- Home

- »

- Next Generation Technologies

- »

-

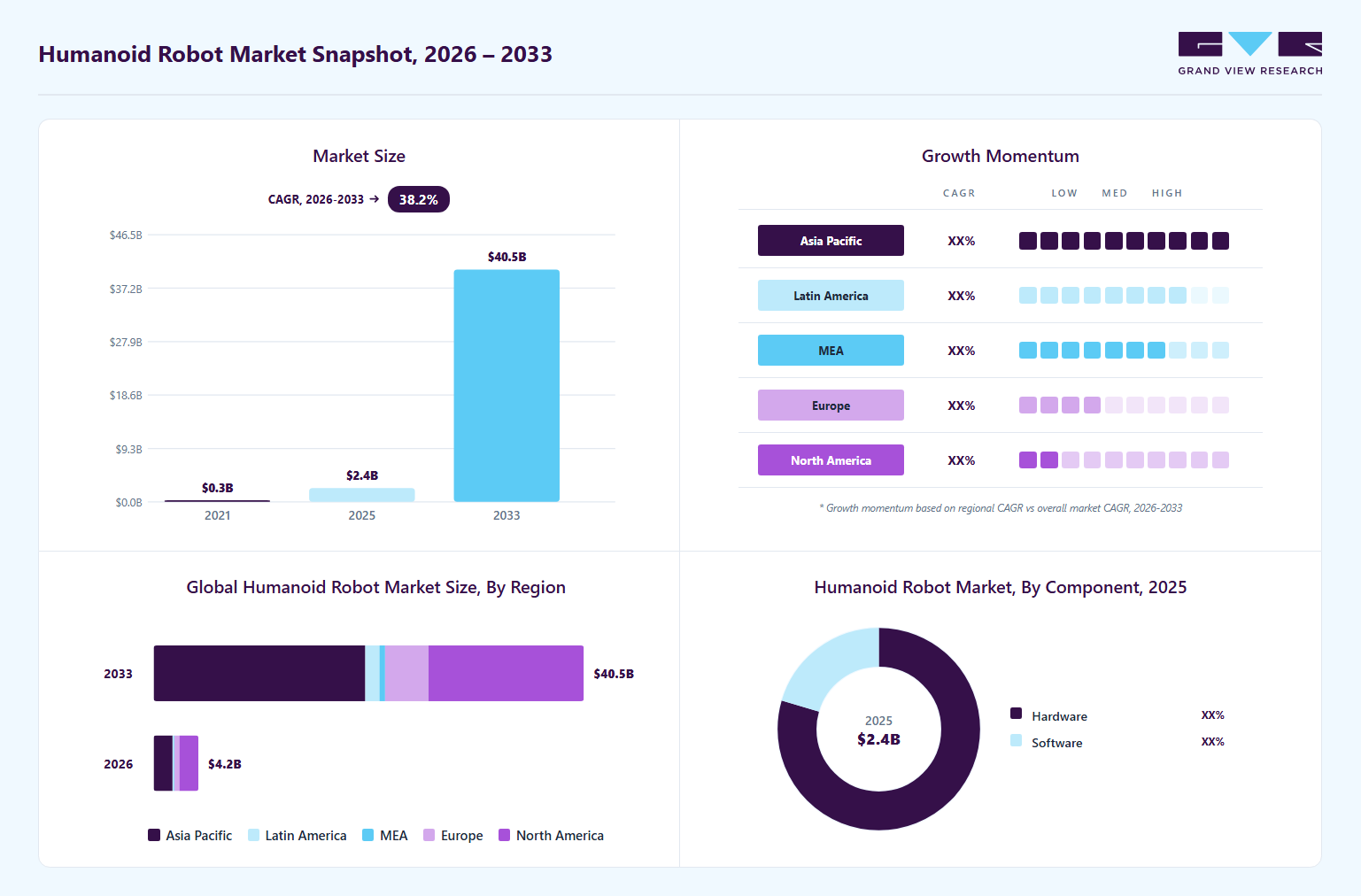

Humanoid Robot Market Size, Share & Growth Report, 2033GVR Report cover

![Humanoid Robot Market Size, Share & Trends Report]()

