- Home

- »

- Advanced Interior Materials

- »

-

Indium Market Size, Share And Trends Report, 2026-2033GVR Report cover

![Indium Market (2026 - 2033)Report]()

Indium Market (2026 - 2033)

Size, Share & Trends Analysis Report By Application (Displays, Semiconductor Materials, Solders & Alloys, Electronics, Chemicals), By Region (North America, Europe, Asia Pacific, Latin America, MEA), And Segment Forecasts

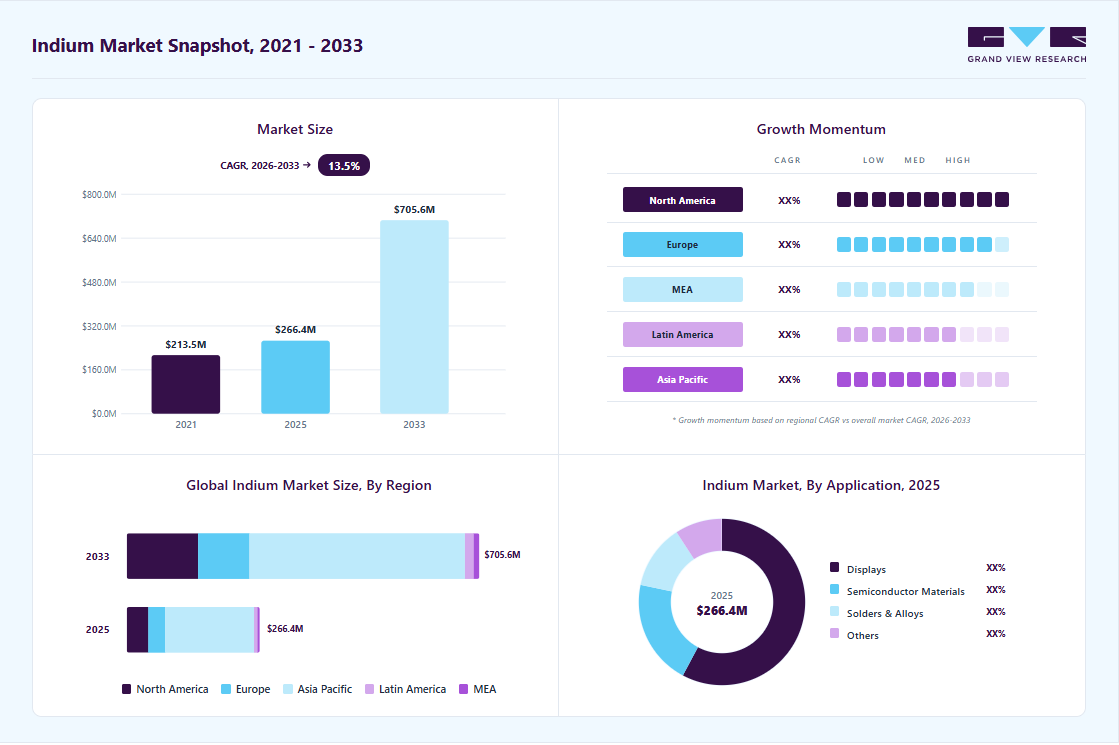

Market Size, 2025

$266.4MMarket Estimate, 2026

$291.4MMarket Forecast, 2033

$705.6MCAGR, 2026–2033

13.5%Indium Market Summary

The global indium market size was valued at USD 266.4 million in 2025 and is projected to grow from USD 291.4 million in 2026 to USD 705.6 million by 2033, at a CAGR of 13.5% from 2026 to 2033. The Asia Pacific held the largest share of 66.6% of the global market in 2025. The market growth is primarily driven by increasing demand from the electronics and semiconductor industries.

Key Market Trends & Insights

- By application, Displays segment is anticipated to register the largest market revenue share in 2025.

Regional Highlights

- Largest regional market: Asia Pacific (66.6% revenue share, 2025)

- Fastest-growing regional market: North America (highest CAGR, 2026-2033)

- By country: The China indium market led the Asia Pacific in 2025.

Market Size & Forecast

- Market size in 2025: USD 266.4 Million

- Estimated market size in 2026: USD 291.4 Million

- Projected market size by 2033: USD 705.6 Million

- CAGR (2026-2033): 13.5%

Indium is widely used in the production of indium tin oxide (ITO), a transparent conductive material essential for manufacturing touchscreens, flat panel displays, smartphones, tablets, and televisions. With the rapid expansion of consumer electronics and the growing penetration of advanced display technologies such as OLED and LCD panels, the demand for indium-based materials has increased significantly. The continuous innovation in display technologies and the rising adoption of smart devices worldwide are supporting the steady consumption of indium.Indium is a critical component in copper indium gallium selenide (CIGS) thin film solar cells, which are known for their high efficiency, flexibility, and ability to perform well under low light conditions. Governments across the world are promoting renewable energy deployment through incentives, carbon reduction policies, and investments in solar infrastructure. As solar power capacity continues to expand globally, the demand for indium used in thin-film photovoltaic technologies is expected to rise steadily.

