- Home

- »

- Medical Devices

- »

-

Infection Control Market Size & Share Report, 2026-2033GVR Report cover

![Infection Control Market (2026 - 2033)Report]()

Infection Control Market (2026 - 2033)

Size, Share & Trends Analysis Report By Type (Equipment, Services, Consumables), By End-use (Hospitals, Medical Device Companies, Clinical Laboratories, Pharmaceutical Companies), By Region, And Segment Forecasts

Market Size, 2025

$55.3BMarket Estimate, 2026

$58.5BMarket Forecast, 2033

$90.0BCAGR, 2026–2033

6.4%Infection Control Market Summary

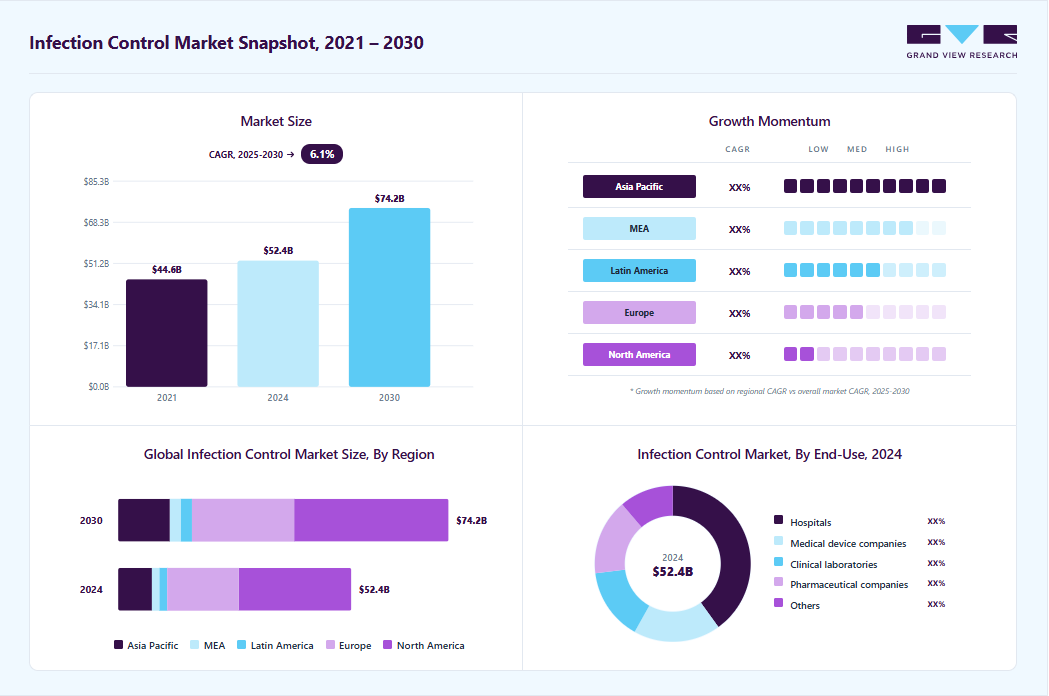

The global infection control market size was valued at USD 55.3 billion in 2025 and is projected to grow from USD 58.5 billion in 2026 to USD 90.0 billion by 2033, at a CAGR of 6.4% from 2026 to 2033. North America dominated the global market with the largest revenue share of 47.2% in 2025. The market is primarily driven by an increasing number of surgical & clinical procedures that require infection prevention.

Key Market Trends & Insights

- By type: Consumables segment led the market with the largest revenue share of 60.7% in 2025.

- By end-use: Hospital segment led the market with the largest revenue share of 40.3% in 2025.

Regional Highlights

- Largest regional market: North America (47.2% revenue share, 2025)

- Fastest-growing regional market: Asia Pacific (highest CAGR, 2026-2033)

- By country: The Infection control market in the U.S. held the largest share in the North America region in 2025.

Market Size & Forecast

- Market Size in 2025: USD 55.3 Billion

- Estimated Market Size in 2026: USD 58.5 Billion

- Projected Market Size by 2033: USD 90.0 Billion

- CAGR (2026-2033): 6.4%

Technological advancements in infection control have significantly enhanced the ability of healthcare providers to prevent and manage infections. Innovations such as automated disinfection systems, UV light technology, antimicrobial surface coatings, and advanced air filtration systems have demonstrated efficacy in reducing HAIs by up to 30% and is expected to contribute to the market growth. An increase in outsourcing sterilization services and the introduction of advanced sterilizing solutions are further contributing to the growth of the market for infection control. One of the important growth drivers is the increasing number of government initiatives to ensure highly intensive infection prevention. Government organizations are increasingly involved in issuing guidelines to promote awareness and efficient prevention measures globally, which is expected to contribute to market growth throughout the forecast period. For instance, the World Health Organization (WHO) has issued guidelines for preventing and controlling pandemic- and epidemic-prone acute respiratory diseases in healthcare. The guidelines range from standard precautions such as hand hygiene and usage of personal protective equipment to guidelines for disinfection and sterilization.")

According to the article published by the National Library of Medicine in May 2024, Acute respiratory infections (ARIs) are a major global health burden, leading to around 4.25 million deaths annually. These infections lead to millions of outpatient visits each year, particularly affecting high-risk groups such as the elderly, young children, and individuals with chronic conditions such as asthma or heart disease.