Humanoid Robot Market (2026 - 2033) Size, Share & Trends Analysis Report By Component (Hardware, Software), By Application (Manufacturing, Logistics & Warehousing, Healthcare, Retail & E-commerce), By Motion Type (Biped, Wheel Drive), By Region, And Segment Forecasts

Market Size, 2025

$2.4BMarket Estimate, 2026

$4.2BMarket Forecast, 2033

$40.5BCAGR, 2026–2033

38.2%Humanoid Robot Market Summary

The global humanoid robot market size was valued at USD 2.4 billion in 2025 and is projected to grow from USD 4.2 billion in 2026 to USD 40.5 billion by 2033, at a CAGR of 38.2% from 2026 to 2033. North America dominated the global market, accounting for the largest revenue share of 43.4% in 2025. The demand for humanoid robots is projected to reach more than 900,000 units by 2033, a significant jump from the 15,000 units as observed in 2025.

Key Market Trends & Insights

- By component: Hardware segment accounted for the largest revenue share of 79.4% in 2025.

- By motion type: Biped segment dominated the market with a revenue share of over 71.0% in 2025.

- By application: Manufacturing segment led the market with a share of 31.9% in 2025.

Regional Highlights

- Largest regional market: North America (43.4% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The U.S. held the largest market share in 2025

Market Size & Forecast

- Market size in 2025: USD 2.4 Billion

- Estimated market size in 2026: USD 4.2 Billion

- Projected market size by 2033: USD 40.5 Billion

- CAGR (2026-2033): 38.2%

The market growth is driven by increasing investments in AI-driven humanoid robotics R&D, expanding use of humanoid robots across industrial and service sectors, rising adoption of Industry 4.0 and automation technologies, growing labor shortages, and continuous advancements in mobility, battery efficiency, and human-robot interaction. The humanoid robot industry is expanding rapidly, owing to major advancements in artificial intelligence, machine learning, computer vision, and robotics engineering. These technologies are enabling humanoid robots to perform complex, human-like tasks with greater autonomy and adaptability. Continuous improvements in perception, reasoning, navigation, and motion control are enabling robots to operate more effectively in dynamic, unstructured environments. As a result, humanoid robots are transitioning from research and pilot-stage applications toward broader real-world deployment across industries such as manufacturing, logistics, healthcare, retail, and personal assistance.")

Additionally, the increasing implementation of advanced artificial intelligence and robotic perception technologies is anticipated to strengthen robotic autonomy, enhance operational precision, and enable humanoid robots to safely operate within dynamic industrial and human-centric environments. The growing focus on intelligent automation, human-robot collaboration, and workplace safety, along with digital transformation across manufacturing, logistics, healthcare, and retail, is driving investments in humanoid robotic platforms and supporting the growth of the humanoid robot industry.

Furthermore, the global labor shortage across industries such as manufacturing, logistics, healthcare, and retail is becoming increasingly critical. This challenge is being intensified by aging populations and a declining pool of skilled workers in many regions. Humanoid robots are emerging as an effective solution to handle repetitive, physically demanding, and hazardous tasks. Their ability to seamlessly operate within existing human-centric environments further enhances their adoption potential.

Moreover, the application scope of humanoid robots is expanding beyond industrial settings into service-oriented sectors. Industries such as hospitality, education, defense & security, and personal assistance are increasingly using humanoid robots for interactive, customer-facing roles. These applications include customer service, training assistance, surveillance, and companionship services. This diversification is significantly widening the humanoid robot industry's potential and expanding the overall demand base.

Market Dynamics

The rapid advancement and adoption of AI-driven robotics technologies are significantly fueling demand for humanoid robots across manufacturing, logistics, healthcare, retail, and service-oriented industries. Organizations are increasingly integrating humanoid robots to automate repetitive and labor-intensive tasks, enhance operational efficiency, and mitigate persistent workforce shortages.

For instance, in February 2026, Agility Robotics expanded the deployment of its humanoid robot Digit at Toyota Motor Corporation’s Canada facility for warehouse and production support tasks, such as tote handling and material movement. This reflects growing adoption of AI-powered humanoid robots to automate repetitive work, improve efficiency, and address labor shortages in manufacturing and logistics.