")

The growing use of indium in the semiconductor and advanced electronics industries is another important factor contributing to market expansion. Indium compounds such as indium phosphide and indium arsenide are widely used in high-speed electronics, optoelectronics, and advanced communication devices. These materials are essential for manufacturing high-frequency transistors, laser diodes, photodetectors, and optical communication systems. The expansion of 5G infrastructure, high-speed data transmission networks, and next-generation communication technologies is expected to increase the consumption of indium-based semiconductor materials.

Indium is widely used in solders, thermal interface materials, and low-melting-point alloys due to its excellent thermal conductivity, ductility, and ability to form reliable seals. These properties make indium valuable in aerospace, defense, automotive electronics, and precision equipment manufacturing. As industries increasingly focus on miniaturization, thermal management, and high-performance electronic components, the demand for indium-based materials continues to expand.

Since indium is primarily obtained as a byproduct of zinc refining, its supply can be constrained by fluctuations in zinc production. To address supply challenges and meet growing demand, many companies are investing in advanced recycling technologies to recover indium from electronic waste, display panels, and manufacturing scrap. The development of efficient recycling processes is helping improve supply stability while supporting sustainable market growth.

Drivers, Opportunities & Restraints

The primary driver of the indium industry is the growing demand for consumer electronics and advanced display technologies. Indium is widely used in the production of ITO, which is a key material in touchscreens, liquid crystal displays, and flat panel televisions. The increasing adoption of smartphones, tablets, laptops, and smart wearable devices across the world is significantly boosting the demand for display panels. As manufacturers continue to introduce high-resolution and flexible displays, the requirement for indium-based materials is expected to grow steadily.

The development of next-generation electronics and communication technologies presents strong opportunities for the indium industry. Indium compounds such as indium phosphide are widely used in high-speed optoelectronic devices, fiber optic communication systems, and advanced semiconductor applications. The expansion of 5G networks, high-speed data transmission infrastructure, and data centers is expected to increase the demand for high-performance semiconductor materials, creating new opportunities for indium consumption in the coming years.

One of the major restraints in the indium industry is its limited primary supply and dependence on byproduct production. Since indium is mainly extracted during zinc processing, its availability is closely tied to the production levels of zinc rather than direct indium demand. This supply structure can lead to fluctuations in availability and pricing, which may affect industries that rely heavily on indium-based materials.

Application Insights

“Displays segment held the revenue share of over 57% in 2025.”

The displays segment represents the largest application of indium, primarily due to the extensive use of ITO in modern electronic display technologies. ITO is a transparent conductive material that allows electrical conductivity while maintaining high optical transparency, making it essential for devices such as LCDs, OLED screens, touch panels, televisions, laptops, and smartphones. This unique combination of conductivity and transparency enables the control of light and electrical signals within display panels, which is necessary for producing high-resolution images and responsive touch functionality.

Indium is widely used in semiconductor materials such as indium phosphide and indium gallium arsenide, which possess superior electrical and optical properties compared with conventional silicon in certain high-performance applications. These materials enable faster electron mobility, improved thermal stability, and efficient signal transmission, making them suitable for high-speed electronics, optoelectronic devices, and communication technologies. The rising deployment of fiber optic communication networks, high-frequency transistors, and photonic devices has significantly increased the demand for indium-based semiconductor materials across the global electronics industry.

Regional Insights

“Asia Pacific held over 66.6% revenue share of the global indium market.”

The Asia Pacific region represents the largest market for indium, primarily driven by its strong electronics manufacturing ecosystem. Countries such as China, Japan, South Korea, and Taiwan serve as major global hubs for the production of smartphones, flat panel displays, televisions, and other consumer electronic devices that rely heavily on indium tin oxide coatings for transparent conductive layers. The increasing production of LCD and OLED display panels, touchscreens, and advanced electronic devices has significantly boosted indium consumption across the region.

China Indium Market Trends

The indium market in China is largely driven by its dominant position in global electronics and display manufacturing. The country hosts a large number of flat panel display and consumer electronics manufacturers that rely heavily on indium tin oxide coatings for liquid crystal displays, touchscreens, and advanced display panels. China is a major production hub for televisions, smartphones, tablets, and laptops, all of which require transparent conductive materials made using indium. The continuous expansion of domestic electronics manufacturing, supported by strong export demand and large-scale industrial infrastructure, has significantly increased the consumption of indium in the country’s display and electronics sector.

North America Indium Market Trends

The indium market in North America is growing due to the strong presence of advanced electronics, semiconductor, and optoelectronics industries. Indium is widely used in semiconductor compounds such as indium phosphide and indium gallium arsenide that are essential for high-speed communication devices, laser diodes, and photodetectors. The region has a well-established semiconductor ecosystem supported by research institutions, technology companies, and integrated device manufacturers.

The U.S. indium market is primarily driven by the country’s strong semiconductor and advanced electronics industries. The U.S. is a major center for research, development, and production of high-performance electronic components that require indium-based semiconductor materials such as indium phosphide and indium gallium arsenide. These materials are widely used in high-speed communication devices, fiber optic networks, laser diodes, and photodetectors due to their superior electron mobility and optical efficiency.