Diseases such as pneumonia and infections such as bloodstream, urinary tract, surgical site, and MRSA constitute most hospital-acquired infections. Other major healthcare-associated infections (HAIs) include catheter-associated urinary tract infections, ventilator-associated pneumonia, and catheter-related bloodstream. One of the utmost concerns for the market is HAIs, which affect patient recovery; thereby, mortality rates are being significantly impacted globally. According to an article by NIH in April 2023, HAIs are the most common adverse effects in hospitals, leading to serious health risks, increased morbidity and mortality, and higher costs for patients, families, and healthcare systems. HAIs affect about 3.2% of hospitalized patients in the U.S. and 6.5% in the EU, with global prevalence expected to be even higher. This facilitates the need for effective infection prevention and control solutions.

According to a practical guide published by the WHO on preventing hospital-acquired infections, the increase in hospitalization duration with surgical infections was approximately eight days. These prolonged stays are predicted to significantly contribute to the overall costs incurred during the hospitalization period, thus, raising the clinical urgency for adopting infection prevention measures. It is presumed that prolonged hospital stay is also not economical for the hospitals and healthcare payers due to excessive usage of resources to treat the acquired infection. These additional costs are majorly generated through increased usage of drugs, additional diagnostic studies, and laboratory equipment, creating a resource allocation imbalance.

Market Dynamics

The infection control market is experiencing steady growth due to the increasing focus on preventing healthcare-associated infections (HAIs), cross-contamination, and the spread of infectious diseases. Healthcare providers, pharmaceutical manufacturers, and other end users are investing in advanced infection prevention solutions to improve safety and maintain regulatory compliance. The market includes a wide range of products and services, such as sterilization and disinfection equipment, infectious waste management systems, personal protective equipment (PPE), disinfectants, safety-enhanced medical devices, and contract sterilization services. Rising awareness of infection prevention practices and growing concerns regarding patient safety are supporting market expansion. In addition, stringent regulatory standards and the increasing incidence of infectious diseases are driving demand for effective infection control measures. Continuous advancements in sterilization, decontamination, and monitoring technologies are further contributing to market growth during the forecast period.

The infection control market is being driven by the increasing prevalence of healthcare-associated infections (HAIs) and the growing emphasis on patient safety across healthcare settings. According to the U.S. Centers for Disease Control and Prevention (CDC) report published in 2026, approximately 1 in 31 hospitalized patients acquires at least one healthcare-associated infection on any given day, highlighting the significant burden of preventable infections. Common HAIs, including surgical site infections, bloodstream infections, and catheter-associated infections, contribute to prolonged hospital stays and higher treatment costs. As a result, healthcare providers are increasingly investing in sterilization, disinfection, and infection surveillance solutions to reduce infection risks and improve clinical outcomes. Furthermore, expanding healthcare infrastructure, stricter infection prevention regulations, and the growing adoption of advanced disinfection technologies are supporting the continued growth of the infection control market.

States

No. of catheter-associated urinary tract infections observed, 2024

Alabama

319

Alaska

28

Arizona

269

Arkansas

147

California

1,675

Colorado

184

Connecticut

124

D.C.

42

Delaware

44

Florida

808

Georgia

507

Guam

NA

Hawaii

71

Idaho

47

Illinois

549

Indiana

279

Iowa

130

Kansas

82

Kentucky

281

Louisiana

240

Maine

85

Maryland

283

Massachusetts

407

Michigan

416

Minnesota

281

Mississippi

170

Missouri

399

Montana

34

Nebraska

68

Nevada

93

New Hampshire

94

New Jersey

383

New Mexico

98

New York

1,043

North Carolina

538

North Dakota

29

Ohio

633

Oklahoma

157

Oregon

225

Pennsylvania

1,000

Puerto Rico

194

Rhode Island

63

South Carolina

245

South Dakota

45

Tennessee

320

Texas

979

Utah

80

Vermont

40

Virgin Islands

NA

Virginia

280

Washington

422

West Virginia

155

Wisconsin

227

Wyoming

14

The infection control market faces challenges due to the high cost of advanced sterilization, disinfection, and infection monitoring systems. Healthcare facilities, particularly small and medium-sized hospitals, often face budget constraints when investing in sophisticated infection control equipment and infrastructure. In addition, expenses associated with regulatory compliance, equipment validation, staff training, and ongoing maintenance increase the overall cost of implementation. For instance, hospital-grade autoclaves can cost around USD 30,000 to USD 250,000 or more, while large pass-through systems can exceed USD 120,000. Such high upfront and ongoing costs can limit adoption, especially in resource-constrained healthcare settings. Furthermore, shortages of trained personnel and inconsistent adherence to infection control protocols in developing regions may reduce the effectiveness of infection prevention programs, thereby restraining market growth.

The infection control market is poised for significant growth, driven by the expanding adoption of infection prevention solutions across healthcare, life sciences, and industrial settings. Increasing investments in healthcare infrastructure, particularly in emerging economies, are boosting demand for sterilization equipment, disinfectants, personal protective equipment (PPE), and infection surveillance systems. Healthcare providers are also increasingly adopting automated and touchless disinfection technologies, such as UV-C systems, hydrogen peroxide vapor solutions, and robotic cleaning platforms, to improve operational efficiency and reduce healthcare-associated infections (HAIs).