Furthermore, the growing advancements in generative AI, edge computing, and real-time data analytics are enhancing decision-making capabilities and operational intelligence, thereby supporting the large-scale commercialization and integration of humanoid robots across diverse end-use industries. Overall, the ongoing advancements are accelerating the widespread adoption and commercialization of humanoid robots globally.

The humanoid robot industry faces substantial challenges due to the high development costs and technical complexity of advanced robotic systems. Advanced components such as precision actuators, high-resolution sensors, AI processing units, and energy-efficient power systems significantly increase the overall cost of humanoid robots. In addition, the integration of complex hardware and software systems requires specialized expertise, further raising development expenses and limiting affordability for many end users.

Moreover, the lack of standardization across robotics platforms adds to technical complexity and slows down large-scale commercialization. Many enterprises face challenges in system compatibility, maintenance, and long deployment cycles, which restrict widespread adoption. These factors collectively make it difficult for small and mid-sized organizations to invest in humanoid robotics solutions on scale.

A significant opportunity in the humanoid robot market is the growing investment from governments, tech giants, and startups in artificial intelligence and advanced robotics development. These investments are accelerating research and development to improve the intelligence, mobility, and energy efficiency of humanoid robots. Strong funding support is also enabling faster prototyping, testing, and commercialization of next-generation humanoid platforms.

Additionally, the growing collaboration between robotics companies, AI developers, and academic institutions is fostering innovation and technological breakthroughs. This is leading to the development of more capable, affordable, and scalable humanoid robots that can be deployed across diverse industries. With expanding global R&D efforts, the market is expected to witness faster product evolution and wider commercial adoption.

Market Concentration & Characteristics

The humanoid robot market is moderately concentrated, with a mix of established robotics companies, diversified technology giants, and emerging startups actively competing for technological leadership and commercialization. The market is characterized by a high degree of innovation, driven by rapid advancements in AI, machine learning, computer vision, and robotics hardware, which are continuously improving humanoid capabilities and expanding real-world applications.

Additionally, the level of M&A activities is medium, as strategic partnerships and selective acquisitions are increasing, but the market is still in an early-to-growth stage where organic R&D remains dominant. The impact of regulations is low to medium, as most regions are still developing dedicated frameworks for humanoid robotics, though safety and AI governance standards are gradually evolving.

Furthermore, the threat of product substitutes is medium, as traditional industrial robots, collaborative robots (cobots), and software automation solutions can partially replace humanoid robots in certain applications. Moreover, end-user concentration is medium to high, since early adoption is primarily driven by industries such as manufacturing, logistics, and technology-forward enterprises, while broader consumer and service sector adoption is still emerging.

Analyst Perspective

The humanoid robot market is rapidly emerging in AI-driven automation, supported by advances in embodied AI, robotics hardware, and human-robot interaction technologies that enable operation in complex, human-centric environments. Growth is being driven by rising labor shortages, increasing demand for flexible automation across manufacturing, logistics, healthcare, and service sectors, and the broader shift toward Industry 4.0 and smart industrial ecosystems. Expanding real-world pilot deployments and growing investments from technology leaders and startups are accelerating commercialization, positioning humanoid robots as scalable, general-purpose automation platforms for the next phase of industrial transformation.

Component Insights

The hardware segment accounted for the largest market share of 79.4% in 2025, driven by the high cost, complexity, and essential role of physical components required to build humanoid robots. Key elements such as advanced sensors, actuators, control systems, power supply units, and precision-engineered structural frameworks form the core foundation of these robots and significantly contribute to overall system value. The ongoing enhancements in materials, robotics engineering, and Motion Type control technologies are further strengthening the demand for advanced hardware.

The software segment is expected to register the fastest CAGR of over 45.0% from 2026 to 2033. This growth is attributed to rapid advancements in artificial intelligence, machine learning, deep learning, and robotic operating systems that are enhancing the cognitive and functional capabilities of humanoid robots. Furthermore, the rising demand for autonomous decision-making, adaptive learning systems, and enhanced human-robot collaboration is driving continuous innovation in robotics software platforms, thereby accelerating deployment across industrial and service applications.

