2025 and is expected to reach USD 2.3 billion in 2026.

Some key players operating in the fluoroscopy systems market include Canon Medical Systems Corporation, Hitachi Medical Systems, Siemens Healthineers, Koninklijke Philips NV, GE HealthCare, Shimadzu Corporation, and Carestream Health, among others.

North America dominated the fluoroscopy systems market, accounting for 42.1% in 2025. This is attributable to the well-established healthcare infrastructure, increasing geriatric population, rapid technological advancements, and the growing use of fluoroscopy in pain management and cardiovascular procedures.

Asia Pacific is the fastest-growing region over the forecast period.

Cardiovascular segment accounted for the largest revenue share of 29.2% in 2025, while orthopedics is the fastest-growing segment.

Hospitals & specialty clinics held the largest revenue share of 55.5% in 2025, while diagnostic imaging centers is the fastest-growing segment

The global fluoroscopy systems market is expected to grow at a compound annual growth rate of 3.4% from 2026 to 2033 to reach USD 2.9 billion by 2033.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.