Furthermore, the growing trend toward outsourcing sterilization and reprocessing services is creating recurring revenue opportunities for specialized service providers. The integration of digital infection surveillance platforms, AI-powered monitoring systems, and predictive analytics is enhancing real-time infection tracking and regulatory compliance. In addition, heightened focus on pandemic preparedness, biosecurity, and outbreak response capabilities is expected to sustain long-term demand for infection control products, services, and advanced monitoring technologies throughout the forecast period.Key Opportunities in the Market

Opportunity Area

Development / Example

Market Impact

Rising Demand from Ambulatory and Outpatient Care Settings

Ambulatory surgical centers, dental clinics, diagnostic laboratories, dialysis centers, and specialty clinics are increasing the use of sterilization equipment, disinfectants, PPE, and reprocessing consumables to meet infection prevention standards.

Expands infection control demand beyond hospitals and creates growth opportunities across smaller and mid-sized healthcare facilities.

Growth in Single-Use and Disposable Infection Control Products

Healthcare facilities are increasing the use of disposable drapes, gowns, masks, gloves, sterilization wraps, and procedure kits to reduce cross-contamination risk and simplify infection prevention workflows.

Supports recurring revenue for consumables manufacturers and increases demand for high-volume infection prevention products.

Focus on Endoscope and Instrument Reprocessing Compliance

Increasing use of endoscopy and minimally invasive procedures is driving demand for automated endoscope reprocessors, washer-disinfectors, sterilization indicators, and instrument tracking solutions.

Creates opportunities for companies offering specialized reprocessing equipment, consumables, validation tools, and maintenance services.

Sustainable Infection Control and Waste Management Solutions

Healthcare facilities are seeking safer disinfectants, improved waste segregation, recyclable packaging, and efficient medical waste treatment solutions to reduce environmental impact and disposal costs.

Supports demand for eco-friendly infection control products and helps service providers differentiate through sustainable waste management offerings.

Training, Audit, and Compliance Support Services

Hospitals and clinics require regular staff training, infection control audits, sterilization validation, and protocol reviews to maintain safety standards and reduce infection risks.

Creates service-based opportunities for infection control companies and supports long-term customer engagement beyond product sales.

Market Concentration & Characteristics

The market growth stage is high, and the market growth is accelerating. The industry is experiencing high innovation as the market players develop advanced innovations in infection control equipment essential for addressing growing challenges in healthcare environments. For instance, automated disinfection robots thoroughly clean high-touch areas within healthcare facilities. For instance, in March 2024, Seal Shield, a healthcare technology company, showcased Shyld AI at the HIMSS 2024 conference in Orlando, Florida.

The market is characterized by a moderate level of mergers and acquisitions (M&A). M&A is driven by factors such as expanding product portfolios and gaining market share. For instance, in August 2023, STERIS plc. acquired BD’s laparoscopic instrumentation, surgical instrumentation, and sterilization container assets. This acquisition is expected to strengthen, expand, and complement STERIS’s product offerings within the healthcare segment.

The impact of regulations is high on industry. Organizations such as the CDC, WHO, and local health authorities often develop these regulations. Each organization has different requirements, leading to inconsistencies in practice. For instance, the CDC outlines specific precautions for different types of infections, which may not always align with local regulations or practices, complicating adherence in healthcare facilities.

Analyst Perspective

The infection control market is growing due to the rising focus on patient safety, prevention of healthcare-associated infections, and proper sterilization and disinfection practices across healthcare facilities. Increasing surgical procedures, diagnostic testing, hospital admissions, and healthcare infrastructure expansion are also supporting demand for infection control products and services.

Demand is expected to remain strong for sterilization equipment, disinfectants, protective barriers, endoscope reprocessing systems, and medical waste management solutions. Companies that provide complete infection control support, including equipment, consumables, services, training, and compliance assistance, are expected to have a stronger position in the market.

In the coming years, infection control providers that help healthcare facilities maintain safety standards, reduce infection risks, and improve operational efficiency are likely to gain stronger customer relationships and better market growth opportunities.

Type Insights

Based on type, the consumables segment led the market with the largest revenue share of 60.7% in 2025. The dominant share captured by consumables is predicted to be a consequence of consistent usage and the short life cycle of these products. Consumables are being extensively incorporated in disinfection, sterilization, and other control procedures and are indispensable parts of the procedures mentioned above, accounting for a larger share.

Increasing hospital admission rate is expected to boost the demand for infection control as these patients contribute to the increasing medical waste, boosting the market growth over the forecast period. For instance, in August 2024, CloroxPro launched new plant-based Clorox EcoClean disinfecting wipes. Such innovations foster the development of environment-friendly products and solutions for waste disposal, fueling market growth.

The services segment is expected to grow at the fastest CAGR of 8.6% during the forecast period. This rapid growth is attributed to the high inclination of market players to reduce overall healthcare expenditure and the utilization of benefits involved. It primarily includes cost advantages, increased efficiency of services, enhanced productivity, and a significantly higher focus on the core areas of development, which are critical to a company’s overall profit and growth. The organizations also strive to promote the adoption through issuing guidelines and recommendations for selection, risk assessment, rational usage, removal, and considerations to reduce the risk of transmission of respiratory pathogens to healthcare workers and other medical staff within a healthcare facility. Furthermore, services are segmented into contract sterilization and infectious waste disposal. The contract sterilization segment is again classified into ethylene oxide sterilization, e-beam sterilization, gamma sterilization, and others.

End Use Insights

Based on end-use, the hospital segment led the market with the largest revenue share of 40.3% in 2025 and is also expected to grow at the fastest CAGR over the forecast period from 2026 to 2033. The considerable share is mainly a result of the high probability of getting infected on hospital premises by transmitting blood-borne or respiratory pathogens. Hospital-acquired infections require rigorous control as it is one of the major challenges faced by the market. This has urged public health organizations and hospitals to adopt highly effective control systems. Also, as per research published in NCBI, 40% to 60% of hospital infections were estimated to be at surgical sites.