Motion Type Insights

The biped motion type segment dominated the humanoid robot market, accounting for a revenue share of over 71.0% in 2025, driven by its ability to replicate human locomotion, enabling humanoid robots to navigate environments designed for people, such as stairs, uneven terrain, and narrow pathways. Additionally, the increasing demand for human-like interaction in industrial, service, and defense applications is further supporting the adoption of biped humanoid robots, as they can seamlessly integrate into human-centric workflows without requiring infrastructure modifications.

The wheel drive segment is expected to witness a significant CAGR from 2026 to 2033. This growth is attributed to continuous improvements in autonomous navigation, sensor fusion, and AI-based path planning, which are enhancing operational efficiency and enabling reliable performance in repetitive material-handling and service tasks. Furthermore, their lower cost, higher energy efficiency, and ease of deployment in structured environments such as warehouses and retail spaces are further accelerating adoption across industrial applications.

Application Insights

The residential segment is expected to grow at the fastest CAGR of over 45.0% from 2026 to 2033. This growth is attributed to the growing demand for personal assistance, elderly care, and home automation solutions as aging populations increase and lifestyles become more technology-oriented. Furthermore, continuous improvements in human-robot interaction, natural language processing, and affordability are gradually making humanoid robots more suitable for domestic environments, supporting long-term growth potential in the consumer market.

The manufacturing segment accounted for the largest share of the humanoid robot industry in 2025, driven by the increasing need for automation in repetitive, precision-based, and hazardous industrial tasks such as assembly, inspection, welding support, and material handling. Additionally, rising labor shortages and growing pressure to improve productivity and operational efficiency are encouraging manufacturers to adopt humanoid robots that can seamlessly operate in existing factory environments, which is further driving the segmental growth.

Regional Insights

The North America dominated the global humanoid robot market with the largest revenue share of 43.4% in 2025, fueled by strong technological leadership in artificial intelligence, robotics, and advanced automation systems, supported by significant investments from both private companies and government initiatives. The region is witnessing rising adoption of humanoid robots across manufacturing, logistics, healthcare, and defense sectors due to acute labor shortages and high operational costs.

U.S. Humanoid Robot Market Trends

The U.S. humanoid robot industry accounted for the largest share of over 86.0% in 2025, driven by significant investments in defense robotics and Industry 4.0 initiatives, which are strengthening the development and real-world deployment of humanoid systems. Additionally, rapid advancements in AI-driven robotics, strong participation from tech giants and startups, and increasing deployment of humanoid robots in industrial and service applications.

Europe Humanoid Robot Market Trends

The Europe humanoid robot industry is expected to grow at a CAGR of over 36.0% from 2026 to 2033. In Europe, the market is driven by a strong focus on industrial automation, workplace safety regulations, and increasing adoption of smart manufacturing practices. Countries across the region are investing in robotics to address labor shortages caused by aging populations and to improve productivity in manufacturing and logistics sectors.

The UK humanoid robot market is growing steadily, supported by strong investments in AI, robotics research, and automation across healthcare, logistics, and service sectors. For instance, the UK government, through UK Research and Innovation (UKRI) and related robotics programs, has been actively funding robotics and AI development to strengthen innovation and commercialization in the sector. These initiatives are helping advance humanoid robotics applications in assistive care, education, and industrial services.

The humanoid robot market in Germany is rapidly expanding, driven by its strong industrial automation base and leadership in Industry 4.0 adoption across the manufacturing and automotive sectors. For instance, Germany’s High-Tech Strategy 2025 supports research and innovation in robotics and smart manufacturing to enhance industrial competitiveness. Combined with strong investment in automation and digitalization, these initiatives are enabling increased use of advanced robotics and supporting long-term development of humanoid robot applications in industrial environments.

Asia Pacific Humanoid Robot Market Trends

The Asia Pacific humanoid robot industry is expected to register the fastest CAGR of over 41.0% from 2026 to 2033, driven by rapid industrialization, expanding manufacturing, and strong government support for robotics and AI development. Countries in the region are increasingly adopting humanoid robots to enhance productivity, reduce labor dependency, and improve operational efficiency across multiple sectors.