Europe Indium Market Trends

The indium market in Europe is primarily driven by the region’s strong electronics, semiconductor, and advanced manufacturing sectors. Countries such as Germany, France, the Netherlands, and the United Kingdom are key hubs for semiconductor research, photonics technologies, and high-precision electronic component manufacturing. Indium-based semiconductor materials such as indium phosphide and indium gallium arsenide are widely used in optical communication devices, laser diodes, and photodetectors that support high-speed data transmission and telecommunications infrastructure.

Latin America Indium Market Trends

The indium market in Latin America is primarily driven by the gradual expansion of the electronics manufacturing and telecommunications sectors across the region. Countries such as Brazil and Mexico are emerging as important centers for consumer electronics assembly, automotive electronics production, and industrial equipment manufacturing. These industries require components such as displays, semiconductors, and optoelectronic devices that utilize indium-based materials, particularly indium tin oxide coatings used in touchscreens and display panels.

Key Indium Company Insights

Some of the key players operating in the market include AIM Solder and Avalon Advanced Materials Inc., among others.

-

AIM Solder is a global manufacturer of solder assembly materials for the electronics industry, with headquarters in Montreal, Canada, and manufacturing, distribution, and technical support facilities across North America, Europe, and Asia. The company focuses on developing advanced materials used in electronics manufacturing, including solder pastes, fluxes, and specialty alloys for applications in automotive electronics, LED lighting, aerospace, and telecommunications. AIM Solder provides a wide range of indium-based materials, including pure indium metal, indium alloys, indium solder preforms, wire, foils, and thermal interface materials.

-

Avalon Advanced Materials Inc. is a Canadian critical minerals development company headquartered in Toronto, Ontario. The company focuses on the exploration and development of rare metals and technology minerals that support advanced manufacturing, clean energy technologies, and electric vehicle supply chains. Avalon’s strategy centers on building sustainable and secure supply chains for high-value minerals such as lithium, rare earth elements, tantalum, and other specialty metals required for modern industrial applications.

Key Indium Companies:

The following key companies have been profiled for this study on the indium market.

- AIM Solder

- Avalon Advanced Materials Inc.

- ESPI Metals, Inc.

- Indium Corporation

- Lipmann Walton & Co Ltd

- Nippon Rare Metal, Inc.

- Nyrstar

- Teck Resources Limited

- Umicore

- Zhuzhou Keneng New Material Co., Ltd. Inc.

Recent Developments

- In March 2026, TNO and High Tech Campus Eindhoven launched construction of the world's first industrial factory for indium phosphide (InP) photonic chips on 6-inch wafers, a breakthrough in scalable photonics manufacturing.

Indium Market Report Scope

Report Attribute

Details

Market size in 2025

USD 266.4 million

Estimated market size in 2026

USD 291.4 million

Projected market size by 2033

USD 705.6 million

Growth rate

CAGR of 13.5% from 2026 to 2030

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative Units

Revenue in USD million/billion, volume in kilotons, and CAGR from 2026 to 2033

Report coverage

Revenue and volume forecast, company ranking, competitive landscape, flit factors, and trends

Segments covered

Application, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; China; India; Japan; Brazil; Saudi Arabia; South Africa

Key companies profiled

AIM Solder; ESPI Metals, Inc.; Avalon Advanced Materials Inc.; Indium Corporation; Lipmann Walton & Co Ltd.; Nippon Rare Metal, Inc.; Nyrstar; Teck Resources Limited; Umicore; Zhuzhou Keneng New Material Co., Ltd.

Customization scope

Free report customization (equivalent to up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Indium Market Report Segmentation

This report forecasts revenue and volume growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global indium market report based on application and region:

-

Application Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

Displays

-

Semiconductor Materials

-

Solders & Alloys

-

Others

-

-

Regional Outlook (Volume, Kilotons; Revenue, USD Million, 2021 - 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

-

Asia Pacific

-

China

-

India

-

Japan

-

-

Latin America

-

Brazil

-

-

Middle East & Africa

-

Saudi Arabia

-

South Africa

-

-

Frequently Asked Questions About This Report

the displays held the largest revenue share of 57.0% in 2025.

Key players include AIM Solder; ESPI Metals, Inc.; Avalon Advanced Materials Inc.; Indium Corporation; Lipmann Walton & Co Ltd.; Nippon Rare Metal, Inc.; Nyrstar; Teck Resources Limited; Umicore; Zhuzhou Keneng New Material Co., Ltd.

Key factors include increasing demand from the electronics and semiconductor industries.

The global indium market size was valued at USD 266.4 million in 2025 and is projected to grow from USD 291.4 million in 2026.

The global indium market is expected to grow at a CAGR of 13.5% from 2026 to 2033, reaching USD 705.6 million.

Asia Pacific dominated with a 66.6% revenue share in 2025.

North America is the fastest-growing region over the forecast period.

About the Author(s)

Advanced Interior Materials Research Team

Advanced Materials · Advanced Interior MaterialsThis report was authored by the advanced interior materials research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the advanced interior materials segment of the advanced materials industry. All findings are based on proprietary advanced materials databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.