One of the major concerns is the high probability of infection from pathogens such as drug-resistance, blood-borne, and others in the operating room, because of which the need of the market is growing. For instance, frequent usage of urinary catheters poses a high probability of UTIs and may result in catheter-associated (CA)-UTIs. According to data published by the National Center for Biotechnology Information (NCBI), Urinary tract infections (UTIs) are among the most common bacterial infections in women, making up about 25% of all infections. More than half of all women around 50-60% are likely to experience a UTI in their lives. This high prevalence highlights a strong demand for effective treatments and prevention solutions for such infections. These factors are expected to widen the future growth prospects of the market.

The medical devices companies’ segment is expected to witness significant growth over the forecast period. Companies such as Medtronic, manufacture a range of single-use medical devices designed to reduce the risk of cross-contamination between patients. These products are typically packaged with sterile barriers and undergo terminal sterilization before being delivered to healthcare facilities.

Regional Insights

North America dominated the infection control market with the largest revenue share of 47.2% in 2025. This is owing to the increasing incidence of hospital-and laboratory-acquired infections. In addition, technological advancements and the local presence of prominent players adopting expansion strategies, such as investment and R&D in infection control equipment, acquisitions, expansions, and new product launches, are expected to fuel the market. Moreover, increasing government support through initiatives and policies encourages end users to adopt advanced and compliant infection control equipment and services.

U.S. Infection Control Market Trends

The Infection control market in the U.S. held the largest share in the North America region in 2025. The U.S. infection control industry is growing due to the high costs and health risks of infections acquired in healthcare settings, known as HAIs, and the rising problem of antibiotic-resistant germs. The government supports infection prevention through strong policies, guidelines, and funding to encourage the use of proven infection control products and practices. The U.S. market is also expected to grow due to increasing incidence of laboratory-acquired infections and the growing availability of technologically advanced control devices. Elsevier Ltd.’s study, “Laboratory-acquired infections and pathogen escapes worldwide between 2000 and 2021: a scoping review,” published in December 2023, highlighted that 309 individuals were affected by laboratory-acquired infections from 2000 to 2021. Of the total infections, around 78.6% of individuals were from North America

Europe Infection Control Market Trends

Europe infection control market held a substantial share in 2024. According to a report by the European Centre for Disease Prevention and Control (ECDC) in May 2024, each year, approximately 4.3 million patients in hospitals across the EU/EEA acquire at least one healthcare-associated infection (HAI), highlighting a significant challenge to patient safety.

Germany infection control market dominated the Europe market with the largest revenue share in 2024, due to the growing incidence of HAIs owing to the rising number of surgeries & hospital admissions in Germany. According to an article published by the Robert Koch Institute (RKI) in February 2024, an estimated 400,000 to 600,000 patients experience HAI annually, resulting in approximately 10,000 to 20,000 fatalities. Furthermore, increasing government support through programs and initiatives encourages healthcare end users to adopt infection control equipment and services.

Asia Pacific Infection Control Market Trends

Asia Pacific is expected to expand at the fastest CAGR of 7.4% over the forecast period from 2026 to 2033, owing to the growing number of outsourcing organizations, growing expenditure on healthcare, and evolving healthcare standards and infrastructure unprecedentedly across this region. Government organizations are focusing more on improving infection control standards, as it is also one of the important factors contributing to the growth of the Asia Pacific region.

China's infection control market held the largest share in 2024, owing to the increasing number of laboratory-acquired infections in the country, which is expected to improve the demand for technologically advanced infection control devices. Some of the notable players operating in the market are Shinva Medical Instrument Co., Ltd.; Galbino Technology Inc.; and Belimed. These players are investing in clinical trials and partnerships to develop technologically advanced products.

The India infection control market is expected to witness significant growth over the forecast period. This is attributed to factors such as inadequate hygiene standards and hospitals witnessing substantially increased patient volumes.

Key Infection Control Company Insights

The competition is marked by the extensive implementation of collaborative strategies by major companies such as Advanced Sterilization Products, STERIS, and 3M, which accounts for their dominant market share. These players are highly focused on adopting competitive strategies such as mergers and acquisitions, new product development initiatives, and geographical expansion.

-

STERIS Life Sciences offers a comprehensive range of infection control solutions, including sterilization equipment, disinfectants, and cleanroom products, designed to help pharmaceutical and biotechnology companies maintain sterile environments and comply with global regulatory standards.

-

Belimed provides a comprehensive range of infection control solutions, including washer-disinfectors, steam sterilizers, and ultrasonic washers, designed to ensure the safe and efficient reprocessing of medical instruments in healthcare facilities.

Key Infection Control Companies:

The following are the leading companies in the infection control market. These companies collectively hold the largest market share and dictate industry trends.

- 3M

- Belimed AG

- O&M Halyard or its affiliates.

- GETINGE AB (publ) Corporate

- ASP

- MATACHANA

- Sterigenics U.S., LLC - A Sotera Health company

- MMM Group

- Medivators Inc.

- STERIS.

- Midmark Corporation.