The Japan humanoid robot market is gaining traction, driven by the need to address labor shortages and an aging population. For instance, the government's Robot Care and Welfare Strategy promotes the development of humanoid robots for elderly care, rural healthcare support, and interaction research. Furthermore, the Ministry of Economy, Trade and Industry (METI) allocates approximately JPY 90 billion annually to support domestic manufacturing and deployment of assistive robotic technologies.

The humanoid robot market in China is witnessing robust expansion, driven by strong government support and industrial development initiatives. For instance, the country designated humanoid robotics as a strategic priority under its 14th Five-Year Plan and AI Development Agenda, while committing over USD 138 billion toward robotics and AI development between 2021 and 2025. Such initiatives are accelerating commercialization, enhancing domestic manufacturing capabilities, and positioning China as a leading global market for humanoid robot development and deployment.

The South Korea humanoid robot market is supported by substantial public investments in next-generation robotics. For instance, the government allocated approximately KRW 2.5 trillion (around USD 1.8 billion) for the development of emotionally responsive humanoid robots and announced subsidies covering up to 70% of R&D costs. These initiatives are accelerating innovation in healthcare, education, and service-oriented humanoid applications.

Key Humanoid Robot Company Insights

Some of the key players operating in the market are SoftBank Robotics and UBTECH Robotics Inc.

-

SoftBank Robotics is a Japan-based robotics company that develops humanoid and service robots for human interaction and commercial use cases. It is known for robots such as Pepper and NAO, which are widely deployed in education, retail, hospitality, and research settings. In the humanoid robot market, SoftBank Robotics plays an important role in the early-stage commercialization of social humanoids, focusing on customer interaction, service automation, and enterprise-level robot deployment across global markets.

-

UBTECH Robotics Inc. is a China-based robotics company developing AI-powered humanoid robots and intelligent service robotics systems. The company has created advanced humanoids such as the Walker series, designed for household assistance, education, and industrial environments. In the humanoid robot industry, UBTECH is a key Chinese player focused on scaling humanoid adoption, integrating AI, computer vision, and motion control technologies to expand use cases across consumer and enterprise segments.

1X Technologies and Engineered Arts Limited are some of the emerging participants in the humanoid robot market.

-

1X Technologies is a robotics technology provider developing AI-driven humanoid robots designed for real-world environments. The company builds general-purpose humanoids such as NEO, aimed at home assistance and service tasks, with a focus on human-centric design and autonomous learning capabilities. In the humanoid robot market, 1X Technologies is positioned as an emerging player targeting household robotics and labor-assist applications, using advanced AI and actuation systems to enable practical real-world deployment.

-

Engineered Arts Limited is an emerging robotics company specializing in highly expressive humanoid robots designed for entertainment, research, and AI interaction applications. The company’s Ameca humanoid platform, known for advanced facial animation, modular robotics architecture, and realistic human-like expressions, supports next-generation human-machine communication and immersive robotic interaction experiences. Continuous investments in AI-integrated robotics software and interactive humanoid systems are strengthening Engineered Arts Limited’s market presence in the humanoid robot industry.

Key Humanoid Robot Companies

The following key companies have been profiled for this study on the humanoid robot market.

-

1X Technologies

-

Agility Robotics, LLC

-

Apptronik

-

Boston Dynamics

-

Engineered Arts Limited

-

Figure AI

-

Fourier Intelligence

-

Hanson Robotics Limited

-

Honda Motor Co., Ltd.

-

Kawada Robotics Corporation

-

Kepler Robotics (Hangzhou Kolin Electric Co., Ltd.)

-

LimX Dynamics Inc.

-

NVIDIA Corporation

-

National Aeronautics and Space Administration (NASA)

-

PAL Robotics S.L.

-

Promobot Corp.

-

Robo Garage Co., Ltd.

-

RobotEra

-

ROBOTIS Co., Ltd.

-

Samsung Electronics Co., Ltd.

-

Sanctuary Cognitive Systems Corporation

-

SoftBank Robotics Group Corp.

-

Tesla, Inc.

-

Toshiba

-

Toyota Motor Corporation

-

UBTECH Robotics Inc.

-

Unitree

-

WowWee Group Limited

-

Xiaomi

-

XPENG, Inc.

Competitive Benchmarking

Operating Strategies

Competitive Edge

Weaknesses

Established Players: SoftBank Robotics, UBTECH Robotics Inc., Agility Robotics, LLC

- Focus on expanding AI-powered service robotics ecosystems through cloud and automation partnerships.