- W&H

Competitive Benchmarking

Category

Operating Strategies

Competitive Edge

Weakness

Established Players (e.g., STERIS plc, Getinge AB, 3M, ASP, Sterigenics U.S. LLC – A Sotera Health company, O&M Halyard or its affiliates)

- Expand global infection control portfolios through sterilization equipment, disinfection systems, consumables, protective barriers, outsourced sterilization services, and hospital infection prevention solutions. Focus on long-term contracts with hospitals, medical device manufacturers, pharmaceutical companies, and life sciences facilities. Invest in product innovation, regulatory-compliant sterilization processes, service contracts, and integrated infection control solutions

- Strong global brand recognition, broad product portfolios, established customer relationships, and strong regulatory expertise. Ability to provide end-to-end infection control solutions across sterilization, disinfection, protective barriers, consumables, and services. Large-scale operations also support wider geographic reach, reliable supply chains, and recurring revenue from consumables and service contracts..

- High dependence on regulatory compliance, complex operations, and hospital procurement cycles. Larger players may face pricing pressure from healthcare systems, high operating costs, and slower flexibility in serving customized local requirements. Some product categories also face competition from private-label and regional suppliers..

Emerging Players (e.g., Belimed AG, MATACHANA, MMM Group, Midmark Corporation, Cantel Medical Corp. / Medivators Inc., W&H)

- Focus on specialized infection control solutions such as washer-disinfectors, sterilizers, endoscope reprocessing systems, dental sterilization equipment, CSSD workflow solutions, and facility-specific reprocessing technologies. Strengthen market presence through distributor partnerships, hospital tenders, equipment upgrades, after-sales service, training, and customized infection control support for hospitals, clinics, dental centers, and diagnostic facilities.

- Strong technical expertise in niche infection control applications and ability to address specific facility-level sterilization and reprocessing needs. Greater flexibility in product customization, service support, and regional market expansion. Strong positioning in selected categories such as endoscope reprocessing, dental sterilization, CSSD equipment, and washer-disinfection systems.

- Relatively narrower product portfolios compared to large diversified players. Higher dependence on capital equipment replacement cycles, tender-based sales, and distributor networks. Limited scale may restrict geographic expansion, marketing reach, and ability to compete on bundled contracts against larger global infection control companies. quality and regulatory compliance.

Recent Developments

-

In July 2024, Midmark Corporation launched its next-generation M11 and M9 steam sterilizers, designed for enhanced durability and ease of use. These sterilizers feature integrated capabilities to improve instrument processing and compliance documentation efficiencies.

-

In January 2023, W&H Dentalwerk launched the Lexa Plus sterilizer, a pre-vacuum, Class B sterilizer designed for the North American market.

-

In March 2023, Getinge, a Swedish medical technology company, acquired Ultra Clean Systems Inc. to expand its ultrasonic cleaning technology portfolio for surgical instruments, especially for complex and robotic surgery tools.

Infection Control Market Report Scope

Report Attribute

Details

Market size value in 2025

USD 55.3 billion

Estimated Market Size in 2026

USD 58.5 billion

Projected Market Size by 2033

USD 90.0 billion

Growth rate

CAGR of 6.3% from 2026 to 2033

Historical data

2021 - 2025

Forecast period

2026 - 2033

Quantitative units

Revenue in USD million/billion and CAGR from 2026 to 2033

Report coverage

Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Segments covered

Type, end-use, region

Regional scope

North America; Europe; Asia Pacific; Latin America; MEA

Country scope

U.S.; Canada; Mexico; Germany; UK; France; Italy; Spain; Norway; Denmark; Sweden; China; Japan; India; South Korea; Australia; Thailand; Brazil; Argentina; Saudi Arabia; South Africa; UAE; Kuwait

Key companies profiled

Getinge AB, 3M, Belimed AG, O&M Halyard or its Affiliates, Midmark Corporation, ASP, MATACHANA, Sterigenics U.S., LLC – A Sotera Health company, MMM Group, Cantel Medical Corp. (Medivators Inc.), STERIS plc., W&H

Customization scope

Free report customization (equivalent up to 8 analysts' working days) with purchasse. Addition or alteration to country, regional & segment scope.

Pricing and purchase options

Avail customized purchase options to meet your exact research needs. Explore purchase options

Global Infection Control Market Report Segmentation

This report forecasts revenue growth and provides an analysis of the latest trends in each of the sub-segments from 2021 to 2033. For the purpose of this report, Grand View Research has segmented the global infection control market on the basis of type, end use, and region:

-

Type Outlook (Revenue, USD Billion, 2021- 2033)

-

Equipment

-

Disinfectors

-

Washers

-

Flushes

-

Endoscope Reprocessors

-

-

Sterilization Equipment

-

Heat Sterilization Equipment

-

Low Temperature Sterilization Equipment

-

Radiation Sterilization Equipment

-

Filtration Sterilization Equipment

-

Liquid Sterilization Equipment

-

-

Others

-

-

Services

-

Contract Sterilization

-

Ethylene Oxide Sterilization

-

E-beam Sterilization

-

Gamma Sterilization

-

Others

-

-

Infectious Waste Disposal

-

-

Consumables

-

Infectious Waste Disposal

-

Disinfectants

-

Sterilization Consumables

-

Safety enhanced medical devices

-

Personal Protective Equipment

-

Others

-

-

-

End Use Outlook (Revenue, USD Billion, 2021- 2033)

-

Hospitals

-

Medical Device Companies

-

Clinical Laboratories

-

Pharmaceutical Laboratories

-

Others

-

-

Regional Outlook (Revenue, USD Billion, 2021- 2033)

-

North America

-

U.S.

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

Denmark

-

Sweden

-

Norway

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

Thailand

-

-

Latin America

-

Brazil

-

Argentina

-

-

Middle East & Africa

-

South Africa

-

Saudi Arabia

-

UAE

-

Kuwait

-

-

Research Methodology

Segment Definition

Segment-Equipment

Revenue capture definition

Equipment

This segment comprises disinfectors, sterilization equipment, and other infection control equipment. They are extensively used in healthcare settings, medical device manufacturers, & pharmaceutical companies to avoid cross-contamination and curb infection

Disinfectors

Automated or manual systems designed to eliminate or reduce pathogenic microorganisms on medical devices, instruments, surfaces, and healthcare equipment through chemical or thermal disinfection processes, supporting infection prevention and patient safety.

Washers

Equipment used for the cleaning and decontamination of reusable medical instruments and devices by removing organic debris, blood, and contaminants prior to disinfection or sterilization, ensuring compliance with infection control standards.

Flushes

Flushing systems are used to rinse and purge internal channels of reusable medical devices, such as endoscopes and surgical instruments, during the cleaning and reprocessing process. These systems help remove residual debris and contaminants before disinfection or sterilization

Endoscope Reprocessors

Automated endoscope reprocessing systems that clean, disinfect, and prepare flexible endoscopes for safe reuse, ensuring adherence to stringent infection prevention and regulatory requirements.

Sterilization Equipment

Devices and systems designed to completely eliminate all forms of microbial life, including bacterial spores, from medical instruments, devices, and healthcare products, forming a critical component of infection control programs.

Heat Sterilization Equipment

Sterilization systems that utilize saturated steam, dry heat, or other thermal methods to destroy microorganisms on heat-resistant medical devices and instruments, widely used in hospitals and healthcare facilities.

Low Temperature Sterilization Equipment

Sterilization technologies employing agents such as hydrogen peroxide vapor, gas plasma, or ethylene oxide to sterilize heat- and moisture-sensitive medical devices while maintaining device integrity and infection prevention efficacy.

Radiation Sterilization Equipment

Sterilization systems that use ionizing radiation, such as gamma rays, electron beams, or X-rays, to achieve microbial inactivation in medical devices, pharmaceuticals, and healthcare products without the use of heat.

Filtration Sterilization Equipment

Sterilization solutions that remove microorganisms and particulate contaminants from liquids, gases, or air streams through specialized filtration membranes, commonly used in pharmaceutical, laboratory, and healthcare settings.

Liquid Sterilization Equipment

Systems designed to sterilize liquids, solutions, and fluid-based medical products using thermal, chemical, or filtration-based processes to ensure microbiological safety and regulatory compliance.

Others

Includes emerging and specialized infection control equipment, such as UV-C disinfection systems, ozone-based disinfection equipment, automated room decontamination systems, and other advanced decontamination platforms used across healthcare and life sciences settings.

Segment- Services

Revenue capture definition

Services

This segment includes contract sterilization and infectious waste disposal services. Its end users include hospitals, clinics, pharmaceutical & medical device companies, and other healthcare settings.

Contract Sterilization

Outsourced sterilization services provided by specialized vendors that sterilize medical devices, pharmaceuticals, and healthcare products on behalf of manufacturers, ensuring regulatory compliance and product safety.

Ethylene Oxide (EtO) Sterilization

Ethylene oxide sterilization refers to outsourced sterilization services that use EtO gas to sterilize heat- and moisture-sensitive medical devices and healthcare products. It is widely used for products that cannot tolerate high-temperature sterilization.

E-beam Sterilization

Sterilization services employing electron beam radiation to rapidly deactivate microorganisms in medical devices, pharmaceutical packaging, and healthcare products without the use of heat or chemicals.

Gamma Sterilization

Sterilization services that use gamma radiation to achieve terminal sterilization of medical devices, biologics, and healthcare products, ensuring product sterility and extended shelf life.

Others (Sterilization Services)

Includes alternative sterilization methods and specialized service offerings such as X-ray sterilization, vaporized hydrogen peroxide sterilization, ozone sterilization, and customized decontamination solutions.

Infectious Waste Disposal (Services)

Collection, transportation, treatment, and disposal services for infectious and biohazardous healthcare waste, designed to minimize environmental contamination and prevent disease transmission.

Segments- Consumables

Revenue capture definition

Consumables

This category includes materials required for sterilization, disinfection, and for the process of infectious waste disposal.

Infectious Waste Disposal Consumables

Disposable products such as biohazard bags, sharps containers, waste collection bins, and containment materials used for the safe handling, segregation, and disposal of infectious waste.

Disinfectants

Disinfectants are chemical agents used to eliminate or inactivate pathogenic microorganisms on inanimate surfaces, medical devices, equipment, and environmental areas. Products used on skin are generally classified as antiseptics, not disinfectants.

Sterilization Consumables

Products used during sterilization processes, including sterilization wraps, pouches, indicators, biological monitoring systems, packaging materials, and chemical integrators that ensure sterility assurance.

Safety-Enhanced Medical Devices

Medical devices engineered with integrated safety mechanisms, such as needle protection systems and sharps injury prevention features, designed to reduce occupational exposure to infectious agents.

Personal Protective Equipment (PPE)

Protective garments and equipment, including gloves, masks, respirators, gowns, face shields, and protective eyewear, used to minimize exposure to infectious pathogens and healthcare-associated risks.

Others (Consumables)

Includes specialized infection control consumables such as antimicrobial coatings, hand hygiene products, surface protection materials, and emerging contamination prevention solutions.