- Invest heavily in humanoid robotics R&D for scalable customer interaction and healthcare solutions.

- Strong global deployment network supports large-scale humanoid robot commercialization.

- Advanced conversational AI capabilities strengthen personalized human-robot interaction and operational efficiency leadership.

- Dependence on service robotics markets may limit diversification across industrial automation applications.

- High operational costs can reduce profitability amid increasing competition from emerging robotics startups.

Emerging Players: Engineered Arts Limited, Promobot Corp., Robo Garage Co., Ltd

- Focus on advancing AI-powered humanoid robotics through automation, conversational AI, and research partnerships.

- Invest heavily in expressive robotics, intelligent mobility systems, and scalable humanoid platform development.

- Advanced human-robot interaction technologies strengthen personalization, engagement, and immersive communication.

- Flexible innovation-driven business models support rapid humanoid robotics customization across emerging commercial applications.

- Limited manufacturing scale may restrict large-volume humanoid robot commercialization and global market penetration.

- Smaller operational structures can face funding limitations against established multinational robotics technology competitors.

Recent Developments

-

In June 2026, NVIDIA Corporation unveiled a humanoid robotics reference platform (Isaac GR00T / H2+) in partnership with Unitree and Sharpa, designed to accelerate development of general-purpose humanoid robots

-

In May 2026, Tesla expanded deployment of its humanoid robot Optimus Gen 3 at the Fremont factory, with reports indicating 1,000+ units operating on live production lines performing tasks such as battery handling, parts sorting, and assembly support.

-

In May 2026, SoftBank Robotics expanded its strategic partnership with Direct Supply to accelerate the deployment of autonomous robotic solutions across senior living communities in North America. The initiative focuses on integrating AI-powered service robotics, autonomous floor care systems, and physical AI programs to improve operational efficiency, reduce labor dependency, and enhance resident experiences, thereby supporting the sustained expansion of the humanoid robot industry.

Humanoid Robot Market Report Scope

Report Attribute

Details

Market size in 2025

USD 2.4 billion

Estimated market size in 2026

USD 4.2 billion

Projected market size by 2033

USD 40.5 billion

Growth rate

CAGR of 38.2% from 2026 to 2033

Base year for estimation

2025

Historical data

2021 - 2024

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion, volume in thousand units, and CAGR from 2026 to 2033

Report coverage

Revenue forecast, volume forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Component, motion type, application, and region

Regional Scope

North America; Europe; Asia Pacific; Latin America; Middle East & Africa

Country scope

U.S.; Canada; Mexico; UK; Germany; France; Italy; Spain; China; Japan; India; South Korea; Australia; Brazil; Argentina; Saudi Arabia; UAE; South Africa

Key companies profiled

1X Technologies; Agility Robotics, LLC; Apptronik; Boston Dynamics; Engineered Arts Limited; Figure AI; Fourier Intelligence; Hanson Robotics Limited; Honda Motor Co., Ltd.; Kawada Robotics Corporation; Kepler Robotics (Hangzhou Kolin Electric Co., Ltd.); LimX Dynamics Inc.; NVIDIA Corporation; National Aeronautics and Space Administration (NASA); PAL Robotics S.L.; Promobot Corp.; Robo Garage Co., Ltd.; RobotEra; ROBOTIS Co., Ltd.; Samsung Electronics Co., Ltd.; Sanctuary Cognitive Systems Corporation; SoftBank Robotics Group Corp.; Tesla, Inc.; Toshiba; Toyota Motor Corporation; UBTECH Robotics Inc.; Unitree; WowWee Group Limited; Xiaomi; XPENG, Inc.