Segments- End Use

Revenue capture definition

Hospitals

Hospitals are the largest end users of infection control products and services. They use sterilization equipment, disinfectants, PPE, reprocessing systems, infectious waste disposal solutions, and related consumables to prevent healthcare-associated infections, maintain patient safety, and comply with infection prevention standards across operating rooms, ICUs, wards, laboratories, and CSSD units.

Medical Device Companies

Medical device companies use infection control solutions for sterilizing, disinfecting, packaging, and validating medical devices before commercial distribution. These companies often rely on in-house or contract sterilization services such as ethylene oxide, gamma, e-beam, and other sterilization methods to ensure product safety and regulatory compliance.

Clinical Laboratories

Clinical laboratories use infection control products to prevent contamination during sample collection, testing, storage, and disposal. This includes disinfectants, PPE, biosafety supplies, sterilization consumables, and infectious waste management solutions used to protect laboratory staff and maintain safe testing environments.

Pharmaceutical Companies

Pharmaceutical companies use infection control solutions to maintain sterile manufacturing environments, prevent microbial contamination, and comply with quality and regulatory requirements. Key applications include cleanroom disinfection, sterilization of equipment and materials, contamination control, and safe disposal of biohazardous waste.

Others

Others include ambulatory surgical centers, dental clinics, long-term care facilities, dialysis centers, research institutes, biotechnology companies, and other healthcare or life sciences facilities. These users adopt infection control products and services to support safe procedures, reduce infection risks, and maintain hygiene and compliance standards.

Estimation Model

Model Details

This research methodology outlines the process for estimating the size of the global infection control market for the period from 2021 to 2033. The study covers key infection control products, equipment, consumables, and services used across hospitals, clinics, ambulatory surgical centers, diagnostic laboratories, pharmaceutical and biotechnology facilities, long-term care facilities, and other healthcare settings.

The infection control market includes sterilization products, cleaning and disinfection products, protective barriers, infectious waste management solutions, infection control services, and related consumables. The objective is to develop a robust and defensible market estimate through a bottom-up and usage-based calculation approach, supported by primary industry validation.

A triangulated market sizing approach was used, combining:

-

Hospital bed and infectious waste generation-based analysis

-

Healthcare facility-based infection control spending analysis

-

Product and consumables utilization analysis

-

Procedure and sterilization cycle-based analysis

-

Primary research validation with industry stakeholders

Step-By-Step Market Estimation Process

Hospital Bed & Infectious Waste-Based Market Model

This model estimates the infection control market by calculating infectious waste generation across healthcare facilities and the associated treatment, handling, and disposal cost.

-

Step 1: Country-level population data for 2021–2025 was collected from international statistical databases and national statistical agencies.

-

Step 2: Hospital beds per person were identified using healthcare infrastructure data, hospital statistics, and country-level healthcare databases.

-

Step 3: The total number of hospital beds was calculated by multiplying the country-level population by hospital beds per person.

-

Step 4: Average medical waste generated per hospital bed per day was applied to estimate total annual medical waste generation.

-

Step 5: The infectious waste share was applied to estimate the portion of total medical waste classified as infectious, hazardous, or requiring controlled treatment.

-

Step 6: Infectious waste volume was multiplied by the average cost of infectious waste treatment, collection, handling, transportation, or disposal.

-

Step 7: Country-level estimates were aggregated to regional and global levels.

Healthcare Facility-Based Infection Control Spending Model

This model estimates infection control spending across different healthcare and life sciences facilities.

-

Step 1: The number of facilities by country was identified using hospital databases, government health statistics, licensing records, healthcare directories, and proprietary databases.

-

Step 2: Facilities were classified into hospitals, clinics, ambulatory surgical centers, diagnostic laboratories, long-term care facilities, pharmaceutical facilities, biotechnology facilities, and other healthcare settings.

-

Step 3: Average annual infection control spending per facility was estimated based on facility size, patient volume, bed capacity, procedure intensity, sterilization requirements, and procurement benchmarks.

-

Step 4: Spending was mapped across key infection control categories, including sterilization products, disinfectants, cleaning supplies, protective barriers, waste management, and outsourced infection control services.

-

Step 5: Country-level market size was calculated by multiplying the number of facilities by average annual infection control spending per facility.

-

Step 6: Facility-level estimates were aggregated to generate regional and global market values.

Segment-Level Market Allocation

After deriving the total infection control market size, the market was split across key segments using facility-level spending, product consumption patterns, procedure volumes, procurement benchmarks, and company revenue mapping.

Primary Research Validation

Primary interviews were conducted to validate the assumptions used in the market sizing model. Respondents included hospital procurement managers, infection control officers, CSSD managers, waste management service providers, distributors, manufacturers, and healthcare facility administrators.

-

The interviews were used to validate:

-

Average infection control spending per facility

-

Medical and infectious waste generation assumptions

-

Sterilization and disinfection product usage

-

Average cost per sterilization / disinfection cycle

-

Product pricing and procurement patterns

-

Public-private facility differences

-

Regional adoption of advanced infection control products

-

Market growth drivers and forecast assumptions.

Final Market Triangulation

The final global infection control market size was derived through triangulation of the following bottom-up and usage-based models:

-

Hospital Bed & Infectious Waste-Based Market Model

-

Healthcare Facility-Based Infection Control Spending Model

-

Product & Consumables Utilization Model

-

Procedure & Sterilization Cycle-Based Model

-

Primary Research Validation

The weighted output from these models was used to generate the final historical estimates for 2021–2025 and forecast projections for 2026–2033.

Final estimates were adjusted for hospital infrastructure expansion, procedure volume growth, infectious waste generation, sterilization demand, disinfection frequency, regulatory compliance intensity, infection prevention protocols, product pricing trends, and adoption of advanced sterilization and disinfection technologies.

Delivered Customizations

This report has been delivered with the following In-depth customizations

CLIENT REQUEST

CUSTOMIZATION DELIVERED

VALUE ADDS

Technological Advancements Analysis

Conducted a comprehensive technology assessment of the nuclear imaging equipment market, focusing on advancements in PET, SPECT, PET/CT, SPECT/CT, and PET/MRI systems. The analysis evaluated emerging trends such as artificial intelligence (AI)-enabled image reconstruction, digital detector technologies, low-dose imaging solutions, automated workflow platforms, and theranostics-driven imaging applications. It further assessed the impact of these innovations on diagnostic accuracy, scan efficiency, patient outcomes, and healthcare provider adoption. Additionally, the study reviewed ongoing R&D activities, product launches, regulatory developments, and investments in next-generation molecular imaging technologies across major global markets.

This analysis enables stakeholders to understand evolving technology trends shaping the nuclear imaging equipment industry. It helps identify high-growth innovation areas, emerging competitive advantages, and future investment opportunities. The findings support product development, strategic planning, technology adoption decisions, and long-term market positioning across the diagnostic imaging ecosystem.

Competitive Analysis

Conducted a detailed competitive assessment of leading nuclear imaging equipment manufacturers based on product portfolios, modality offerings, technological capabilities, pricing strategies, geographic presence, service networks, strategic partnerships, and recent product innovations. The analysis examined competitive positioning across PET, SPECT, and hybrid imaging segments while evaluating key differentiators such as AI integration, image quality, workflow efficiency, and after-sales support. It also assessed mergers, acquisitions, collaborations, and expansion initiatives influencing market dynamics.

This analysis enables stakeholders to evaluate competitive intensity, benchmark key market participants, and identify growth opportunities within the nuclear imaging equipment market. It supports strategic decision-making related to product differentiation, partnership development, market entry planning, and competitive positioning across developed and emerging healthcare markets.

Geographic Expansion

Conducted a detailed assessment of regional and country-level opportunities within the nuclear imaging equipment market across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The analysis evaluated healthcare infrastructure, diagnostic imaging adoption rates, availability of radiopharmaceuticals, reimbursement frameworks, regulatory environments, disease prevalence, and investments in precision medicine initiatives. It further assessed country-specific demand drivers, installation trends, healthcare spending patterns, and expansion opportunities for advanced nuclear imaging technologies.

This analysis enables stakeholders to understand regional growth potential and market attractiveness across key geographies. It helps identify high-opportunity countries for expansion, investment, and strategic partnerships while providing insights into healthcare infrastructure readiness, reimbursement landscapes, and long-term demand trends. The findings support informed geographic expansion and market penetration strategies within the global nuclear imaging equipment industry.

Frequently Asked Questions About This Report

The hospital segment led the market with the largest revenue share of 40.3% in 2025, and is the fastest-growing segment.

The global infection control market size was estimated at USD 55.3 billion in 2025 and is expected to reach USD 58.5 billion in 2026.

The global infection control market is projected to grow at a CAGR of 6.35% from 2026 to 2033, reaching USD 90.0 billion by 2033.

Some prominent players in the infection control market include 3M, Belimed Inc., O&M Halyards, Getinge, ASP (Advanced Sterilization Products Services, Inc.), Sterigenics U.S., LLC - A Sotera Health Company, MMM Group, Midmark Corporation, STERIS, W&H, Metrex Research, LLC., MATACHANA GROUP

The infection control market is experiencing steady growth driven by increased focus on preventing healthcare-associated infections (HAIs), cross-contamination, and the spread of infectious diseases. Healthcare providers, pharmaceutical manufacturers, and other end users are investing in advanced infection prevention solutions to improve safety and maintain regulatory compliance.

North America dominated the infection control market with the largest revenue share of 47.2% in 2025

Based on type, consumables segment led the market with the largest revenue share of 60.7% in 2025. The increasing demand for infection control consumables can be attributed to the rising number of hospitals in developing countries, the increasing patient population, the rising volume of diagnostic & lab testing samples, and the growing awareness of the benefits of hospital waste management in curbing the spread of infection. The increasing hospital admission rate is anticipated to increase medical waste, boosting the market over the forecast period. For instance, in August 2024, CloroxPro launched new plant-based Clorox EcoClean disinfecting wipes. Such innovations foster the development of environment-friendly products and solutions for waste disposal, fueling market growth.

About the Author(s)

Medical Devices Research Team

Healthcare · Medical DevicesThis report was authored by the medical devices research team at Grand View Research - comprising two research analysts, one senior research analyst, and one industry expert - with specialized expertise in the medical devices segment of the healthcare industry. All findings are based on proprietary healthcare databases, executive interviews, and regulatory analysis, subject to internal peer review prior to publication.

Last Updated:

Speak to Analyst

Need a Tailored Report?

Customize this report to your needs — add regions, segments, or data points, with 20% free customization.

Or view our licence options:

ISO 9001:2015 & 27001:2022 Certified

We are GDPR and CCPA compliant! Your transaction & personal information is safe and secure. For more details, please read our privacy policy.