Customization scope

Free report customization (equivalent to up to 8 analyst’s working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet you exact research needs. Explore purchase options

Global Humanoid Robot Market Report Segmentation

This report forecasts revenue & volume growth at the global, regional, and country levels and provides an analysis of the latest technology trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global humanoid robot market report based on component, motion type, application, and region:

-

Component Outlook (Revenue, USD Million/Billion, 2021 - 2033)

-

Hardware

-

Software

-

-

Motion Type Outlook (Volume, Thousand Units; Revenue, USD Million/Billion, 2021 - 2033)

-

Biped

-

Wheel Drive

-

-

Application Outlook (Volume, Thousand Units; Revenue, USD Million/Billion, 2021 - 2033)

-

Manufacturing

-

Logistics & Warehousing

-

Healthcare

-

Retail & E-commerce

-

Hospitality

-

Education & Research

-

Defense & Security

-

Residential

-

Others

-

-

Regional Outlook (Volume, Thousand Units; Revenue, USD Million/Billion, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

Saudi Arabia

-

UAE

-

South Africa

-

-

Research Methodology

(a) Segment Definition

Segment - Component

Revenue capture definition

Hardware

Revenue is generated from physical components used in humanoid robots, including actuators, sensors, control systems, power units, robotic frames, and mobility systems. Monetization is driven by hardware sales, system integration, assembly, and deployment of humanoid robotic platforms across industrial and commercial environments.

Software

Revenue is derived from AI-driven software platforms enabling perception, decision-making, motion planning, and human-robot interaction in humanoid robots. Monetization includes licensing, subscriptions, embedded AI models, robotic operating systems, and integration with cloud and edge computing ecosystems.

Segment - Motion Type

Revenue capture definition

Biped

Revenue is generated from humanoid robots designed with two-legged locomotion systems that enable human-like movement in complex environments. Monetization is driven by advanced robotics hardware, AI-based motion control systems, and deployment in industrial, service, and research applications requiring human-centric mobility.

Wheel Drive

Revenue is derived from humanoid robots using wheeled mobility systems that provide stable, energy-efficient movement in structured environments. Monetization includes deployment in logistics, warehousing, retail, and controlled industrial settings where cost efficiency and operational stability are prioritized.

Segment - Industry Vertical

Revenue capture definition

Manufacturing

Revenue is generated from deployment of humanoid robots in industrial environments for tasks such as assembly, inspection, material handling, and production support. Monetization is driven by automation contracts, productivity enhancement solutions, and smart factory integration services.

Logistics & Warehousing

Revenue is derived from humanoid robots used for inventory management, sorting, picking, packing, and internal transportation of goods. Monetization includes warehouse automation systems, fleet deployment, and operational efficiency optimization solutions.

Healthcare

Revenue is generated from humanoid robots used in patient assistance, elderly care, rehabilitation support, and hospital service operations. Monetization is driven by healthcare automation solutions, caregiving services, and assistive robotics deployment.

Retail & E-commerce

Revenue is derived from humanoid robots used for customer assistance, in-store support, inventory management, and order fulfillment tasks. Monetization includes service automation, customer engagement solutions, and retail operational optimization systems.

Hospitality

Revenue is generated from humanoid robots used in hotels, restaurants, and tourism services for guest assistance, concierge services, and service delivery. Monetization is driven by customer experience enhancement and service automation solutions.

Education & Research

Revenue is derived from humanoid robots used in academic training, robotics research, AI experimentation, and skill development programs. Monetization includes educational robotics platforms, research collaborations, and institutional deployments.

Defense & Security

Revenue is generated from humanoid robots used in surveillance, reconnaissance, threat detection, and security operations. Monetization includes defense contracts, security automation systems, and autonomous monitoring solutions.

Residential

Revenue is derived from humanoid robots used in home assistance, companionship, elderly care, and domestic task automation. Monetization includes consumer robotics sales, subscription-based services, and smart home integration.

Others

Revenue is generated from emerging and niche applications of humanoid robots, such as entertainment, personal assistance, and experimental deployments, among others.

(b) Estimation Model

Layer No.

Layer Name

Key Question

Description

01

Humanoid Robot Demand Base Layer

What forms the demand base?

Identify the global demand for humanoid robots across key end-use sectors, including manufacturing, logistics & warehousing, healthcare, retail, hospitality, construction, defense, education, and domestic services. This layer establishes the total addressable market by assessing labor-intensive processes, automation requirements, workforce shortages, and tasks suitable for human-like robotic intervention.

02

Adoption & Deployment Penetration Layer

Where are humanoid robots being adopted?

Estimate the penetration of humanoid robots across industries, comparing pilot deployments, commercial-scale implementations, and future adoption potential. Assess adoption rates by geography, enterprise size, and application type, while evaluating factors such as labor economics, automation maturity, technological readiness, and return-on-investment considerations.

03

Operational Intensity Layer

How extensively are humanoid robots utilized?

Analyze average robot utilization rates, operating hours, fleet sizes, task complexity, autonomy levels, and human-robot collaboration requirements across industries. Operational intensity is influenced by workflow complexity, labor replacement potential, AI capabilities, environmental adaptability, safety requirements, and enterprise automation strategies.

04

Revenue Layer

How is market revenue generated?

Market revenue is generated through the sale, leasing, and deployment of humanoid robots, as well as recurring revenues from software subscriptions, AI platform licensing, maintenance contracts, system integration, training, fleet management, upgrades, and after-sales support services. Revenue streams are driven by demand from industrial enterprises, logistics providers, healthcare institutions, commercial facilities, government agencies, and consumer applications.

Delivered Customizations

This report has been delivered with the following In-depth customizations

Client Request

Customization Delivered

Value Adds

Humanoid Robot Market Adoption & Commercialization Trends

Conducted a comprehensive assessment of humanoid robot adoption across manufacturing, logistics & warehousing, healthcare, retail, hospitality, defense, construction, and domestic service sectors. The study evaluated key adoption drivers, labor substitution opportunities, human-robot collaboration requirements, deployment readiness, use-case maturity, and scalability potential across industrial and commercial environments.

Helps stakeholders identify high-growth adoption segments, prioritize investment areas, assess market readiness, and evaluate opportunities arising from workforce shortages, productivity improvement initiatives, and increasing automation demand.

Humanoid Robot Technology Landscape & Innovation Assessment

Evaluated advancements in AI-enabled autonomy, machine vision, sensor fusion, natural language processing, dexterous manipulation, mobility systems, edge computing, battery technologies, and embedded intelligence. Assessed technology maturity levels, development roadmaps, and emerging innovations shaping next-generation humanoid robot capabilities.

Enables stakeholders to understand technology evolution, identify disruptive innovations, benchmark technology leadership, and prioritize R&D investments aligned with future market requirements.

Competitive Benchmarking & Strategic Positioning Analysis

Analyzed leading humanoid robot manufacturers, robotics startups, AI technology providers, and system integrators. Assessed product portfolios, performance capabilities, pricing models, deployment strategies, partnership ecosystems, funding activities, and commercialization progress across global markets.

Supports strategic decision-making by identifying competitive advantages, market gaps, partnership opportunities, acquisition targets, and areas for differentiation in a rapidly evolving market landscape.

Frequently Asked Questions About This Report

The North America humanoid robot market dominated with a share of 43.4% in 2025.

The Asia Pacific is the fastest-growing region over the forecast period.

The manufacturing segment led with a 31.9% revenue share in 2025, while the residential segment is the fastest-growing segment.

The global humanoid robot market size was estimated at USD 2.4 billion in 2025 and is expected to reach USD 4.2 billion in 2026.

The global humanoid robot market is expected to grow at a compound annual growth rate of 38.2% from 2026 to 2033 to reach USD 40.5 billion by 2033.

The market growth is driven by the increasing adoption of AI-powered automation and intelligent robotics systems across industrial, healthcare, logistics, and service sectors, and rising demand for human-machine collaboration.

The biped segment led with a 71.6% revenue share in 2025, while wheel drive is the fastest-growing segment.

The hardware segment accounted for the largest market share of over 79.4% in 2025, driven by the increasing demand for advanced sensors, actuators, robotic mobility systems, AI processors, and high-performance power management components.

Some of the key players in the humanoid robot market are Tesla, Inc., Agility Robotics, LLC, Hanson Robotics Limited, Engineered Arts Limited, Honda Motor Co., Ltd., KAWADA Robotics Corporation, SoftBank Robotics Group Corp., UBTECH Robotics Inc., Figure AI, Toshiba Corporation.

About the Author(s)

Next Generation Technologies Research Team

Technology · Next Generation TechnologiesThis report was authored by the next generation technologies research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the next generation technologies segment of the technology industry. All findings are based on proprietary technology databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.